Publication - Research and analysis

Monthly economic brief: February 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Labour Market

The labour market remains tight, however recruitment activity has slowed.

Official labour market statistics

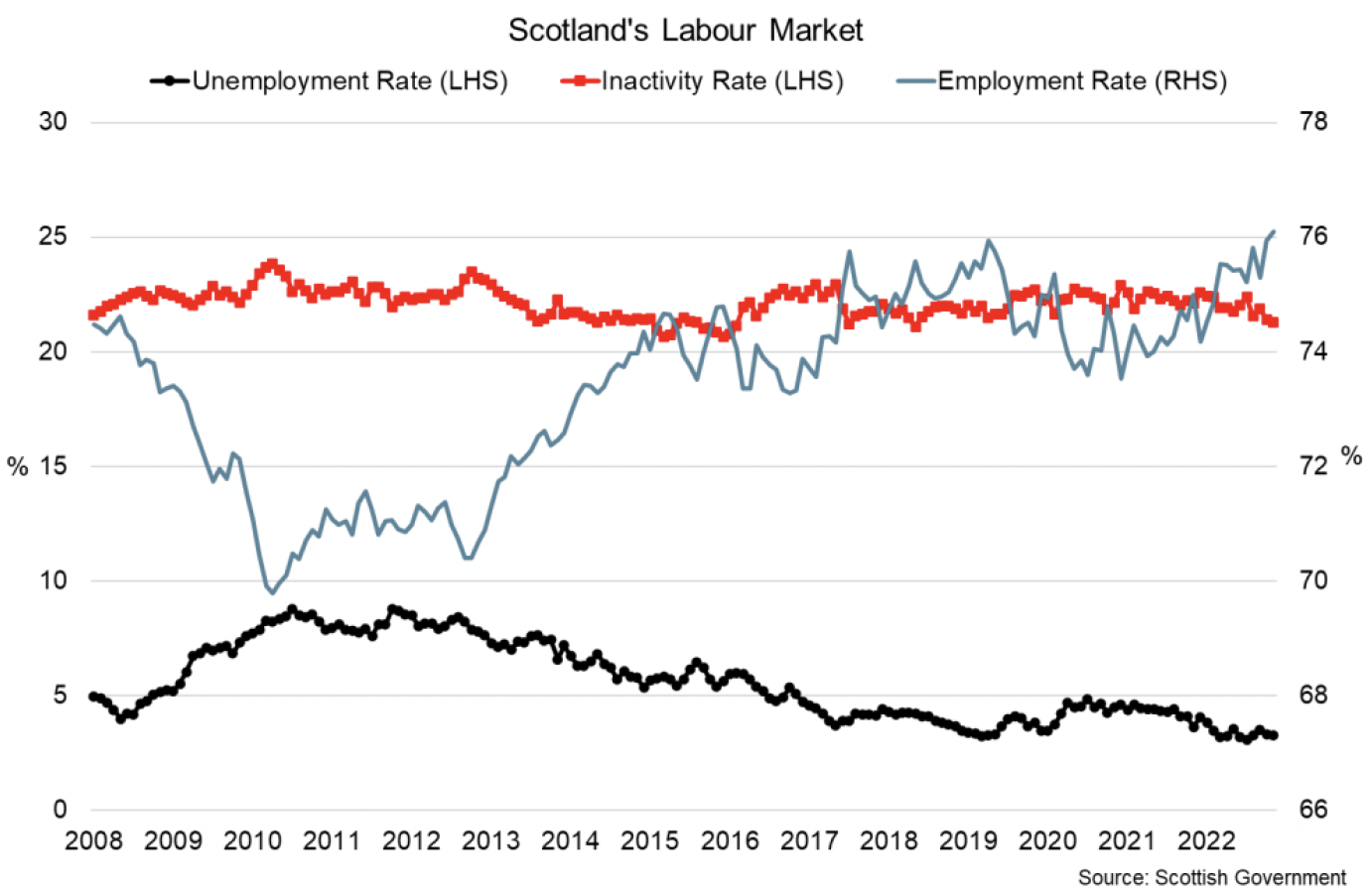

- The latest labour market statistics for September to November 2022 in Scotland show there were 2.7 million people in employment with the employment rate rising by 1.1 percentage points over the year to 76.1% and 92,000 people were unemployed with the unemployment rate falling 0.4 percentage points to 3.3%. This is a similar pattern to the UK labour market as a whole with the employment rate rising 0.2 percentage points over the year and unemployment falling 0.4 percentage points.

- Scotland's inactivity rate fell 0.8 percentage points over the year to 21.3% with 733,000 people economically inactive in Scotland. The fall in the inactivity rate continues a recent downward trend in Scotland with overall inactivity rates broadly similar to pre-pandemic levels. This is a different recent pattern to the UK as a whole, in which the inactivity rate increased by 0.2 percentage points over the year to 21.5% continuing an upward trend from the start of the pandemic.[9]

- Latest PAYE data signals a further increase in employment in December with the number of PAYE employees rising 5,000 (0.2%) over the month and is 47,470 higher than in December last year.[10]

Demand and supply of staff

- Business surveys signal that labour market conditions have remained tight going into the final quarter of the year, however recruitment activity has slowed.

