Expansion of funded early learning and childcare to 1140 hours: 2018-2025 national outcomes evaluation

This is the overarching report on the national programme of evaluation from 2018 to 2025 of the expansion of funded early learning and childcare in Scotland to 1140 hours. It presents the main findings across all the strands of research and analysis that together form the outcomes evaluation.

4. Capacity to provide 1140 hours

The programme logic model (Figure 1) underlines that the delivery of the expansion of funded ELC is dependent on having sufficient capacity in place, in terms of buildings, ELC places, and workforce. Having sufficient local capacity in different types of services has implications for accessibility and flexibility of provision, and parental choice. Additionally, a skilled workforce is fundamental to achieving the intermediate outcomes – particularly providing high quality ELC – and subsequently achieving the policy’s high-level outcomes. As discussed in Chapter 2, the childcare sector experienced a challenging period during and after the pandemic and cost-of-living crisis, which coincided with preparation for, and implementation of, the expansion.

4.1 Infrastructure development for the expansion

SFT collected ELC infrastructure data on a quarterly basis from local authorities. The most recently published update reports that the total number of ‘new build, extension, outdoor, or refurbishment’ projects in the capital programme was 893 (Improvement Service, 2024). When all of these are complete, local authorities estimate that they will deliver around 21,000 additional ELC spaces. As of October 2024, 875 of these were complete, delivering 98% of the total planned additional space. Five projects were in construction while the remaining 13 projects were in development.

4.2 Changes in the childcare sector and workforce

This section discusses changes in the childcare sector and workforce between 2016 and the most recent year data are available (2024 or 2025, depending on the source). Full details can be found in the Supporting Tables that accompany this report.

The childcare sector in Scotland operates as a mixed economy model including public, private and third sector providers, and childminders. In Scotland, around half of registered daycare of children services places are provided by the public sector, compared with England where more than half of childcare places are provided by the private sector (Care Inspectorate, 2024; Simon et al., 2022). The majority of providers in the private and third sectors in Scotland are small, often independent businesses. Not all private, third sector, and childminder providers offer funded ELC (see Section 4.2.2). All ‘daycare of children’ and childminding services must be registered with the Care Inspectorate to operate in Scotland. ‘Daycare of children services’ includes nurseries, children and family centres, crèches, school age childcare settings, and playgroups.[5] See Appendix B for definitions.

4.2.1 Changes in the number and capacity of childcare services

The Care Inspectorate ELC statistics show that the overall number of daycare of children services in Scotland steadily decreased from 3,733 to 3,414 between 2016 and 2024. The decrease has largely been in the number of children and family centres (161 to 92) and playgroups (248 to 96). While the evaluation did not gather data on this, Early Years Scotland gathered views from their members on the challenges of running playgroups, which include a lack of volunteers (e.g. as parents are working longer hours), navigating the legal and regulatory framework, and the cost-of-living crisis adding to the financial burden. The number of nurseries increased from 2,468 in 2016 to 2,534 in 2024, with most of the increase between 2019 and 2021 in preparation for the expansion.

Between 2016 and 2024, the number of childminders declined by 46%, from 5,669 to 3,040 childminders. Analysis by the Scottish Childminding Association (SCMA) suggests that the annual percentage decrease in the number of childminders increased between 2016 and 2022. This decrease appears to be slowing between 2022 and 2024. The SCMA analysis also found that, while the number of childminders has declined in all local authorities since 2016, the size of the reduction varies substantially between local authorities (from 20% to 78%). Three local authorities also saw small percentage increases in 2024.

Scottish Government published research on Childminding Workforce Trends (Glencross et al., 2022) that explored the range of factors that may be contributing to the decline in the childminding workforce, in order to identify ways to better recruit and retain them. This highlighted that administration and paperwork was perceived to be a key issue for recruitment and retention of childminders, alongside perceptions of low pay, lack of training, and feeling isolated or undervalued. SCMA (2022) also published an evidence paper on childminding, which highlighted similar issues, as well as concerns about inconsistent local implementation in terms of promoting childminding and financial sustainability.

All childminding services are privately operated, while daycare of children services are operated by a range of private, public sector (mainly local authority), and third sector providers. The percentage of all registered daycare of children services provided by the public sector has increased from 46% in 2016 to 52% in 2024, while the percentage provided by the third sector has decreased steadily from 23% in 2016 to 18% in 2024. The percentage of services provided by the private sector was 30% in 2024 and has remained fairly stable since 2016.

