Scotland's Fiscal Outlook: The Scottish Government's Medium-Term Financial Strategy

This is the fifth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament. This context will also frame the Resource Spending Review.

2. Scotland's Fiscal Outlook

2.1 How Scotland's fiscal outlook is determined

This chapter sets out the Scottish Government's expectations for its funding position over the next five years. It includes the assumptions that underpin the Scottish Government's central funding scenario, supporting resource spending plans for 2023-24 to 2026-27 as published in the accompanying RSR. It also includes the assumptions that support the funding envelope for capital, with the update to the CSR also published alongside this MTFS.

The Scottish Government's funding outlook is determined by combining forecasts and risk based assumptions from multiple sources, and is affected by decisions of both the UK and Scottish Governments. This results in a funding outlook with a high degree of uncertainty and volatility. The funding position described in this chapter is our view of a 'central' outlook, with some analysis of the downside and upside risks. As part of its remit, the SFC are tasked with independently assessing the reasonableness of our funding assumptions, and have independently confirmed that our central funding scenario is reasonable.

The remainder of this chapter describes:

- The aggregate funding outlook that informs the Scottish Government's spending plans;

- The anticipated outlook for each component of the Scottish Government's fiscal position;

- The assumptions underpinning the central outlook that supports the spending plans; and

- The risks and uncertainties associated with this central outlook.

The Scottish Government is committed to being open and transparent with the public on the risks to the funding outlook. We intend to replicate the structure of this chapter in future iterations of the MTFS, in order to allow readers to track how each component of our funding position evolves over time

2.2 Summary of Scotland's fiscal outlook

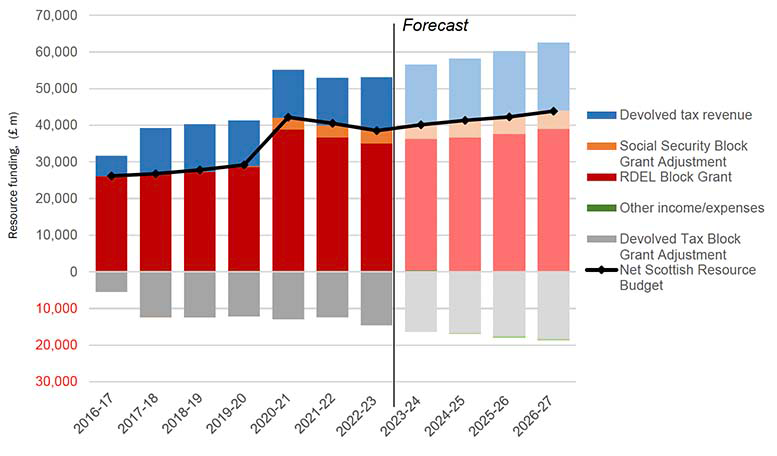

Table 2 below describes the anticipated resource funding position, broken into five high level categories, each discussed in detail in this chapter:

- The Block Grant – the single largest source of funding for the Scottish Government. It is determined by the Barnett Formula, based on the spending plans of the UK Government.

- Devolved taxes – the Scottish Government receives the revenue from these, the largest of which is Scottish Income Tax. However, the Budget is also reduced based on how quickly revenues of the corresponding tax have grown in rUK (adjusted for population).

- Non-domestic rates – this revenue is raised by Local Authorities from non-domestic rates. All revenue raised is ultimately returned to Local Government.

- Social Security Block Grant adjustments – this is revenue provided by the UK Government for devolved social security payments, based on the growth in expenditure on the corresponding payment in the rest of the UK.

- Other income and expenses – assorted revenue and costs that do not fit into one of the above categories.

Overall, we expect the funding available to the Scottish Government to grow steadily over the next four years, with slightly higher growth from 2025-26. Relative to 2022-23 levels, the funding envelope grows by 14% by 2026-27. In real terms the growth is only 5% in aggregate over the next 4 years, largely due to the growth in Block Grant not keeping pace with inflation. However, a significant part of this growth relates to the devolution of social security benefits and so is directly associated with similar demand-led increases in social security in Scotland. Stripping out this growth implies real terms growth of just 2% across the whole four year period.