- The RBS Report on Jobs for December signalled that growth in demand for staff remained positive (55.4) but had slowed to its softest rate since the start of 2021.[11] For businesses seeking to recruit, supply side challenges in the labour market have also continued with candidate availability (labour supply) falling and at an accelerated rate in December (30.5). Alongside underlying challenges of skills shortages and Brexit, recruiters cite the uncertain outlook, cost of living crisis and fear of recession as key factors weighing on the movement of labour.

- The underlying tightness in the labour market continued to provide upward pressure to starting salaries in December with the overall pace of growth picking up over the month (74.3), however remaining slightly slower relative to the first half of the year.

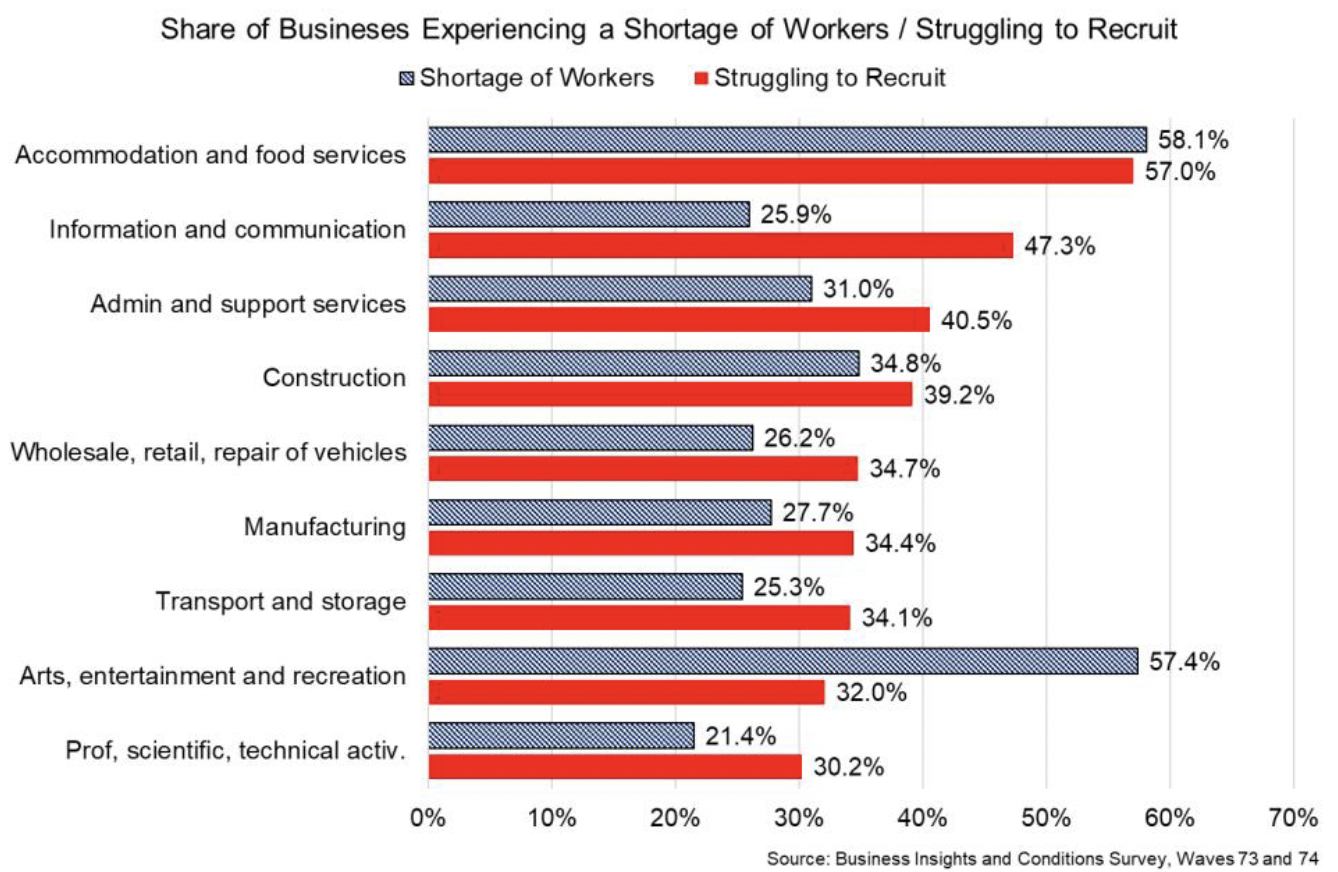

- Labour shortages are affecting a range of sectors with BICS data indicating 33.6% of businesses experienced a shortage of workers at the start of January. The overall share has fallen from the end of November when it was 43.4%, however remains highest in accommodation and food services (58.1%), arts, entertainment and recreation (57.4%), and construction (34.8%) sectors.[12]

- Furthermore, when asked about recruiting in December, 42.1% of all business reported experiencing difficulties recruiting employees. This is highest within accommodation and food services (57%) and information and communication (47.3%). Most businesses responded that a lack of qualified applicants (63.9%) and a low number of applications (55.6%) were reasons for why the business experienced difficulties in recruiting employees.

