Publication - Research and analysis

Monthly economic brief: February 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation

Food prices continue to rise despite overall inflation falling in December.

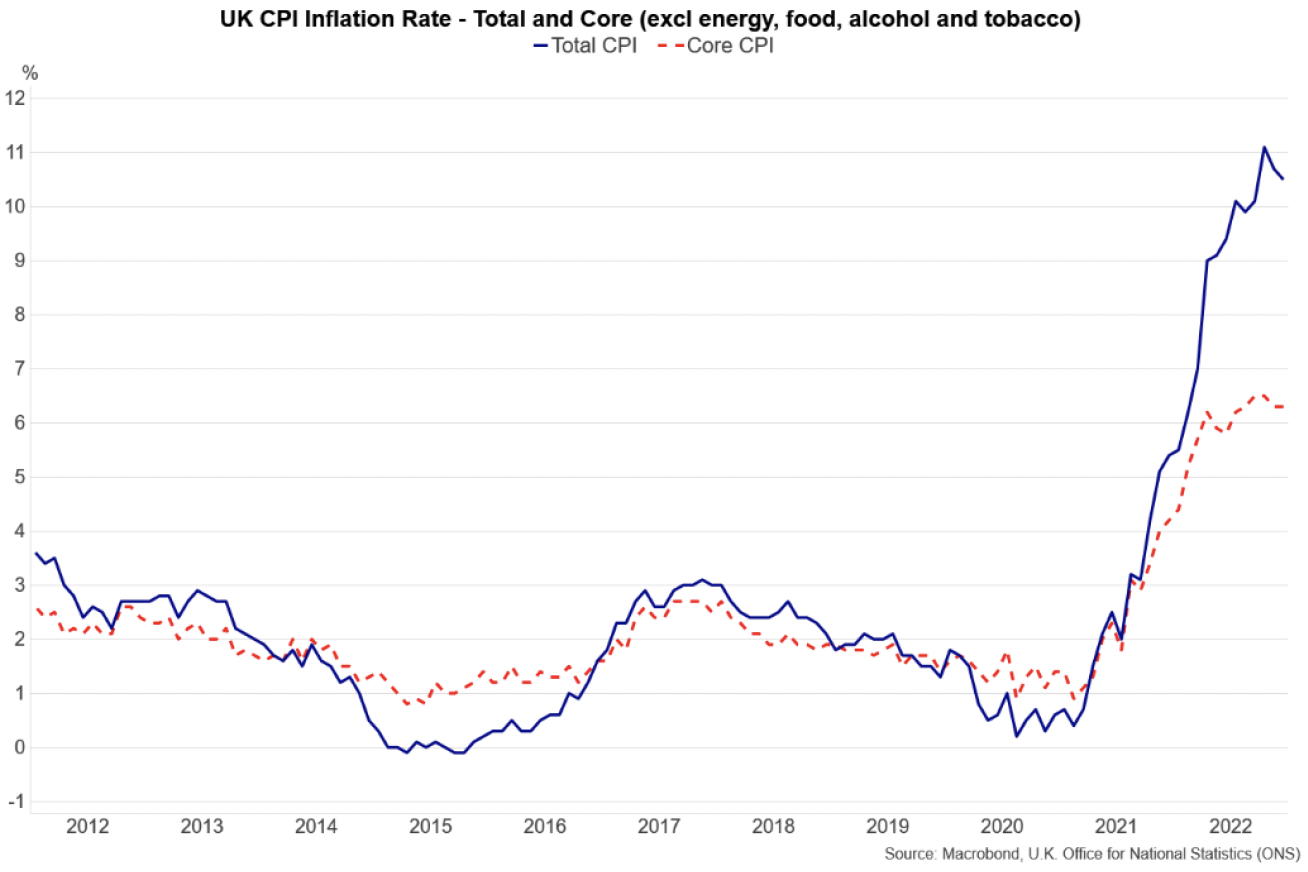

- UK CPI inflation fell to 10.5% in December, down from 10.7% in November, and its recent peak of 11.1% in October.[2]

- The fall over the month was particularly driven by motor fuels, with petrol prices now around 20% lower than their peak in July.[3] Further downward contributions to the rate came from clothing and footwear and recreation and culture, although the annual inflation rate for these categories remained elevated (6.5% and 4.9% respectively).