| All figures in £million, current prices | Forecast | ||||

|---|---|---|---|---|---|

| Resource Funding | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

| Block Grant | 35,026 | 35,908 | 36,691 | 37,674 | 39,048 |

| Net tax position | -86 | -265 | 167 | 103 | -31 |

| Of which: | |||||

| Devolved tax revenue | 14,521 | 16,058 | 16,897 | 17,716 | 18,433 |

| Block Grant Adjustment | -14,607 | -16,324 | -16,730 | -17,612 | -18,464 |

| Non-domestic rates distributable amount | 2,766 | 3,190 | 3,134 | 3,323 | 3,651 |

| Social Security Block Grant Adjustment | 3,587 | 4,082 | 4,574 | 4,825 | 5,103 |

| Non-tax income & block grant adjustments | -8 | -9 | -8 | -8 | -8 |

| Other income/expenses | 549 | 416 | -119 | -317 | -265 |

| Total resource funding, inc NDR income | 41,836 | 43,321 | 44,439 | 45,600 | 47,498 |

Based on funding position as set at Budget 2022/23

Totals may not sum due to rounding

Looking over a longer time horizon, as shown in Figure 4 below, the forecast growth in the funding envelope is marginally below the growth seen in the years prior to COVID-19, at an average of 2.4% per annum (compared to 2.7% in the four years prior to 2019-20). However, as noted above, a large part of the persistent increase in the funding envelope from 2020-21 and into the future reflects the devolution of additional Social Security powers. These increase the funding via the Social Security BGA (in orange below), but are fully utilised by additional costs of the newly devolved benefits.

2.3 Components of Scotland's fiscal outlook

This section describes the source of our assumptions for each of the sources components of funding. This is summarised in Table 3.

| Funding Component | Source of Central funding assumption |

|---|---|

| Block Grant | October 2021 Spending Review Settlement[13], updated with March 2022 OBR forecasts and Scottish Government risk-based assumptions |

| Net tax position: | |

| Devolved tax revenue | May 2022 SFC forecasts |

| Block Grant Adjustment | March 2022 OBR forecasts |

| Social Security Block Grant Adjustment | March 2022 OBR forecasts |

| Other income | Risk-based judgement by Scottish Government. |

The approach to these funding assumptions has not changed substantially from that taken in the last MTFS published alongside the Scottish Budget in December 2021. However, some assumptions have been revisited in light of new policy announcements made by the UK Government, or the need to make longer-term judgments on the funding position to support the Resource Spending Review. Where there have been significant changes since the December MTFS, these are noted below.

2.4 Block Grant

The Block Grant is the amount of revenue funding that Scottish Government receives from the UK Government. It is determined by the Barnett formula, which is applied to the UK Government's spending decisions. Higher (or lower) UK Government spending on devolved policy areas results in more (or less) funding being available to the Scottish Government. The Block Grant is the largest single determinant of the Scottish Government's funding.

The UK Government's Autumn Budget in 2021 set out an expected funding Settlement for the Scottish Government, based on the UK Government's spending plans over the UK Spending Review period of 2022-23 to 2025-26.

This forms the starting point of the projected forecast Block Grant over the next five years. Three judgement-based adjustments have been applied to this outlook, shown in Table 4:

- As the UK Spending Review settlement only extends to 2024-25, an assumption for the Block Grant must be made beyond this point. This assumes that the Block Grant in future years grows at around 4% per annum, based on the OBR's March 2022 forecast of RDEL expenditure in these years;

- A small upward adjustment is made to the expected Block Grant received in the two remaining years of the UK Spending Review settlement. This is due to the historic tendency of the UK Government to exceed Spending Review settlements, discussed further below; and,

- Ring-fenced funding sources outside the usual Block Grant, such as the Rail Resource Grant and replacements for EU funding, remain fixed in nominal terms based on our current working assumptions.