While the number of services has declined, the overall capacity[6] of daycare of children services increased from 165,010 to 179,580 places between 2016 and 2024. There were larger increases between 2018 and 2021 as phasing for the expansion took place, and a decrease between 2022 and 2023. The increase in capacity has been wholly in nurseries, while capacity in other service types decreased. In line with the decrease in the number of childminders, the capacity of childminding services also decreased from 35,180 places in 2016 to 19,000 places in 2024.

The average number of places per service in daycare of children services also gradually increased during this period from 44.2 to 52.6. While for childminders the average number of places per service remained consistent at 6.2, increasing slightly to 6.3 in 2023 and 2024.[7]

4.2.2 Services providing funded ELC

Data from the ELC Census show that the number of services providing funded ELC increased from 2,514 in 2016 to 2,630 in 2021, falling slightly again to 2,558 in 2025. In 2025, 37% of services providing funded ELC were run by the private or third sector and 63% by local authorities. These proportions have been similar since 2016. Of the children registered for funded ELC, the proportion of children registered at private or third sector services has however increased, from 24% in 2016 to 32% in 2025.

Care Inspectorate data show that the proportion of services providing funded ELC places increased for relevant daycare of children service types between 2016 and 2024. In 2024, almost all (98%) nurseries, 91% of children and family centres and 81% of playgroups were providing funded ELC.

4.2.3 Delivery of funded ELC by childminders

In line with the overall trend, the number of childminding services that are approved to deliver and are delivering funded ELC places has decreased: from 1,316 approved to deliver and 851 delivering funded ELC in 2020 to 1,084 approved and 759 delivering funded ELC in 2024. However, the proportion of childminding services delivering funded ELC places has increased over this period from 19% to 25%. Again, SCMA report (2025) substantial variation between local authorities.

As noted in the Interim Report, the decrease in the number of childminding services delivering funded ELC, alongside the substantial decline in the overall number of childminding services is an issue, both in terms of the diversity of the childcare sector and the potential implications for parental choice and accessibility. Scottish Government's Commitment to Childminding Report (2021) sets out some of the reasons childminding services are an important and unique element of the childcare sector. Research on perceptions of the impact of childminding services (2021) highlighted benefits of childminding provision for children, parents, and families.

4.3 The ELC workforce

This section presents analysis of the daycare of children workforce, looking at whether there have been any changes in the composition of the workforce over the period of the expansion. It focuses on the ‘ELC workforce’ that specifically delivers publicly funded ELC where possible. However, it does not include childminders – discussed instead in Section 4.2 above – or GTCS registered teachers working in ELC – see Section 5.1 for discussion of ELC staff qualifications, including teachers and other early years graduates working to deliver funded ELC.

