Coronavirus (COVID-19) business support measures: evaluation

This evaluation assesses the outputs and indicative outcomes of the COVID-19 business support measures available in Scotland up to summer 2021.

4. Evaluation Results

This chapter presents the results from the second stage of the evaluation of business support schemes available to businesses in Scotland, drawing on scheme management information data, ONS' Business Insights and Conditions Survey (BICS) data, qualitative evidence from business representative organisations and OCEA's Strategic Framework Sectoral Viability Model. It:

- provides an overview of the uptake of the support schemes;

- considers the impact of the support provided on businesses' viability and survival, and impacts on employment in the short-run;

- considers the 'additionality' of the support provided by the Scottish Government, over and above the impact of the UK Government support; and

- considers how well the schemes are perceived to have been delivered.

4.1 Uptake of Business Support Schemes

Summary

- Data from the Office for National Statistics' (ONS) Business Insights and Conditions Survey (BICS) shows that 32% of businesses in Scotland received SG grant support, 80% received support from the Coronavirus Job Retention Scheme (CJRS) at its peak and 34% received support from UK Government-backed accredited loans or finance agreements.

- There was a steady increase in the share receiving UK Government-backed loan support over the period June-July 2020 to June-July 2021.

- 43% of businesses still had staff on furlough leave in June-July 2021, highlighting the reliance many businesses had on CJRS even as restrictions eased in Scotland.

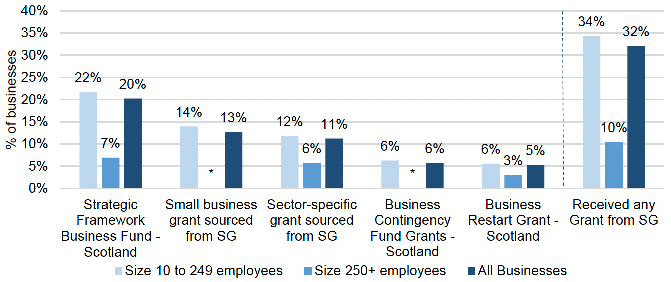

- Of the Scottish Government (SG) grant schemes, the Strategic Framework Business Fund had the greatest reach with 20% of businesses in scotland receiving support. 13% received Small Business Grants, 6% received the Business Contingency Fund, and 5% received financial support from the Business Restart Grant. 1 in 10 (11%) businesses received sector-specific grants from the SG.

- The Accommodation & Food Services sector had the highest proportion of firms receiving support from SG grants (78%), reflecting the targeting of much of the SG support schemes at those sectors most impacted.

- A higher proportion of SMEs (34%) received SG grant support than large businesses (10%), reflecting the targeting of SG grant support at smaller businesses.

- The BICS findings are reflected in the scheme management information which indicates that the CJRS had the greatest reach of all the schemes, with 906,400 jobs in Scotland furloughed under the scheme since its inception, accounting for more than a third of all employee jobs in Scotland.

- Of the SG schemes, the management information data shows, in line with the BICS findings, that the core grant schemes had the greatest reach, with 91,258 grants approved for the (now closed) Business Support Fund Grants, reflecting the relative scale of funding available under the scheme (£1 billion out of the £3.7 billion Scottish Government total). As at June 2021, 47,658 grants had been awarded through the Strategic Framework Business Fund totalling £344.8 million.

This section provides an overview of the uptake of the support schemes available to businesses in Scotland based on the latest available BICS[10] and scheme management information data. For the most part, the latest available BICS data relates to wave 31 (17th to 30th May 2021) however data from other waves is used where the relevant data is not available in wave 31.[11] Data from earlier waves is also referenced for comparison. The BICS data provides a high level overview of the proportion of businesses in Scotland applying for and receiving Scottish and UK Government support. The management information data provides a more granular scheme-by scheme picture and reflects the actual numbers of businesses that received support. Further detail on the management information data for each scheme is provided in Annex 1.