| All figures in £million, current prices | Forecast | ||||

|---|---|---|---|---|---|

| Resource Funding | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

| RDEL Block Grant as at SR21 | 34,322 | 34,943 | 35,577 | N/A | N/A |

| Assumed Block Grant outside SR period | 36,959 | 38,333 | |||

| Assumed future consequentials | 250 | 400 | |||

| Non-Barnett ringfenced funding | 704 | 715 | 715 | 715 | 715 |

| Total RDEL block grant | 35,026 | 35,908 | 36,691 | 37,674 | 39,048 |

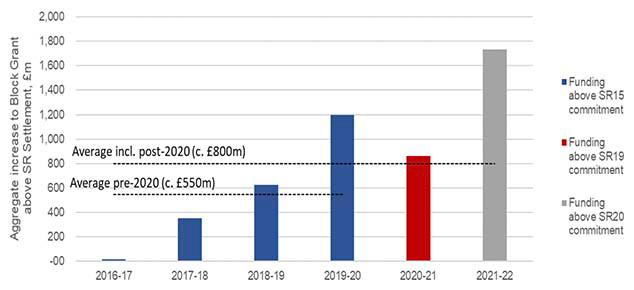

The assumption of future Barnett consequentials beyond the core Block Grant is based on analysis of historic data. Figure 5 shows the additional funding received by the Scottish Government via the Block Grant in addition to the original Spending Review settlements set in 2015, 2019 and 2020. As this shows, the UK Government's historic tendency has been to increase the available funding envelope at each Budget, with greater increases in future years of the Spending Review. While the years of the COVID-19 pandemic are clearly exceptional in the degree of spending increases seen, our assumptions are well within with the degree of additional spending increases seen over the Spending Review 2015 period.

Overall, we view these funding assumptions as reasonable and prudent. However, as the Scottish Government has no direct control over the UK Government's spending decisions, changes in UK Government policy present a high degree of risk to the funding outlook.

2.5 Net impact of devolved tax revenue & Block Grant Adjustments

The Scottish Government receives the revenue from partially and fully devolved taxes – namely Scottish Income Tax (SIT), Land and Building Transactions Tax (LBTT) and Scottish Landfill Tax (SLfT).

Each of these taxes has a corresponding 'Block Grant Adjustment' (BGA). This is the amount deducted from the Scottish Government's Block Grant based, in simple terms, on how much revenue the corresponding tax has grown in the rest of the UK since 2016-17.

The difference between these two figures determines the net impact of devolved tax on the Scottish Budget, otherwise known as the 'net tax position'. A consequence of the Fiscal Framework[14] BGA mechanism means that the Scottish Budget only benefits from faster tax revenue growth when revenue per person grows faster in Scotland than the rest of the UK.

The central funding outlook uses the SFC's forecasts of devolved tax revenue, as published in Scotland's Economic and Fiscal Forecast May 2022.[15] These are based on the SFC's latest assessment of the Scottish economy and incorporate the impact of Scottish Government policy decisions to date.

The Block Grant Adjustments used in the central funding outlook are based on the OBR's forecasts published at the Spring Statement in March 2022[16]. They are calculated based on a method stipulated in the Fiscal Framework.

Table 5 summarises the revenue and BGA forecasts for each devolved tax.

| All figures in £million, current prices | Forecast | ||||

|---|---|---|---|---|---|

| Resource Funding | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

| Income Tax | |||||

| Revenue | 13,671 | 15,143 | 15,954 | 16,754 | 17,484 |

| Block Grant Adjustment | -13,861 | -15,502 | -15,883 | -16,737 | -17,534 |

| Net Income Tax position | -190 | -359 | 71 | 18 | -50 |

| Land and Buildings Transaction Tax | |||||

| Revenue | 749 | 821 | 849 | 886 | 932 |

| Block Grant Adjustment | -664 | -741 | -772 | -807 | -854 |

| Net LBTT tax position | 86 | 80 | 77 | 79 | 78 |

| Scottish Landfill Tax | |||||

| Revenue | 101 | 95 | 94 | 75 | 16 |

| Block Grant Adjustment | -82 | -81 | -75 | -69 | -76 |

| Net SLfT position | 18 | 14 | 19 | 6 | -59 |

| Total net tax impact | -86 | -265 | 167 | 103 | -31 |

*Figures shown for 2022/23 are based on the SFC and OBR forecasts as at the Scottish 2022/23 Budget, published in December 2021. The latest SFC and OBR forecasts for 2022 will affect the Scottish funding position through reconciliations. *Some figures may not sum due to roundings

The net tax position – as reflected in final outturn data – will be determined by the relative growth of tax revenue per person between Scotland and the rest of the UK. This will in turn be determined by both economic factors and policy choices made by the two governments.

Where economic or policy factors affect both tax bases equally, the net tax position would be largely unaffected. This provides a degree of insulation from economic shocks, both positive and negative.

