Negative Emissions Technologies (NETS): Feasibility Study

This study estimates the maximum Negative Emissions Technologies (NETs) potential achievable in Scotland, 2030 - 2050.

2. The relevance of NETs for Scotland

2.1 Introduction

This section highlights the issues which need to be considered when developing NETs pathways for Scotland. Important considerations include availability of bioresources, availability of CO2 storage, future demand for NETs, improvements over time in the performance of CO2 capture systems, future demand for power and renewables, GHG accounting, MRV and certification procedures. Each of these considerations and their relevance to Scotland are discussed below.

It should be noted that this information is gathered from a review of the latest literature sources and publications and from the stakeholder consultation (see Appendix 3 of the technical appendices document for a summary of the stakeholder consultation which was undertaken as part of this study).

The considerations highlighted in the section below are combined with the methodology described in Section 3 and 4 to develop the pathways described in Section 5.

2.1.1 Key Findings

- Current support for biogenic carbon emitting sites: Existing support is provided to current biogenic carbon emitters through the Renewable Obligations (RO) and Renewable Heat Incentive (RHI) schemes. New incentives will be necessary once these schemes end to ensure their continued operation.

- Transition of biogas sites: Biogas sites constructed after November 2021 will lose support after the RO scheme concludes. To maintain fiscal support, these sites may need to transition to biomethane production if a GGR support scheme is established. This transition can contribute to NETs if carbon is captured and stored during the AD upgrading process.

- BECCS Biomethane sites: To prevent operational disruptions at BECCS biomethane sites, grid agreements must be in place to minimise curtailment.

- BECCS EfW sites: It is likely that CCS will be installed onto EfW sites, regardless of whether additional fiscal support is provided by the government. This is out of necessity, to ensure that these sites are awarded planning permission and meet revised emission regulatory requirements.

- Deployment challenges for NETs: BECCS Power, BECCS Industry, DACCS, and BECCS Hydrogen all face challenges due to higher costs and lower technical maturity, making deployment at large scale unlikely without significant government support.

- BECCS Industry sites: Industrial sites emitting biogenic carbon, like pulp and paper manufacturers, will be compelled by regulations to implement carbon capture to meet planning permission requirements and comply with new emission regulations.

- Carbon capture in brewing and distilling: Breweries and distilleries might adopt carbon capture due to demand for captured carbon in their operations, such as carbonating drinks. This would not be considered NETs.

- Interest in Biochar: Stakeholders are expressing significant interest in biochar due to its versatility across various sectors. Deployment could be substantial, even without additional support.

- Availability of bioresources: The availability of future bioenergy resources could be a limiting factor behind the deployment of BECCS and biochar technologies. In order to maximise the total bioenergy available in Scotland (13.2 TWh for dry and 3.1 TWh for wet bioresources by 2045), the growth in bioenergy crops must be supported in the Bioenergy Action Plan, Biomass Strategy or potentially an agriculture and land use strategy.

- MRV framework for NETs: To qualify as a NET, captured CO2 must either be permanently stored underground or used in industries where CO2 becomes a permanent part of the product, such as concrete curing or green polymers. To account for this carbon, an appropriate MRV framework must be developed. This is ongoing and should consider the entire life cycle of a NET process, including biomass sources, electricity and heat sources, and the fate of captured CO2.

- Competition and Market Demand: Industry discussions reveal that existing biomethane and fermentation sites could implement CCS, but CO2 is likely to be utilised rather than stored. Additional incentives are required to shift this carbon to permanent storage. Competition between BECCS Power and other low-carbon electricity sources is also possible.

- CCS as an enabler of NETs: The development of CCS industry and infrastructure is considered the cornerstone on which the NETs industry depends upon. Therefore, establishing CCS demonstration projects now is crucial to making the technology available in time.

- See section 2.3 for a summary of the key findings form the stakeholder feedback.

2.2 Important considerations and assumptions

This section presents key assumptions in the NETs pathway development for Scotland.

2.2.1 Future viability of biogenic sites without fiscal support

Many large sites that emit biogenic CO2 currently have some fiscal support via either the Renewables Obligation (RO) Scheme or Renewable Heat Incentive (RHI) schemes. Once this subsidy support ends, such sites will be forced into fundamental decisions over whether it is financially beneficial to continue operating. Many of these sites are owned by global companies which will likely have similar decisions to make across a number of sites.

