Negative Emissions Technologies (NETS): Feasibility Study

This study estimates the maximum Negative Emissions Technologies (NETs) potential achievable in Scotland, 2030 - 2050.

Executive summary

Key findings

This study estimates that the maximum Negative Emissions Technologies (NETs) potential achievable in Scotland in 2030 is 2.2 MtCO2/year (60% of the available biogenic CO2 emissions), based on existing and future potential sites and given technical, economic and other constraints. This is significantly lower than the stated NETs ambition in the CCPu of 5.7 MtCO2/year by 2032. With additional policy interventions from both the UK and Scottish Governments, this figure could potentially reach 6.8 MtCO2/year by 2045 with technologies such as direct air carbon capture and storage (DACCS), bioenergy CCS (BECCS), energy from waste (EfW) and biomethane and distillery sites all playing a role.

- Policies that introduce a negative emission trading element could have the greatest impact on NETs development in Scotland, which we estimate could add ~5.7 MtCO2 of additional carbon removals. This is because of the introduction of a revenue mechanism based on the negative emissions produced at each site, which we estimate could lead to an additional 50-60 sites being able to profitably deploy NETs.

- Sector specific funding could be used to deliver projects, in particular to the biomethane and fermentation sectors, to support the development of NETs in these sectors which have highly pure CO2 streams. We have estimated that a £40m investment by SG could contribute between 0.12 MtCO2 and 0.36 MtCO2 of additional emissions reduction depending on how it is targeted.

- The deployment of CCS infrastructure is essential to ensure NETs targets are achieved. Scotland benefits from ample CO2 storage capacity in the North Sea and a strong base in CCS R&D and engineering skills. In addition, companies such as Carbon Capture Scotland and Carbogenics are leading the way in Scotland in the deployment of NETs and can help facilitate early deployment which puts Scotland in a unique position to lead the way.

- Stakeholders consulted with during this project had an overall positive perception of NETs, but all highlighted that policy changes to incentivise NETs are needed, with most suggesting that long-term financial support is needed as well as up-front CAPEX support. The range of stakeholders were consulted with on this project were from a mixture of industries, higher education, research and trade associations.

- The deployment of NETs in Scotland and its contribution to Net Zero targets is significantly dependent on the development of the Acorn Storage facility by 2030. However, there are certain existing sites which can help initiate a NETs industry in Scotland prior to 2030. These are mainly biomethane and distillery sites where the capture of the CO2 requires comparatively minimal investment.

- Many existing biomethane and distillery sites in Scotland can have an attractive breakeven point for profitably installing NETs and can act as ‘low hanging fruits’, contributing to the initiation of a NETs industry in Scotland, although at very small volumes (0.0001 MtCO2 – 0.2 MtCO2). Any feasibility studies for future biomethane sites should explore the option of adopting CO2 capture and becoming net-negative.

- Biochar applications are emerging worldwide with several hundred thousand tonnes of carbon dioxide captured via biochar annually and contributing to carbon removal across Europe. This option can be deployed easily across Scotland where expertise already exists. However, the regulatory landscape to facilitate the use of biochar as well as Monitoring, Reporting and Verification (MRV) and certification procedures to ensure permanent storage of the carbon are needed for biochar as well as other NETs.

- A renewable source of electricity is essential for DACCS to ensure it contributes effectively to NETs targets. Strong competition for renewable electricity (e.g., with green hydrogen production) will exist and is very likely to affect the deployment of DACCS projects in Scotland. Taking this into account, a modest DACCS deployment capacity of 0.5 MtCO2/year is expected in 2030, doubling by 2040.

- Carbon capture and storage is a key and important decarbonisation option for EfW sites and can contribute negative emissions. This feasibility study recommends that policy is developed to encourage the development of CCS on future EfW sites and to ensure such sites are carbon capture-ready. Furthermore, policies should prioritise the deployment of CCS on existing EfW sites which are also combined heating and power (CHP) and part of district heating (DH) schemes.

- This study recommends that only domestic Scottish bioresources are included when estimating BECCS targets. Imported biomass is associated with higher life cycle emissions which are likely to negate the effect of carbon removals. The available domestic dry biomass sources in Scotland limit the development of new biomass power plants to a small number of a few 50 MW plants and consequently limits the potential for BECCS power. The position in the UK Government’s Biomass Strategy (published August 2023) on biomass imports will impact NETs developments in the UK as a whole and in Scotland. Nevertheless, any future MRV and NETs certification regime is expected to include emissions from biomass transport and is expected to reduce the negative emissions potential of power BECCS in Scotland.

