Rural Scotland Business Panel survey: report

This report presents findings from the first Rural Scotland Business Panel survey carried out in October/November 2021.

2. Optimism and performance

Key findings

Thinking about the economic outlook for Scotland over the next 12 months, 60% of businesses were confident, while 38% were not. Most had seen their confidence either increase (17%) or remain stable (48%) in the past six months. Confidence had decreased for 34% of businesses.

Around three fifths of businesses were operating at either the same level (40%) or over and above the level (20%) they were before COVID-19. Just under two fifths (39%) were operating below their pre-pandemic levels.

Over the past six months, sales or turnover performance was mixed, while employment had remained relatively stable. Exports were more likely to have decreased than increased, but had remained stable for around half of businesses.

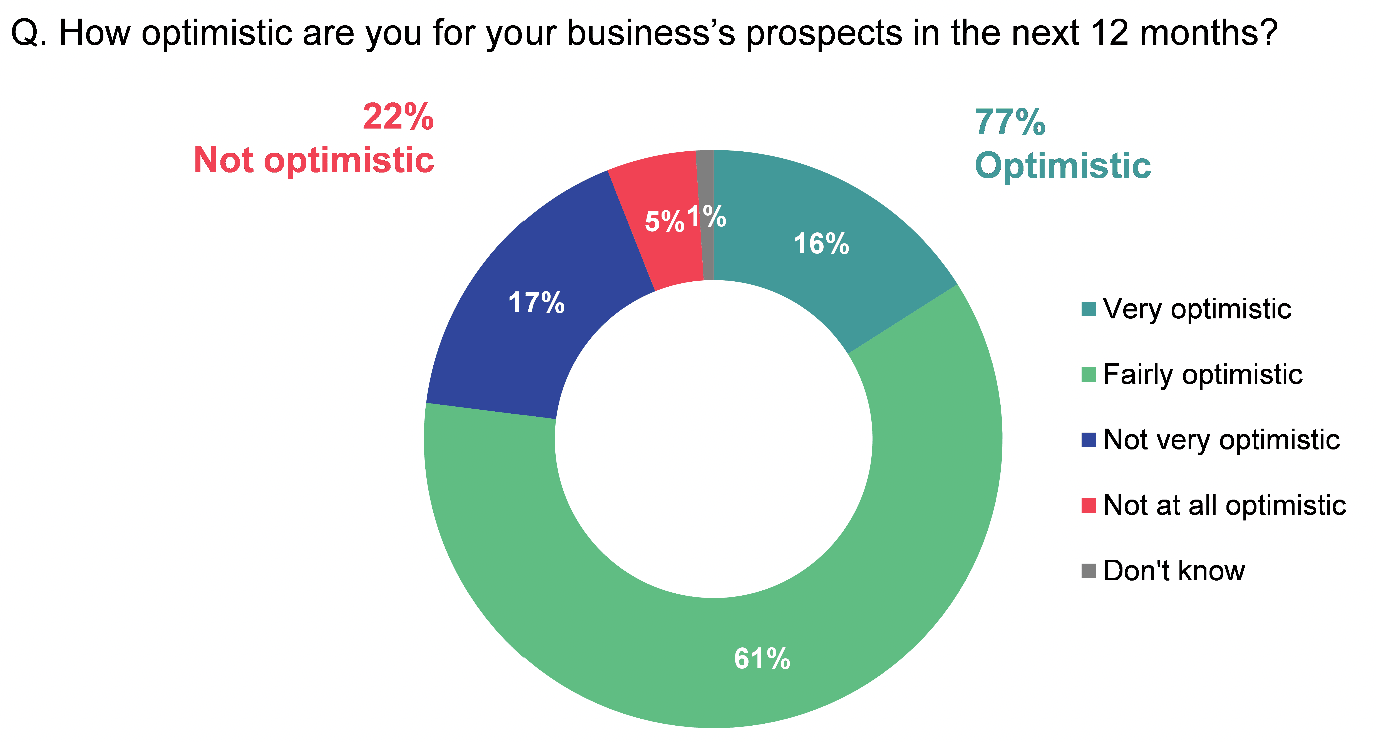

Most (77%) businesses were optimistic about their prospects in the next 12 months, but 22% were not.