Once the RO scheme ends, several biogas sites may be forced to switch to producing biomethane to ensure they receive continued financial support through a future GGR scheme[28]. This creates a significant opportunity for NETs through BECCS Biomethane if sites decide to capture the carbon from the biogas upgrade process and invest in infrastructure to allow its permanent storage (e.g., via transporting to other parts of the UK or global storage hubs or utilising it in specific industrial applications where it remains permanently trapped, e.g., concrete curing or green cement). Regarding EfW, it is unlikely that CCS will be installed because of fiscal incentives alone, but rather as a necessity of obtaining planning permission and as a regulatory requirement. This is likely to fundamentally impact whether an EfW site is a profitable installation or not.

For NETs that are more expensive and less mature (e.g., DACCS, BECCS Power, BECCS hydrogen), it is expected that deployment will remain at very small scale without significant central support from either the Scottish or UK Governments. Existing UK Government support schemes/competitions such as the GGR Competition, the Hydrogen Innovation Scheme, and Hydrogen Investment Fund could support this. Finally, discussions with stakeholders indicate great interest in biochar, due to its applicability in various sectors such as agriculture, wastewater treatment, and even the construction industry and several test-scale plants are planned in Scotland. Biochar deployment could therefore be significant in terms of number of sites (although in small volumes of NETs) even without additional support.

2.2.2 Availability of bioresource

The impact that NETs may have on the availability of bioenergy resources in the future could be a limiting factor in the development and capacity of sites that may be developed. This is particularly relevant given that the analysis excluded biomass imports and only considered domestic bioresources in estimating the NETs potential of each pathway. Thus, the availability of bioresources is a limiting factor for the development of BECCS and biochar technologies. Table 6 shows the split of dry (for power/industry/biochar & hydrogen) and wet bioresources (those that are more suited to anaerobic digestion), the information in this table is taken from the CXC report “Comparing Scottish bioenergy supply and demand in the context of Net-Zero targets”[29].

| Bioresource Availability | TWh | ||

|---|---|---|---|

| 2022 | 2030 | 2045 | |

| Dry | |||

| Currently Used | 8.0 | ||

| Potential unused resource | 1.7 | 2.9 | 5.3 |

| Total available resource | 9.7 | 10.8* | 13.2* |

| Wet | |||

| Currently Used | 0.9 | ||

| Potential unused resource | 1.9 | 2.1 | 2.2 |

| Total available resource | 2.9 | 3.0 | 3.1* |

*Totals do not match due to rounding

Table 6 shows that there are currently 1.7 TWh of dry bioresources in Scotland that are available but unused. These are predominantly forestry residues and offcuts/brash that could be used in a high capacity[30] biomass boiler/power station. The increase in the available but unused dry bioresources (up to 5.3 TWh in 2045) comes predominantly from short rotation forestry and short rotation coppice as well as increase in forestry offcuts and sawmill residues, which are often used in the power industry. This increased availability increases the potential for power BECCS although it should be noted that increased future domestic demand could also lead to higher feedstock prices thus reducing the benefit for future power BECCS plants.

If it is assumed that a BECCS power station with a 50MWe gross capacity has a 31% efficiency with carbon capture technology installed, an availability of 90% and a capture rate of 90% this would require approximately 1 TWh of fuel per year. This means that in 2045 the available bioresource could support ~ 5 x 50 MWe BECCS Power stations or BECCS CHP plants – and could potentially result in around 1.5 MtCO2 of negative emission if 90% of CO2 captured and permanently stored. The 50 MWe figure has been chosen based on was taken as an arbitrary figure as this is the capacity of EON’s Steven’s Croft Power station in Lockerbie.