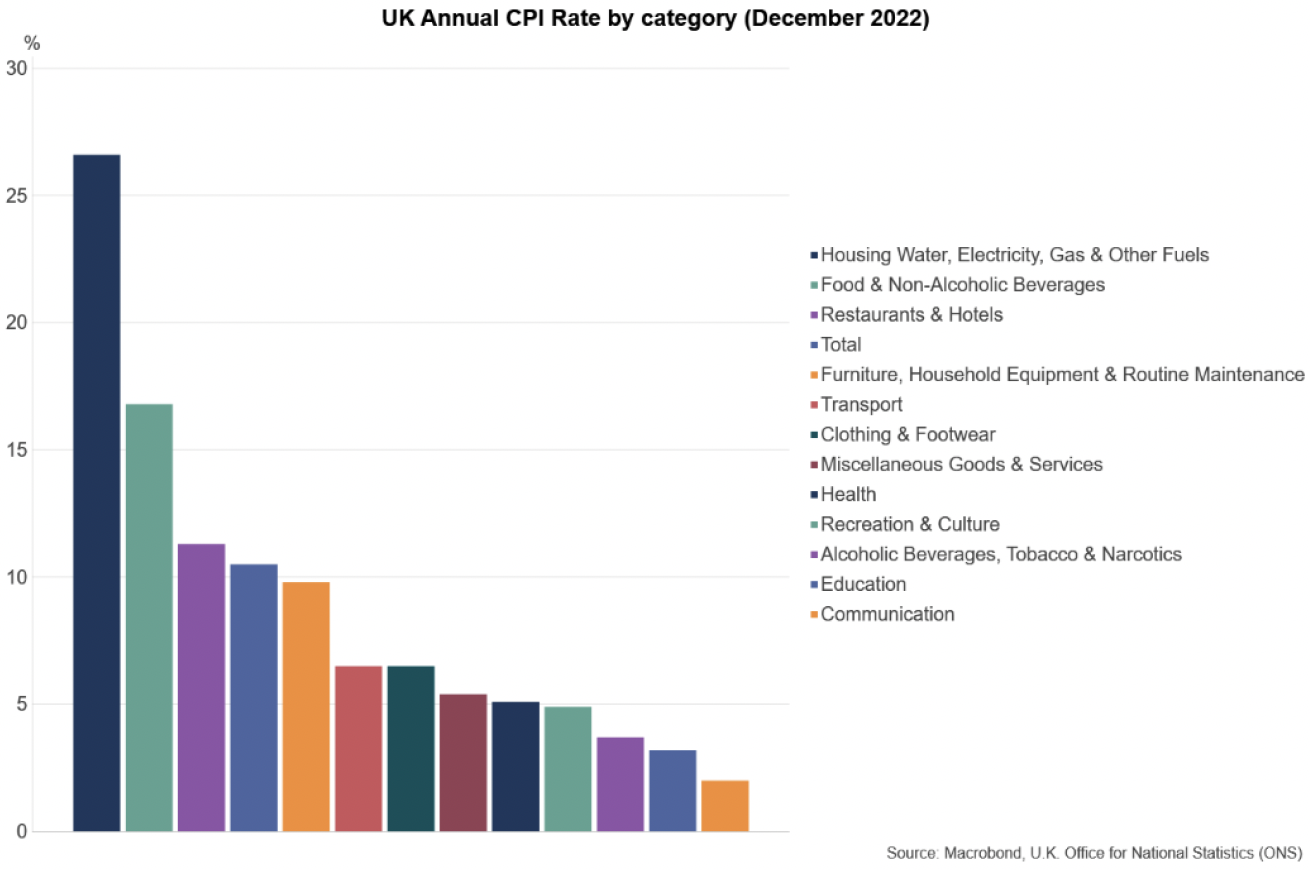

- However, inflation continued to rise across a range of categories, including essentials such as food and non‑alcoholic drinks (16.8%) and restaurants and hotels (11.3%).

- Core inflation, which excludes food, energy, alcohol and tobacco, remained at 6.3% in December, unchanged from November. Core inflation has been around 6% since April 2022, and highlights that energy price rises have been the main driver of changes in inflation over this period. However, core inflation has risen from 1.4% at the start of 2021 and its persistence reflects that inflation has been broad based.