However, there is some evidence that tax revenue growth (primarily for Income Tax) has been diverging between Scotland and the rest of the UK in recent years, driven in part by strong earnings growth in London. This is discussed in detail in Annex A. Under the Fiscal Framework, Scotland's Budget depends on what happens both in the Scotland and rUK, and as a result our Budget can be reduced even if tax revenue is growing strongly in Scotland, due to factors out of the Scottish Government's control in the rest of the UK. There are alternative Fiscal Framework mechanisms that can reduce these effects. For example, the Welsh Fiscal Framework includes a 'by band' mechanism that reduces the impact of tax growth among higher earners on the Budget position.

Further divergence in revenue growth presents a major risk for the Scottish Government's funding position and is currently the main driver of the negative net Income Tax position forecast in 2022-23 and 2023-24.

The Income Tax forecasts for this MTFS are also affected by a change to the SFC's assumptions for forecasting Income Tax policy. The Scottish Government confirms Income Tax rates and thresholds annually at each Budget in line with economic forecasts and conditions at the time. To inform the forecasts for future years, assumptions about future policy have to be built into the forecasts.

Those assumptions are informed by a range of factors, including past policy decisions of the Scottish Government and, for example, the UK Government's decision to freeze the Higher Rate Threshold to 2025-26. The SFC forecasts are based on the assumption that the Scottish Higher Rate Threshold will be frozen across the forecast horizon, rather than increasing with CPI. This approach has been discussed with and agreed by the Scottish Government. Consistent with past forecasts, the Top Rate threshold remains frozen, and the Starter and Basic Rate Bands are indexed to inflation. The impacts of this on the forecasts are discussed further in the Scottish Economic and Fiscal Forecast document.[17]

This assumption does not represent a policy decision on the part of the Scottish Government. The Scottish Government will continue to make decisions on Income Tax thresholds at each Budget and retain the flexibility to change thresholds in future. However, any future increase in thresholds would reduce available funding relative to the funding envelope presented in this document. This remains a risk to the funding position.

The net tax position also incorporates the current position regarding UK Government tax policy, including the stated intention to reduce the Basic Rate to 19p in 2024-25. By reducing rUK tax revenue growth, this improves the Scottish Government's Budget position from that year onward. As stated above, the Scottish Government takes tax policy decisions at each annual Budget. The current SFC forecasts include no policy changes. Any future reductions in Scottish tax rates would reduce the funding envelope from that shown in this document.

In addition to economic and policy risks, the net tax position remains subject to forecast variation and error. This is typical for revenue sources affected by economic fluctuations. In the case of the Scottish Budget, the risk of forecast error is heightened by the reliance on two different forecast institutions. This is discussed further in Box 1.

Box 1: Impact of differences in the net tax position

The net tax position, which is a critical component of our funding position, is derived by comparing the SFC's forecasts of the three devolved Scottish taxes to the OBR's forecasts of the corresponding Block Grant Adjustments. Comparing two different forecasts can introduce a source of risk in relation to the funding available to allocate in each Budget. These potential differences include:

- Timing – the OBR typically produce forecasts in March and October of each year to align with UKG fiscal events, while the SFC produce forecasts in May and December alongside Scottish fiscal events, as determined by the Scottish Government. If new statistics or figures are published in the gap between forecasts, this can potentially lead to forecasts being based on different sets of data.

- Judgement – even when using the same set of data, the two forecasting institutions may – reasonably and with good justification – make different judgements on the economic outlook. For example, the SFC have typically forecast lower population growth in Scotland than the OBR, which in turn affects their respective tax forecasts.

- Methodology – the two forecasters use different approaches to forecasting the tax base or wider economy. For example, the OBR's Scottish Income Tax forecast is 'top-down' and calculated as a percentage of the OBR's UK wide income tax forecast. In contrast, the SFC's forecast is 'bottom-up', and calculated using Scotland specific economy and tax data and then forecasting tax liabilities at the individual taxpayer level.

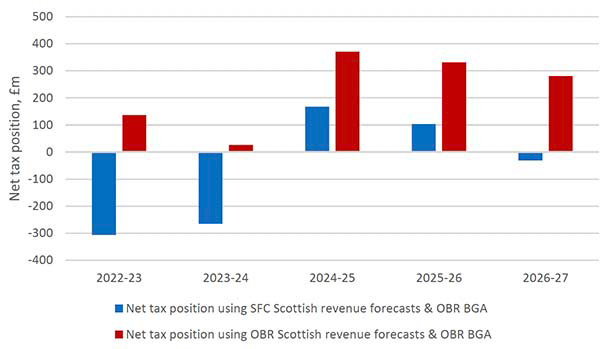

- Comparing the SFC's May 2022 tax revenue forecasts to the OBR's March 2022 BGA forecasts. This is the approach used in the central funding outlook.

