Rural Scotland Business Panel survey: report

This report presents findings from the first Rural Scotland Business Panel survey carried out in October/November 2021.

4. Financial concerns and access to finance

Key findings

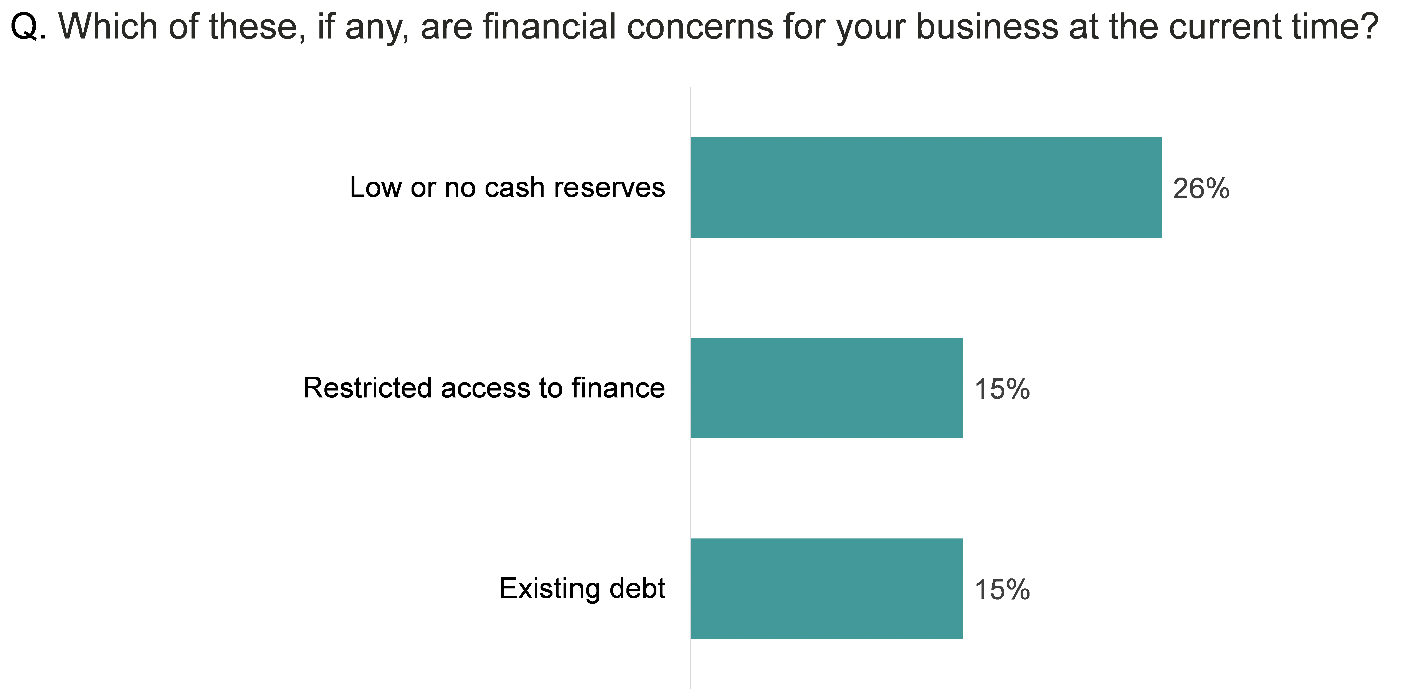

Overall, around a third (35%) of businesses were concerned about at least one of these aspects of their finance: low or no cash reserves (26% concerned), access to finance (15%) and existing debt (15%).