Businesses applying for support[12]

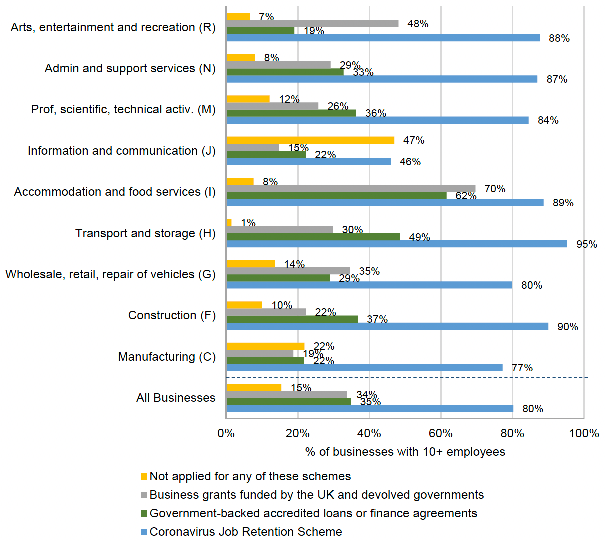

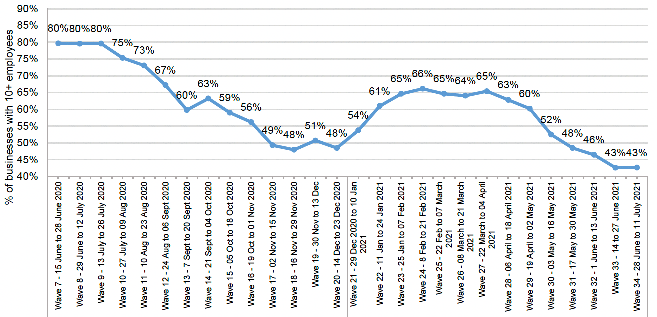

Data from BICS wave 16 (covering the period 19 October to 1 November 2020) shows that, of the three major forms of business support (Coronavirus Job Retention Scheme, Government-backed accredited loans or finance agreements, and business grants funded by the UK and devolved governments),[13] the highest proportion of businesses in Scotland (80%) applied for the CJRS (Chart 16).

A similar proportion of businesses in Scotland applied for other grant support (excluding the CJRS) funded by the UK and Scottish Governments (34%) as Government-backed loan support (35%). This is in contrast to wave 8 of the survey (29 June to 12 July 2020) where more businesses applied for grant support (38%) than loan support (26%). This perhaps indicates that there has been an increase in businesses willing to utilise external finance through the loan schemes as restrictions returned later in 2020. However, it should be noted that the data is cumulative and may have captured more businesses that received support in the first lockdown. 15% had not applied for any of the support schemes.[14]

Reflecting the targeting of much of the grant support schemes (at least, those funded by the Scottish Government) at sectors most impacted by COVID-19, the sectors with the highest proportion of businesses applying for grant support were Accommodation & Food Services (70%) and Arts, Entertainment & Recreation (48%). The Accommodation & Food Services sector also had the highest proportion of businesses applying for Government-backed loan support (62%), followed the Transport & Storage sector (49%). The Transport & Storage (95%) and Construction (90%) sectors, on the other hand, had the greatest share of businesses applying for CJRS.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 16

Notes: Data for Mining and Quarrying (B); Water Supply, Sewerage, Waste (E); Real Estate Activities (L); Education (P); Health & Social Work (Q) and Other Service Activities is not available.

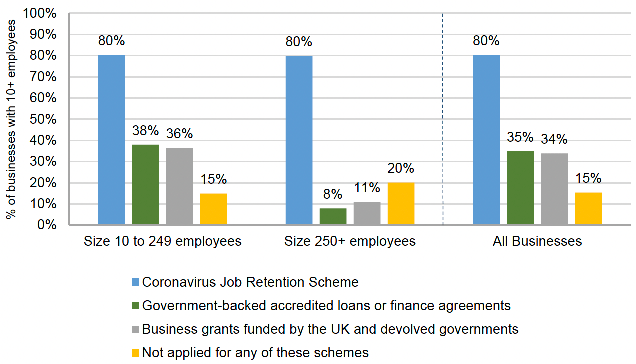

The CJRS had the same proportion of small and medium-sized enterprises (SMEs) applying as large businesses (80%) (Chart 17). However, a higher proportion of SMEs (36%) applied for grant support than large businesses (11%), reflecting the targeting of grant support at smaller businesses. This was also the case for the government-backed loan schemes where 38% of SMEs applied compared to 8% of larger businesses. An increased proportion of small businesses had applied for loan schemes in BICS wave 16 (19 Oct to 1 Nov 2020) compared to wave 8 (29 June to 12 July 2020) where 27% had applied at the time. This perhaps indicates that more businesses were willing to take on debt to weather the impact of the pandemic as businesses reported to be hesitant in the initial evaluation report in summer 2020.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 16