Several NETs options will compete for the available bioresources. The assumption above would rely on all bioresources being diverted to BECCS Power and none to Industry, Hydrogen, biochar or any other industry, which is unrealistic. The assumptions for Pathway 3 (UK Government & Scottish Government Action) take the available bioresources into consideration when evaluating future BECCS systems that could be supported. The UKG Action Pathway includes 5 x 50 MWe plants and a future penetration of CCS deployment rate of 50% (i.e., the model essentially has 125 MWe of BECCS Power included for the future scenario). Note that a sensitivity increasing this penetration rate to 100% was included, see section 5.6.6, page 90. The Decarbonisation Readiness consultation[31] proposes to update the 2009 carbon capture readiness (CCR) criteria by removing the 300 MWe threshold and expanding the scope of generation technologies to also include biomass and EfW. This means that any new biomass CHP plant in the UK will need to be capture-ready by leaving space to install carbon capture when the technology becomes feasible. On that basis, all new biomass plants are expected to be capture-ready but to not necessarily install CO2 capture until it becomes feasible to do so under specific circumstances. As TRLs improve, CAPEX and consequently LCOC will reduce in the future, making it more attractive to install CCS on biomass power and CHP plants. The 50% deployment rate is estimated based on the expectation that carbon capture will become economically feasible for half of the biomass capacity installed in Scotland in the future. The consultation applied to England only meaning that the current CCR requirements would still apply in Scotland – a similar policy or approach to that taken in England is needed for Scotland to incentivise NETs in the future.

The 2045 future bioresources have a significant short rotation coppice element – this needs to be supported in the Bioenergy Action Plan, Biomass Strategy or potentially an agriculture and land use strategy in order for that to be achieved. Without these additional energy crops, the future available bioenergy resources would be similar to the current estimates, which would only be able to support around 84 MWe of capacity (approx. 1.7 x 50 MWe capacity plant).

There is also 1.9 TWh of wet bioresources that are available but unused. This rises to an estimated 2.2 TWh in 2045. This capacity of available bioresources can support the pathway assumptions, with 20 biomethane plants with carbon capture installed with a penetration of 50% (based on trends in existing biomethane sites which shows that for half of these, it is economically feasible to install CCS). Future biomethane plants are assumed to be carbon capture-ready – but ultimately the demand for biomethane and incentives made available by the UK Government (e.g., as replacement to the existing Green Gas Support Scheme (GGSS)) will be the governing factor as to how many new biomethane plants come online.

The demand for biomethane on an hourly/daily basis can also lead to biomethane plants being curtailed. If these periods are only a matter of a few hours, then plants can typically deal with diverting the biomethane away from grid injection. If the curtailment periods are longer, this can have a knock-on impact on the generation of biomethane. When considering the additional equipment that would be included on a biomethane plant which was carbon capture ready, this curtailment in output would have an additional knock-on impact onto the running of the CO2 capture plant – which could be detrimental to the overall operation and maintenance of the entire facility if curtailment occurred frequently. Thus, any biomethane site that would want to implement NETs would likely need to have necessary grid agreements in place to minimise this curtailment or potentially the associated on-going OPEX associated with the site/plant could be higher than estimated in this report.

2.2.2.1 Biomass imports

Imported biomass is associated with high upstream emissions (such as from shipping) which are likely to negate the effect of carbon removals, increasing the levelised cost of capture. We have assumed that there are no biomass imports for use in any NETs project. This means that the future demand for bioenergy/biomass/biogenic CO2 is limited to the available domestic resource[29].

2.2.3 Future power demand

As with future biomass demand, there will be a huge competition for available power with the main uses being:

- Powering the national grid

- Electrification of heat and transport will lead to a significant increase in power demand in the future, in line with both the CCC’s 6th carbon budget[7] and National Grid’s Future Energy Scenarios[32]

- The 2030 renewable energy target has 50% of Scotland’s energy consumption to be supplied by renewable sources[33]

- Green hydrogen production via electrolysis plants

- As an energy source for future DACCS plants

It is expected that renewable electricity will continue to play an important role in decarbonising the energy sector in Scotland. In addition, blue hydrogen is viewed as a transition fuel to a green hydrogen-based economy and so it is expected that green hydrogen targets will increase in the future. This means that a cautious approach should be taken when considering future DACCS in Scotland, as competition for available renewable power means that there may be more effective uses for the renewable power available to achieve net-zero and decarbonisation targets, rather than diverting this to removals.

This is a conservative approach but is included in all pathways. The purpose of this is to project a more realistic impact that DACCS can have based on this available power, rather than assume that high volumes of DACCS can be implemented in Scotland resulting in high NETs.

