Negative Emissions Technologies (NETS): Feasibility Study

This study estimates the maximum Negative Emissions Technologies (NETs) potential achievable in Scotland, 2030 - 2050.

PART 1: NETS pathways development

1. Introduction

The purpose of this study is to help the Scottish Government better understand the NETs market, understand what NETs options can realistically be deployed in Scotland to support the transition to net-zero, and to subsequently develop NETs deployment pathways and policy recommendations for the Scottish Government to adopt. The objectives of this study are as follows:

- To review existing Negative Emission Technologies (NETs) and compare them in terms of their operating parameters and costs,

- To undertake stakeholder engagement to understand business development and investment plans in the private sector,

- To evaluate costs and benefits of different NETs options,

- To develop NETs pathways on the evidence gathered and to make suggestions on future policies for the Scottish Government in terms of NETs deployment.

Section 1 of this report discusses the importance of NETs in achieving Net Zero targets. Section 2 outlines key considerations for NETs in Scotland based on the stakeholder consultation undertaken as part of the study. Section 3 provides an assessment of the maximum NETS potential achievable in Scotland based on data gathered for existing and future sites and Section 4 then undertakes an economic feasibility and estimates of the levelised cost of carbon (LCOC) for all sites within the database. Section 5 introduces the set of NETs pathways developed for this study, outlining the assumptions and limiting factors, and describing the impact of certain policies on these pathways. A sensitivity analysis is also given in Section 5. Finally, Section 6 provides conclusions and policy recommendations. The Technical Appendices at the end of this report provide a comprehensive summary of the literature reviewed, data gathered, and assumptions made in undertaking the economic feasibility and pathway development.

1.1 The need for NETs targets in Scotland

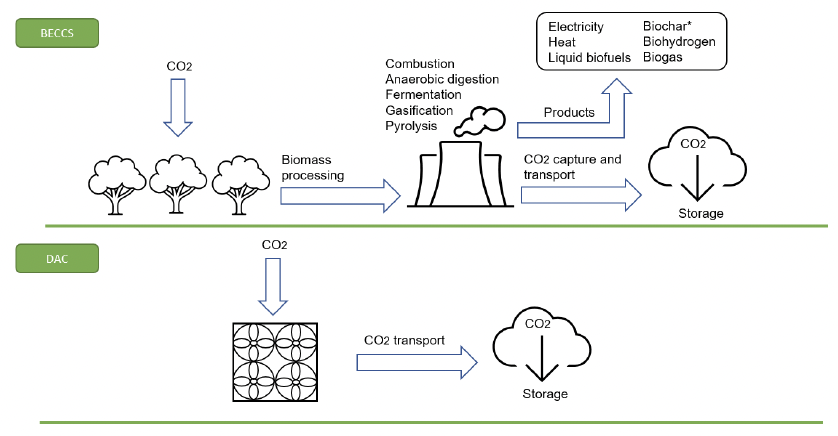

Negative emission technologies (NETs), also known as Greenhouse Gas Removal (GGR), Carbon Dioxide Removals (CDRs) or simply Carbon Removals, are vital for achieving domestic and global Net Zero targets[5]. They encompass both nature-based and engineered solutions, where atmospheric CO2 is captured and sequestered in order to achieve a ‘net removal’ of carbon (whether permanently stored underground in depleted oil and gas fields or saline aquifers or in manufactured products such as concrete). Engineered solutions include options such as the thermal treatment of biomass through combustion, gasification, pyrolysis, anaerobic digestion, or fermentation (known as Bioenergy with Carbon Capture and Storage (BECCS). Other engineered solutions include the use of fanned capture units to capture atmospheric CO2 using solvents and adsorbents (known as Direct Air Carbon Capture and Storage (DACCS)). Pyrolysis of biomass and waste to produce biochar where the carbon remains permanently stored is another engineered solution. See Figure 2 for further detail on the carbon flows of NETs.