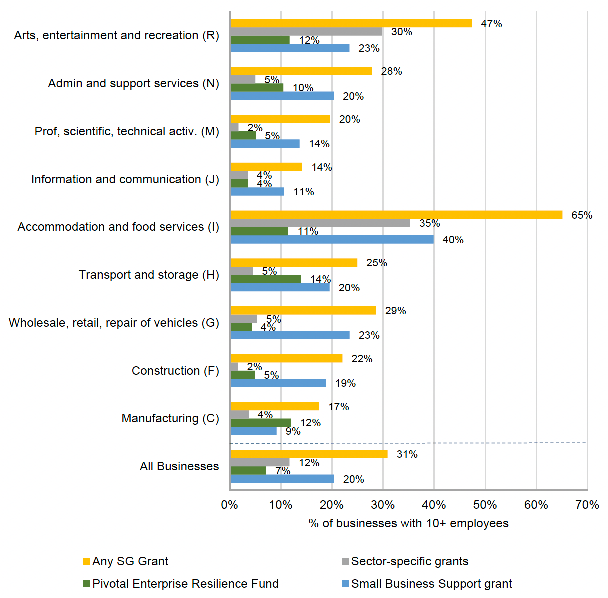

Looking specifically at Scottish Government (SG) grants, data from BICS wave 16 shows that 31% of businesses in Scotland had applied for an SG grant over the period 19 October to 1 November 2020 (Chart 18). Of the three categories of grants asked in wave 16, the Business Support Fund Grants (which comprise the Small Business Grant Scheme and the Retail, Hospitality and Leisure Business Grant Scheme) had the highest proportion of businesses in Scotland applying (20%). 7% applied for the Pivotal Enterprise Resilience Fund (PERF) delivered by Scottish Enterprise (SE). 12% applied for sector-specific grants compared to 8% in BICS wave 8.

By sector,[15] the Accommodation & Food Services sector (65%) had the highest proportion of businesses applying for SG grant support, followed by the Arts, Entertainment & Recreation (47%) and Wholesale, Retail, Repair of Vehicles (29%) sectors, again reflecting the targeting of much of the SG grant schemes at those sectors most impacted. The business viability analysis will show later these are among the sectors most impacted by the pandemic.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 16

Notes: Reliable data for Mining and Quarrying (B); Water Supply, Sewerage, Waste (E); Real Estate Activities (L); Education (P); Health & Social Work (Q) and Other Service Activities is not available.

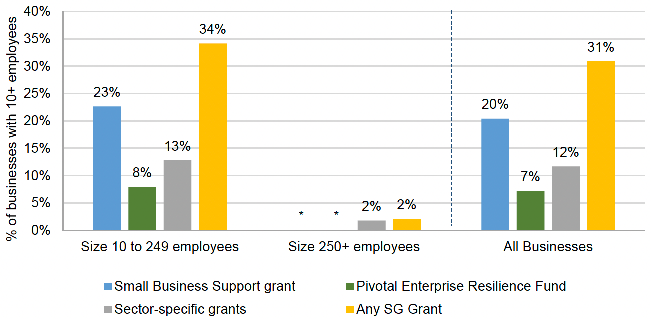

By business sizeband, a higher proportion of SMEs (34%) applied for SG grant support than large businesses (2%), again reflecting the targeting of the SG grant support at smaller businesses (Chart 19), but also the dominance of SMEs in the Scottish business base. This was the case across the three categories of schemes.[16]

Chart 19: Scottish Government Grant Schemes applied for by Businesses in Scotland, by business size band

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 16

Notes: Data for large businesses for the Small Business Support Grant and Pivotal Enterprise Resilience Fund is not available.

Businesses receiving support

Data for the period to 28 June to 11 July 2021 (wave 34) shows that 32% of businesses in Scotland (that had not permanently stopped trading at the time of the survey) had received grant support funded by the SG (an increase from 29% in wave 16), 80% had received support from the CJRS at its peak and 34% had received support from Government-backed accredited loans or finance agreements (an increase from 21% in Wave 8 and 31% in wave 16).

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 34

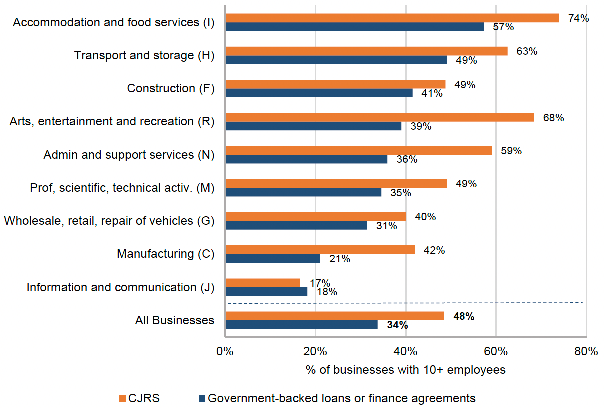

Looking at the CJRS, the sectors with the highest proportion of businesses receiving support from the scheme were Arts, Entertainment & Recreation (62%), Accommodation & Food Services (61%), Admin & Support Services (60%), and Transport & Storage (59%). A slightly higher proportion of SMEs (43%) received support from the CJRS in Wave 34 than large businesses (39%), however it has been broadly similar across nearly all waves of BICS. The significant proportion of businesses still utilising CJRS (43%) highlights the reliance many businesses still have on the scheme despite the gradual opening of the economy in May 2021.

