Publication - Research and analysis

Monthly economic brief: February 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic outlook

The economy is forecast to contract in 2023 as the inflation rate starts to fall sharply.

- The economic outlook remains challenging, with the economy broadly at the same level as February 2022. Although energy prices have fallen back slightly from their peak, prices will remain elevated over the coming year, despite inflation falling back from its current rates, and tightening monetary conditions will add further pressures to household finances.

- At a global level, in January the IMF forecast global economic growth to slow to 2.9% in 2023, with Europe in particular seeing slower growth. Euro Area growth is forecast to slow to 0.7% over the year whilst in the USA it slows to 1.4%.[17] However, the overall forecast for growth in 2023 has been revised up by 0.2 p.p since October, in part reflecting the potential for stronger growth following the recent reopening of China's economy.

- Global inflation is estimated to be 8.8% in 2022 and is expected to fall back but remain elevated in 2023 at 6.6%, with rising interest rates, weaker demand and falling energy prices to moderate inflation further into 2024 to 4.3%. For advanced economies the IMF forecast inflation to fall to 2.6% in 2024.

- Reflecting weakening global conditions, in December, the Scottish Fiscal Commission forecast that Scotland would enter a recession during 2022, and recover only slowly from the shocks of the pandemic and the war in Ukraine, with GDP not returning to pre-pandemic levels until 2025 Q3.[18] Real household incomes will be particularly affected by inflation, falling by a record amount, and are not forecast to recover to 2021-22 levels until 2027-28.

- At UK level, the Bank of England and the Office for Budget Responsibility forecast the UK will enter recession, with inflation and tightening financial conditions expected to cause a significant fall in real household disposable incomes and demand over 2023-24.[19]