While only engineered removals fall within the scope of this study, nature-based solutions, such as afforestation, enhanced weathering, ocean mineralisation, habitat restoration, and soil carbon sequestration, will play a vital role by increasing carbon storage in natural sinks. However, these alone cannot deliver removals at the pace and scale required to achieve UK climate goals and so engineered solutions will also be required.

NETs may play an important role in offsetting emissions from carbon intensive industries, such as aviation and agriculture, which are anticipated to continue to grow in carbon intensity and may emit circa 15 MtCO2/year[6] in the UK in 2050. Under the UK’s Net Zero Strategy, there is an ambition to deploy at least 5MtCO2/year of engineered removals by 2030, in line with the National Infrastructure Commission’s assessment, whilst the CCC[7] and Royal Society[8] estimate that 43.5-130 MtCO2/year of NETs are needed by 2050. It is also expected that the UK's storage capacity will take around 10 years to be made ready, so work will need to begin now in anticipation of the quantity of captured CO2 requiring permanent storage in the future[9], [10]. On a global scale, to achieve Net Zero emissions by 2050 it is estimated that a total of 1.2 GtCO2 of carbon capture is required by 2030 and 7.6 GtCO2 is to be captured in 2050; 30% of which comes from BECCS and DACCS, 50% from fossil fuel combustion, and 20% from industrial processes[12]. Currently, there are approximately 35 commercial CCUS facilities in operation globally, with a collective CO2 capture capacity of 45 MtCO2/year.

Apart from their climate change benefits, NETs also provide an opportunity for the UK to export specialist skills. In addition, facilitated by Article 6 of the Paris Agreement, the UK could sell negative emissions to countries abroad (the UK has CO2 storage capacities of ~78,000 MtCO2, which is greater than domestic demands)[10]. This could lead to co-benefits of increased employment, innovation through start-up industries and creation of new value chains[11]. In the near future, NETs capacities are expected to grow significantly. Analysis by Element Energy[12] indicates that Scottish BECCS and DACCS capacities could reach 5-6 MtCO2/year by 2050[6]. Furthermore, stakeholders predict even more optimistic deployments rates, with DACCS potentially operating at the megaton scale by the next decade[6].

*Majority of biochar production facilities do not utilise CCS. Instead, biogenic carbon is stored permanently within the biochar product and applied to soils; in the construction industry or for other emerging applications, hence enabling negative emissions.

**Flowchart adapted from work completed by the IEAGHG[13].

1.2 Existing scottish NETs ambitions

The Climate Change Plan Update (CCPu)[14], published in December 2020, provided a detailed overview of Scotland’s existing trajectory towards Net Zero and suggestions for improvement. A section was dedicated to NETs, which highlighted the need for negative emissions to offset hard-to-abate carbon-intensive sectors (e.g., aviation and agriculture). The CCPu considered both BECCS and DACCS as the engineered GGR options for Scotland, with BECCS categorised into BECCS Power, BECCS Gasification, BECCS Industry and BECCS Biofuels. The CCPu concluded that NETs will need to be implemented in 2029 at 0.5 MtCO2e/year and scaled up to 5.7 MtCO2e/year by 2032. This would be achieved by developing and commercialising the St Fergus gas terminal by 2024 (capturing 10 MtCO2/year by 2030 of non-biogenic emissions), having the Acorn hydrogen site operational by 2025, and developing the St Fergus DACCS facility by 2026. The captured CO2 can then be stored in depleted oil and gas reservoirs in the North Sea, which have a capacity of circa 46 GtCO2[15].

The Scottish Government reviewed the update in May 2022[16], and concluded that the proposed NETs ambitions are unrealistic. This is due in large part to the UK Government’s announcement that the Scottish CCUS Cluster would not be granted Phase 1 status for the CCUS Fund[17]. However, the development of a Scottish Cluster is still possible, due to £425,000 of direct financial support for the St Fergus site and the launch of the £5M CO2 Utilisation Challenge Fund[18] in 2022. The Scottish Government also accepts that these BECCS ambitions are unrealistic, as a 2022 paper by Ricardo[19] highlighted a lack of available home-grown sustainable biomass within Scotland to meet future BECCS demands (according to the TIMES and 6CB pathways), resulting in a heavy reliance on biomass imports.