In terms of Government-backed loan support, the sectors with the highest proportion of businesses receiving loan support over the period 17 to 30 May 2021 (BICS wave 31) were Accommodation & Food Services (57%), Transport & Storage (49%), Construction (41%), Arts, Entertainment & Recreation (39%), Admin & Support Services (36%) and Professional, Scientific & Technical Activities (35%) (Chart 21). A higher proportion of SMEs (36%) received loan support than large businesses (10%). This may reflect the more favourable terms for the Coronavirus Business Bounce Back loans, which targeted SMEs.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

Notes: Data for Mining & Quarrying (B), Water Supply & Sewerage & Waste (E), Real Estate Activities (L), Education (P), Health & Social Work (Q) and Other Service Activities (S) is not available.

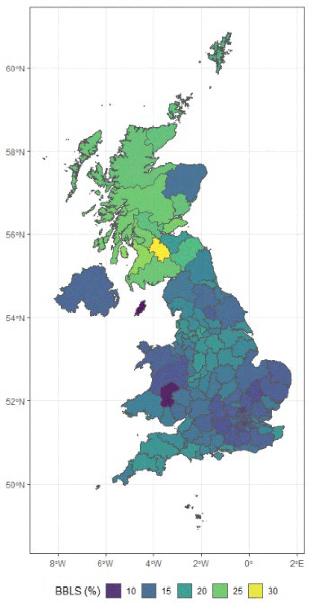

Chart 22 shows that a greater share of businesses in Scotland received government-backed loan support from the UK Government through the bounce back loan scheme (BBLS) compared to the rest of the UK.

Source: Bank of England

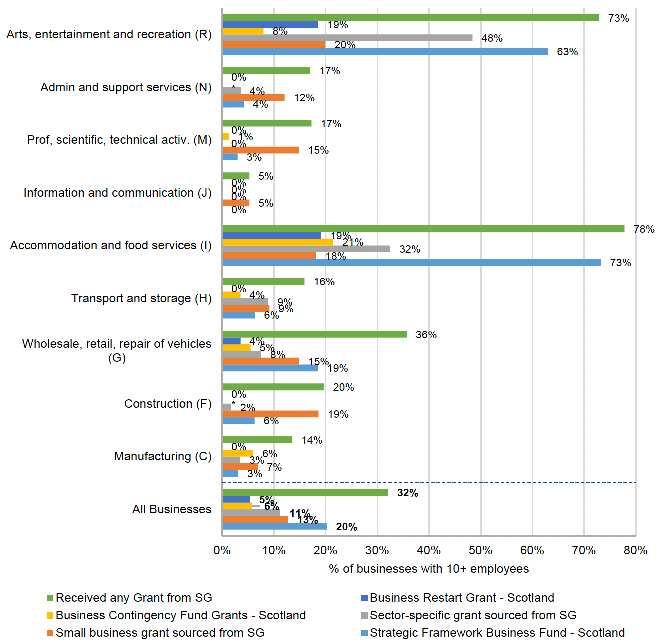

Looking at SG grant support, the Strategic Framework Business Fund had the greatest reach with 20% of businesses in Scotland receiving support (Chart 23) over the period 17 to 30 May 2021. 13% of businesses in Scotland received Small Business grants, 6% received the Business Contingency Fund, and 5% from the Business Restart Grant. The Accommodation & Food Services sector saw the highest proportion of firms receiving SG grants (78%). This was followed by the Arts, Entertainment & Recreation (73%) and Wholesale, Retail & Repair of Vehicles (36%) sectors.

1 in 10 (11%) businesses received sector-specific grants from the Scottish Government. The Arts, Entertainment & recreation (48%) and Accommodation & Food Services (32%) sectors saw the highest proportion of firms receiving sector specific grants.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

Notes: Reliable data for Mining & Quarrying (B), Water Supply & Sewerage & Waste (E), Real Estate Activities (L), Education (P), Health & Social Work (Q) and Other Service Activities (S) is not available.