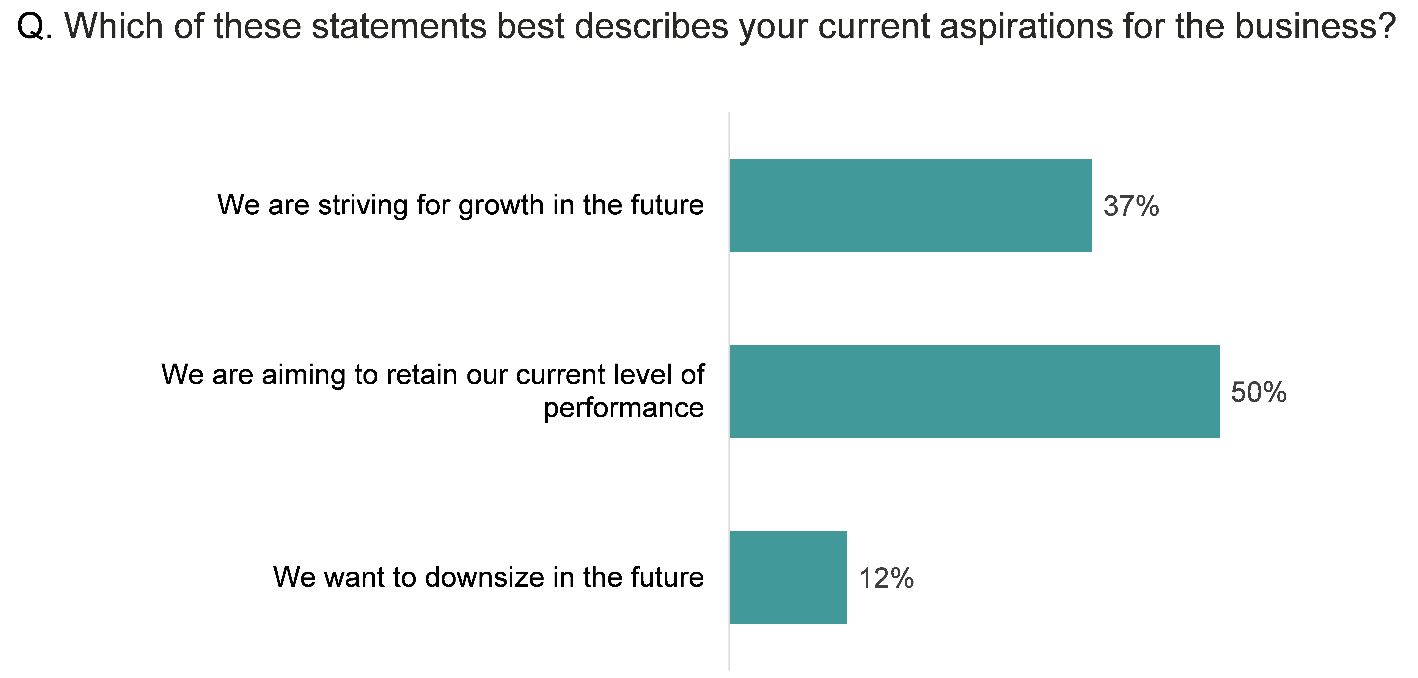

In terms of their current aspirations, just over a third (37%) were striving for growth while half (50%) were content with their current level of performance. Around one in ten (12%) wanted to downsize.