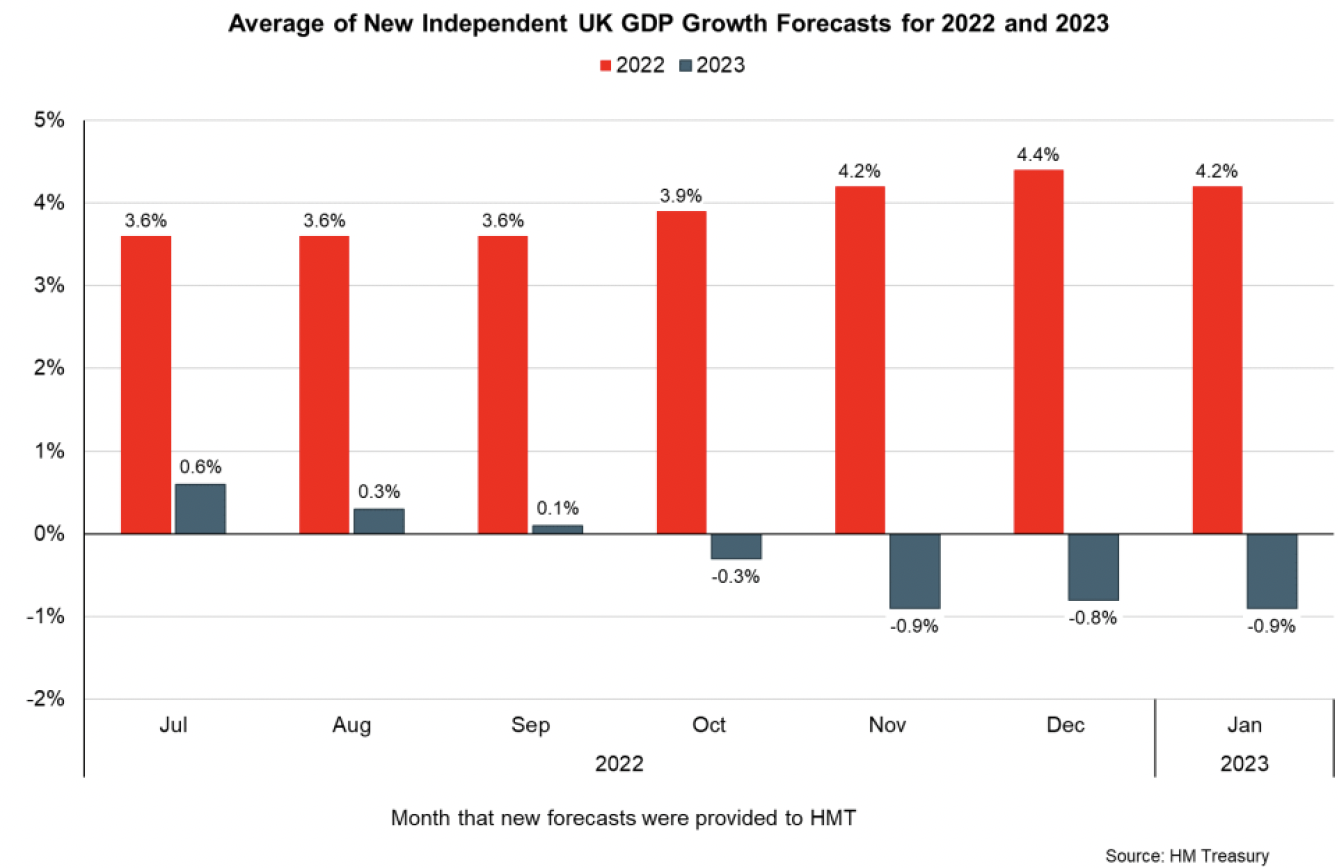

- More broadly, the average of new independent forecasts in January (published monthly by HMT) highlights the downgrades over the past year to UK 2023 growth forecasts as economic conditions have weakened.[20] Latest forecasts from December project, on average, that UK GDP will fall 0.9% in 2023, broadly unchanged for the last three months, and in stark contrast to the average expectation of 2% growth from forecasts released at the start of the year in February.

- There is significant uncertainty over the depth and duration of the expected recession, the pace at which inflation will fall back towards the 2% target, and the pace at which output will return to pre-recession peaks. This will reflect domestic and global economic developments, the impacts of fiscal and monetary policy and the persistence of the current energy supply and price shock.

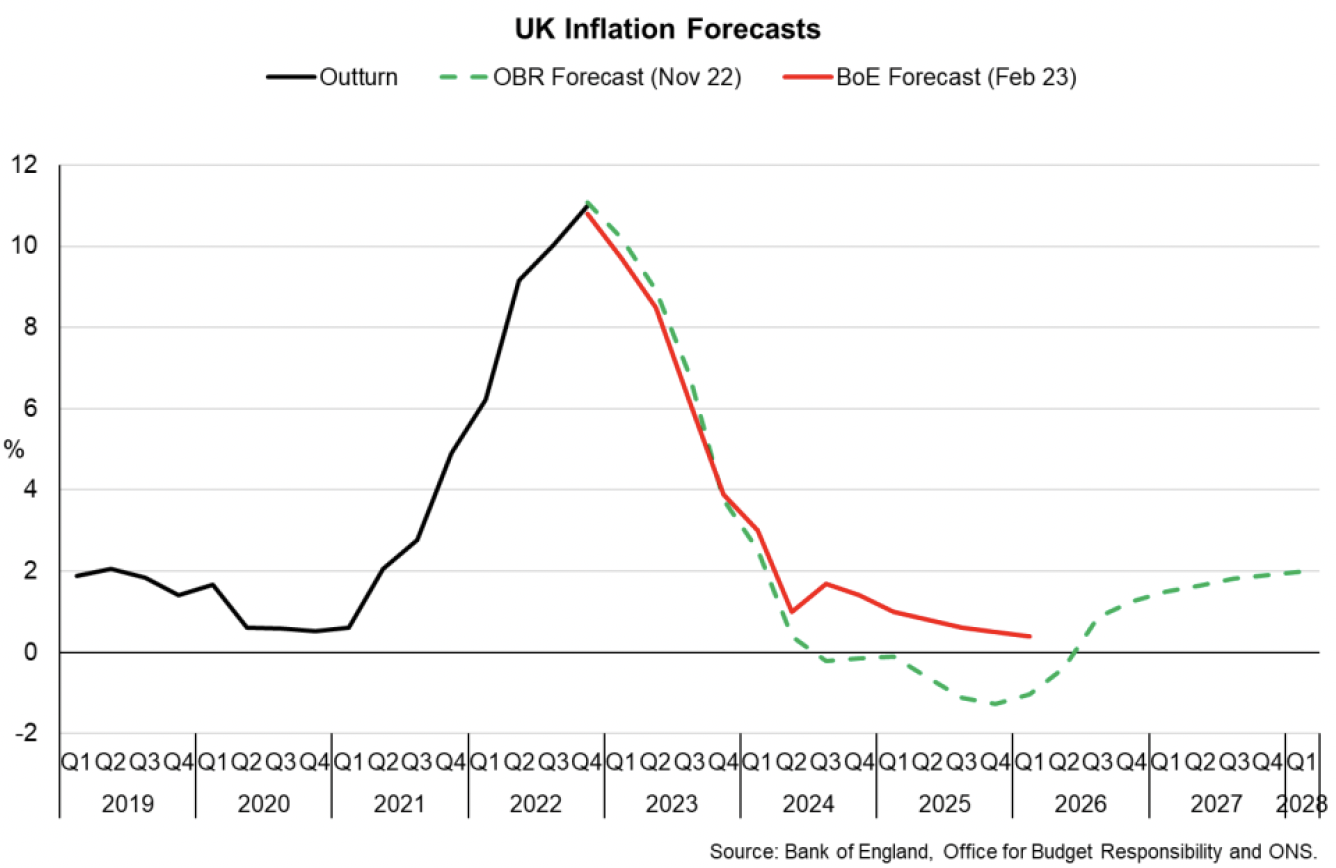

- In February, the Bank of England forecast the UK economy to remain in recession from Q1 2023 through to Q1 2024 with UK GDP forecast to fall 0.5% in 2023 (revised up from a 1.5% fall in November forecast) and 0.25% in 2024 (revised up from a 1% fall). This is much shallower than their November forecast, reflecting a reassessment due to strength in the labour market, and the rapid decline in the contribution of energy to inflationary pressures.