The CCPu also detailed actions for the Scottish Government to undertake, some of which have been completed, including: feasibility studies on biomass feedstock availability[19] and a horizon scan of international NETs deployment[20]. A draft Bioenergy Action Plan will be published in 2023, which will identify the most appropriate and sustainable use for bioenergy resources across Scotland. In addition, a proportion of the £80M from the Emerging Energy Technologies Fund will be provided to NETs partners[16]. The Scottish Government also acknowledges suggestions to use CfDs and the UK ETS to reward negative emissions (both of which are outlined in section 1.3 of the technical appendices document), in a bid to develop a NETs market, and develop a cross-sectoral approach towards the sustainable biomass use. One of the primary outcomes from this report will be to supply up-to-date, industry-specific information on future demand for NETs, to allow a more accurate assessment of the future implementation of NETs technologies for Scottish Government ministers and analysts.

The Committee on Climate Change (CCC)’s 6th Carbon Budget,[21], published in December 2020, provided detailed Net Zero targets for the UK, which were partitioned out to all respective UK countries (including Scottish specific targets). Similar to the CCPu, a chapter was dedicated to NETs deployment, which stressed the importance of adopting engineered NETs early on, and modelled 5 different scenario pathways: Headwinds, Widespread Engagement, Widespread Innovation, Balanced Net Zero Pathway, and Tailwinds.

The CCC’s target for the UK is to reduce emissions by 78% by 2035 (relative to 1990), which is significantly more ambitious than the UN’s targets of 68%. This will build on the current investment of around £10Bn per year to around £50Bn by 2030[7]. In the 2023 Spring budget, a further £20Bn of UK Government support for CCUS was announced.[22]

According to the ‘balanced’ pathway, emissions fall rapidly in the electricity supply sector due to further adoption of renewables, whilst the heating and transport sectors decarbonise in the mid-2030s due to heat pumps and electric vehicles. Emissions from manufacturing and construction drop in the late 2020s, because of electrification and low carbon hydrogen, whilst emissions from agriculture and aviation stagnate and/or increase. These latter emissions must be offset using NETs.

Based on the GHG removal sector scenarios modelled in the 6th Carbon budget, the scale of UK NETs deployment via BECCS by 2050 ranges from 44-97 MtCO2/year. This figure is composed of BECCS Power (16-39 MtCO2/year), BECCS EfW (1-10 MtCO2/year), BECCS Industry (3-4 MtCO2/year), BECCS Hydrogen (0-36 MtCO2/year), BECCS Biomethane (0.5-0.6 MtCO2/year), and 0-15 MtCO2/year for DACCS. The resulting demand for biomass increases to around 190-360 TWh, the UK domestic resource supply varies from 95-195 TWh[23] – indicating that imported biomass would be highly likely to be required to meet these future demands.

According to the 6th Carbon Budget, Scotland has more ambitious targets of achieving Net Zero by 2045, which will require 3-9 MtCO2/year of engineered NETs by 2050. Interestingly, the ‘balanced’ pathway is simulated to reduce Scottish emissions by 64% by 2035 and 99% by 2050 (compared to 1990 levels) without using NETs.

The requirements for NETs are often linked back to the targets for carbon emissions. A high emphasis can sometimes be placed on NETs to meet national targets. This study used a bottom-up approach in determining the NETs potential in Scotland to provide a more realistic assessment of NETs possible contribution. The policies required to enable NETs varies in the pathways, showing that there is considerable variation in NETs deployment possible.