- Our analysis suggests that in 2045, for future sites in the SG & UK Government Pathway:

- Around 7.7 TWh of available bioresources are required for BECCS Power and BECCS Industry

- Around 0.9 TWh of available bioresources are required for biochar

- Around 0.15 TWh of available bioresources are required for BECCS Hydrogen

- Around 4.3 M tonnes of waste is required for BECCS EfW

- Around 1.9 M tonnes of feedstock are required for future biomethane sites

- The development of the carbon removal or NETs industry in Scotland and across the UK requires the development of MRV and certification procedures to ensure that the captured CO2 remains permanently stored whether in geological formations or in emerging industrial applications. In addition, for biochar and BECCS applications, the MRV and certification guidelines need to ensure that the feedstock is sustainably-sourced and of biogenic origin.

- An important consideration for NETs in Scotland is whether the carbon captured in Scotland is traded in the UK under the UK ETS or internationally under Article 6 of the Paris Agreement.

This study assumes that the captured carbon would contribute to NETs targets for Scotland regardless of where it is stored irrespective of if or where any resulting credits were sold through the UK ETS. In reality, and particularly for DACCS, whether negative emission credits are sold/traded is a decision for an individual site/developer/organisation to make.

NETs have an important role to play in achieving Net Zero targets in Scotland.

Following the Paris Agreement, in 2015, NETs are a key element in many countries’ Nationally-Determined Contributions (NDCs). For Scotland, the CCPu and the CCC’s 6th Carbon Budget highlighted the importance that NETs need to play in Scotland’s climate change planning, including playing a key role in balancing residual emissions from hard-to-abate sectors such as aviation and agriculture.

The Climate Change Plan update (CCPu) for Scotland commits to undertaking a detailed feasibility study of opportunities for developing Negative Emission Technologies (NETs) or carbon removal projects in Scotland that would identify specific sites and applications of NETs, including developing work to support policy on technologies such as Direct Air Carbon Capture and Storage (DACCS) and Bioenergy Carbon Capture, Utilisation and Storage (BECCS). This NETs feasibility study referred to in the CCPu aims to help understand the NETs market and what technologies can realistically be deployed to meet the CCPu targets, and to develop deployment pathways and policy recommendations to help accelerate deployment of CCUS and NETs in Scotland.

This study considered a range of engineered NETs options including (i) direct air carbon capture and storage (DACCS), (ii) biochar produced from biomass pyrolysis, and (iii) various bioenergy CCS options including power and CHP BECCS, industrial BECCS, EfW BECCS, biomethane BECCS, hydrogen BECCS, biofuels BECCS and BECCS on distillery sites across Scotland. The study gathered evidence from the literature and through targeted stakeholder interviews on the feasibility, prospects and challenges for NETs deployment in Scotland. In addition, technology and cost data for the different NETs options was gathered to facilitate techno-economic analysis of existing and future sites which have potential to deploy carbon capture and to contribute to NETs targets in Scotland.

The study involved data gathering on existing sites which could potentially contribute to a NETs target in Scotland. Data for distillery and brewery sites, biomass CHP, biomethane sites and EfW (including both incineration and gasification sites) was collected. The amount of CO2 available from existing sites which could potentially be captured was evaluated and the total NETs potential estimated.

The analysis shows that the total biogenic[1] CO2 currently available from existing sites is around 3.3 MtCO2/year, split across five main sectors (39% from biomass CHP and power sites, 26% industry, 14% EfW, 15% distilleries and 6% from biomethane sites). An additional 1 MtCO2/year from these existing sites is attributed to feedstocks of fossil fuel origin (for example EfW feedstock containing high proportions of plastics, metals and glass). The total amount of biogenic CO2 available for capture could increase if sites currently using fossil fuels switched to biogenic fuel inputs. Additionally, increasing the volume of biogenic waste entering EfW sites could in turn increase Scotland's negative emissions potential.

An economic feasibility analysis was undertaken on the basis of a Levelised Cost of Carbon (LCOC)[2] comparison in order to assess the feasibility of sites adopting NETs on a common basis and to identify the level of support that would be needed from the Scottish and UK Governments to make NETs viable. The economic and cost analysis assumes permanent storage of CO2 in the North Sea as part of the Acorn project utilising existing pipework infrastructure. Storage in the Liverpool Bay area for HyNet or storage in the coast of Humber and Teesside under the East Coast Cluster were also assessed but associated transportation costs made it economically unfeasible to send captured CO2 to these sites.

