Climate change duties: statutory guidance for public bodies

Statutory guidance to support public bodies in implementing their climate change duties under the Climate Change (Scotland) Act 2009.

Annex C: Carbon Management Plan template

The purpose of this template and guidance

Who is this document for?

This carbon management plan (CMP) template and guidance is to help smaller and less complex public bodies that may have limited capacity to measure, monitor and report on their greenhouse gas (GHG) emissions, and that have relatively simple corporate emissions inventories and influence over these emissions. It is designed to ensure all public bodies tackle the essential emissions relating to their operations, and to highlight the importance of focusing on the use of public body functions to influence change more widely.

The template has been designed to align with the mandatory public bodies climate change duties (PBCCD) reporting. It may be appropriate for bodies that are not classed as ‘major players’, and are not subject to the reporting duty, to simplify the template to reflect their more limited emissions and influence. For example, it may be appropriate for such bodies to focus on scope 1 and 2 emissions initially.

In all cases, public bodies should use the template as a starting point and develop it to reflect their own needs and circumstances.

Throughout, the term ‘carbon’ is used for ease, as other greenhouse gases are typically reported in terms of carbon dioxide equivalent.

Why have a Carbon Management Plan?

A CMP serves as a strategic and action-oriented document to help public bodies understand, measure, manage and reduce their corporate greenhouse gas emissions.

What are the key parts of a Carbon Management Plan?

As outlined in this guidance and template, the key parts of a Carbon Management Plan are:

- overview of the organisation: its size, key activities and functions

- governance and management arrangements, including how the CMP fits into corporate management and governance structures and processes. This section should also include a signed declaration verifying that the CMP information is accurate and formally signed off by an appropriate senior manager. It should also note how often the CMP will be reviewed

- identification of key stakeholders and partners

- key drivers and objectives of the CMP, including reference to key policy and organisational priorities

- baseline year for the CMP, from which emission reductions will be monitored

- clear boundaries of which emission sources (relating to organisational functions) will be included in the CMP, and any exclusions

- collating an emissions inventory based on the emission sources within the agreed boundary

- emissions reduction targets, overall and activity specific

- a register of emission reduction projects

- a visualisation of the decarbonisation pathway

- monitoring and reporting the impact of the emissions reduction projects and setting out the expected impact of projects in the years ahead

- Publishing annual reports on progress.

Statutory public bodies climate change duties reporting

Many sections of this Carbon Management Plan correspond to the public bodies climate change duties reporting (PBCCD report) template as defined in Schedule 2 of The Climate Change (Duties of Public Bodies: Reporting Requirements) (Scotland) Order 2015, as amended. This guidance indicates where the Carbon Management Plan relates to the PBCCD report template, using the relevant Part and table or question numbers.

Please refer also to the public bodies climate change duties reporting guidance on how to fill out the annual report which can be found at SSN reporting resources, where applicable.

Carbon Management Plan Template

1. Public Body Overview

Provide a general description of the organisation stating key information such as when established, size or scale, current practices and key functions. Provide a brief description of your offices or physical estate, budget, number and type of buildings used, number of staff, if you operate any fleet vehicles etc.

This information can be used to answer relevant questions in Part 1 of the PBCCD report.

2. Governance and management

Explain the arrangements in place to provide a robust system of governance and management of the CMP, covering decision making and leadership.

- Governance refers to arrangements at Board (Non-Executive) level

- Management refers to senior executive functions such as Chief Executives, Finance Directors and Corporate Management Teams or equivalent

- Responsibility for delivering elements of the plan will lie with named roles in the organisation (e.g. Head of Estates), and these should be stated, along with the person with ultimate responsibility, usually the Chief Executive or equivalent. If such arrangements lie outside the organisation, they should also be included here.

Include:

- the period covered by the CMP (typically three to five years)

- the date the next iteration of the CMP is required

- the frequency for reviewing this CMP – this should not be less than annually

- the date the next review is due.

Enter relevant information in Part 2 (a and b) of the PBCCD report.