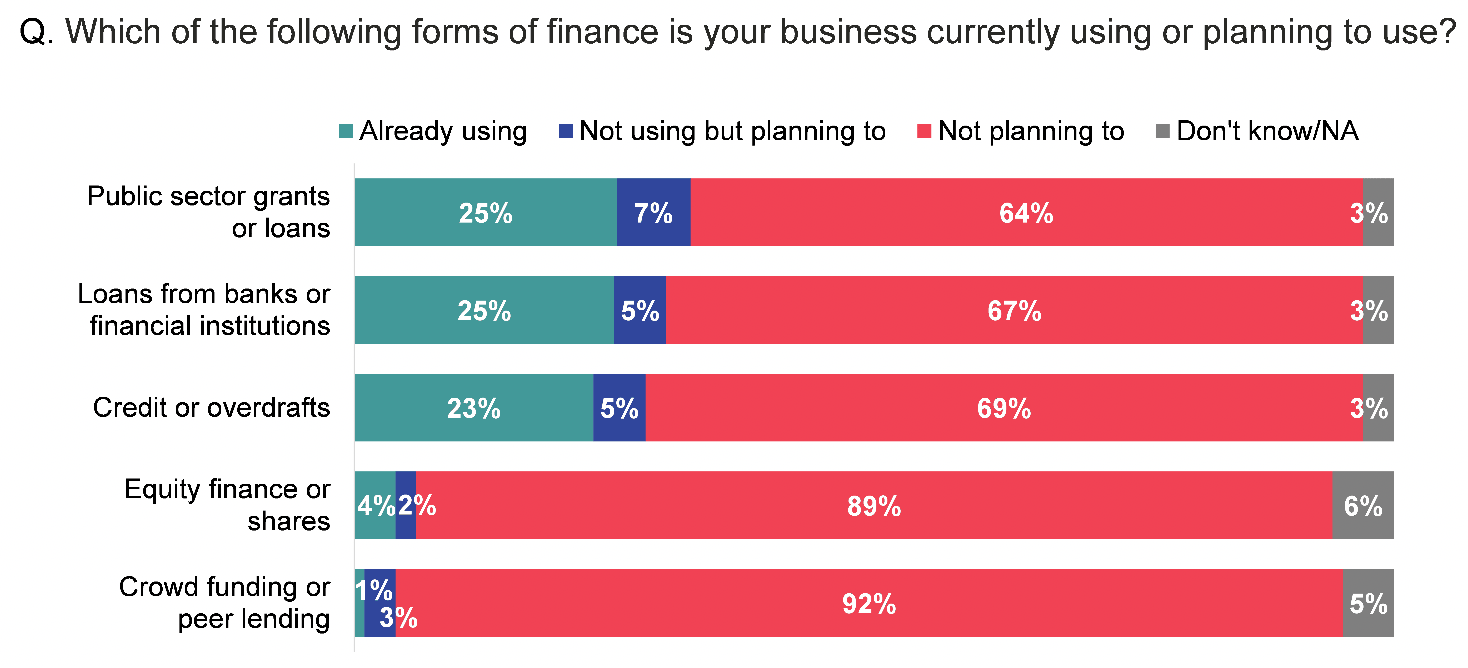

Just over half (55%) were currently using or planning to use finance. A quarter were already using loans from banks or financial institutions (25%), public sector loans or grants (25%) and credits or overdrafts (23%).

