Rural Scotland Business Panel survey: report

This report presents findings from the first Rural Scotland Business Panel survey carried out in October/November 2021.

5. Increased costs

Key findings

It was clear that businesses in the region were feeling the effects of the economic challenges occurring at the time of the survey, with the majority reporting cost increases across almost all measures asked about in the survey. The exceptions were cost of premises and business rates, which remained relatively stable.

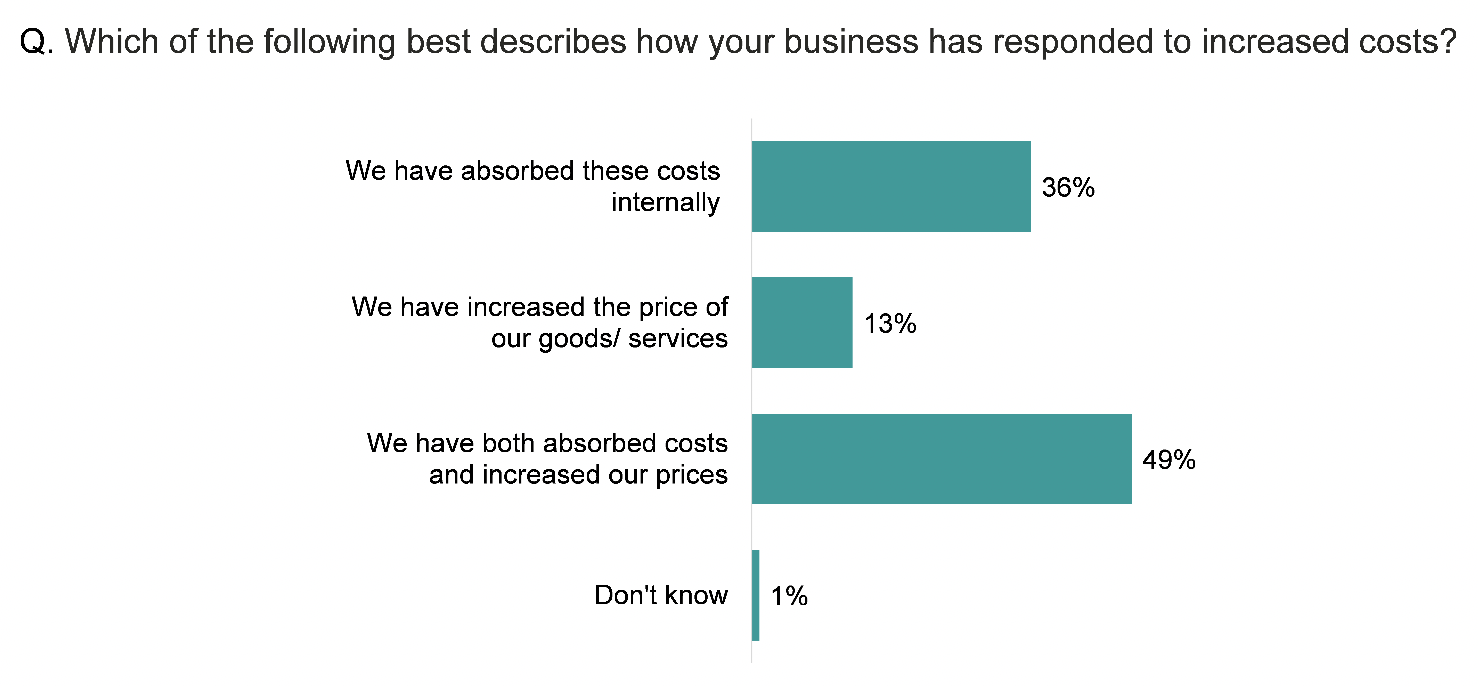

Among those that had experienced cost increases in the last 12 months, 36% had absorbed those costs internally, 13% had increased their prices, and 49% had done both.