Earnings

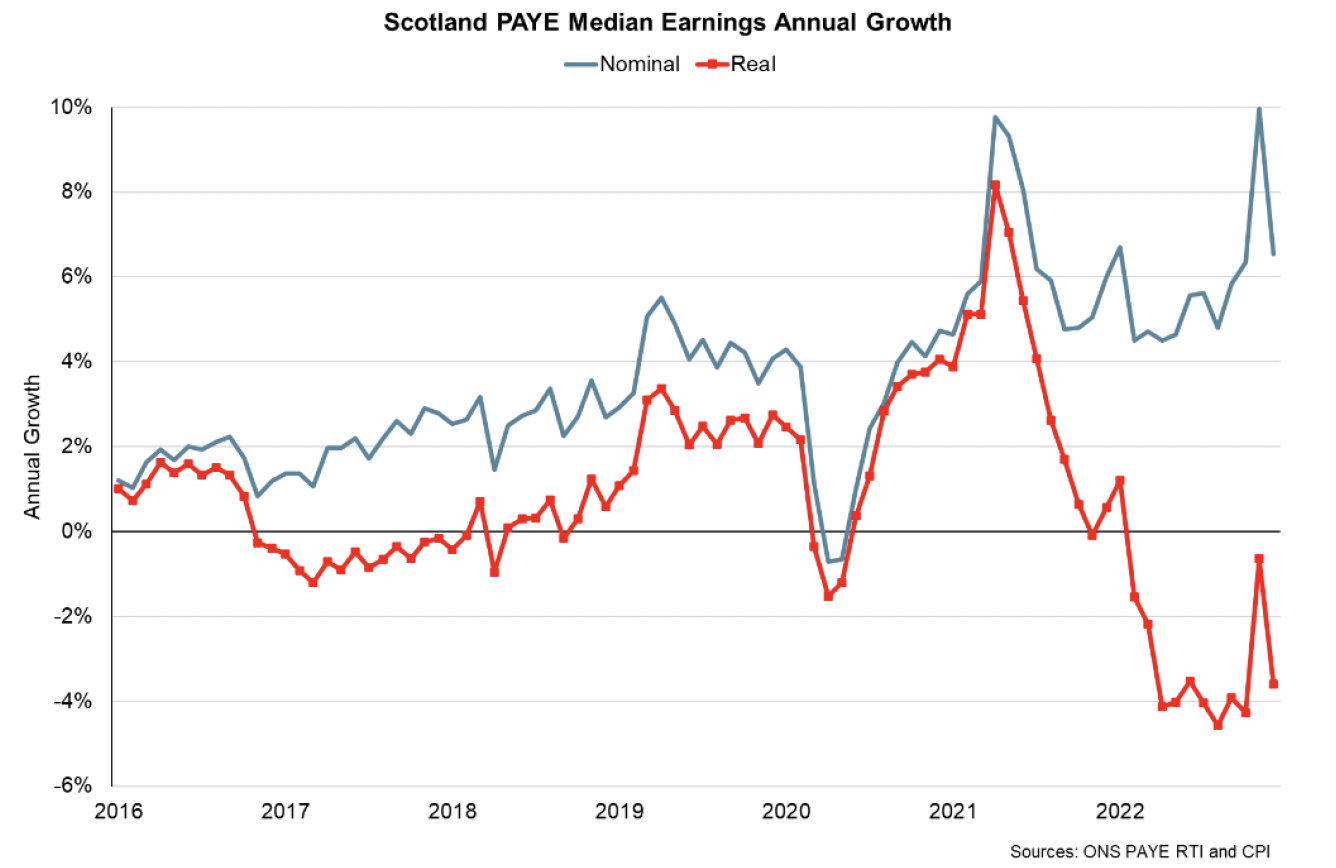

- Nominal median monthly PAYE earnings fell 0.4% in December 2022 to £2,201. The monthly figure can be volatile, and over the past year earnings have grown 6.5%.[13]

- However, adjusting for inflation, which was 10.5% in December, real median earnings fell 3.6% on an annual basis. This is the eleventh consecutive month of negative annual growth, although the gap between nominal earnings and inflation has narrowed slightly as the inflation rate has fallen.

- The sharp fall in real median earnings over the past year emphasises the cost of living challenges that continue to face individuals and households.

Contact

Email: OCEABusiness@gov.scot