Current economic optimism

Base: All buisinesses (2,726)

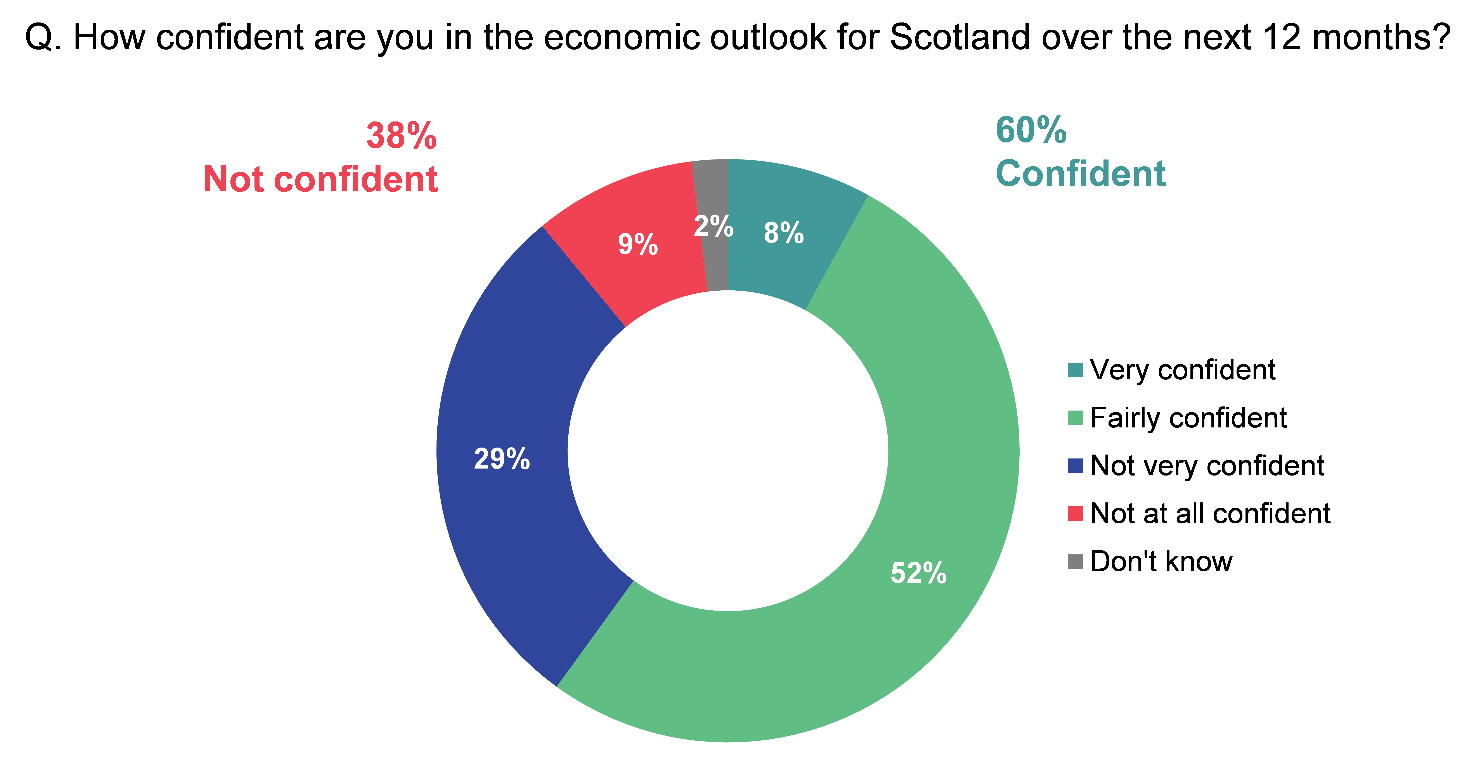

Thinking about the economic outlook for Scotland over the next 12 months, 60% of businesses said they were confident, while 38% said they were not (Figure 2.1).

Variation in optimism

Businesses in the Highlands and Islands were more confident (64%) than those in the South of Scotland (60%) and the rest of rural Scotland (58%).

Confidence in the economy was also higher than average among:

- larger businesses with 11-24 (74%) and 25+ staff (72% confident),

- financial and business services (66%),

- those in small towns and peripheral urban locations (62%), and

- those operating above the level they were before COVID-19 (75%).