4.3.1 Change in the size and distribution of the ELC workforce

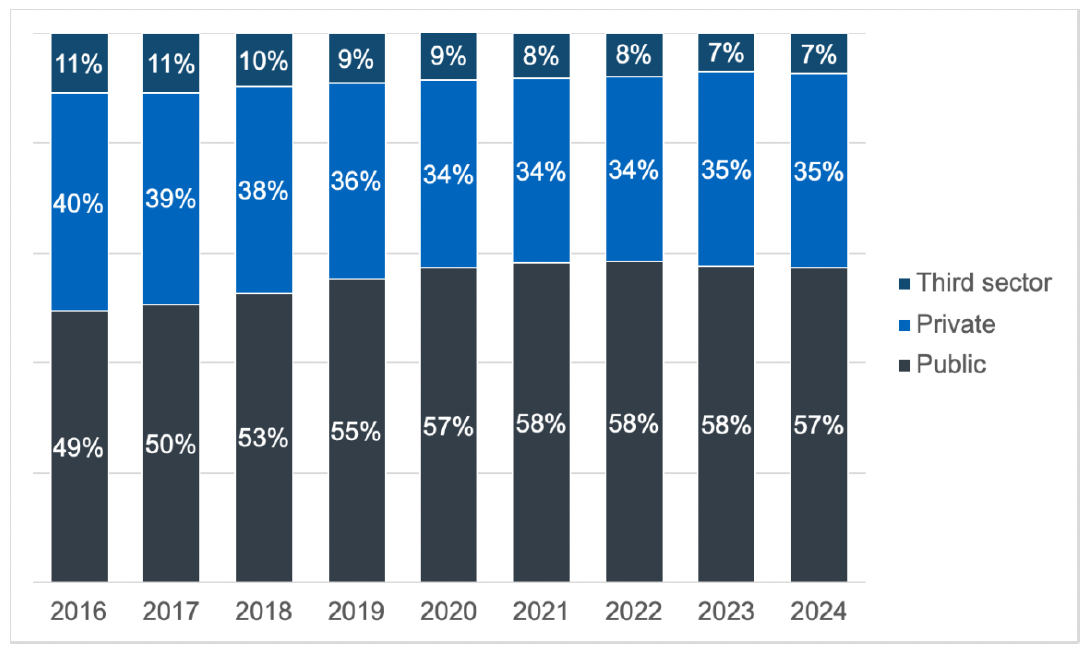

Overall, the ELC workforce has increased substantially to meet the demands of the ELC expansion. When looking at the funded ELC workforce this has grown from 25,580 in 2016 to 36,200 in 2024, a 42% increase – with most of the increase taking place between 2018 and 2021 prior to the expansion.

Figure 2 shows that, over this period, the public sector share of the ELC workforce has increased, from 49% in 2016 to 57% in 2024 (with numbers increasing from 12,590 to 20,730), while the private and third sector shares decreased. Although staff numbers in the private sector increased when comparing 2016 and 2024 figures (from 10,170 to 12,800), the third sector experienced a decline, both in proportion and absolute staff numbers (from 2,810 to 2,670 over this period).

Source: SSSC Children’s services workforce data

SSSC's (2024) analysis of the distribution of the workforce (headcount) shows similar patterns for the wider daycare of children workforce (the part of the SSSC register under which members of the ELC profession are recorded, including those who do not deliver funded ELC). The overall daycare of children workforce grew by 26% between 2016 and 2022, rising from 33,430 to 42,190, then a smaller increase to 42,250 in 2024. The public sector's share of the daycare of children workforce steadily increased from 40% in 2016 to 51% in 2024. In contrast, between 2016 and 2024 there was a decline in the proportion of the daycare of children workforce based in the private sector (from 41% to 36%) and third sector (from 19% to 13%).

Given the changes in the ELC workforce described above, it is worth noting that, during the lead up to the ELC expansion the number of opportunities arising from new posts has been greatest in the public sector. In general, private and third sector settings were already able to offer full day childcare prior to the ELC expansion. Those working in partnership with local authorities were, therefore, able to switch some of their existing capacity over to funded ELC. Many public sector settings were only set up to deliver limited hours, usually around school opening times. They, therefore, required additional staff capacity to deliver enhanced provision.

4.3.2 Movement in the daycare of children workforce

Retention and turnover of ELC staff are affected by issues such as low pay, terms and conditions, and workforce status and satisfaction (Early Education, 2025). Staff retention and turnover can, in turn, affect staff wellbeing and have implications for the level of staff experience and the stability within settings, which can impact on both sustainability of services and quality of provision.

Looking at movement of daycare of children registrants within the sector, SSSC (2023) analysis for the 2021-22 financial year[8] found that the public sector had the lowest turnover of staff and the highest retention rates at almost 90%. Of those staff who did move from a public sector role to another service, over 90% moved to another public sector service. Retention was lowest in the private sector during 2021-22, with around 75% of staff remaining in the same post one year on. The third sector retained just over 81% of staff in the same service during 2021-22. Of those moving from the private sector, the majority (59%) moved to another private sector service. Of those who moved to a different sector, over 34% moved to a post in the public sector while 7% moved to the third sector.

SSSC’s (2023) report noted that the issue, during 2021-22, therefore appeared to be less about a disproportionate flow of staff from the private and third sectors to the public sector, than the near absence of a flow from the public sector to the private or third sectors. Further analysis suggested that private and third sector employers were more dependent on new entrants to the sector to fill posts that were vacant. If this pattern is found to continue, this may have implications for experience and training of staff in the private and third sector. The SSSC’s forthcoming update to their analysis on the movement of staff across the sector will provide a more detailed understanding of patterns of change in the workforce in recent years.