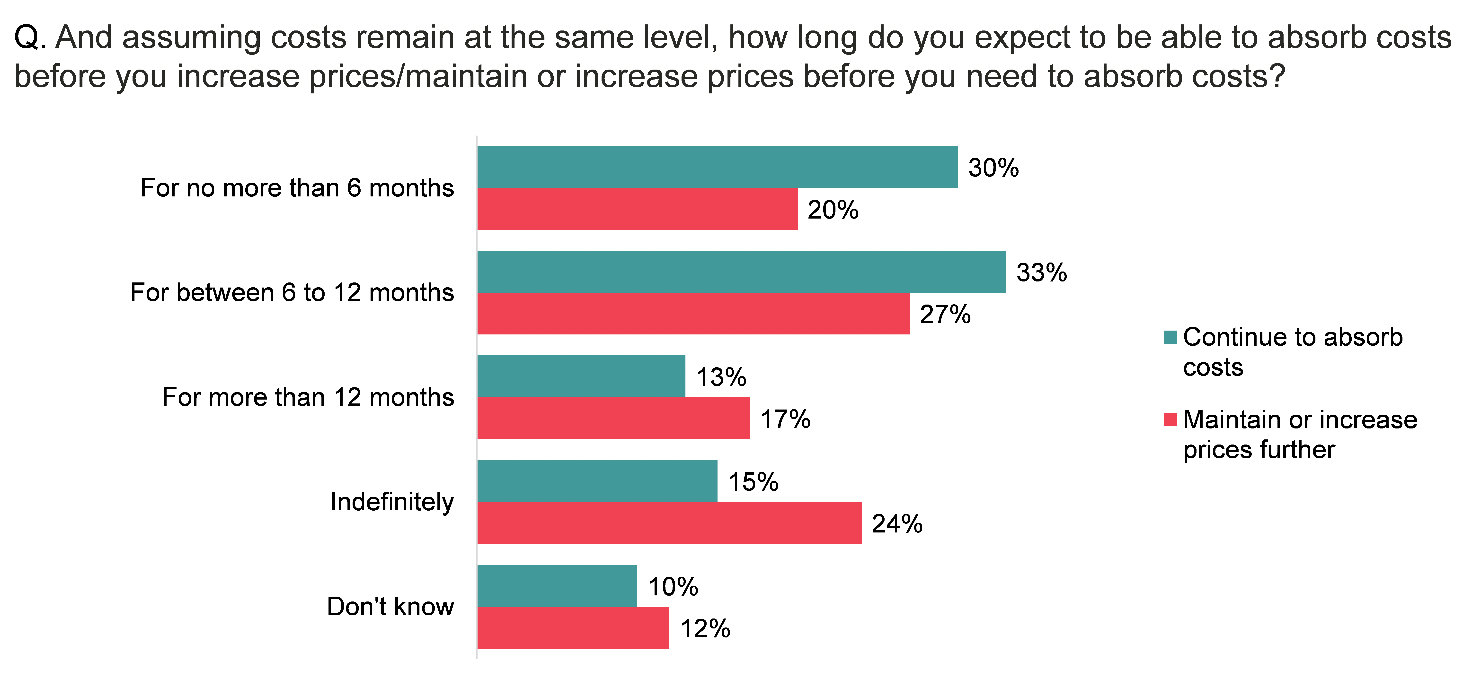

Nearly two thirds (63%) of businesses that had absorbed costs said they could do so for up to 12 months before having to increase their prices, while a quarter (27%) felt they could do so beyond 12 months

Among businesses that had increased their prices in response to rising costs, 47% felt they could maintain or increase prices further for up to 12 months before absorbing costs, while 41% felt they could do so for longer than 12 months.