Confidence was lower than average among:

- sole traders (43% not confident) and other small businesses (1-4 staff) (41%),

- food and drink (47%), and

- those that were operating below the level they were before COVID-19 (52%).

Economic optimism over the past six months

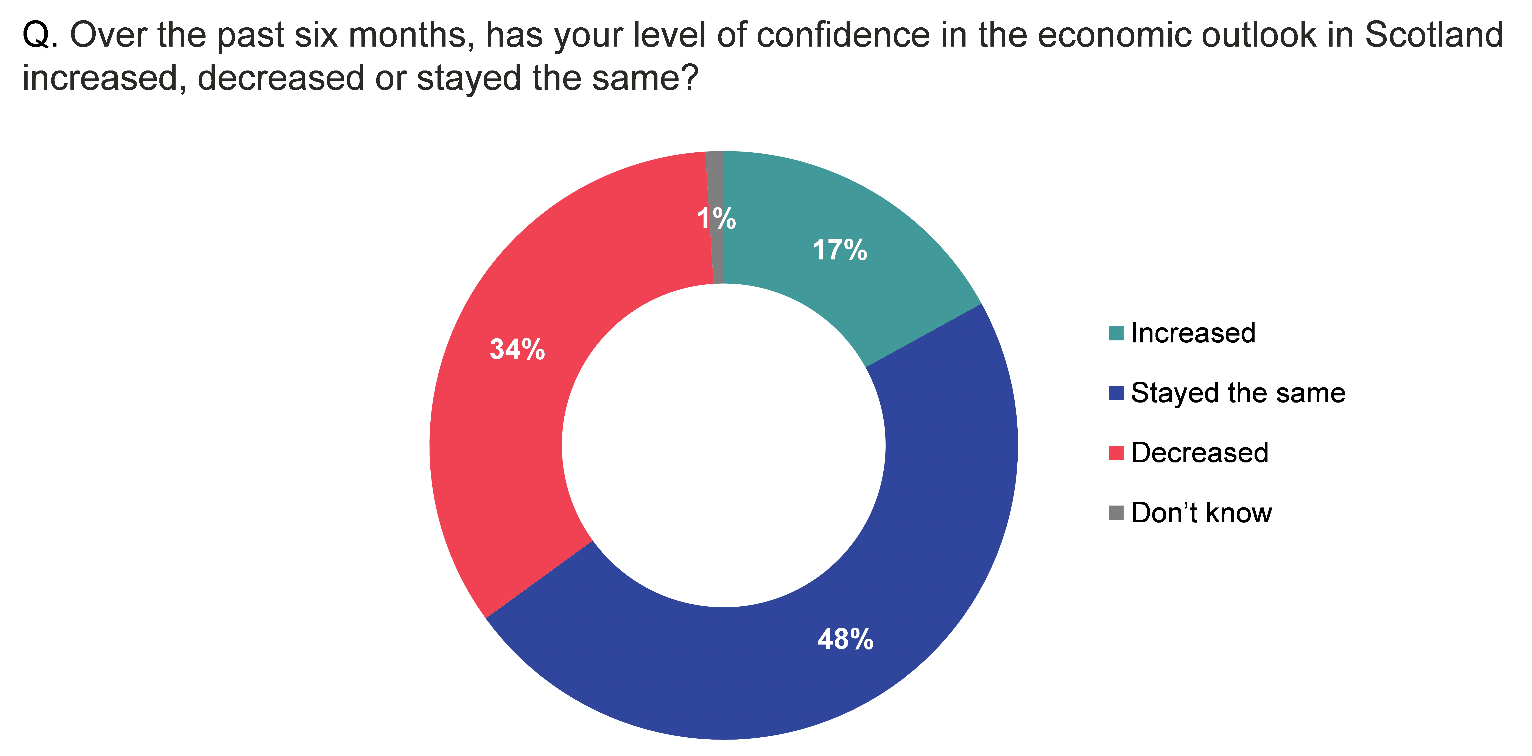

Thinking about the preceding six months, around half (48%) of businesses said their confidence in the economic outlook in Scotland had stayed the same, while 17% said it had increased and 34% decreased (Figure 2.2).