It should be noted that uses of the carbon dioxide from NETs are emerging as an alternative to geological storage. In any NET feasibility analysis, the permanence of the CO2 needs to be considered. Some emerging applications such as sustainable aviation fuels (SAFs) are promising for CO2 utilisation but cannot contribute to NETs or carbon removal targets as the CO2 is released back into the atmosphere. Other emerging applications including concrete curing, mineral carbonation, green cement and polymers can offer CO2 permanence. However, further work needs to be done on demonstrating these options in the future and developing the regulatory framework to allow these applications to be considered net-negative. This study assumes that the CO2 captured from NETs remains permanently trapped regardless of whether it is stored in geological formations or via industrial applications thus contributing to NET targets. However, only permanent storage in geological formation was costed for the feasibility study, not utilisation options.

The economic feasibility analysis shows that existing biomethane and distillery sites can act as ‘low hanging fruits’ and are considered early opportunities to deploy NETs in Scotland. Despite the small volumes of CO2 involved, these can help to demonstrate the NETs supply chain and identify opportunities for CO2 utilisation in industries where the carbon can be permanently stored. BECCS EfW is also an opportunity in spite of the higher costs as CCUS is viewed as one of the very few solutions to allow EfW to continue to be deployed in Scotland. In addition, the combination of EfW with combined heat and power (CHP) and district heating (DH) operation is an option that helps improve efficiency and improve the financial viability of EfW BECCS. Several EfW BECCS plants with DH are currently in development in Scandinavian countries.

Three pathways of support were considered:

- Pathway 1 – No Action assumes minimal action or policies are promoted by the Scottish and UK Governments to influence the development of NETs in Scotland, and that there is no negative emission credit trading mechanism.

- Pathway 2 – Scottish Government Action represents a pathway that is made up of the ‘low hanging fruit' sites that could adopt NETs for a relatively low investment cost and at the lowest levelised cost of carbon. Pathway 2 is bounded by specific policies and assumes no negative emission credit trading mechanism exists. This Pathway assumes only the Scottish Government will develop a policy package to support NETs deployment.

- Pathway 3 – UK Government and Scottish Government Action assumes a suite of policies and mechanisms are implemented from both the UK and Scottish Governments that result in high CCUS and NETs deployment. A negative emission credit trading mechanism is included in this pathway. The analysis shows that the maximum NETs potential achievable from existing sites in 2030 is around 2 MtCO2/year (60% of the available biogenic CO2 emissions).

A range of pathway-specific assumptions have been made, as outlined in Table 1. Some assumptions such as the deployment of the Scottish CCUS cluster were held constant for all pathways, while others were pathway dependent. These include a proxy to test whether or not a site may remain relatively profitable after including a NET facility without additional support and the scope for negative emissions credits trading through the UK ETS.

Common Assumptions

- Acorn project - Active by 2030

- Feeder 10 - Feeder 10 pipeline repurposed for CO2 transportation between Bathgate and Peterhead, Garlogie and Kirriemuir compressor stations used as potential injection points

- Transportation - Combination of road and onshore pipeline using feeder 10 pipeline

- Storage - Storage in the North Sea either via the Acorn project, in the Liverpool Bay via the HyNet project or in the coast of Humber and Teesside under the East Coast Cluster.

- Bioenergy limitations - Bioenergy resource modelling to 2045 used for the analysis (Comparing Scottish Bioenergy supply and demand in the context of net zero, CXC, Report by Ricardo, 2022)[3]

- Imports - No biomass imports

- Capture performance - 90-95% maximum capture rates (technology specific) Capture rate learning curves deployed such that sites can achieve the maximum CO2 capture faster in later years of the modelling