The latest SSSC workforce report shows an increase in the stability index for daycare of children staff. This is an indicative measure of the proportion of staff who have stayed in the same post as they were in the previous year. For 2024 the stability index was 80%, compared with 75% in 2023 and 76% in 2022. This is the highest figure since the measure was introduced in 2016. This increased stability in the workforce is a positive indicator given the period of significant change seen throughout the 1140 expansion.

4.3.3 Terms and conditions for those delivering funded ELC

The National Standard for funded ELC requires that private and third sector providers who agree to deliver the funded entitlement will commit to paying the real Living Wage to all ELC workers delivering the funded entitlement and to operating Fair Work Practices. As set out previously, over half of the total daycare of children workforce are employed by local authorities, all of whom are paid at least the real Living Wage.

Analysis in the Financial Review of the ELC Sector (Scottish Government, 2016) estimated that in 2016, prior to the ELC expansion, around 80% of practitioners and 50% of managers in private and third sector settings delivering funded ELC were paid an hourly rate below the real Living Wage.

In the Financial Sustainability Health Check (Scottish Government, 2023a) provider surveys, 81% of private and third sector ELC providers reported that they paid the real Living Wage to either all staff (56%) or to staff delivering funded ELC (25%). However, 72% of childminders said that they did not pay themselves the real Living Wage. Just under three quarters (73%) of services delivering funded ELC indicated that they planned to pay all staff in their setting the real Living Wage by August 2023. It should be noted, however, that the response rate to the surveys was low.

While it is not possible to make direct comparisons over time, these figures suggest that the ELC real Living Wage commitment has led to increases in pay across private and third sector services. Scottish Government has worked with local authorities to implement a process for monitoring progress with providers paying the real Living Wage. This involves collecting data in the Care Inspectorate’s Annual Returns and the SSSC’s Have Your Say survey.

4.4 Financial sustainability

4.4.1 Payment of sustainable rates to private and third sector providers

Local authorities are responsible for setting sustainable funding rates for providers in the private, third, and childminding sectors who deliver funded ELC.[9] Joint Scottish Government and COSLA Guidance published in 2019 sets out key principles for setting sustainable rates, including that rates should: support delivery of a high quality ELC experience; reflect the costs of delivery; allow for investment in the setting; and be set at a level to enable payment of the real Living Wage to childcare workers delivering funded ELC. The guidance also states that every child attending a funded ELC session will be provided with a free meal.

The Scottish Government (2023a; 2024b; 2025e) has published data on the sustainable rates set by local authorities over the expansion period showing:

- The average rate paid by local authorities to private and third sector providers for the delivery of funded ELC to three- to five-year-olds increased by around 78%, from £3.68 per hour in 2017-18 to £6.55 per hour in 2024-25. Between 2017-18 and 2022-23, the average rate paid increased 57% to £5.80 per hour.

- The gap narrowed between the highest and lowest sustainable rate paid by local authorities for the delivery of funded hours to three- to five-year-olds, from 41% (£1.32) in 2017-18 to 22% (£1.17) in 2022-23, increasing slightly again to 25% (£1.48) in 2024-25. In 2024-25, the lowest rate paid was £6.00 per hour and the highest rate was £7.48 per hour.

- There is greater variation in the rates paid by local authorities for the delivery of funded hours to two-year-olds, from £6.15 per hour to £9.08 per hour in 2024-25 (a gap of 48%). The average rate across local authorities for eligible two-year-olds was £7.25 per hour in 2024-25.

While rates have increased over the expansion period, in light of sustainability concerns raised through the 2023 Financial Sustainability Health Check, the Scottish Government and COSLA (2023a) undertook a Sustainable Rates Review in 2023. The Review noted that, while variation is to be expected due to differences in local circumstances and costs, there was not sufficiently robust evidence on varying costs of delivery across each local authority area to indicate what level of variation should be expected. Affordability was cited as a primary concern by a large majority of local authorities in relation to setting rates. A number of councils cited long-standing pressures on local authority core funding, reductions in the ELC ring-fenced grant, and a lack of clarity on future ELC budget allocations as key factors.

The Review set out a programme of reform to strengthen the process for setting sustainable rates. A new national survey of funded ELC providers’ costs was undertaken independently in 2025 and evidence from this will inform rate-setting guidance from 2026-27 onwards.