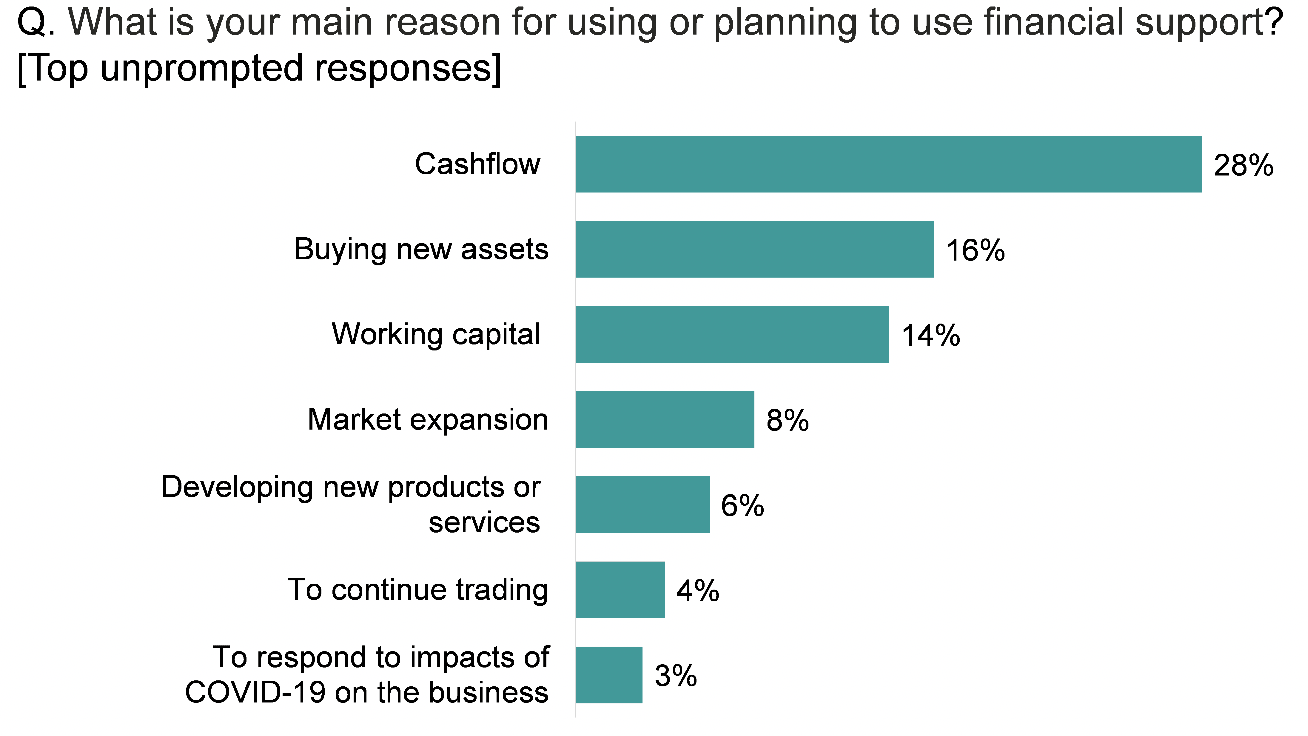

The main reason for using, or planning to use, finance was for cash flow (28%) followed by buying new assets (16%) and working capital (14%). The main reason for not doing so was that businesses felt there was simply no need (80%), while 12% said they wished to remain debt free.