- Comparing the OBR's March 2022 Scottish forecasts of devolved tax revenue to the OBR's March 2022 BGA forecasts.

The latter approach removes any differences in timing, judgement, or methodology from the net tax position with the resulting forecast reflecting the OBR's judgement of the relative tax growth between Scotland and rUK. This results in an improvement in the forecast funding position averaging around £300m in each year of the forecast. The extent of the difference indicates how forecasters can vary in their results despite both making use of their best professional judgement and access to similar data. It is also important to note that there may be times when an illustration like this would show a deterioration in the forecast funding position.

The purpose is to demonstrate the scale of this particular element of volatility, which can arise as a result of the operation of the Fiscal Framework. This further demonstrates the inadequacy of the tools available to the Scottish Government to manage and smooth volatility over the medium term.

Any differences between forecasters will ultimately be resolved in reconciliations, which are determined by the final outturn data. However, divergence in forecasts affects the funding available to the Scottish Government to allocate when budgets are set, and large differences between the forecasters can lead to greater volatility in future years when the reconciliations apply.

Having official independent forecasts is intrinsically beneficial, as it removes bias and improves overall fiscal transparency. However, the differences in timing, judgement and methodology between the OBR and SFC continues to present a risk for the Scottish Government's funding outlook and contributes to continuing volatility in the fiscal outlook, as noted in more detail in Chapter 4. The tools the Scottish Government currently has to manage and smooth risks of this nature are inadequate and must be addressed in the upcoming Fiscal Framework Review.

2.6 Block Grant Adjustments for devolved Social Security benefits

The central funding trajectory uses the Social Security Block Grant Adjustments forecast by the OBR, based on their March 2022 forecasts.

These BGAs are based on OBR forecasts of benefit expenditure in England and Wales as of March 2022. The growth in social security BGAs over time will be affected by both economic factors and the policy decisions made by the UK government. This can include technical changes to the eligibility of certain benefits, changes to the generosity of certain payments or decisions around the rate at which payments are increased or uprated over time.

The Social Security BGAs that inform the funding envelope are set out in Table 6 below. These are based on the OBR forecasts, with the exception of the BGA for the Winter Fuel Payment. As this is a newly devolved benefit, the OBR has not yet produced a forecast to inform the BGA. For the purposes of the MTFS, the Scottish Government have forecast the expected BGA. This will be updated following publication of OBR forecasts of Winter Fuel Payment expenditure, broken down by territory, when available.

| Forecast | |||||

|---|---|---|---|---|---|

| 2022-23* | 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

| Carer's Allowance | 323 | 362 | 393 | 423 | 459 |

| Attendance Allowance | 545 | 594 | 626 | 649 | 672 |

| Adult Disability Payment (replacement for Personal Independence Payment) | 1,933 | 2,298 | 2,566 | 2,799 | 3,014 |

| Disability Living Allowance | 687 | 732 | 713 | 677 | 682 |

| Industrial Injuries Disablement Scheme | 79 | 83 | 82 | 80 | 79 |

| Severe Disablement Allowance | 6 | 6 | 5 | 5 | 4 |

| Low Income Winter Heating Assistance (replacement for Cold Weather Payment) | 14 | 8 | 7 | 7 | 7 |

| Winter Fuel Payment | N/A | N/A | 181 | 184 | 185 |

| Total social security BGA | 3,587 | 4,082 | 4,574 | 4,825 | 5,103 |

*Based on OBR forecasts, with the exception of the BGA for the Winter Fuel Payment, at the point the 2022-23 Scottish Budget was set.

The BGAs are also subject to in-year reconciliations, with a final reconciliation made once outturn data is available. If outturn expenditure in England and Wales is higher than forecast, a positive BGA reconciliation (i.e. an addition) will be made to the Scottish Budget to reflect these changes, and vice versa. For example, social security expenditure in England and Wales in 2020-21 was higher than had been forecast, resulting in a final BGA which was £22m higher than forecast. This was reconciled by adding £22m to the Scottish Budget in 2022-23.