2.2.4 Improvements in carbon capture process performance and costs over time

2.2.4.1 Availability of the CO2 capture plant

A typical assumption for carbon capture rates in CCS feasibility studies is 90%. In reality, instantaneous CO2 capture rates can exceed 99%. The 90% capture rate assumption means that over a given period (typically one year of operation), ninety percent of the carbon dioxide produced is captured from the generation plant. This percentage is affected by the chemical process (which in theory can capture all of the carbon dioxide produced in a given moment) as well as by the plant performance parameters including for example whether the CO2 capture plant is shut down for maintenance or for other reasons. Experience from CCS demonstrations in recent years shows that, due to optimisation and snagging issues, the availability of the CO2 capture plant during initial operation for the first few years was low and improved to over 90% over time[34]. Improvement in the CO2 capture rate was applied to provide a more accurate representation of the actual captured carbon at a potential site. These rates vary depending on the implementation year (early adopters will have a steeper learning curve than sites implementing CCS into the 2030s).

The following availability assumptions were adopted (in all cases the example is based on a maximum capture rate of 90%.)

Short term / Early Years 2023-2030

- 70% in year 1 = 0.7 * 90% > 63%

- 80% in year 2 = 0.8 * 90% > 72%

- 90% in year 3 = 0.9 * 90% > 81%

- 100% in subsequent years 90%

Medium term 2030 - 2035

- 80% in year 1 = 0.8 * 90% > 72%

- 90% in year 2 = 0.9 * 90% > 81%

- 100% in subsequent years 90%

Mid-late term 2035 - 2040

- 85% in year 1 = 0.85 * 90%; 77%

- 95% in year 2 = 0.95 * 90%; 86%

- 100% in subsequent years 90%

Late term 2040 onwards

- 90% in year 1 = 0.9 * 90%; 81%

- 95% in year 2 = 0.95 * 90%; 86%

- 100% in subsequent years 90%

These assumptions mean that the carbon capture plant shows improved availability with time and reaches higher carbon capture rates (>90%) in fewer years from initial operation.

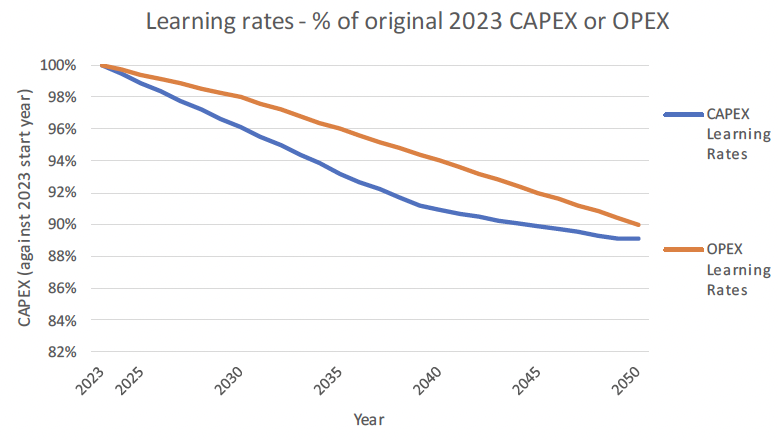

2.2.4.2 Cost learning curves

We have included both CAPEX & OPEX learning rates against our calculated 2023 CAPEX/OPEX for CCS. This is shown in Figure 3. There is a moderate decrease to around 10-11% depreciation in original CAPEX-OPEX in 2023. This is applied to the CAPEX & OPEX rates for each site, varying on the year in which this site can implement NETs. This has the impact of reducing the LCOC for each site depending on which year it is implemented.

2.2.5 Carbon accounting, utilisation & storage capacity

In order for the CCUS to contribute to NETs targets, the captured carbon needs to be permanently stored. This includes the trapping of CO2 in saline aquifers (for example as the case with the Sleipner CCS project in Norway) or in depleted oil and gas fields. Carbon dioxide has many applications in industry but the majority of the these (e.g., urea and fertiliser manufacturing, greenhouses, food & drink) lead to the release of the CO2 back into the atmosphere at some point and so cannot be considered as NETs. Emerging applications such as the use of CO2 in producing sustainable aviation fuels (SAF) substitute for fossil-based aviation fuel rather than lead to negative emissions. However, some emerging industrial applications such as concrete curing, manufacturing of green cement and green polymers will lead to CO2 permanence (i.e., permanent storage). Such processes are still at the early stage and require demonstration before they are deployed at a large scale cost-effectively.