Base: All buisinesses (2,726)

Overall net confidence was -17[8]. This was similar across the three regions covered in the survey: net confidence was -15 in the Highlands and Islands, -16 in the South of Scotland and -18 in the rest of rural Scotland.

Variation in optimism over past six months

Businesses more likely than average to say their confidence had increased were:

- tourism businesses (23%),

- those in small towns and peripheral urban areas (19%),

- operating above their pre-pandemic levels (32%), and

- selling goods to markets in Northern Ireland (22%), the EU (24%) and outside the EU (25%).

Those more likely to report decreased confidence were:

- food and drink businesses (44%),

- operating below pre-pandemic levels (46%), and

- trading only in Scotland (37%).

Level of current operation

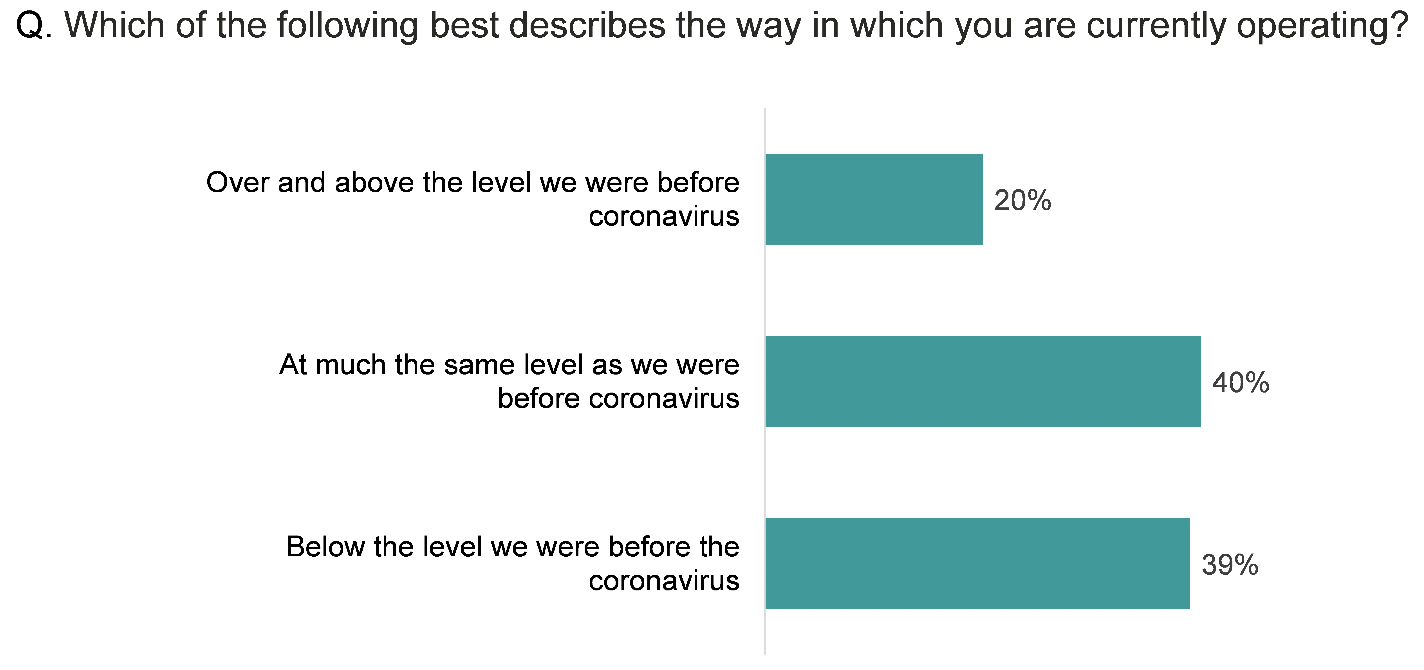

Three fifths (60%) of businesses said they were now operating at either the same level (40%) or over and above the level (20%) they were before the COVID-19 pandemic. Just under two fifths (39%) were operating below their pre-pandemic levels (Figure 2.3).