3. Drivers and motivation for change

Set out a brief overview of the key drivers and objectives of the CMP. This could contain reference to:

- key strategy and policy commitments of the body

- an overview of how the CMP supports other organisational objectives

- key drivers within the public sector and motivations of leaders and managers

- reference to the financial and operational benefits of the CMP

- wider outcomes and co-benefits that the CMP aims to help deliver or support.

Reference should also be made to the public bodies duties in section 44 of the Climate Change (Scotland) Act 2009:

- Mitigation – in exercising their functions, public bodies must act in the way best calculated to contribute to delivery of Scotland’s emissions reduction targets. In this context, ‘targets’ includes the net zero target of 2045, and the five-yearly carbon budgets.

- Adaptation – in exercising their functions, bodies must act in the way best calculated to help deliver the National Adaptation Plan. The Scottish National Adaptation Plan 2024-2029 (SNAP3) addresses climate impacts, guided by the third UK Climate Change Risk Assessment (CCRA3). CCRA3 was based on the Independent Assessment of UK Climate Risk and national summaries, including the National Summary for Scotland that assesses 61 climate change risks and opportunities for Scotland.

- Acting Sustainably – in exercising their functions, bodies must act in the most sustainable way. Acting sustainably requires public bodies to align with wider sustainable development goals, such as the United Nations Sustainable Development Goals (SDGs). Scotland's National Performance Framework aligns with UN SDGs, tracking progress through 81 indicators, including carbon footprint, greenhouse gas emissions, natural capital, renewable energy, waste, biodiversity, active travel, public services, and local influence.

The Climate Change (Duties of Public Bodies: Reporting Requirements) (Scotland) Order 2015, as amended, mandates annual reporting for listed bodies.