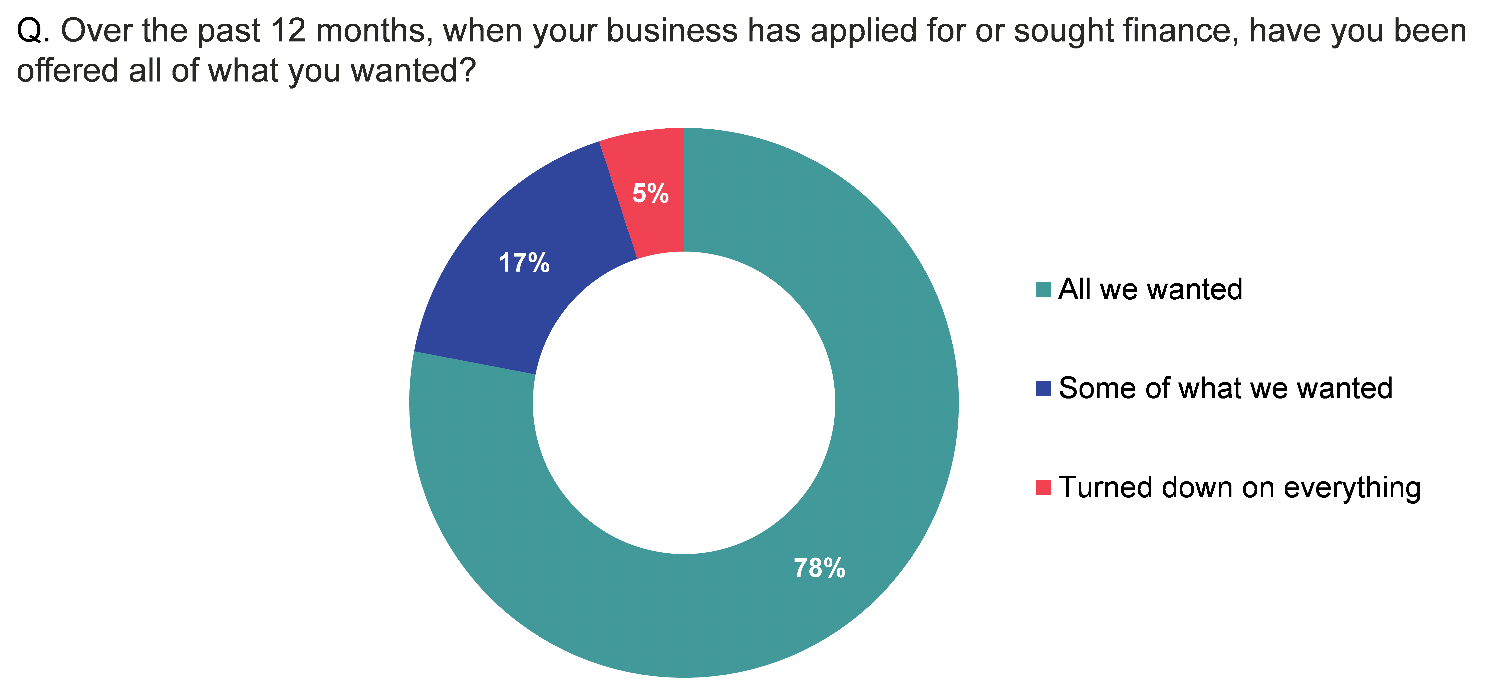

Half (50%) of businesses had applied for financial support in the past 12 months. Of those, 95% had been successful (78% getting all and 17% some of what they wanted). Only 5% were turned down on everything.

Current financial concerns

Overall, around a third (35%) of businesses were concerned about at least one of these aspects of their finance: low or no cash reserves (26% concerned), restricted access to finance (15%) and existing debt (15%) (Figure 4.1).

Base: All buisinesses (2,726)

Variation in financial concerns

As might be expected, those operating below pre-pandemic levels, and those not optimistic about their future, were more likely to say each was a concern: low or no cash reserves (38% and 45%), access to finance (22% and 22%) and existing debt (19% and 22%).

Food and drink and tourism businesses also each had higher than average concern with existing debt (21% and 24% respectively).

Use of finance

Just over half (55%) of businesses were currently using or planning to use some form of finance. A quarter were already using loans from banks or financial institutions (25%), public sector loans or grants (25%) and credits or overdrafts (23%) (Figure 4.2).

Base: All buisinesses (2,726)

Variation in use of finance

Use of finance was higher than average among: food and drink and tourism businesses, those in the Highlands and Islands and in remote rural areas, large businesses (25+ staff), and those importing internationally. The specific types of finance that these types of businesses were more likely to be already using are shown in Table 4.1.

| Type of finance | Food and drink | Tourism | Highlands and Islands | Remote rural | Large (25+) | All |

|---|---|---|---|---|---|---|

| Public sector grants or loans | 33 | 39 | 32 | 30 | 38 | 25 |

| Loans from banks or other financial institutions | 44 | 33 | 31 | 30 | 46 | 25 |

| Credit or overdrafts | 41 | In line with average | 26 | In line with average | 27 | |

| Base | 502 | 301 | 1,003 | 876 | 155 | 2,726 |

(Figures shown are those that are higher than the average)

Reasons for using finance

The main reason for using or planning to use financial support was for cash flow (28%) followed by buying new assets (16%) and working capital (14%) (Figure 4.3).

Base: All using/planning to use finance (1,580)

Variation in reasons for using finance

Findings were fairly similar across different types of business, however:

- Food and drink businesses were more likely to have used/planned to use finance for working capital (19%) or market expansion (13%).

- Using finance for cash flow was more common among those operating below their pre-pandemic levels (31%).

Reasons for not using finance

The main reason for not using or planning to use financial support was that businesses felt there was simply no need (80%), while 12% said they wished to remain debt free. Other reasons, such as plans to retire or close the business, the economic climate, the cost of repayment, and funding being provided from elsewhere, were given by only small proportions (fewer than 3%).

There was little variation by type of business. However, those that were operating below their pre-pandemic levels (16%) and were not optimistic about their future (23%) were more likely than average (12%) to say they wanted to remain debt free.

Applying for financial support

Half (50%) of businesses had applied for financial support in the past 12 months. Of those, 95% had been successful (78% getting all and 17% some of what they wanted). Only 5% were turned down on everything (Figure 4.4).

Base: All that applied for finance (1,362)

Variation in experience of applying for finance

Similar to their use of finance, outlined above, both tourism (69%) and food and drink (55%) businesses were more likely than average (50%) to have applied for financial support. In contrast, financial and business services were least likely to have applied (37%).

