Publication - Research and analysis

Monthly economic brief: February 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Businesses

Business activity fell at a slower rate in December though cost pressures broadened.

Business activity

- The Purchasing Managers Index (PMI) business survey indicates that business activity in Scotland's private sector continued to contract in December (48.3), though to a lesser extent than in recent months across the manufacturing and services sectors.[5]

- This was partly driven by less widespread falls in inflows of new business and orders (46.0) during the month, though the indicator did signal a sixth consecutive month of contraction in December. The persistence of this period of falling business activity alongside elevated inflationary pressures, are reflected in a further reduction in business optimism (53.6), which remained positive overall but had weakened notably over the second half of the year.

Business costs

- Rising costs (energy, materials, staffing) continued to present a significant challenge to business operations and resilience in the face of weakening demand in the final quarter of 2022. There are signs that the pace of cost increases is easing, however annual rates remain significantly higher than they were prior to the pandemic.

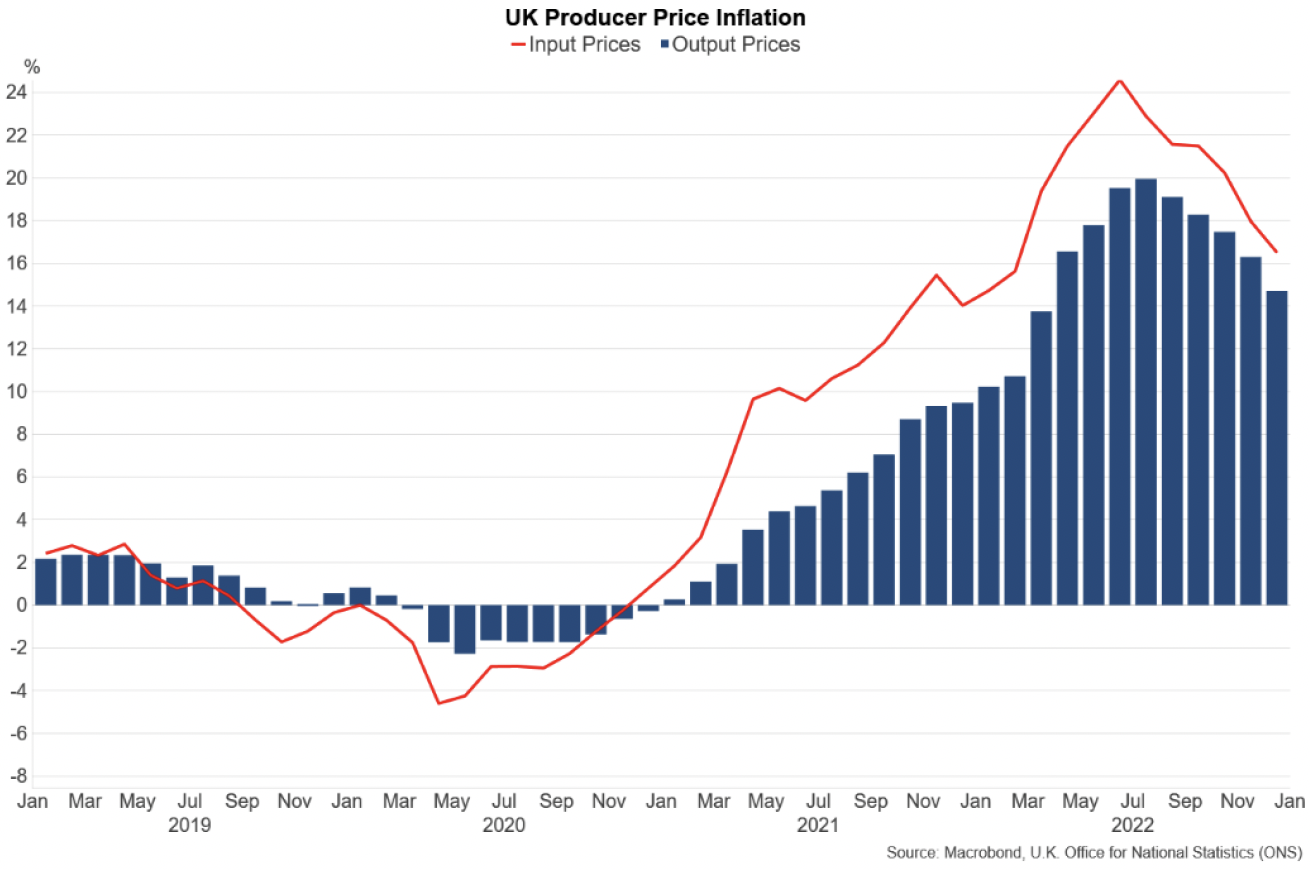

- Producer price inflation (changes in the prices of goods bought and sold by UK manufacturers, including price indices of materials and fuels purchased and factory gate prices) rose by 16.5% over the year to December, though the annual rate eased for the fifth consecutive month and prices fell by 1.1% over the month.[6]

- Input fuel costs have increased the most over the past year (70%) followed by crude oil (28%) and imported food materials (26.2%), however over the month of December, most input cost categories fell; crude oil (-10%), parts and equipment (-0.8%), chemicals (-0.4%)

- Similarly output price inflation also continued to ease back at the end of the year to 14.7% in December, down from the recent peak of 19.9% in July, but also remains elevated. Over the month of December, output prices for petroleum products fell 11.9% while food products continued to rise by 0.8%.