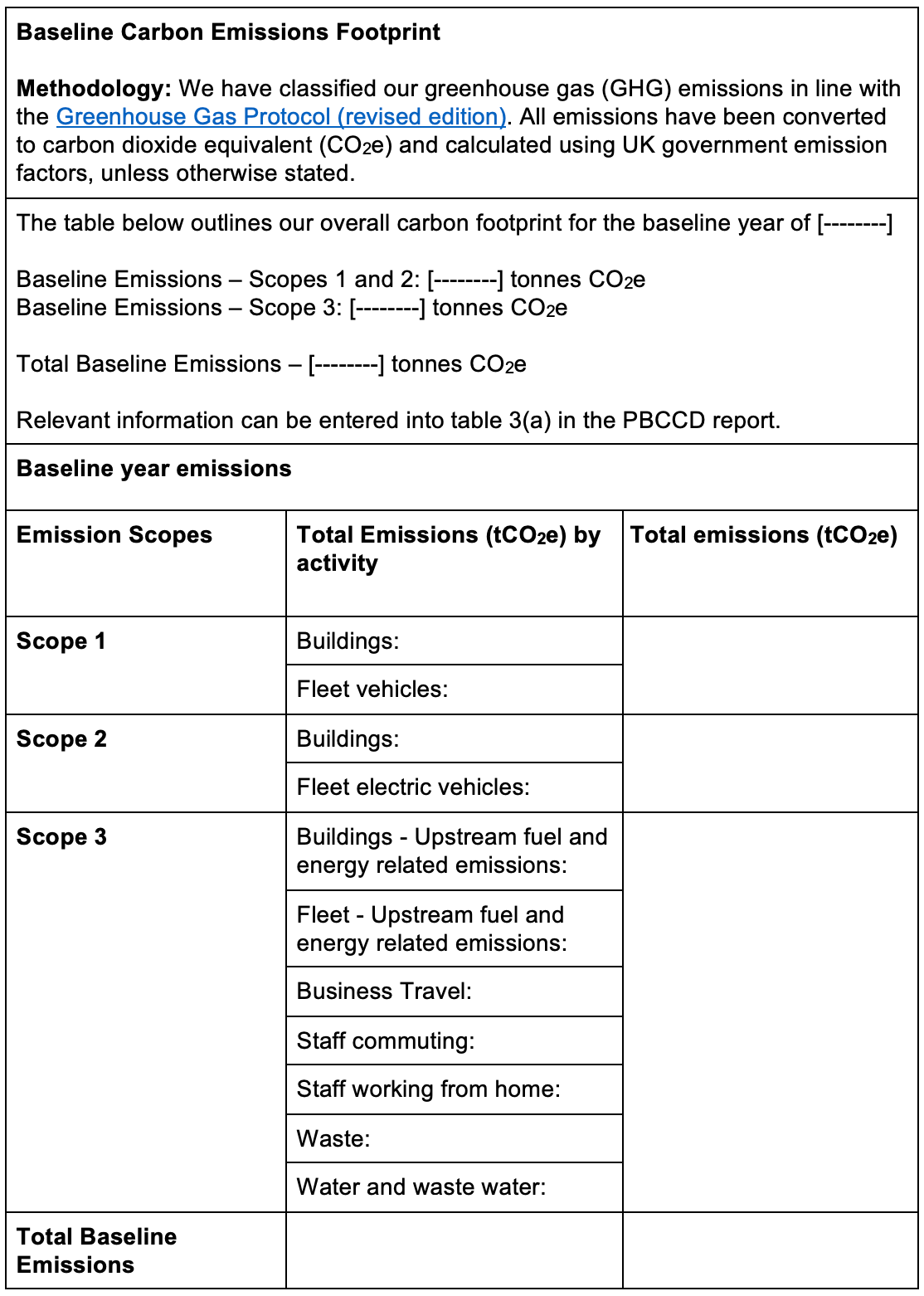

4. Baseline period

The baseline year for this Carbon Management Plan is financial year [--------]

The date included here should be the period chosen as the first estimation of your emissions.

Information on establishing a baseline can be found in the SSN Reporting Guidance available from the Reporting Resources page and from the GHG Protocol.

5. Organisational boundary

The CMP should clearly set out the organisational boundary used for monitoring and managing emissions. A basic CMP should, where applicable, have the following organisational boundary of emission sources, grouped by standard carbon accounting protocol scopes. These could be included in a table, as illustrated below.

Bodies may choose to report on other sources of emissions, and these should be included as appropriate. The table is intended to illustrate a starting point only.

| Operational area or activity | Source of emissions* | Scope designation |

|---|---|---|

| Buildings** | Gas use, primarily from heating | 1 |

| Other heating fuels, e.g. oil, biomass | 1 | |

| Mains electricity | 2 | |

| Fugitive gases, where applicable. Most likely to be refrigerant gases from cooling equipment or heat pumps | 1 | |

| Upstream energy and fuel-related emissions, i.e. those associated with the extraction, refining and transport of fuels, and transmission and distribution losses | 3 | |

| Fleet vehicles owned or operated by the public body | Fuel used (e.g. petrol, diesel) in fleet vehicles | 1 |

| Electricity used by EVs (electricity used to charge vehicles may be included within the overall building consumption if not separately metered) | 2 | |

| Upstream energy and fuel-related emissions, i.e. those associated with the extraction, refining and transport of fuels, and transmission and distribution losses | 3 | |

| Business travel | Personal vehicles used for business (i.e. ‘grey fleet’) | 3 |

| Public transport used for business | 3 | |

| Flights taken for business | 3 | |

| Overnight stays taken for business | 3 | |

| Staff commuting | Staff vehicle fuel used in commuting Public transport used in commuting | 3 |

| Staff working from home | Number of FTEs working from home or actual energy and fuel use reported by staff while working at home | 3 |

| Waste | Waste generated by the public body | 3 |

| Water | Water supply or consumption; and related waste water treatment | 3 |

*Annex H provides information on common data sources for some of the emissions listed. Refer also to the GHG Protocol for further guidance.

**Note: certain public bodies may not have direct control over their buildings and services if they lease or share space with another body. Refer to Annex H.