Base: All buisinesses (2,726)

Variation in level of operation

Businesses in the Highlands and Islands (44%) and the South of Scotland (46%) were more likely than those in the rest of rural Scotland (37%) to be operating at much the same level as pre-pandemic. Those in the rest of rural Scotland were more likely to be operating below their former levels (42% compared with 32% and 31% respectively) (Table 2.1).

| Operating level in relation to before the coronavirus | Highlands and Islands (%) | South of Scotland (%) | Rest of rural Scotland (%) | Total (%) |

|---|---|---|---|---|

| Over and above | 22 | 23 | 19 | 20 |

| At much the same level | 44 | 46 | 37 | 40 |

| Below | 32 | 31 | 42 | 39 |

| Base | 1,003 | 602 | 1,121 | 2,726 |

Other types of business more likely than average to be operating below pre-pandemic levels were:

- sole traders (44%),

- tourism businesses (54%),

- those in small towns and peripheral urban areas (44%), and

- those trading internationally (43%).

Those more likely to be operating over and above their former levels were:

- larger businesses with 11-24 (30%) and 25+ (32%) staff, and

- those who said they were striving for growth in the future (27%).

Food and drink businesses (68%) and those in remote (44%) and accessible (47%) rural areas were more likely than average to be operating at the same level as they were before.