Overall, this suggests that, nationally, the policy has resulted in significant increases to the rates paid to funded providers in the private, third, and childminding sector and improvements to pay amongst workers delivering funded ELC. Substantial challenges remain, however, and the programme of work underway following the Rates Review is considered by the sector to be vital to improving the long term sustainability of funded ELC provision.

4.4.2 Views of ELC setting managers on financial sustainability

The 2023 Financial Sustainability Health Check update highlighted that the childcare sector, like many other parts of Scotland's economy, was facing challenges due to the ongoing costs-of-living crisis, workforce pressures and the lasting impacts of the pandemic. Some types of services had been disproportionately impacted due to their business models and changes in demand. In addition, it emphasised that financial and workforce issues within the sector are closely linked.

Provider surveys were undertaken as part of the Health Check during 2023. It should be noted that the response rate to the surveys was low. These found that providers' confidence in their financial sustainability declined across all types of childcare services since the previous Health Check in 2021. The largest declines in the assessment of sustainability were for funded ELC services and for private services. Key concerns highlighted by survey respondents were around increased delivery costs, increases in income not keeping pace with rising costs, and reduced demand for some services.

During the post-expansion phases of the SSELC, an online questionnaire for heads or managers of participating ELC settings was used to capture their views on what impacts the expansion of funded ELC had on their setting.[10] Many private and third sector providers mentioned finances as being an issue: over half (53%) said the rates paid by local authorities were one of the main challenges, and almost two fifths (38%) cited the challenge of meeting additional costs.

4.5 Adaptation of ELC settings for the expansion

4.5.1 Views of ELC setting managers

During the post-expansion phases of the SSELC, setting managers were shown a list of potential challenges in meeting the requirements of the expansion and asked to pick up to three that they considered affected their setting (Hinchliffe et al., 2025). Only 7% of setting managers said that they did not face any challenges. Over three-fifths (62%) said “recruiting good quality staff” and 39% said “retaining good quality staff” were challenges. Almost half (48%) said staff training and a similar proportion (47%) said accommodating children with ASN. Concerns about staffing were also raised in the Financial Sustainability Health Check update. In particular, loss of staff from private and third sector services (including some who have left the sector altogether) and challenges in recruiting suitably experienced staff.

Setting managers were also presented with a list of activities and asked to choose which, if any, they had done to “meet the requirements of the ELC expansion”. Almost three-quarters (73%) said they had taken on extra staff, 48% said they provided additional training to staff, and 35% lengthened opening hours. Three in ten (30%) said they started providing food – as set out above, as part of the expansion programme every child attending a funded ELC session can receive a free meal.

More than half of private and third sector providers (53%) reported that they had increased fees for unfunded children (for example younger children) as a result of the expansion. As noted above, these providers highlight a range of financial pressures, including rising costs.[11] Around half (51%) of local authority settings had lengthened opening hours (11% of private and third sector providers said this) and two-fifths (41%) started providing food (15% of private and third sector providers said this). This is as expected, given that, in general, private and third sector providers tended to have longer opening hours and were more likely to provide food prior to the expansion.

The West Partnership – eight local authorities within the Glasgow City region – did an evaluation of 1140 hours during 2022 and 2023 (West Partnership, 2024). This found differences in experiences between respondents in term time and mixed model settings. For example, 52% of term time ELC practitioners agreed that the overall impact of 1140 hours for their setting had been positive, while only 16% of those in mixed model settings agreed (overall 27% agreed). In interviews and focus groups, many practitioners discussed the negative impact of the expansion on their own wellbeing, and how this has led to increases in staff absences and staff leaving the sector.

4.6 Summary: capacity to provide 1140 hours

Both the overall capacity of daycare of children services and the size of the ELC workforce have increased to meet the demands of the ELC expansion. This increase has been primarily in nurseries, with the number and capacity of childminders, children and family centres, and playgroups falling. The data considered suggest that, nationally, the policy has resulted in significant increases to the rates paid to funded providers in the private and third sector and improvements to pay amongst workers delivering funded ELC. However, delivery of the ELC expansion – along with other pressures – has led to variable and challenging impacts for parts of the sector which are still evolving. Staffing was highlighted as the main challenge for all setting types, but particularly for those in the private and third sector. These sectors also raised concerns about their financial sustainability. Local authorities have also highlighted financial challenges in terms of ELC delivery.

Contact

Email: socialresearch@gov.scot