Climate change duties: statutory guidance for public bodies

Statutory guidance to support public bodies in implementing their climate change duties under the Climate Change (Scotland) Act 2009.

4. Putting the duties into practice

This chapter focuses on how public bodies can put the climate change duties into practice in a proportionate and effective way, reflecting their size, functions, assets and influence. It outlines the importance of leadership, governance and mainstreaming.

Under the 2009 Act, the climate change duties must be met as public bodies exercise their functions. These functions include spatial and transport planning, service delivery, place making, investment, infrastructure and economic development, funding, regulation, education, community development and partnership facilitation. Through these, public bodies can exert a wide influence on emissions and climate action well beyond their organisational boundaries.

A whole systems approach

Climate change is a complex, systemic challenge requiring coordinated action across society to achieve a just transition to net zero and build resilience. Actions in one policy area can deliver co-benefits across others but can also create unintended consequences if not considered holistically. Whole systems approaches apply systems thinking to understand interdependencies, address root causes, and support collaboration across partners, emphasising long-term outcomes, social justice and power dynamics, and involving stakeholders in agreeing shared priorities, managing trade-offs and aligning actions.

Public bodies are well placed to work with communities and partners to reduce emissions, adapt to climate impacts and act sustainably while delivering wider social, economic and health outcomes. This requires collaboration across sectors and levels of government, supported by collective and adaptive leadership. Climate change strategies and route maps should balance strategic direction with flexibility for local solutions, encouraging innovation and learning so that effective approaches can be scaled.

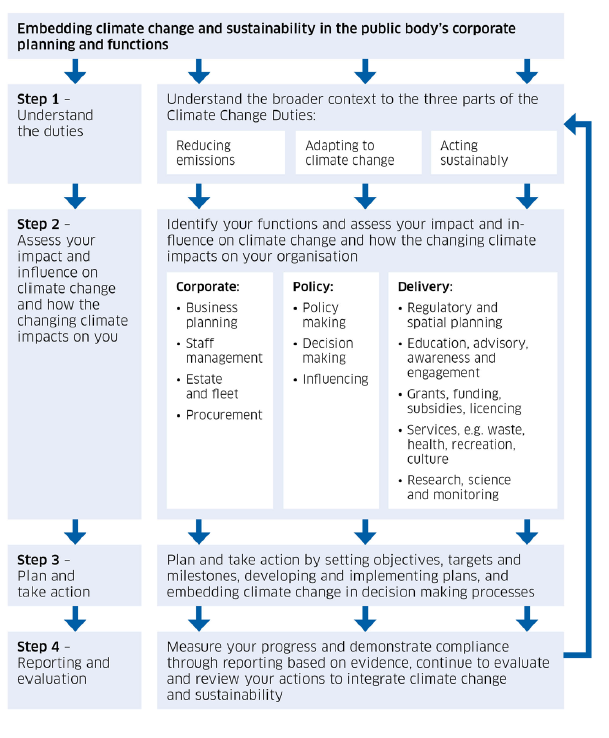

Implementing the climate change duties: a step by step method

Mainstreaming climate change and sustainability into business processes is essential. While many bodies already have mature arrangements in place, others may benefit from a structured approach. The step-by-step method illustrated in figure 1 below is intended as a flexible support tool, not a prescriptive model.

The overall outcomes are:

- climate and sustainability action embedded in corporate governance

- the public sector demonstrating leadership to wider society.

The process is cyclical, recognising that climate action is ongoing and iterative.

Embedding climate change and sustainability in the public body's corporate planning and functions

Step 1 - Understand the duties

Understand the broader context to the three parts of the Climate Change Duties:

- Reducing emissions

- Adapting to climate change

- Acting sustainably

Step 2 - Assess your impact and influence on climate change and how the changing climate impacts on you

Identify your functions and assess your impact and influence on climate change and how the changing climate impacts on your organisation

- Corporate:

- Business planning

- Staff management

- Estate and fleet

- Procurement

- Policy:

- Policy making

- Decision making

- Influencing

- Delivery:

- Regulatory and spatial planning

- Education, advisory, awareness and engagement

- Grants, funding, subsidies, licencing

- services. e.g. waste. health, recreation, culture

- Research. science and monitoring

Step 3 - Plan and take action

Plan and take action by setting objectives, targets and milestones, developing and implementing plans, and embedding climate change in decision making proce

Step 4 - Reporting and evaluation

Measure your progress and demonstrate compliance through reporting based on evidence, continue to evaluate and review your actions to integrate climate change and sustainability

Return to Step 1.