Cost changes in the last 12 months

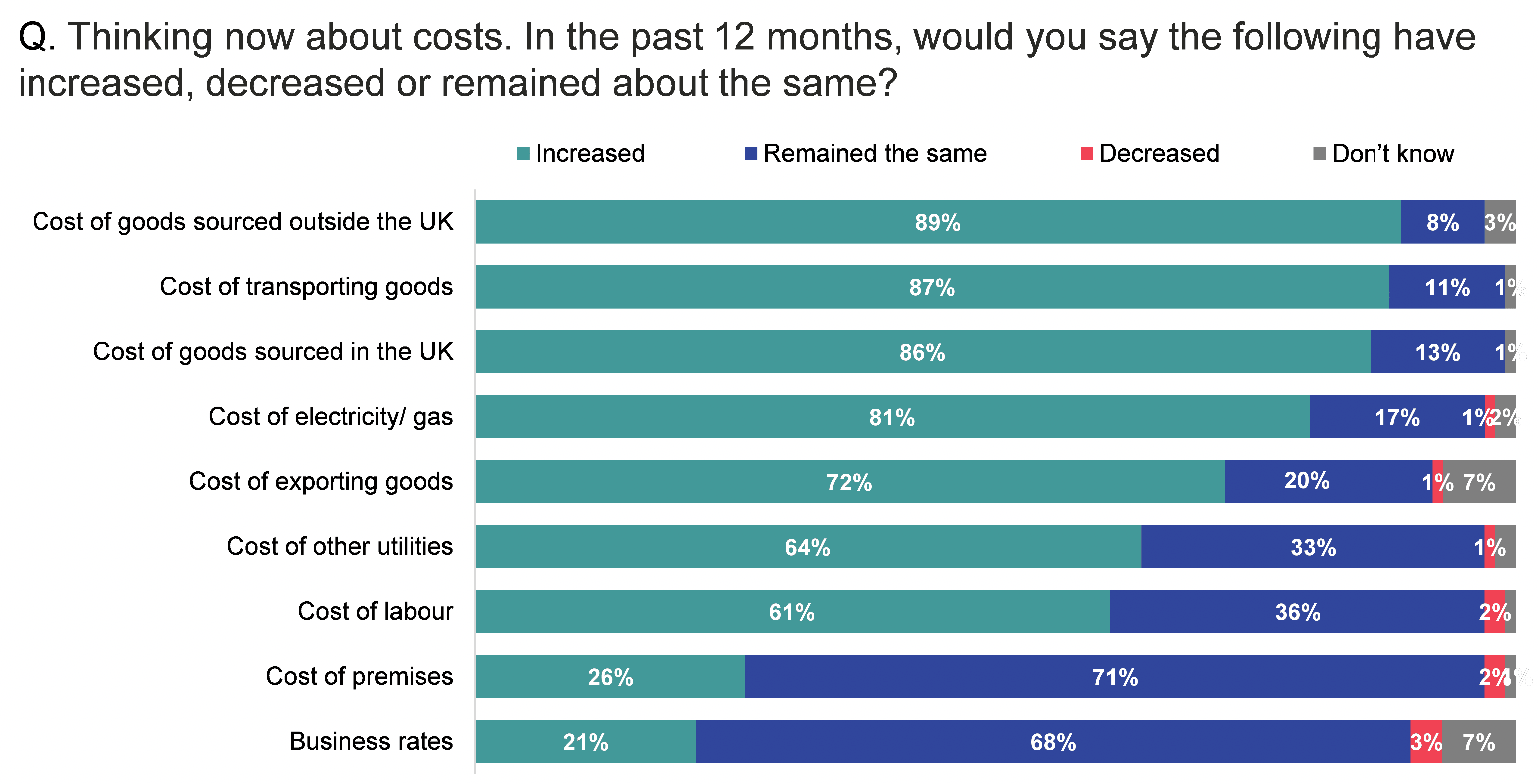

The majority (95%) of businesses had experienced at least some form of cost increases over the last 12 months, highlighting the impacts of the economic challenges facing rural businesses at the time of the survey. The majority of businesses reported cost increases across almost all measures, with the exception of cost of premises and business rates (Figure 5.1).

The most common increases related to costs of goods including: sourcing goods from both outside (89%) and within (86%) the UK, transporting goods (87%) and exporting goods (72%). Increased cost of utilities was also common: 81% experienced an increase in electricity and gas and 64% in other utilities. Almost two thirds experienced increased labour costs (61%).

Cost of premises and business rates remained relatively stable (for 71% and 68% respectively). The general stability in business rates may reflect the Scottish Government's rates relief for businesses during COVID-19 (up to until 31 March 2021). However, 26% said cost of premises had increased, while 21% said business rates had increased.

Base: All for whom it applied

Variation in experience of cost changes

Cost changes were more apparent among certain types of business, including those in the Highlands and Islands, the food and drink and tourism sectors, and larger businesses. The following were more likely than average to experience specific cost changes (see Appendix A for further variations).

- Highlands and Islands (78%), remote rural locations (79%), and island locations (85%) were all more likely than average to experience increased costs of exporting goods.

- Accessible rural locations were more likely than average to experience increased costs of goods sourced within the UK (88%).

- Food and drink businesses were also more likely to experience increased costs of goods sourced in the UK (92%).

- Tourism businesses were more likely than average to experience increased costs of utilities (other than electricity/gas) (72%) but also a decrease in business rates (10%). This decrease likely reflects the Scottish Government rates relief for leisure businesses during and after the pandemic (they received 100% rates relief due to continue until March 2022).

- Increased cost of labour was more commonly experienced by businesses employing 25+ (82%), 11-24 (78%) and 5-10 (73%) staff, compared with those employing 1-4 staff (55%).

- Views on the costs of goods did not vary much by the markets outside of Scotland that businesses were importing from – this was the case for both cost of goods from within and outside of the UK.

- Increased costs of exporting goods were also experienced at similar levels by exporters to each market outside Scotland.

Responses to increased costs

Among those that had experienced cost increases in the last 12 months, 36% had absorbed those costs internally, 13% had increased their prices, and 49% had done both (Figure 5.2).

Base: All that had experienced cost increases (2,606)

Variation in response to increased costs

Businesses more likely to have absorbed costs included:

- food and drink (54%) and financial and business services (48%),

- sole traders (45%) and other small businesses (1-4 staff) (40%),

- those in remote rural areas (40%), and

- those with lower levels of optimism (48%) and economic confidence (40%).

Those more likely to have increased the price of goods/ services included:

- non-growth sector businesses (17%), and

- those operating above pre-COVID-19 levels (19%).

Outlook for responding to cost increases

Nearly two thirds (63%) of businesses that had absorbed costs said they could do so for up to 12 months before having to increase their prices, while 28% felt they could do so beyond 12 months (Figure 5.3).

Among businesses that had increased their prices in response to rising costs, 47% felt they could continue do so for up to 12 months before absorbing costs, while 41% felt they could for longer than 12 months.

Base: All that had absorbed cost increases (902); all that increased prices (328)

Variation in outlook or responding to cost increases

Among those that absorbed costs, the financial and business services sector were more likely than average to say they could continue doing so indefinitely (30%). Those only able to absorb costs for up to 6 months were more likely to be:

- tourism businesses (45%),

- operating below pre-pandemic levels (37%), and

- striving for growth (35%).

Businesses more likely to be able to absorb costs for more than 12 months included:

- those with increased economic confidence (28%),

- operating above their pre-pandemic levels (25%), and

- those trading with Northern Ireland (31%) and England and Wales (25%).

Contact

Email: socialresearch@gov.scot