6. Setting a baseline carbon emissions inventory

Based on the agreed boundary, a baseline inventory of emissions should be calculated. The table above illustrates a simplified way of presenting this. This can be calculated using the emissions reporting tables in Part 3 of the PBCCD report template, tables 3(a) and 3(b). These tables require information on the consumption of gas, electricity and fuels, as well as information on business travel modes and distances, and data on waste generated and water consumed.

Once these tables have been completed, a CMP summary table, as illustrated above, can be published.

To calculate the emissions relating to each scope and area of activity, table 3(b) in Part 3 of the PBCCD report template can be used as a tool. This template is publicly available and can be used by all public bodies, not just those subject to the mandatory reporting duty.

The PBCCD report template will calculate emissions and allocate scopes based on consumption data entered against each type of activity. Table 3(b) can be used within the CMP to provide a more detailed overview of emissions by activity, if required.

Bodies may wish to include consumption data in their baseline assessment as well as emissions (e.g. kWh of electricity or car km driven). For example, if in the future mains electricity or road fleet are fully decarbonised, the emissions associated with these sources will drop to zero. However, bodies will also wish to monitor the data from a demand reduction perspective. Considering this aspect at the start and building consumption data into the baseline position will aid bodies in the longer term.

7. Targets and milestones

The body’s overarching CO2e emissions reduction target is [absolute target, percentage reduction target or net zero target] of [------------] by year [--------].

The public body should establish an overarching net zero carbon target, in line with the Scottish Government target of net zero by 2045 where feasible, ideally earlier, covering emissions from scopes 1 and 2.

They should also set appropriate scope 3 targets including a target for reducing car kilometres travelled and targets related to waste and recycling. Targets should be set for each source of emissions, relating to the various activities, as illustrated in the table below. Targets should include a date and, generally, a baseline year - refer to section 5.3.4 in the guidance above for further information on target setting.

The targets included in the table below are intended to be illustrative examples only. Bodies should set evidence-based targets appropriate to their own body, assets, location and operational activities.

| Operational area or activity | Source of emissions by activity | Scope | Target* |

|---|---|---|---|

| Buildings | All | - | All owned buildings to be energy efficiency rating band C or better by 2038. |

| Gas | 1 | 80% reduction in emissions by 2035, from [the baseline year]. Zero emissions by 2040. | |

| Other heating fuels | 1 | Zero emissions by 2038. | |

| Electricity | 2 | 20% reduction in total electricity consumption by 2040. By 2040, 25% of total electricity consumed is to be self-generated using on-site renewables. | |

| Vehicles owned by the body | All | - | A percentage reduction in car use by a given year against a defined baseline (based on local circumstances). |

| Fuel used (petrol, diesel) | 1 | 50% of vans under 7.5t to be zero emission by the end of 2027. 30% reduction in fleet emissions by end of 2027 based on 2020 baseline. Fleet to be fully electric by 2030. | |

| Business Travel | All | 3 | 25% reduction in total business travel emissions by 2030. |

| Personal vehicles (‘grey fleet’) | 3 | A percentage reduction in car use by a given year against a defined baseline (based on local circumstances). | |

| Public transport | 3 | 10% increase in the number of journeys taken using public transport by 2030. | |

| Flights | 3 | Zero domestic flights to be taken by 2028 (within mainland UK). 25% reduction in emissions from non-domestic flights by 2028. | |

| Staff commuting** | All | 3 | 25% reduction in total staff commuting emissions by 2030. |

| Active travel to work | 3 | 25% of journeys to be made by active travel by 2030. | |

| Public transport travel to work | 3 | 40% of journeys to be made using public transport by 2030. | |

| Private vehicle travel to work | 3 | A percentage reduction in car use by a given year against a defined baseline (based on local circumstances). All owned sites with car parking to provide at least 2 EV charging points accessible to staff by 2030 (where feasible). | |

| Working at home** | Energy efficiency actions at home | 3 | Home energy efficiency training to be added to staff induction process by 2026; and delivered to all staff by 2028. |

| Waste | Weight or volume of waste generated | 3 | 25% reduction in the [weight or volume] of waste generated by 2030. |

| % of waste recycled | 3 | 80% of waste to be recycled by 2030. | |

| % of waste to landfill | 3 | Zero waste to landfill by 2028. | |

| Water | Volume of water used | 3 | 25% reduction in the consumption of water by 2030. |