The carbon accounting methodology used may influence whether a site may implement NETs. Monitoring, Reporting and Verification (MRV) methodologies and certification of negative emissions to ensure the permanence of CO2 storage are still in development worldwide. While CCS is included in some emission trading schemes, currently CO2 utilisation is still not included. It should be noted that any NETs MRV methodology should consider the full life cycle of the process including sources of the biomass, the source of electricity and heat as well as the fate of the CO2 captured.

Other considerations for NETs accounting in Scotland are whether the carbon that is captured is stored domestically in Scotland or transported and stored elsewhere (i.e., to HyNet, the East Coast Cluster or shipped to the Northern Lights project in Norway). For this study, it has been assumed that if the carbon is captured in Scotland, then it would contribute to NETs targets for Scotland regardless of where it is stored.

2.2.6 Competition for NETs Deployment

2.2.6.1 Implementing NETs in Scotland versus other parts of the world

Many sites/operators are owned by global companies. The decision to implement NETs at any specific site will often be a decision based on the relative benefits offered for implementing based on the specific country where the site is based. Thus, organisations that may look to implement NETs in Scotland are likely looking at other countries where they have active sites where carbon capture technologies could be implemented. This is particularly relevant for BECCS Power / CHP and BECCS Industry (including the cement industry – noting that there is only one cement factory in Scotland). If Scotland had an incentive for businesses to invest in NETs in Scotland through either fiscal CAPEX support or a revenue stream for NETs through trading, then this could significantly increase deployment. For the purpose of this study, we assume that other countries do not have this type of mechanism which would make it relatively more attractive to implement a NETs project elsewhere.

2.2.6.2 Competing technologies and uses for stored carbon

If an existing site meets the criteria to be included as part of the suite of sites that eventually form the pathway, it is important to consider the alternatives to the technologies or industries where carbon can be captured. The specific competing uses for stored carbon (i.e., via utilisations streams as opposed to permanent storage) should also be considered.

As highlighted above, stored carbon may not end up being permanently stored – indeed there are many current uses for CO2 that could be captured – particularly before any storage facility is available. Certain industries are optimistic over the potential for capturing biogenic CO2 but uncertain over whether this captured CO2 would end up permanently stored. Ultimately, if carbon is captured at a site, the end-use of the captured carbon is expected to be dominated by the financial benefit offered.

Common alternatives to permanent storage include use in producing SAF and synthetic fuels, use in the food and drink industry, chemical synthesis, producing micro algae and use in enhanced oil and gas recovery operations. Some industry-specific applications are also being trialled for example, methanisation of hydrogen in the whisky industry to produce methane that can be combusted as an alternative to direct hydrogen combustion, this instance, the captured carbon reduces the requirement to upgrade all plant equipment to be hydrogen ready. Both existing and new sites will face competition

Discussions with industry reveals that existing sites that could implement CCS now (biomethane & fermentation) currently have alternative uses for the stored carbon (food & drink industry – Renewable Transport Fuel Obligation (RTFO)). Such practice will not contribute to NETs in the early stages but in the future, when the right incentives are available, the captured carbon would be for permanent storage thus resulting in such sites contributing to NETs targets.

There may be competition between future BECCS & DACCS sites for CO2 transport infrastructure and storage sites. However, this is not expected to be significant as Scotland benefits from the availability of large storage capacity in the North Sea. DACCS and BECCS could be complementary in the sense that low carbon electricity for DACCS can be provided via BECCS power or CHP sites.

BECCS power will also have competition from other sources of electricity including large scale renewable power, fossil-generated power with CCS, increased imported power from interconnectors or nuclear (noting that the Scottish Government is opposed to new nuclear power).

There is a need for a diverse energy mix in the future and combustion plants producing power (and heat) with carbon capture will form a part of that future energy mix. Torness nuclear power plant has a nameplate capacity of 1,290 MWe, leaving a considerable gap in power generation when it comes offline. Note that this gap will be plugged by a variety of renewable and low carbon technologies – and BECCS Power is considered to be one of these.