- CAPEX & OPEX - Literature information used to develop the CAPEX & OPEX for sites. Learning rates for both CAPEX and OPEX introduced

| Pathway Specific | Pathway 1 | Pathway 2 | Pathway 3 |

|---|---|---|---|

| Minimum tCO2 for viability | 2,500 tonnes | 2,500 tonnes | 1,000 tonnes |

| Relative Profitability Test | N/A | Yes | N/A – overwritten by NETs trading |

| Fiscal Policies | No additional fiscal support | Fiscal support of £40M allocated to NETs Sensitivities adjusting this allocation undertaken | |

| NETs trading scheme | N/A | N/A | Active - £80/tCO2 in 2025 |

All pathways have been developed based on an assumption that the Acorn storage facility located in the north-east of Scotland is active by 2030. Realistically, biomethane and distillery sites in Scotland can start capturing CO2 before 2030, and either export it for permanent storage globally (e.g., via The Northern Lights project) or for utilisation in industry (e.g., concrete curing or mineral carbonation) where it remains permanently stored. The relatively small volumes of CO2 available from biomethane and distillery sites (i.e., in comparison to biomass CHP and EfW sites) make it possible for industrial utilisation to use most of the available carbon dioxide without the need for large and complex CO2 storage infrastructure in the North Sea. This, however, requires these emerging CO2 utilisation processes (e.g., concrete curing) to be recognised as permanent storage applications.

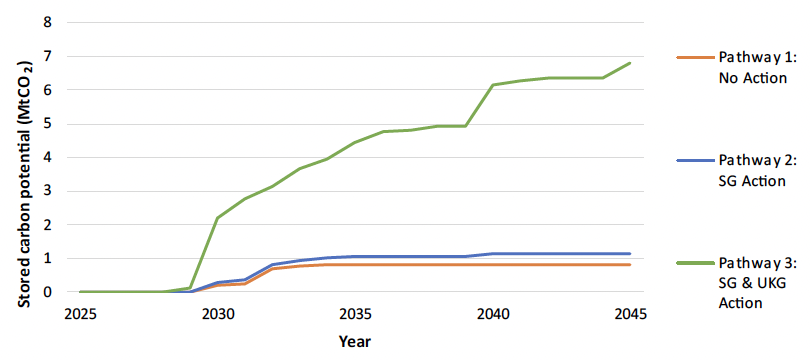

The analysis shows that the cumulative NETs potential between 2030 and 2045 ranges from 16 MtCO2 (under the ‘No Action’ pathway) to 112 MtCO2 (under the UKG and SG Action pathway), with a total investment requirement of £0.7–4.3 Bn over the 15-year period, as shown in Table 2 and Table 3. Note that these investment figures are contingent on the full range of policies envisioned in the respective pathways materialising.

| Pathway | Annual stored Carbon, MtCO2 | Cumulative Stored Carbon MtCO2 | |||

|---|---|---|---|---|---|

| 2030 | 2035 | 2040 | 2045 | ||

| 1 - No Action | 0.6 | 0.8 | 0.8 | 0.8 | 16 |

| 2 – SG Action | 0.8 | 1.2 | 1.3 | 1.3 | 25 |

| 3 – UKG & SG Action | 2.2 | 4.5 | 6.1 | 6.8 | 112 |

Under the SG Action pathway, the total lifetime cumulative NETs potential is 25 MtCO2 (0.4 MtCO2/year in 2030 increasing to 1.3 MtCO2/year in 2045). This includes existing biomethane and distillery sites as well as future EfW and biomethane sites. It also includes the planned Storegga DACCS project.

Under the UKG and SG Action pathway, the NETs potential increases from 2.2 MtCO2/year in 2030 (which is significantly lower than the stated NETs target in the CCPu of 5.7MtCO2e/year by 2032) to 6.8 MtCO2/year in 2045 and includes all NETs technological options.

| Pathway | Annual CAPEX (£M) | Lifetime CAPEX (£M) | |||

|---|---|---|---|---|---|

| 2030 | 2035 | 2040 | 2045 | ||

| 1 - No Action | 702 | - | - | - | 708 |

| 2 – SG Action | 823 | - | 1 | - | 824 |

| 3 – UKG & SG Action | 1,314 | 292 | 1,568 | 157 | 4,320 |

The study assumes that only domestic bioresources within Scotland are available for BECCS and biochar applications and that there are no biomass imports for NETs in any pathway, from either the rest of the UK or the rest of the world. The available domestic dry biomass sources limit the development of new biomass power plants in Scotland to a small number of 50 MW plants. This limits the potential for BECCS power, considering that not all of these sites will install CCS. Biomass imports could increase this potential, but it should be noted that any NETS Monitoring, Reporting and Verification (MRV) should take the source of biomass into account as the negative emissions potential is likely to reduce if upstream emissions from biomass transport are significant.