4.1 Leadership

Public bodies have a critical role in reducing emissions, supporting a just transition, and preparing for a changing climate. Leadership at all levels is essential to deliver these outcomes and inspire wider change.

Public bodies act as:

- corporate entities - managing estates, fleets, and staff

- service providers - influencing infrastructure, communities and behaviour

- anchor institutions - helping shape local economies and environments

- significant buyers - with leverage over supply chains and emissions

- partners and influencers - across regions and sectors

- trusted messengers.

By leading through their own actions, public bodies can model best practice, stimulate innovation, and build a culture that supports Scotland’s net zero ambitions; as well as delivering wider co-benefits such as improved population health, reduced inequalities, cleaner air and enhanced biodiversity.

Key actions

Public bodies should:

- commit publicly to climate action - Publish a formal, visible commitment to meet climate change duties and net zero targets. Transparency strengthens accountability and influences staff, stakeholders, suppliers, and service users.

- integrate climate governance into corporate systems - Embed responsibility for climate and sustainability action within existing governance, risk, and reporting frameworks.

- embed climate change and sustainability in risk management - Identify, assess, and manage climate-related risks and opportunities through established corporate risk management systems.

- reflect climate priorities in strategies and reporting - Include climate action and sustainability in corporate plans, annual reports, and statutory plans. Set measurable targets and report progress.

- make climate and sustainability action a corporate priority - Ensure leadership commitment is backed by investment, resourcing and performance management.

- mainstream climate considerations -Integrate the “climate and sustainability question” into all major decisions, policies, and investments.

- collaborate with partners - Work with other public bodies and sectors to share learning, maximise efficiency, and deliver multiple outcomes across sustainability, health, equity, and economic development.

- build organisational capability - Embed climate and sustainability within learning and development for all staff.

Corporate leadership and governance

Strong internal leadership and effective governance is vital to ensure that climate commitments translate into meaningful action and long-term change. The importance of having senior leadership buy-in to drive climate action and embed climate thinking into decision making cannot be overstated.

Public bodies should:

- train leaders and managers

Provide climate, carbon, biodiversity, and sustainability training for all managers, and appropriate climate leadership training for senior decision-makers.

- ensure senior accountability

Ultimate responsibility for meeting the climate change duties should sit with the most senior leadership level, with accountability clearly identified in roles. Bodies should publish their climate governance arrangements in corporate strategies or equivalent documents.

- align strategy and investment

Ensure major financial and strategic decisions are consistent with net zero targets and adaptation needs, and support sustainable development.

- treat climate change and sustainability action as core deliverables, and include associated indicators in their core performance framework

Embed climate considerations across all functions and link actions to broader outcomes such as health and wellbeing. Key performance indicators (KPIs) should be directly linked to organisational climate strategies and action plans.

- assess their organisation’s readiness and maturity in responding to the climate emergency

Assessments should identify strengths, gaps and priorities for action. Useful tools include Leader’s Climate Emergency Checklist and Leader’s Climate Adaptation Checklist.

- engage internal and external auditors to drive improvement

Record and evidence how climate considerations influence decisions; and promote openness and fairness to maintain public trust.

Risk and opportunity

Risk management enables public bodies to plan for, respond to, and benefit from climate-related change. Climate risks should be identified, assessed, and managed within existing corporate risk frameworks and escalated as appropriate.