1.3 Negative emissions technologies

The negative emissions technologies covered in this report are separated into the sectors they broadly relate to. The sectors considered were Power, Energy from Waste (EfW), Industry, Hydrogen, Biomethane, Direct Air Carbon Capture and Storage (DACCS), Biochar and Biofuel. The capture equipment used may be applicable across multiple sectors. For example, if it is assumed biogenic CO2 emissions from Power, EfW and Industry arise from combustion, a number of capture methods may be equally applicable to these sectors. Capture equipment and NETs (as defined in this report) are discussed in greater detail within sections 1 and 2 of the technical appendices document, but a brief summary is given in this section.

1.3.1 Technologies included in this study

Table 4 provides the technologies that were considered in and out of scope in this report. The out of scope/non-engineered NETs are outlined in summary form in Appendix 9 of the technical appendices document.

Table 4: Technologies considered in this study

In scope:

- DACCS

- BECCS Power (including Combined Heat and Power (CHP))

- BECCS Hydrogen

- BECCS Energy from Waste (EfW)

- BECCS Biogas (e.g., biomethane)

- BECCS Biofuels (e.g., bioethanol)

- BECCS for Fermentation

- BECCS Industry

- Biochar

Out of scope

- Reforestation and afforestation

- Soil Carbon Sequestration

- Enhanced Weathering

- Ocean Alkalinisation

- Ocean Fertilisation

- Embodied carbon practices (e.g., using wood in construction or creating concrete via DACCS)

1.3.2 Technology readiness levels (TRL)

Throughout sections 1 and 2 of the technical appendices, reference is made to the technology readiness level (TRL) of NETs. This is a method of categorising the state of development of a technology. Technologies are assigned a TRL of 1 to 9 depending on their maturity, with 1 being the least developed and 9 the most. TRL was originally developed by NASA and the terminology used in definitions of each TRL level often reflect this, in the context of NETs, TRLs may be defined as shown in Table 5.

After reaching a TRL of 9, the focus shifts to full commercial deployment, driven by factors like profitability and competition with alternative technologies. This study explicitly addresses this next step in the pathways section.

Table 5: Categorisation of technologies by technology readiness level (TRL)[24]

Research and development

- TRL 1 - Basic Research

- TRL 2 - Applied Research

Applied research and development

- TRL 3 - Critical Function or Proof of Concept Established

- TRL 4 - Laboratory Testing/Validation of Component(s)/Process(es)

- TRL 5 - Laboratory Testing of Integrated/Semi-Integrated System

Demonstration

- TRL 6 - Prototype System Verified

- TRL 7 - Integrated Pilot System Demonstrated

Pre-commercial deployment

- TRL 8 - System Incorporated in Commercial Design

- TRL 9 - System Proven and Ready for Full Commercial Deployment

1.3.3 BECCS Power

The archetypical bioenergy power facility could be a solid biomass fuel (e.g., wood pellet or wood chip) boiler supplying steam to a steam turbine. The site may be power generation only or make use of waste heat from the process and be classed as combined heat and power (CHP). To such sites, amine post-combustion capture equipment may be fitted to capture bio-derived CO2 from the flue gas. This briefly describes a system currently at TRL 8-9, however, attaching post-combustion capture to generating stations comes with an energy penalty as heat is required to regenerate the CO2 capturing solvent.

An alternative method is oxy-fuel combustion. This broadly refers to a system where a stream of oxygen (rather than air) is provided for combustion. The advantage of this method is a higher CO2 concentration in the flue gas, making CO2 capture easier. The disadvantage is the requirement to run an air separation unit (ASU) to provide the oxygen stream. This combustion method, providing steam to a steam turbine, has been demonstrated at pilot level but not at commercial scale, so has a TRL of 7.

Existing at lower TRLs is pre-combustion capture. Biomass is gasified to produce syngas, CO2 can be removed from syngas before combustion via physical absorption, reducing capture costs. Disadvantages of this system are high capital and operating costs, a system incorporating both integrated gasification combined cycle (IGCC) power generation and carbon capture is also yet to be demonstrated.