- PMI business survey data for Scotland also indicated that the pace of input price rises across the services and manufacturing sectors continued to moderate in December, while remaining elevated overall, with businesses citing higher wages, inflation, energy prices and Brexit as key factors generating upward pressure on prices.

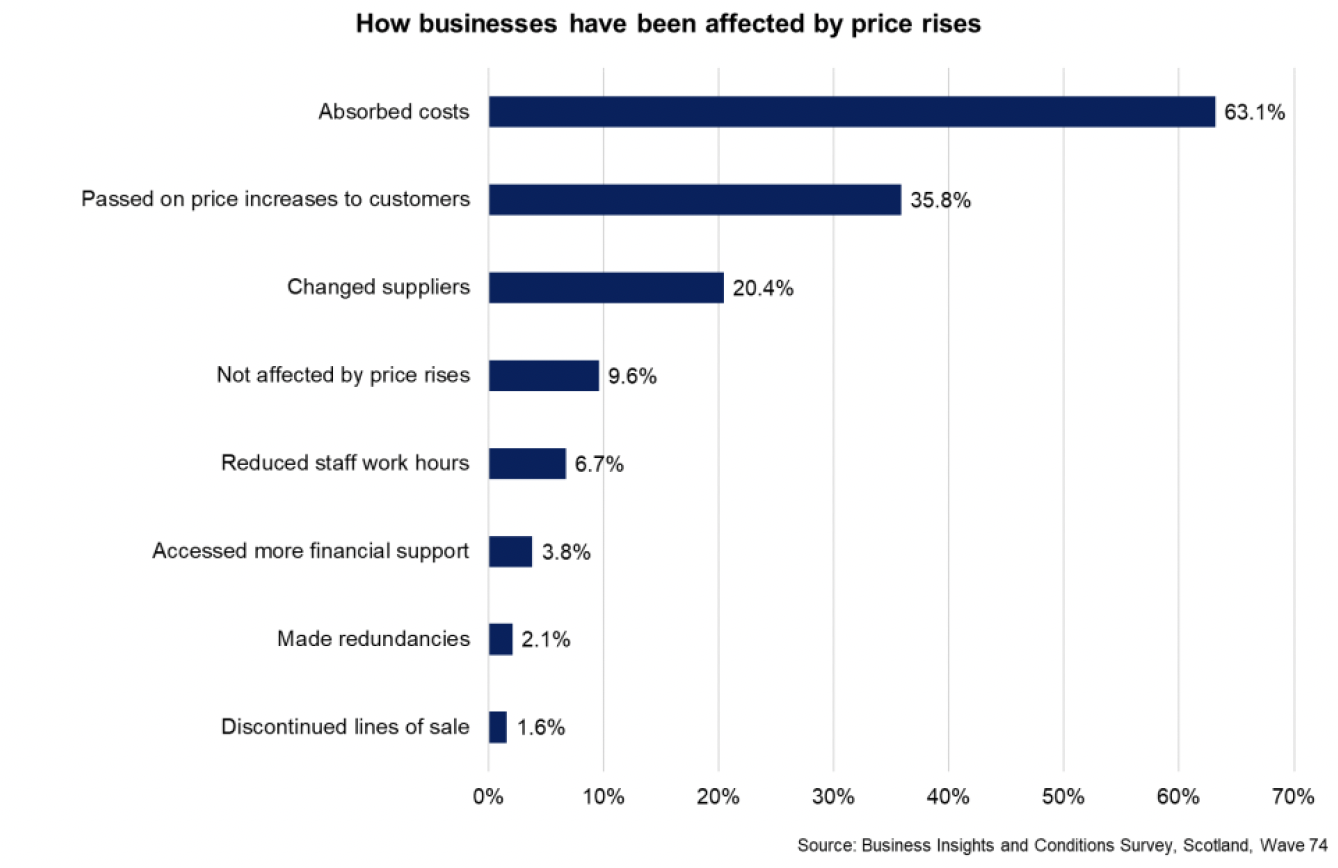

- Business Insights and Conditions Survey (BICS) data provide latest insights into the effects on businesses of price rises. In January, 63% of businesses reported that they had to absorb costs, 35% reported having to pass on price increases to customers and 20% had to change suppliers. A much lower percentage of firms reported having to access more financial support (4%) and having to reduce staff work hours (7%), however the latter continued to increase from previous months, as has the proportion having to change supplier, indicating that businesses are adopting a broader set of approaches to tackling the persistence of cost pressures.[7]

- There continues to be notable differences across sectors. For example, 20.4% of Accommodation and Food sector businesses and 15% of Arts, entertainment and recreation businesses reported having to reduce staff work hours (compared to 6.7% for all businesses). Furthermore 34.3% of Professional, Scientific and Technical Activity businesses and 32.6% of Information and Communication businesses reported that they had not been affected by price rises (compared to 9.6% for all businesses).