Examples of climate-related risks:

- compliance – breach of environmental regulations due to extreme weather impacts (e.g. wastewater discharge after heavy rainfall)

- legal – failure to act on emissions reduction, leading to potential legal challenge

- reputational – setting but not delivering on net zero targets, damaging public trust

- strategic – ignoring climate impacts in long-term estate planning, leading to unfit facilities

- financial – increased costs from damage repair; lack of investment in adaptation measures to build resilience

- operational – disruption to services or supply chains from extreme weather events

- physical – damage to land, assets or infrastructure (e.g. wildfire loss, flooding).

Public bodies should also recognise and aim to maximise opportunities, such as innovation, local employment, skills development, improved resilience and cost savings through proactive adaptation planning and action.

Risk appetite will vary by organisation and function, but all public bodies should ensure that climate risks and opportunities are consistently captured, reviewed and managed. Refer to Chapter 6 and Annex G for further guidance on the assessment of climate risks.

Further guidance:

- Scottish Public Finance Manual

- UK Government Management of risk in government: framework

- HM Treasury: The Orange Book – Principles and Concepts of Risk Management.

4.2 Taking climate into account in decision making

It is essential that public bodies embed climate change into decision making, both to comply with the 2009 Act and to avoid unintended consequences such as increased emissions, lock-in of high carbon behaviour, or maladaptation. Decisions must be transparent and defensible, showing how climate considerations were weighted.

It is important to develop policy and take decisions with an awareness that our climate is changing. Appraisal should account for climate impacts, where significant, and respond to them where cost-effective to do so. Otherwise decisions will not necessarily be based on a full understanding of how public value can best be delivered over time.

A mix of qualitative and quantitative methods can help integrate climate thinking into decisions. Organisations may adopt one or a combination of these approaches depending on their functions and the nature of the decision.

Core appraisal frameworks

- Scottish Public Finance Manual and HM Treasury’s Green Book Both provide the foundation for appraisal and evaluation of public funds. They encourage appraisal that accounts for climate impacts (physical and transitional), and consider how value is delivered over time under changing conditions.

- The Green Book supplementary guidance on Accounting for the Effects of Climate Change supports the identification of climate risks, and aids in designing and appraising adaptation measures.

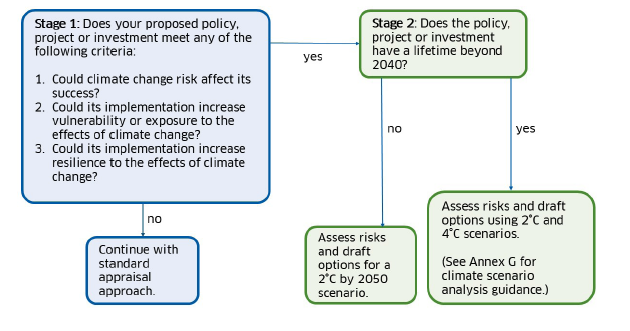

The Climate Change Committee advises policymakers to plan for 2°C by 2050, and to assess the risks for 4°C of global warming by 2100.

Public bodies should use the decision tool in figure 2 to take a proportionate approach to the appraisal of policies, programmes, and projects, in line with CCC advice.

Stage 1: Does your proposed policy, project or investment meet any of the following criteria:

1. Could climate change risk affect its success?

2. Could its implementation increase vulnerability or exposure to the effects of climate change?

3. Could its implementation increase resilience to the effects of climate change?

No: Continue with standard appraisal approach.

Yes:

Stage 2: Does the policy projct or investment have a lifetime beyond 2040?

No: Assess risks and draft options for a 2°C by 2050 scenario.

Yes: Assess risks and draft options using 2°C and 4°C scenarios.

(See Annex G for climate scenario analysis guidance.)

Embedding climate in impact assessments

Many statutory impact assessments (e.g. SEA, EIA) already allow for environmental and climate impacts (see Annex B). However, many decisions fall outside those statutory scopes. Public bodies should ensure that internal impact assessment processes explicitly include climate.

- Strategic Environmental Assessment (SEA)

For plans, programmes or strategies with likely significant environmental effects, SEA is required. Whether or not a full SEA is needed depends on the significance of effects (in scale, sensitivity, certainty). Screening decisions should be justified.