1.3.4 BECCS Energy from Waste

Energy from waste (EfW) plants typically comprise a boiler and steam turbine, similar to a BECCS power site. Where EfW differs is the fuel input, which may include municipal solid waste (MSW), commercial or industrial waste. The fuel may therefore vary widely in moisture content, calorific value and biogenic fraction. The latter is estimated to be between 40% and 60% of waste utilised in EfW plants. As such, the NETs potential from EfW is included within this study.

Similarly, to BECCS power, post-combustion capture technology can be retrofitted to existing EfW plants (accepting that similar energy penalties will apply). Whilst post-combustion capture has been demonstrated commercially in other applications, it has yet to be integrated at a commercial scale with EfW, leading to a TRL of 7 in this case.

1.3.5 BECCS Industry

The BECCS industry category spans a range of activities. These encompass manufacturing of wood-based products such as paper mills, wood panel (orientated strand board and medium-density fibreboard) and wood pellet production, where wastage from processing provides an integral source of fuel. Such sites are similar to BECCS power and the same TRLs are assumed.

Cement production was also considered for its NETs potential. As part of the production process, clinker is produced in kilns at operating temperatures between 1400degC and 1500degC. This is traditionally achieved using fossil fuels, however, a limited amount of fuel switching (using waste derived fuel called solid renewable fuel (SRF)) has been demonstrated, with co-firing of up to 30-40% biomass is possible. Post-combustion capture may be applied to this process. Biomass kilns with CCS is at TRL 7, whilst co-firing kilns with CCS may be considered to be higher, with some commercial scale facilities planned[25].

In comparison to industries incorporating combustion process, CO2 capture from the brewing and whisky industry is relatively simple. Fermentation of the grain or malt input results in a high purity stream of CO2 that may be readily captured. This could constitute an early opportunity to achieve around 0.5MtCO2/year of negative emissions.

1.3.6 BECCS Biomethane

Biomethane can be produced by the upgrading or methanation of other biomass derived gases (such as biogas or syngas). Thermochemical routes, such as gasification and pyrolysis may be used to produce syngas from a range of solid biomass feedstocks, including MSW, energy crops and forest residues. Alternatively, biogas can be produced by anaerobic digestion (AD) of wet biomass, such as manure, sewage sludge and food waste. The resulting biogas or syngas has a methane content ranging from 40-60% (depending on feedstock used), with CO2 comprising the majority of the remaining volume. Upgrading of these gases increases the methane concentration to 93-97% by removal of the CO2.

Upgrading of biogas from AD is an established process (TRL 9), with the resulting biomethane often mixed with natural gas in the grid. The upgrading process presents an opportunity to capture and store a highly concentrated stream of biogenic CO2.

1.3.7 BECCS Hydrogen

Production of biohydrogen is a further process of the biomethane production described in section 1.3.6. Carbon is removed from the biomethane using processes that may be employed for natural gas, steam methane reforming (SMR) and auto thermal reformation (ATR). Following these processes, CO2 is separated from the Hydrogen stream using amine based (MDEA) or vacuum pressure swing adsorption (VSPA) capture, resulting in a CO2 offtake of 22gCO2 to 71gCO2 per MJ of Hydrogen for SMR and ATR respectively. TRLs for these processes range between 4 and 9.

1.3.8 Direct Air Carbon Capture and Storage (DACCS)

Direct air carbon capture and storage (DACCS) refers to various means of removing CO2 directly from the atmosphere and storing it. TRLs for these technologies range from 4 to 7, with some pilot scale plants in operation. Methods that have been demonstrated can be split into liquid solvent DACCS and solid adsorbent DACCS. The former method may use a potassium hydroxide solution, which reacts with the CO2 in the air, producing potassium carbonate. The solution is then reacted with calcium hydroxide, producing calcium carbonate and potassium hydroxide (which may be reused in the air contactor to capture CO2). The resulting calcium carbonate is then heated in an oxy-fuel calciner to release the CO2 and is later reformed into calcium hydroxide for reuse. Whilst it is assumed that the potassium carbonate is regenerated and reused, the system must be replenished with calcium carbonate at a rate of 0.03t per tCO2. The solid adsorbent process uses a solid material filter to capture CO2, the filter is then heated to a relatively low temperature (80degC to 120degC) to release the CO2. This process degrades the sorbent material overs time, an average depletion rate of 7.5kg/tCO2 gives the sorbent a lifetime of less than 1 year. Supply chains for adsorbent material will need to expand substantially to employ this technology at scale.