2.7 Other income

Other income is a relatively small component (net less than 1%) of the total funding position, and relies on risk-based assumptions by the Scottish Government. It captures a number of funding sources (and deductions to funding). The material elements are described below:

- Income Tax Reconciliations. These relate to OBR and SFC forecast error in past years. They occur after tax outturn data becomes available, and affect the financial year three years after the tax year to which they relate (i.e. the reconciliation that affects the 2023-24 Scottish Budget relates to the 2020-21 tax year). Estimates of future reconciliations are based on the latest SFC and OBR forecasts, compared to the forecasts used at the relevant Budget. Future reconciliations are currently forecast to be negative but could feasibly be positive or negative in future years. As reconciliations are caused by error in forecasts, they are (by definition) challenging to forecast or predict. This adds an additional degree of volatility to the Scottish Budget position.

- Income Tax Spillovers. The Fiscal Framework allows for transfers from the UK Government to the Scottish Government (or vice versa) to allow for impacts of tax policy changes that are not accounted for by the BGA mechanism which have a disproportionate effect on Scottish Income Tax receipts. We have included an assumption concerning transfers related to a spillover effect linked to increases in the Personal Allowance. We are currently in dispute over the handling of the spillover, and expect this to be considered as part of the Fiscal Framework Review, if not addressed in advance of that.

- Resource Borrowing. This provides funding to offset the impact of adverse income tax reconciliations in future years. Plans and policies regarding borrowing are discussed in chapter 4.

- Projected Resource Costs associated with Capital and Resource Borrowing. These costs are now included as deductions to funding rather than in the portfolio budgets. This reflects both the operational impact of how these payments are deducted from the Scottish Consolidated Fund and the manner in which they are managed in line with the policies outlined in Chapter 4.

- Scotland Reserve Drawdowns. These are anticipated funds available based on fiscal framework aggregates applying to each year and historical average of funds carried forward between years. Scotland Reserve policies are discussed further in chapter 4.

- ScotWind Revenue. This is income from option fees from ScotWind leasing and assumes that the income will be drawn down over the first two years of the forecast period. This will be re-invested in action to tackle the twin challenges of climate change and biodiversity loss over the spending review period, as described in the Resource Spending Review.

- Migrant Surcharge is demand led income collected by the UK Home Office and redistributed to Devolved Governments on a Barnett basis. This differs from Barnett Consequentials which are derived from spending allocations to UK departments on areas of devolved competence.

| Forecast | ||||

|---|---|---|---|---|

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

| Reconciliations | -221 | -817 | -238 | 0 |

| Resource Borrowing | 110 | 300 | 119 | 0 |

| Resource Borrowing Costs | -110 | -124 | -169 | -191 |

| Capital Borrowing Costs | -100 | -122 | -144 | -166 |

| ScotWind | 310 | 350 | 0 | 0 |

| Scotland Reserve | 279 | 250 | 113 | 87 |

| Migrant Surcharge | 120 | 120 | 120 | 120 |

| QLTR | 5 | 5 | 5 | 5 |

| Other* | 100 | 52 | 30 | 32 |

| Spillover** | -77 | -133 | -154 | -152 |

| Total other income | 416 | -119 | -317 | -265 |

*Other includes a risk-based assumption reflecting the uncertainty in all elements of funding in this table

** Numbers and approach currently subject to dispute.

2.8 Non-Domestic Rates

Non-Domestic Rates (NDR) are, unlike most other sources of funding, ring-fenced in what they can be used for. All NDR revenue raised is ultimately distributed back to Local Authorities. It is therefore usually considered separately from the Scottish Budget as a whole, but still forms an important component of the overall funding available to the Scottish Government.

The central funding envelope uses the SFC's forecasts of NDR revenues. Informed by past policy decisions of the Scottish Government, the SFC have assumed the next revaluation on 1 April 2023 will be revenue-neutral in real terms. This approach has been discussed with and agreed by the Scottish Government. However, due to relief provided through the pandemic support and other factors including higher-than-expected levels of NDR income lost to write-offs, bad debts following COVID-19 and emerging 2017 revaluation appeals losses, the NDR deficit has increased.

For the next revaluation to be revenue-neutral in 2023-24, based on current expectations about the tax base, an increase in the poundage would be required. Decisions on tax rates are set at each Budget, and any changes in the poundage – or the amount of NDR funding available for allocation - will be based on the forecasts available at that time.

| All figures in £million, current prices | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Non-domestic rates distributable amount | 2,766 | 3,190 | 3,134 | 3,323 | 3,651 |

2.9 Capital Funding

Capital funding is primarily provided by the Block Grant and Financial Transactions (FT) allocations, both determined by the UK Government's capital spending plans. The remaining sums arise from: income and receipts; deployment of Scottish capital borrowing and reserve powers; innovative financial and revenue finance models; and recycling repayments from earlier FT loans.