- Environmental Impact Assessment (EIA)

EIA forms part of the Development Planning process, and is a means of drawing together an assessment of the likely significant environmental effects arising from a proposed development. Whether an EIA is required or not is set out in regulation.

- Climate Change Impact Assessment (CCIA)

CCIA is a flexible, internal assessment approach (non-statutory) that can be introduced early in project, policy or procurement stages, and iterated over time. It helps to:

1. identify, quantify (where feasible) and record potential climate risks and emissions impacts

2. minimise negative effects (e.g. emissions, maladaptation, compounded inequalities)

3. maximise opportunities for positive interventions and outcomes (e.g. cleaner air, reduced inequalities, improved resilience and biodiversity).

Benefits of CCIA include: making climate impacts visible at decision points; providing evidence to justify choices; helping mainstream climate across organisations; and supporting compliance with climate change duties and net zero and adaptation goals.

Further guidance:

- guidance on SEA is available from Scottish Government, NatureScot, SEPA and Historic Environment Scotland

- how to develop a Climate Change Impact Assessment Framework, Sustainable Scotland Network

- Annex B for further information and resources on impact assessments.

Financial decision making

Financial choices (capital and resource budgets, procurement, business cases) must reflect climate priorities if mitigation and adaptation aims are to be credible.

Key practices include:

- treat climate as a corporate priority – align major investment and resource allocations with climate objectives

- involve finance teams early – their expertise is vital in embedding climate into budgeting, reporting, and monitoring.

Public bodies subject to the statutory reporting duty (see section 8.1 and 8.2) should include information on their financial decision-making processes and alignment with net zero and adaptation action in their annual public bodies climate change duties (PBCCD) reports. Following a robust process, including use of the tools and methodologies outlined below or others, can help demonstrate compliance with the climate change duties.

Tools and methodologies to aid financial design making

As low-carbon or resilient options often carry higher upfront costs, a ‘spend to save’ mindset is needed. It is important that carbon and wider sustainability factors are taken into account when making decisions, to ensure that best value over the useful life of the asset is achieved. Decision makers should include carbon, climate risks and potential impacts and co-benefits in appraisals.

Some useful tools and methods include:

- carbon budgets (can be used at project, department or organisational level)

- including the cost of carbon in business cases

- whole life carbon assessment frameworks, e.g. Net Zero Public Sector Buildings Standard, UK Net Zero Carbon Buildings Standard, RICS whole life carbon assessment, PAS 2080 (2023)

- Institute for Climate Economics (I4CE) climate assessment methodology for local authority budgets

- Sustainable Procurement Tools and buyer guides

- UK Co-benefits Atlas

- NatureScot’s Natural Capital Tool

- Climate Change Impact Assessment as part of financial appraisal.

Refer to Annex M – Resources for more tools and sources of information.

Below are selected sources to support climate-aware business cases, adaptation finance, and integration of private or blended finance approaches.

Further guidance and tools (for project development, business cases and finance):

- Scottish Futures Trust (SFT) – Net Zero Buildings - Provides guidance on developing business cases, infrastructure procurement, retrofit programmes, and enabling private investment in net zero projects.

- Net Zero Public Sector Buildings Standard - Resources include sector guides, tools templates and case studies.

- Adaptation Scotland – Adaptation Finance - Resources include a guide to adaptation finance, an insights and opportunities report, and guidance on developing adaptation finance business cases.

- ClimateXChange – Opportunities for Financing a Climate-Resilient Scotland - Event report summarising Scotland’s adaptation finance landscape, gaps, and models for mobilising investment across sectors.

- Sustainable Scotland Network (SSN) – Public sector resources - Offers templates, case studies, and guidance for developing internal climate tools, climate change impact assessments and adaptation planning.

- Audit Scotland – Climate Change Reports - Highlights how public bodies can integrate climate risk into financial governance, performance reporting and accountability.

- UK Government – Business case guidance for projects and programmes - This guidance is supplementary to the Green Book.

Contact

Email: climate.change@gov.scot