Aspects of business performance

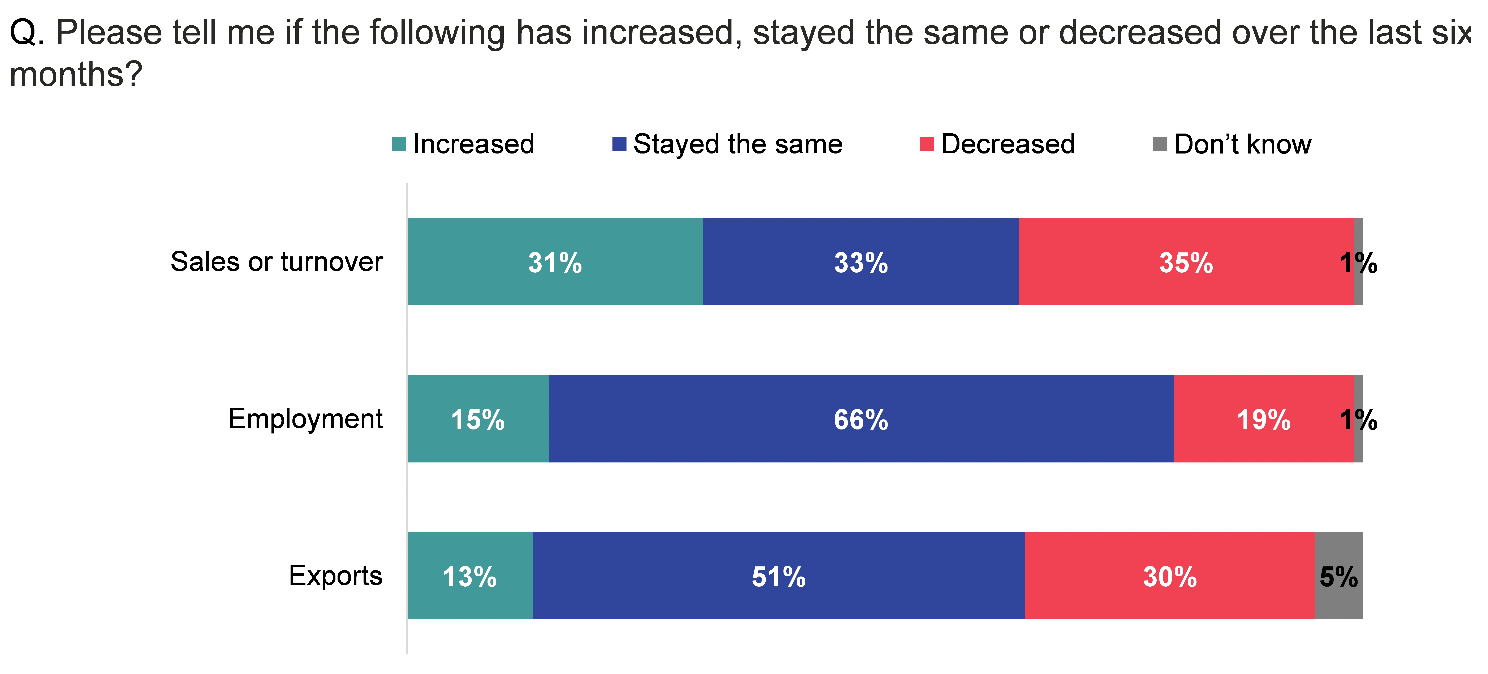

Over the past six months, sales or turnover performance was mixed: it had increased for 31% of businesses, decreased for 35%, and stayed the same for 33%. In the same period, employment had remained relatively stable (66%). Exports were more likely to have decreased than increased (30% vs 13%) but had remained stable for around half of businesses (51%) (Figure 2.4).

Base: All buisinesses for whom each applied

Variation in aspects of business performance

Businesses in the Highlands and Islands and the South of Scotland were more likely than those in the rest of rural Scotland to report an increase in sales and turnover. Highlands and Islands businesses were also more likely to report an increase in employment, although most experienced stability in this aspect of performance (Table 2.2).

| Aspects of business performance | Highlands and Islands | South of Scotland | Rest of Rural Scotland | Total |

|---|---|---|---|---|

| % saying 'increased' | ||||

| Sales or turnover | 38 | 36 | 28 | 31 |

| Employment | 19 | 14 | 14 | 15 |

| Exports | 14 | 10 | 14 | 13 |

| Base (All businesses for whom each applied in each area) | ||||

On sales or turnover:

- Decreases were more common than average among tourism and creative industries (47% and 44% respectively).

- Food and drink were more likely than average to report stability (47%).

On employment:

- Increases were more common than average among larger businesses (25+ staff) (34%), and those operating above pre-pandemic levels (37%).

- Decreases were more common among tourism (31%), and those operating below pre-pandemic levels (34%).

Exports were more likely to have increased for businesses selling to the EU (20%) and outside the EU (22%) but decreased for those selling to England and Wales (35%).

Future prospects

More than three quarters of businesses (77%) were optimistic about their prospects in the next 12 months, while 22% were not (Figure 2.5)

Base: All buisinesses (2,726)

Variation in optimism

Optimism was higher among businesses in the Highlands and Islands (82% optimistic) than in the South of Scotland (77%) or rest of rural Scotland (75%).

Others that were more optimistic than average:

- large businesses (25+ staff) (90% optimistic),

- those operating above their pre-pandemic levels (92%), and

- striving for growth (83%).

The businesses which were less optimistic than average included:

- food and drink (67% optimistic, 32% not),

- sole traders (71% optimistic, 27% not) and other small businesses (1-4 staff) (75% optimistic, 24% not),

- those in remote rural areas (74% optimistic, 25% not), and

- operating below pre-pandemic levels (63% optimistic, 37% not).

Growth aspirations

Just over a third (37%) of businesses were striving for growth while half (50%) were content with their current level of performance. Around one in ten (12%) wanted to downsize (Figure 2.6).