DACCS has advantages in that there are few restrictions to deployment locations (other than a means of storing the captured CO2). The high energy demand of these systems, particularly with regards to heat (with demand between 1.46-2.45 MWh/tCO2, see section 1.2.2 in the technical appendices document), mean that they would be ideally deployed near sources of waste heat. This would be most useful for solid adsorbent DACCS, where temperature demands are lower. Liquid solvent, however, requires temperatures in excess of 900degC in the calciner. Providing this by natural gas (as is currently the case) reduces the NETs CO2 removal per tonnes of CO2 captures, as the CO2 released to fuel the process must be discounted.

Unlike other forms of NETs, the primary output of DACCS is the captured CO2 (as opposed to generated power or heat). The potential to sell the captured CO2 for utilisation purposes may be considered in the future, once the storage infrastructure is fully operational. Accordingly, capture costs for DACCS are potentially greater. Estimates for this range from as low as £67/tCO2 up to £507/tCO2. With no other associated revenue streams, the technology will be reliant on a negative emissions market emerging.

1.3.9 Biochar

Biochar is a charcoal-like product formed when biomass is thermally decomposed in very low or zero oxygen levels. This process is known as pyrolysis, which may be further categorised into fast and slow pyrolysis. Slow pyrolysis is favoured when biochar (as opposed to biofuel) production is prioritised. Applicable feedstock can vary greatly, with the process able to use most forms of dry biomass or waste material, with the feedstock providing most of the energy for the process. The resulting biochar retains carbon in the feedstock is a stable form and, applied to soil, may be considered a form of carbon capture and storage. Applying biochar to soil has further benefits in improving soil condition by absorbing heavy metals (e.g., arsenic and copper), increasing water and nutrient retention, and stabilising pH and microbial populations. By-products of biochar production include syngas and bio-oil, which may be combusted to provide heat and power.

The application rate of biochar must be limited to 30-60 t/ha, to ensure soil surface reflectivity does not decrease significantly and damage crops. Therefore, the deployment of biochar is also limited. The maturity of the technology is also debateable, with conflicting estimates for TRL between 3 to 6, or 5 to 7.

1.3.10 Common barriers

Although the deployment of NETs is accelerating, there are still a number of challenges and barriers that need to be overcome. These can be broadly categorised into economic, technical, infrastructure, supply chain, environmental, social and regulatory barriers.

Section 2.1 in the technical appendices document provides a more detailed overview of the common barriers to NETs implementation.

1.3.10.1 Technical

The most cited barrier for NETs is the need to develop CO2 transport and storage infrastructure; there could be competition for storage capacity once this infrastructure is online. The high energy requirements of NETs are another common limitation, with oxy-combustion capture and DACCS being particularly energy intensive. Pre-combustion capture has an advantage over post-combustion capture in that physical absorption instead of chemical absorption can be used for the capture process due to the higher pressures involved. As a result, pre-combustion capture is associated with lower energy penalties due to the lower energy needed for physical solvent regeneration. Finally, engineered NETs have not yet been shown to operate at scale, and hence there is a knowledge constraint associated with operating these facilities.

1.3.10.2 Economic

Economic barriers to NETs exist due to the high capital cost associated with upfront investment. As an example, constructing a 1 MtCO2/yr liquid solvent DACCS plant would cost £951.4M (see section 2.7 in the technical appendices document). Additionally, several NETs technologies possess high operating costs. This is most prevalent for DACCS, which requires the construction of large capture units to process and extract the diluted concentrations of CO2 in the air (~400 ppm) and consumes significant heat and power.