The study also assumes that if the carbon is captured in Scotland, then it would contribute to NETs targets for Scotland regardless of where it is stored. For all pathways, it was assumed that all sites that form part of a pathway (by meeting the LCOC and market requirement) where carbon is captured at site, will be counted – and not traded internationally. Trading of captured carbon credits is being negotiated under Article 6.4 of the UNFCC’s Paris Agreement. It should also be noted that whether negative emission credits are sold/traded is a decision for an individual site/developer/organisation to make (in particular for DACCS). For the purposes of the negative emissions trading credits mechanism, it is assumed that this mechanism would operate as part of the UK ETS and that the apportionment of negative emission credits to be allocated to government greenhouse gas accounts would be based on the relative proportion of production. In other words, it is assumed that the negative emissions created in Scotland would be counted as part of Scotland’s emission reduction targets irrespective of where in the UK the credits were sold through the ETS.

For NETs with a lower Technological Readiness Level (TRL) (e.g., DACCS, BECCS Power, BECCS hydrogen), it is expected that deployment will remain at very small scale without significant central support from either the Scottish or UK Governments. Biochar applications already exist in Scotland, albeit at a small scale. Biomass pyrolysis is well-established already in several EU countries and already contributes to carbon removal in some countries. Certification schemes and MRV procedures are needed to ensure that biochar plays its role as a NET.

A renewable source of electricity is essential for DACCS to ensure it contributes effectively to NETs targets. Renewable electricity will be required to decarbonise the electricity grid, and by extension the electrification of energy demand such as heating or transport, and to establish a green hydrogen economy in Scotland. Thus, strong competition (i.e., for renewable electricity) could exist and, if so, affect the deployment of DACCS in Scotland. This study assumes a modest DACCS deployment of 0.5 Mt CO2/year (based on existing stated commercial plans as part of the Scottish Cluster bid) in 2030 and assumes that this capacity will double by 2040, making only a small contribution of 0.1% of the required global DACCS targets by 2040 (according to the IEA).

The total NETs potential or the timeline at which NETs can be deployed was tested by varying the impact of fiscal, general and technical policies. Sensitivity analysis was undertaken to test the impact of the policy where this could be quantified.

Fiscal policies are those that either offer direct or indirect financial support to NETs while general policies and non-NETs specific policies are those which could impact the future of NETs through, for instance, public perception campaigning. Technical policies offer technical support to other related areas that could impact the development of NETs in Scotland, such as those related to improving transport infrastructure or planning policies.

At the time of analysis and reporting, the position in the UK Government’s Biomass Strategy (subsequently published August 2023[4]) on biomass imports and supporting specific biomass technologies (e.g., biomass gasification) was unknown. If large amounts of biomass imports are included, this could in theory have a significant impact on the development of large NETs projects in Scotland due to a larger available bioresource volume. The emphasis on specific biomass feedstocks in the Bioenergy Action Plan will also be linked to which BECCS technologies can develop in the future.

The future feasibility of NETs in Scotland is also dependent on what NETs targets are introduced and whether emphasis is placed on specific technologies. Improvements in planning and consenting processes could lead to advancing NETs deployment. Policies to support the R&D and implementation of industrial processes which lead to permanent storage of CO2 (e.g. concrete curing, mineral carbonation) could help accelerate early deployment. Furthermore, policies which facilitate supporting the development of CCUS infrastructure (including improving road conditions to facilitate road transport), addressing gaps in skills across the CCUS supply chain and addressing public concerns through public awareness campaigns can all lead to positive impacts on the development of NETs. Estimating the impact of such policies against a suite of emerging technologies is challenging due to the immature nature of the sector, with limited verified literature on existing and successful policies to draw upon.

The analysis of the various pathways shows that technology-specific funding can help early deployment of NETs. For example, the level of funding required to develop biomethane BECCS on existing sites is £20-70M. This only leads to a NETs potential of around 0.5Mt CO2/year but can be seen as a way of kick-starting the NETs industry and infrastructure in Scotland, and of testing various CO2 utilisation routes. Pathway analysis assumed a funding pot of £40M was available to support NETs in Scotland which is not linked to a specific NETs sector. Business model development is also essential to accelerate NETs deployment, allowing for more certainty in project viability throughout the development stage. Finally, the expansion of the UK ETS to include NETs and negative emission credits, and a CfD mechanism to support NETs development, are also seen as key policies which could encourage the deployment of NETs in Scotland and the UK as a whole.

Contact

Email: NETs@gov.scot