Base: All buisinesses (2,726)

Variation in growth aspiration

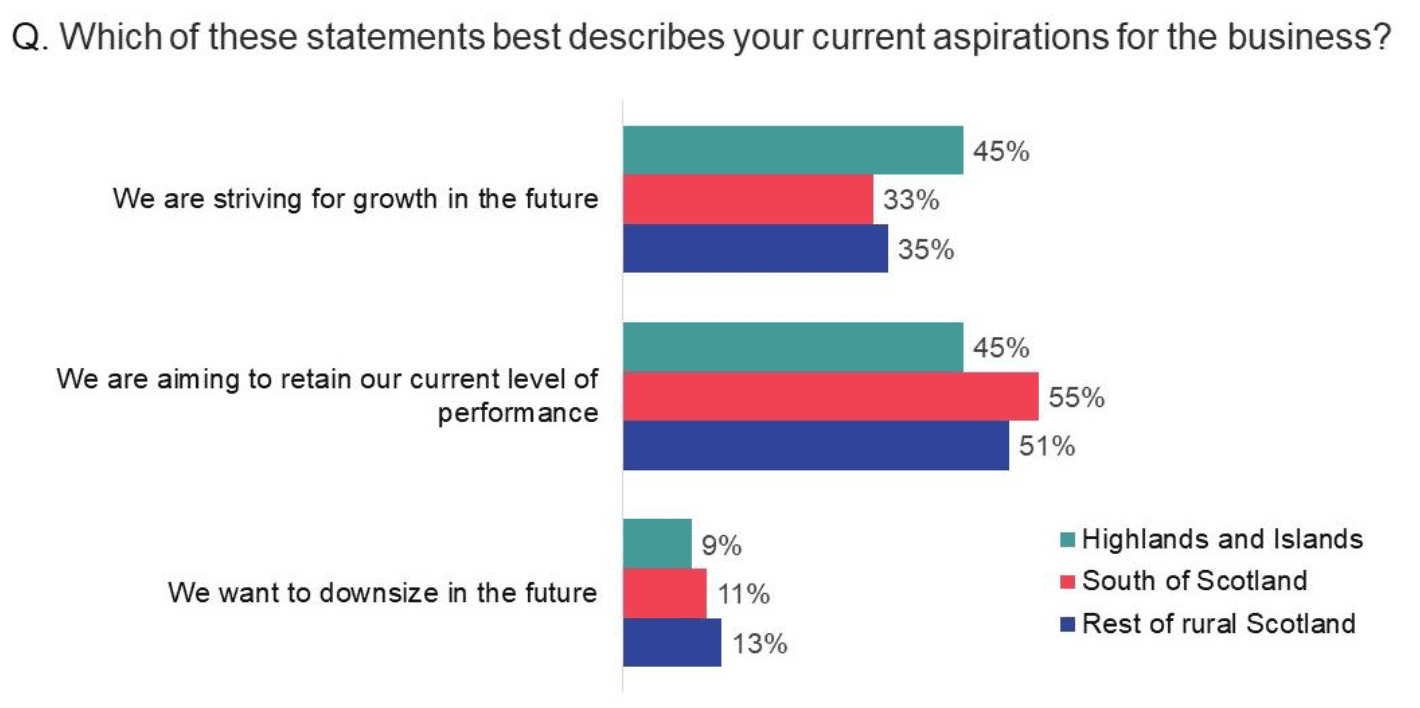

As with economic confidence and business optimism, growth aspirations were higher among businesses in the Highlands and Islands than in the South of Scotland and rest of rural Scotland (Figure 2.7).

Base: All buisinesses in Highlands and Islands (1,003), South of Scotland (602) and the rest of rural Scotland (1,121)

In terms of further variation:

- Tourism businesses were more likely than average to be striving for growth (49%), while food and drink were more likely to want stability (57%) and financial and business services to want to downsize (19%).

- Larger businesses (25+) were more likely to want growth (62%) while small businesses with 1-4 staff were more likely to want to downsize (12%).

- Growth aspirations were higher than average among businesses importing from (45%) and exporting to (48%) international markets.

Contact

Email: socialresearch@gov.scot