1.3.10.3 Policy and Regulatory

Currently the costs of NETs are prohibitively high unless additional financial support is provided, resulting in economic barriers to their widescale deployment. The UK Government are proactively considering the most appropriate support to limit such barriers; however, support has been limited to date. Therefore, further financial incentives are necessary in order to provide stakeholders with greater long-term clarity and revenue certainty.

Additionally, the requirement to have effective monitoring, reporting and verification (MRV) standards in place is another key challenge. The high resource requirements (bioresources for BECCS and biochar & electricity/heat for DACCS), lack of CO2 T&S infrastructure, and lack of policy incentives for GGRs are some of the main constraints towards deployment. Most notably, without a price or reward for negative emissions, GGR deployment may not be financially viable for the private sector[6].

1.3.10.4 Environmental

A major environmental challenge relates to the changes in land use to accommodate the large amounts of feedstock required for BECCS and biochar, which may result in species loss and reduced biodiversity. The future availability of bioresources for BECCS and biochar have been used in this report. Furthermore, land use changes may affect the price of agricultural commodities, such as food, which will negatively impact the poorest households.

1.3.10.5 Social

Public perception is an important aspect to ensure the successful wide-scale deployment of NETs; however, the unfamiliar nature of novel technologies may pose as a risk to gaining public support. To date, prior studies have shown that public acceptance varies across different NETs, with nature-based solutions having higher acceptance rates and engineering NETs being seen as a risk. A study on the perception of BECCS was recently undertaken in the UK, where a large majority (79%) of participants stated that prior to the experiment they knew little to nothing about BECCS[26].

1.3.10.6 Supply chain

The increased demand for negative emissions will result in an increase in the demand for carbon capture equipment. It can therefore be expected that the number of suppliers will need to increase to meet this demand in order to avoid significant supply chain barriers.

1.4 Non-engineered NETs

GGRs can be divided into two categories, nature-based and engineered removals – this report focusses on engineered solutions. A brief summary of nature-based/non-engineered NETs is presented in Appendix 9 of the technical appendices document.

There are four main categories of nature-based NETs:

1. Forests and forestry management

- Afforestation, reforestation, and forest management are various land-based GGRs that consider carbon removals through woodland expansion and forest management.

- The maximum technical potential of this GGR in the UK is 26.5 MtCO2/year by 2050, which is the highest of the land-based GGRs, however, still notably lower than engineered GGRs[27].

- It should be noted that carbon can move from this GGR to others, due to biomass supply for biochar, BECCS and wood in construction. Additionally, GGR afforestation competes with biochar and bioenergy feedstock (for BECCS) for land.

2. Peatland/ peatland restoration

- Peatland habitat restoration as a GGR method involves the re-establishment of functional, and hence carbon-accumulating, peatland ecosystems in areas that have been degraded to the extent they no longer sequester CO2.

- The maximum technical potential of this GGR in 2050 is 4.7MtCO2/year; this figure is based on restoration of 750 kha of the most degraded peatlands in the UK[27]

3. Soil carbon sequestration

- Soil carbon sequestration is a GGR method that considers how the carbon content of soil can be increased through land-use or land-management change. It is more relevant to agricultural land use, and hence has greater impact on cropland and grassland.

- The maximum technical potential of this GGR is 15.7 MtCO2/year by 2050, which again is considerably lower than engineered GGRs[27]

4. Wood in construction

- Wood in construction as a GGR method is defined as the increased use of domestically produced wood in buildings to permanently store carbon. This has the potential to increase the amount of biogenic carbon stored in harvested wood products (HWP).

- Due to several limitations, the maximum technical potential in the UK of this land-based GGR is 3.3 MtCO2/year by 2050, which is significantly less than any other engineered GGR[27].

Contact

Email: NETs@gov.scot