Industrial sites that already have biogenic emissions typically use biogenic fuels as these are by-products from their production (wood/paper and pulp industries). Implementing carbon capture at these sites is again likely to be driven by regulatory reasons (i.e., they have been forced into implementing carbon capture via planning or consenting requirements). Organisations with net-zero targets will be forced away from traditional fossil-based systems without CCUS.

Breweries and distilleries that might implement carbon capture from fermentation processes have so far been driven by demand for the captured carbon for use in processes (for use in carbonation of drinks – or methanisation as outlined above). The alternatives to capturing carbon as a means to reduce emissions at these sites is the same as other industrial sites (biogenic fuels, electrification and hydrogen).

2.2.7 Future market demand for NETs and market penetration rates

NETs and carbon removals in general are seen worldwide as a way of balancing residual emissions from sectors which are hard to abate (such as aviation, agriculture and construction). On the route to Net Zero, it is essential that countries meet their interim carbon reduction targets; if they are not, the demand for NETs will only increase. The development of CCS industry and infrastructure is also seen as the enabler and cornerstone on which the NETs industry must rely on. It is thus important that CCS demonstration projects are established now with innovation to allow the technology to be available in time. Note that enhanced oil recovery (EOR) which uses carbon dioxide to improve the viability of oil production has so far been the major driver of the carbon capture industry.

The penetration and deployment rate of CCS projects in various sectors depends on various factors including: the current readiness of the technology, the willingness of various sectors to adopt CCS and their role in demonstration projects as well as the availability of support from government. The current study established projections for the growth of future industries which could be contributors to NETs and applied CCS deployment rates for each of the sectors to estimate future NETs potential. These penetration rates were estimated based on economic feasibility analysis for existing sites which showed the percentage of existing sites which could implement CCS and achieve a sufficiently low levelized cost of carbon (LCOC) below the threshold. It should be noted that this is a rough estimate and so a sensitivity analysis is undertaken on penetration rates.

The pathway model developed has a market penetration rate function to allow for sensitivities to be applied. Penetration rates can be applied to existing or future sites. The purpose of this function was to provide a “what if” into the modelling. If a site meets the LCOC threshold and is included in the pathway – this does not necessarily mean that it will inevitably implement NETs – the site may not have the capital to implement NETs, or there may be viable alternative uses for any captured carbon at that site. The penetration rate works in the following way:

1. Sites are chosen in each pathway based on the specific assumptions as outlined in sections 2.1 and 5.2

- This provides a long list of existing, future & fuel switch sites in each of the technology categories

2. Penetration rates can theoretically vary from 0% to 100%

- The higher the penetration rate the greater the anticipated impact of that specific NETs technology

- This is useful in particular for sensitivity analysis as the number of sites that could deploy NETs could be easily varied.

3. For existing sites – the market penetration has been set to 100%

- Ultimately this means that if the sites have been selected from the original list of ~300 into the pathway modelling process then it will adopt NETs.

- E.g., if we assume a 10% penetration rate then for every 10 BECCS sites from the long list, one will be included in the final pathway.

4. The market penetration rate operates differently for future sites

- As we cannot predict the number of future sites beyond what is currently planned, the boundaries for future NETs sites have been set by available bioresources (BECCS & biochar) and competition for available power (DACCS).

- Future biomass and EfW plants will receive permitting only if they are carbon capture-ready (Decarbonisation Readiness consultation, 2022). This means sites will need to leave enough space to install CCS in the future when it is feasible to do so. Sites need to submit a feasibility study as part of the planning and permitting process. However, being carbon capture ready (CCR) does not necessarily mean that sites will install CO2 capture and be carbon removals from the start. Our assumptions on penetration rates are based on the economic feasibility of sites in the future (learning curves, cost reduction and improved performance). Options where CO2 capture is currently more established (e.g., biomethane) are expected to have higher penetration rates in the future where CO2 capture in the power sector is currently less established and so while there will be improvement in performance and costs in the future, we do not expect each biomass power and CHP site will install CO2 capture from the start.