* Targets can take various forms. For scopes 1 and 2, these should focus on carbon reductions, e.g. a 75% reduction in the scope 2 emissions from electricity by 2030. Scope 3 targets may focus on carbon emissions, or may relate to the activity, e.g. 70% of waste to be recycled by 2030; 50% of business travel journeys to be taken using active travel or public transport by 2035. Refer to section 5.3.4 in the guidance above for further information.

** Note: the number of staff commuting and the number of staff working at home are related. Targets should encourage both low carbon commuting (walking, cycling, public transport) and, only where appropriate, working from home (which is typically lower carbon than commuting). Public bodies should encourage staff to adopt good practice energy efficiency and low carbon behaviours while working at home in order to minimise emissions generated while working at home.

Targets should be set for overall emissions reductions, as well as sub-targets on reducing demand (energy efficiency, etc.) and greening supply (shifting to low carbon alternatives) in each of the activities that are sources of emissions.

Targets should be set in line with policy objectives set by the Scottish Government or agreed collectively by public bodies by sector.

Targets should be set out and reported annually in table 3(d) in Part 3 of the PBCCD report.

The body may wish to include a route map in this section, to provide a clear visualisation of the pathway to net zero, including key milestones, targets and headline actions.

8. Policies and projects

To meet targets public bodies should develop and implement policies and projects that support emission reductions. Each policy and project should be carbon impact assessed to calculate the likely carbon reduction impact. Public bodies need to use these reduction estimates to assess the range of policies and projects needed to meet agreed targets.

Within this section, outline why you have chosen these specific policies and projects. Outline those which are directly related to meet your reduction targets, describe how you are planning on implementing them, key stakeholders, and identify any barriers or critical dependencies which could prevent their implementation. Not all projects have to be directly related to emissions reduction, they could be around behavioural change, capacity building or education (i.e. enabling measures).

More mature bodies could also include information on how the other two climate change duties have been taken into consideration in relation to the policy or project. For example, how the impacts of the changing climate have been taken into account in the design and specification of a building-related project; and how this will contribute to the body’s resilience. Bodies could also consider wider benefits that the project or policy may help achieve, such as cleaner air, improved flood resilience or providing local employment; and could reference the impact assessments carried out.

Taking this approach may encourage more holistic thinking, and can help demonstrate compliance with all three of the climate change duties.

Policies and projects register

The policies and projects included in the example register below are intended to be illustrative examples only. Bodies should plan and implement approaches and measures appropriate to their own body, assets, location and operational activities. Including the expected source of funding (e.g. self-funded through the capital investment programme or reliant on external grant funding) can highlight critical dependencies and aid with budget planning and delivery.

More mature bodies could consider adding additional columns relating to, for example, adaptation outcomes and wider co-benefits that the project will contribute to; and how the project may help to address inequalities or socio-economic disadvantage.

| Project name | Description | Direct emissions reduction or enabling measure | Emissions Scope addressed | Predicted carbon reduction (tCO2e) | Target completion date | Funding source |

|---|---|---|---|---|---|---|

| Example: EV charging infrastructure | Installation of EV charging points for fleet vehicles at all sites | Enabling measure | 1 | Not applicable | 2025-26 | Combined: Self-funded and grant funding (e.g. Transport Scotland funding) |

| Example: EV charging infrastructure | Install at least 2 EV charging points for staff vehicles at all owned sites (where feasible) | Enabling measure | 3 | Not applicable | 2029-30 | Self-funded |

| Example: Renewable electricity | Install solar PV panels at HQ building | Direct measure | 2 | 5 | 2027-28 | Self-funded |

| Example: Clean heating in buildings – phase 1 | Replace gas heating in HQ building with air source heat pump | Direct measure | 1 | 150 | 2029-30 | Combined self-funding and external funding: e.g. GPSEDS |

| Example: Clean heating in buildings – phase 2 | Replace oil heating in main laboratory building and 2x regional offices with air source heat pumps | Direct measure | 1 | 75 | 2032-33 | Regional offices: self-funded Main building: combined self-funding and external funding: e.g. GPSEDS |

Annual reporting of policies and projects

Carbon reduction policies and projects should be reported annually in mandatory public bodies climate change duties reports.