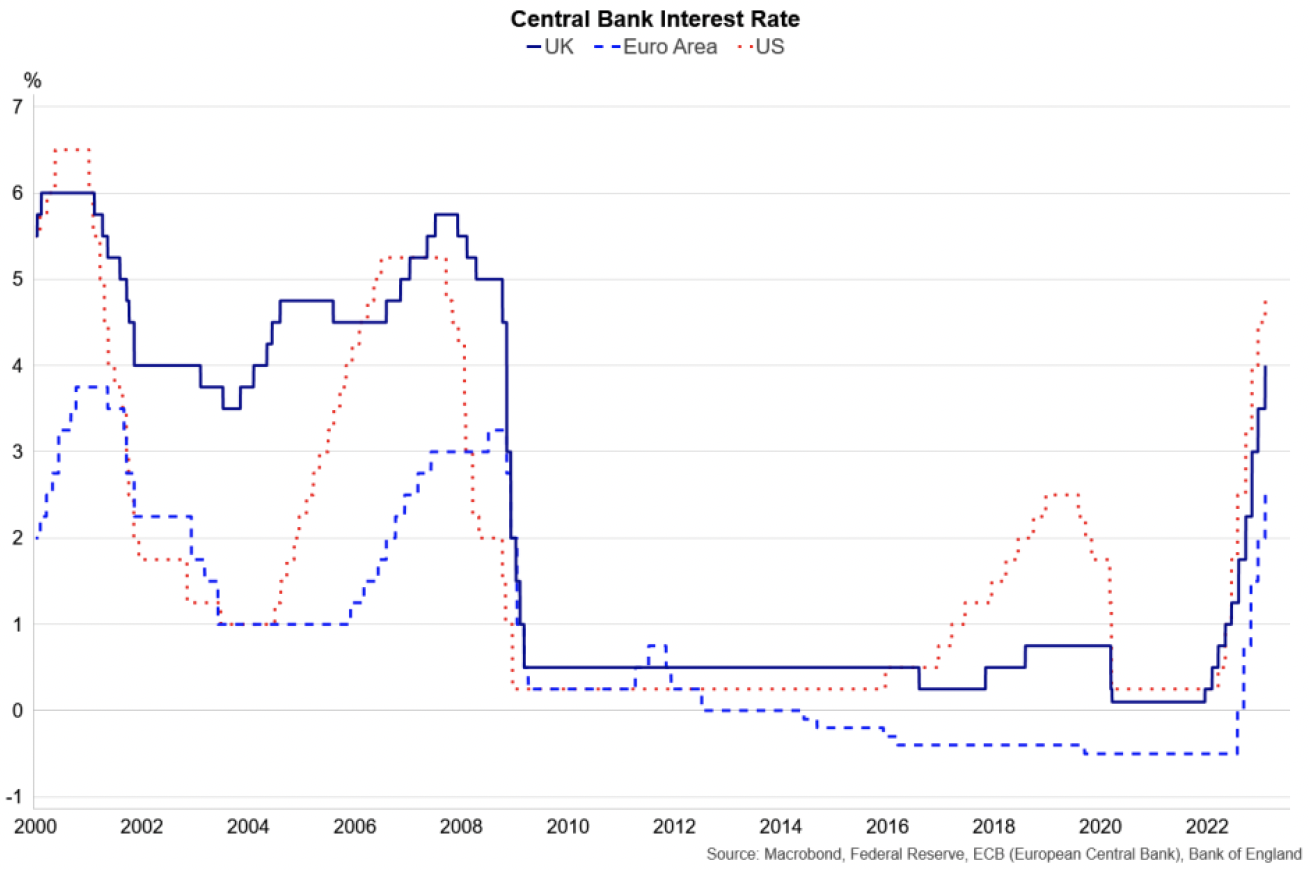

- Due to the further rise in underlying inflationary pressures, the Bank of England's Monetary Policy Committee (MPC) increased the Bank Rate by 0.5 percentage points to 4% in February; its tenth consecutive rate rise since December 2021 and up from 0.1% over this period.[4]

- The increase in interest rates over the past year follows a similar pattern to the US Federal Reserve (currently 4.75%) and the European Central Bank (ECB) (currently 2.5%) as monetary policy has tightened to reduce inflationary pressures. Market expectations are that the Bank of England could raise interest rates further over the coming year to around 4.5%, while the Federal Reserve and ECB have indicated that there is potential for further tightening in the US and Euro Area.

Contact

Email: OCEABusiness@gov.scot