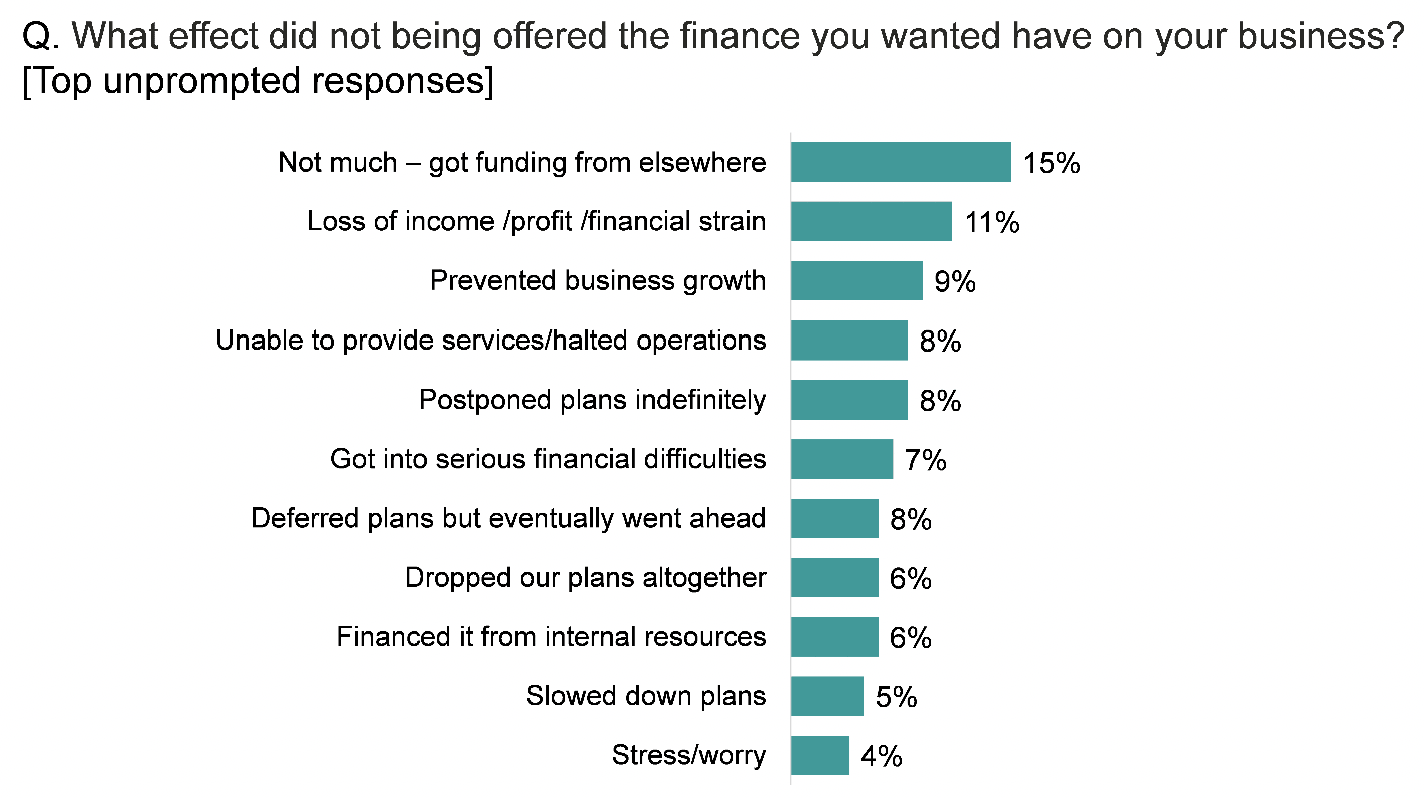

Impact of not receiving finance

For those that were not offered the finance they wanted, around one in five (22%) said this had impacted on their plans in some way:

- 8% said they were unable to provide the services they had planned to,

- 8% had postponed plans indefinitely,

- 6% had dropped them altogether, and

- 9% said it had prevented business growth.

Around one in five also mentioned negative financial impacts, as in loss of income or profit (11%) and getting into serious financial difficulties (7%).

For 15%, there was little impact as they had received funding from elsewhere (Figure 4.5).

Base: All that had not been offered the finance they wanted (318)

Contact

Email: socialresearch@gov.scot