- Estimated total annual carbon savings from all policies and projects implemented by the body in the reporting year. Use PBCCDR table 3(e).

- Detail the top carbon reduction projects carried out in the reporting year:

provide details of the projects which are estimated to achieve the highest carbon saving during the reporting year. Use PBCCDR table 3(f).

- Carbon reduction projects for the year ahead: anticipated annual carbon savings from all projects to be implemented by the body in the year ahead. Use PBCCDR table 3(h).

- Estimated decrease or increase in emissions from other sources in the year ahead. If the body’s corporate emissions are likely to increase or decrease for any other reason in the year ahead, provide an estimate of the amount and direction. PBCCDR table 3(i).

- Total carbon reduction project savings since the start of the year the body used as a baseline for its carbon footprint. PBCCDR table 3(j).

9. Other factors influencing emissions

The other factors that have influenced the body’s emissions in the past or are expected to in the future are:

Sometimes emissions will increase or decrease due to other factors influencing the operations of the organisation. This could include such things as significant changes in the scale of staffing, operations and budgets, changes in office locations or number of buildings, or ways of working. These contextual influences on emissions should be reported within the CMP; and also reported in mandatory public bodies climate change duties reports (PBCCDR table 3(g)).

If significant change takes place, organisations may need to recalculate their baseline emissions and overhaul their CMP.

10. Monitoring and reporting

Governance and management of the Carbon Management Plan:

Reporting arrangements for the Carbon Management Plan:

Internal:

External:

An outline of how the CMP is monitored and reported on should be provided. This can be done as narrative text as a minimum, but can also include diagrams or tables to help explain structures and processes to a range of stakeholders.

Within this section bodies should make it clear how the CMP will be reported on both internally and externally. Bodies should report on progress and performance through their corporate reporting suite. They should aim to report publicly on progress on an annual basis as a minimum. Reports could be made available on the body’s website, if appropriate, or information could be published on a webpage.

Example text:

“We collect data from multiple internal and external sources to calculate our operational emissions. This includes our building facilities management contractors, travel agent, and our finance and operational departments. Staff commuting is captured via annual employee surveys…. Data to measure the progress of our CMP is collected quarterly, with updates provided to relevant working groups and the organisation’s Board, as well as communicated externally via the organisation’s website, and in the annual report and accounts.”

As referenced throughout this guide the body, where relevant, should also use its mandatory PBCCD report as a key data reporting and publication mechanism. The PBCCD report requires reporting of Governance, Management and Strategy in Part 2, as well as detailed annual reporting of emission, targets, policies and projects. The CMP should feature clearly within the body’s annual mandatory reports.

11. Verification and senior leadership declaration

Verification of the Carbon Management Plan and related reports has been done using the following:

Verification of CMP data and reporting is good practice. For CMPs, this verification could be done internally, by working with internal auditors, by working collaboratively with peers in the public sector to undertake peer-to-peer review, or by engaging a third party to provide a verification or external audit service. For most smaller public bodies, internal auditing of data should be sufficient and cost-effective. Peer-to-peer review offers benefits in terms of knowledge sharing and capacity building.

If verification is undertaken, make reference to this in a statement in your Carbon Management Plan and in any progress reports.

Carbon Management Plans should also contain a formal senior level declaration from the organisation’s Chair or Chief Executive endorsing the Carbon Management Plan and confirming that all information in the CMP is accurate and agreed.

Leadership Declaration

I confirm that the information in this report is accurate and provides a fair representation of the body’s performance in relation to carbon management.

Name:

Position:

Organisation:

Date:

Next review due date:

Contact

Email: climate.change@gov.scot