- This further reflects that costs rises are impacting sectors differently and business responses to price rises will reflect a range of factors such as the nature of the business and customer base within sectors and the options available to improve efficiency and reduce costs.

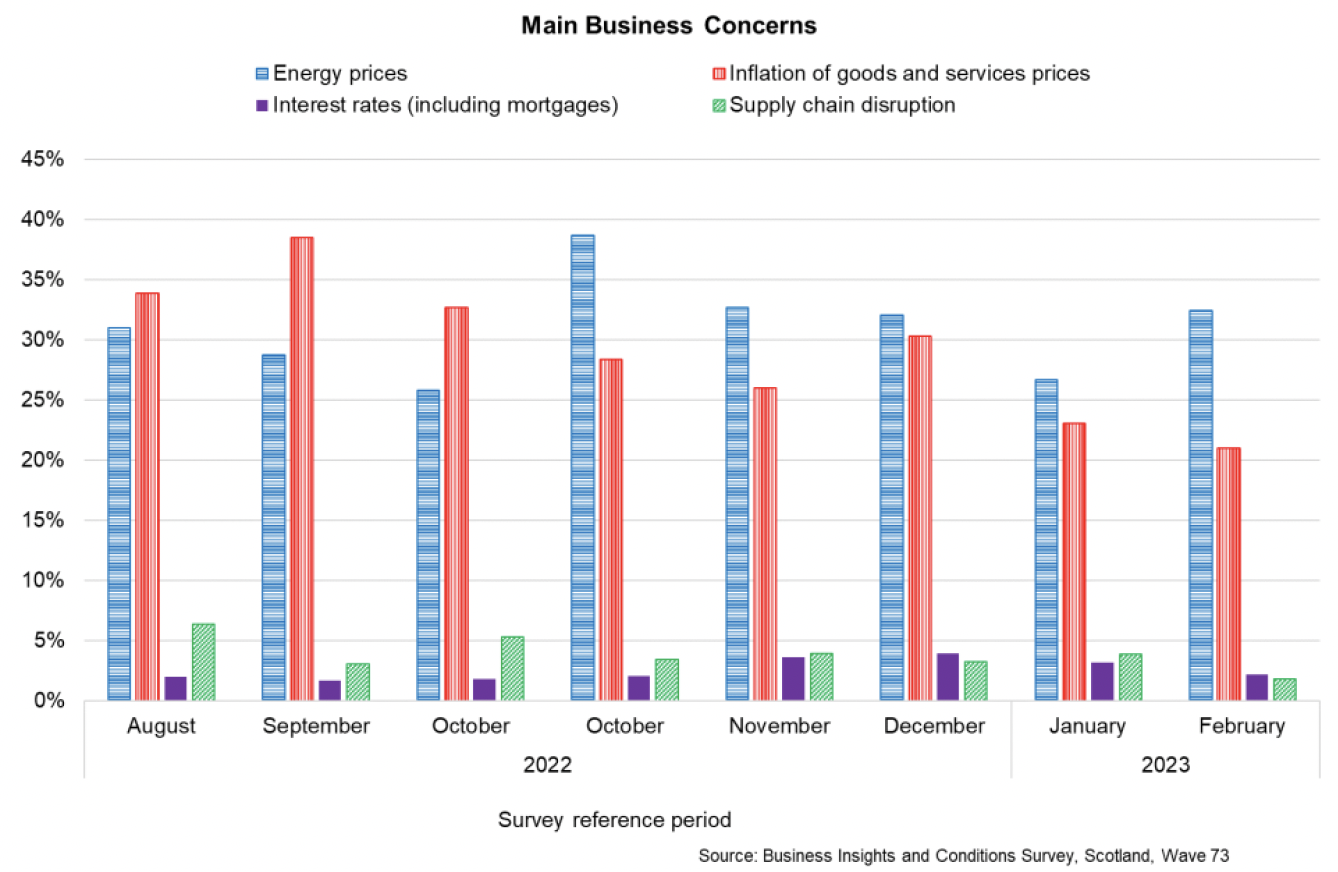

- Overall, the main concern for business at the start of 2023 continues to be energy prices (32.4%), which remains elevated, and inflation of good and services prices (21%), which has been decreasing through the turn of the year. Much lower and declining percentages of businesses are concerned about supply chain disruption (1.8%), which may reflect that disruption has eased or businesses have been changing suppliers where required, while concerns about interest rates (including mortgages) (2.2%), fell slightly at the start of the year.

- Similarly, the latest Scottish Business Monitor report for Q4 2022 indicated that energy prices were the most common cost issue for businesses (73%), followed by input costs (69%). However, looking ahead, a higher share of respondents reported employee costs (75%) than energy costs (71%) as a key cost driver they are expecting in the next 6 months.[8]

Contact

Email: OCEABusiness@gov.scot