Section 3.2 shows the funding outlook for the capital Block Grant and discusses the changes since the last MTFS in more depth. As with the resource outlook, the UK Government's Spending Review settlement provides a degree of certainty over the next three financial years. In 2025-26 and 2026-27, the capital grant funding available to the Scottish Government is assumed to grow at around 4% per year, in line with the OBR's forecasts for UK wide public sector investment[18].

2.10 Risks and uncertainties for resource funding

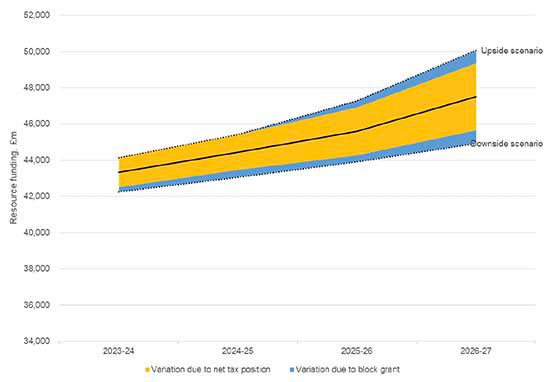

As noted above, all sources of the funding envelope are subject to uncertainty. These risks are difficult to quantify and ascribe specific probabilities to. However, the Scottish Government needs to anticipate the degree of likely volatility in the funding envelope in order to plan and manage spending over time.

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

|---|---|---|---|---|

| Central funding envelope | 43,321 | 44,439 | 45,600 | 47,498 |

| Upside scenario | 44,144 | 45,419 | 47,285 | 50,069 |

| % variation | 1.9% | 2.2% | 3.7% | 5.4% |

| Downside scenario | 42,248 | 43,059 | 43,914 | 44,927 |

| % variation | -2.5% | -3.1% | -3.7% | -5.4% |

Figure 7 and Table 9 above present an illustrative upside and downside scenario for the funding envelope based on some of these risks. These do not relate to a specific economic scenario, and the probability of either scenario cannot be easily quantified. However, they are based on the range of feasible outcomes for major components of the funding envelope. It allows for two principal sources of variation in the funding position:

- Changes in the UK Government Block Grant. As noted above, UK policy changes have a major impact on the overall funding position. In the downside scenario the UK Government adheres closely to the Spending Review settlement in the next two years, and the additional consequentials assumed in the central scenario do not materialise. The subsequent two years reflect a wider range of possible outcomes for UKG fiscal policy and assume the Block Grant growing at 1 percentage point higher or lower than the c. 4% annual growth assumed in the central scenario.

- Forecast variation in tax revenue. Both tax revenue and Block Grant Adjustment forecasts are subject to forecast movements reflecting changes in policy, economic conditions, and forecast error. Based on SFC and OBR forecasts to date, on average, forecasts of tax revenue and BGAs produced today will differ by around 5% from the forecasts applied in the upcoming 2023-24 Budget. This forecast variation increases over a longer time horizon, reaching around 10% over a 5-year period. Much of this variation will be out of the control of the forecasting institutions, and will include the impact of unforeseeable economic shocks such as the COVID-19 pandemic. The figures cited above also reflect the forecast variation in the early stages of both institutions forecasting newly devolved taxes, which we would expect to reduce over time. Nevertheless, these figures are useful to set parameters on how much tax and BGA forecasts could change in future.

The upside and downside scenario are modelled on the basis of varying forecast tax revenue based on this average forecast variation. This results in a widening range between the upside and downside funding envelopes across the forecast, reflecting the greater uncertainty further in the future.

In practice, forecasts of the BGA and tax revenue will often vary in the same direction – for example, economic shocks such as COVID-19 that reduce both tax revenue in Scotland rUK, so the overall impact on the net position will often be smaller.

Other sources of funding could also vary substantially. In particular, the components of the 'other income' line as described in Section 2.7 are especially volatile, and components of this could vary between being reductions or increases to the funding envelope. However, these variations have not been included in the scenarios above, which are intended to portray the potential variation of the most significant drivers of variation around the central funding envelope.

Contact

Email: sophie.osborn@gov.scot