- The assumed penetration rates for future sites are as follows:

Table 7: Penetration rates for future sites

- BECCS Power - 50%

- BECCS Industry - 50%

- BECCS Fermentation* - N/A

- BECCS Biomethane - 20%

- BECCS EfW** - 50%

- DACCS*** - 100%

- Biochar**** - 100%

- BECCS Hydrogen - 100%

*No new fermentation sites included in any pathway as to the best of our knowledge there are no new large-scale sites planned (arbitrarily; any new fermentation sites constructed in recent years have been smaller-scale artisan sites).

** The number of EfW sites in each pathway varies from 1 in pathway 1, 2 in pathway 2 to 10 in pathway 3

*** The number of DACCS sites in each pathway varies from one in pathways 1 and 2 to 3 in pathway 3

**** The number of biochar sites in each pathway varies from 1 in pathway 1, 2 in pathway 2 to 10 in pathway 3

These market penetration rates have not been applied to future sites that could fuel switch to biogenic CO2 – sites that are included in this part of the pathway have been estimated based on stakeholder commentary and existing biogenic CO2 sites.

Fuel-switching sites have been applied only in the maximum NETs pathway and are assumed to be industry sites, most likely in the wood-based industry (i.e., sites that would have easier access to significantly cheaper biomass resources, that may be implementing biomass heat or biomass CHP systems without the historic fiscal support that would have been on offer from the RHI or ROC schemes).

The penetration rates were also used to produce the variability in the figures presented in the results section (section 5.4). Adjusting the penetration rates +/- 20% for each technology input was undertaken to show some high-level variance in results for each pathway. This method of adjusting the inputs rather than the results of the pathway modelling by +/- 20% was done to test the impact that future CCS deployment rates in the various NET sectors on the pathways.

2.3 Key findings from stakeholder feedback

1. The development of the Acorn Storage Facility is seen as a necessity for NETs to develop on a large scale in Scotland.

2. Biomethane BECCS is already an option that many sites are considering in the UK. While several projects are currently financially viable, wide scale deployment of biomethane BECCS is not seen as realistic until the late 2020s. In parallel to this NETs option developing, focus needs to also be on creating and incentivising industrial CO2 utilisation options where CO2 remains permanently stored (these include concrete curing, green cement and mineral carbonation for example)

3. Power / CHP BECCS and EfW BECCS were seen as important options for achieving NETs targets due to the large volumes involved. However, these are not seen as viable options before the 2030s. Combining BECCS with CHP and / or DH applications provides the benefit of higher efficiencies and should be prioritised over power-only BECCS.

4. EfW BECCS were seen as an attractive option to focus on as CCS is the only option for EfW sites to decarbonise. Deployment of NETs for EfW plants was projected to be a credible option from around 2030 onwards, with the Acorn CCS CO2 transport and storage infrastructure project cited as a key enabler. Projects installing CCS on EfW facilities are, however, planned in Scandinavian countries prior to 2030.

5. Sustainable aviation fuels (SAF) are seen by stakeholders as a better use for DAC-CO2. Permanent storage of DAC-CO2, which is the key driver for NETs, is unlikely to become feasible unless the right incentives are available to facilitate this approach. Future NETs policy should aim to prioritise geological storage of NETs over the use of CO2 in the production of SAF which is a focus for the aviation industry.

6. Several barriers exist which need to be overcome if wide scale deployment of NETs is to be achieved in the next decade. These include financial barriers as well as non-financial barriers (supply chain and skills development, policy to encourage capture and permanent storage of CO2 from specific sectors, planning and permitting, long-term environmental impacts, for example air and water emissions from wide scale deployment of CCS, etc.). NETs deployment is not seen as viable in the absence of incentives for the permanent storage of the carbon, whether in geological formations or via industrial applications. Scotland has a strong R&D base which can be utilised and supported to improve innovation in solvents, process design and optimisation, minimise environmental impacts from CCS deployment.

7. Previous work on supply and demand of bioenergy sources in Scotland shows that by 2045, short rotation coppice will be key. This means that the Bioenergy Action Plan, the Biomass Strategy or any agricultural and land use strategy should support this type of feedstock.

A summary of stakeholder engagement is provided in Appendix 3 of the technical appendices document. The following are key messages from the stakeholder consultation. Stakeholders included biomass power generators (including CHP), energy from waste sites and biomethane producers. Also included were industries such as distilleries, water and sewage, cement production, fuel and wood-based products (such as panel boards and paper).

Contact

Email: NETs@gov.scot