- In November, the Office for Budget Responsibility forecast the UK recession to last just over a year from Q3 2022 with UK GDP forecast to fall 1.4% in 2023 and grow 1.3% in 2024. Both forecasts expect a notably shallower recession than those in 1980, 1990 and 2008. Furthermore, the inflation rate is forecast to fall back sharply over 2023 to around 4% by the end of the year and below 2% in 2024.

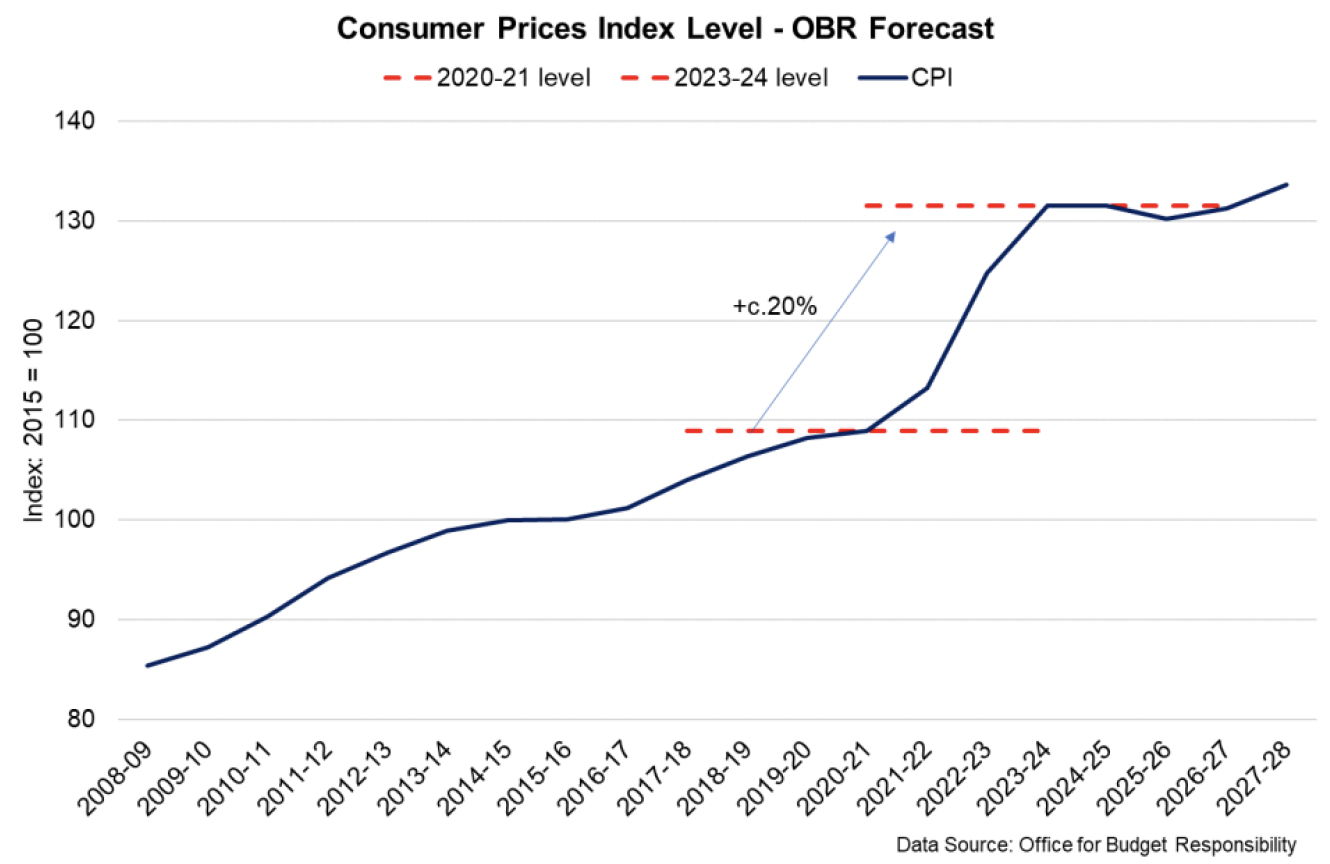

- However, even when the inflation rate does fall back towards target in 2024, the price level will remain notably higher than it was in 2021. The OBR forecast price levels in 2023-24 to be around 20% higher than in 2020-21. Previously it had taken around 9 years from 2008-09 for the price level to rise 20%.

- As such, the outlook for households and businesses remains extremely challenging as the economy continues to adjust to the significant increase in price levels over such a short period of time, while trend growth estimates for the UK, which reflect the underlying capacity of the economy to grow without generating inflation, continue to be reduced, reflecting weak investment and productivity growth.

Contact

Email: OCEABusiness@gov.scot