By business sizeband, as expected given the targeting of much of the SG grant support at smaller businesses, a higher proportion of SMEs (34%) received SG grant support than large businesses (10%) (Chart 24). More large businesses had received SG grant support compared to the last comparable wave of BICS (wave 16 – 19 Oct to 1 Nov 2020) where only 2% had received support.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

Notes: Data for large businesses for the Pivotal Enterprise Resilience Fund is not available

Small Business Survey (SBS) 2020

According to the Small Business Survey results for the period Spetember 2020 to April 2021, more than a third (36%) of SMEs with employees in Scotland had increased borrowing since the outbreak of COVID-19 to mitigate the impacts of the pandemic. This was in line with the UK as a whole. 27% reported using government or local authority grants or schemes directly related to COVID-19 at the time of the survey, which was broadly consistent across all the UK regions.

Table 3 below shows the share of SME employers in Scotland that applied to and then received funds from mentioned UKG COVID-19 support schemes. 67% of SME employers in this category had applied for the CJRS, the majority (91%) of which received funding. 15% had applied for the SEISS, but only 17% of those were successful. SME employers were asked roughly what proportion of their workforce was on furlough at its highest level. Half (51%) reported that all of their workforce were furloughed at one point in time.

| Share of businesses applied | Share of businesses applied that received funding | |

|---|---|---|

| Coronavirus Job Retention Scheme (CJRS) | 67% | 91% |

| Self-employment Income Support Scheme (SEISS) | 15% | 17% |

| None of these | 29% | 2% |

Base: All SME employers

38% of SME employers in Scotland used COVID-19 government-backed accredited loans or finance agreements such as CBILS and BBLS, broadly in line with the UK as a whole at 37%. Only 9% of Scottish SME employers used the business rates holiday initiative compared to 17% across the UK. A quarter (26%) deferred VAT payments and 8% took advantage of HMRC's Time to Pay scheme, broadly in line the UK. 42% of SME employers had used a COVID-19 business grant funded by government or local authorities, in line with the UK.

A quarter (25%) of SME employers with a separate business premise received COVID-19 Non-Domestic Rates Relief, in line with the UK as a whole. Of those that received relief, the majority (54%) did not know what share of relief they received. 23% received 91-100% rates relief while 14% received 0-10%.

Management Information

For most schemes, the management information data shows the value of the support provided in Scotland, and the number of applications and approvals. For some schemes, data on applications and approvals is also available by location, sector and equalites characteristics. Table 4 overleaf provides a high level summary of the key metrics for each scheme in scope of this evaluation, with further detail provided in the paragraphs that folllow it. Full management information data for each scheme is provided in Annex 1.

While it is not possible to make direct comparisons of relative support between schemes that targeted jobs directly (e.g. the CJRS) and those targeted at businesses (as is the case with most Scottish Government support), the management information indicates that the CJRS has had the greatest reach of all the schemes. The CJRS has supported 906,400 jobs in Scotland, accounting for more than a third of all employee jobs in Scotland. The SEISS also supported over half a million (553,000) self-employed individuals. Of the Scottish Government support schemes, the Business Support Fund Grants had the greatest reach, with 91,258 grants approved, reflecting the relative scale of funding available under the scheme (£1 billion out of the £3.7 billion Scottish Government total). These findings are consistent with the BICS results above.

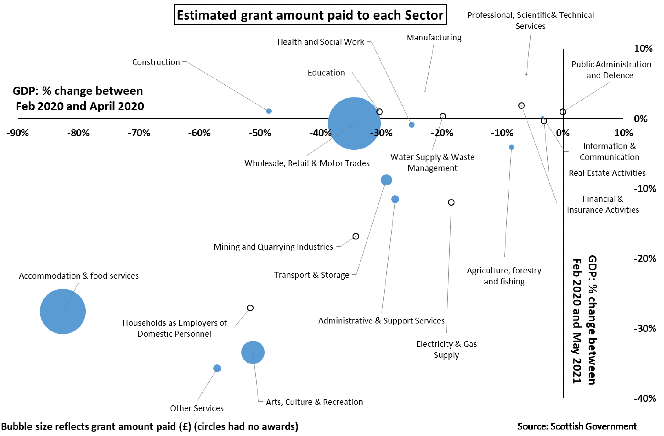

Chart 25 shows the estimated amount of Scottish Government funding allocated to businesses in Scotland by sector alongside the impact on economic output in terms of GDP over the period of the pandemic in Scotland. Those sectors that received the greatest share of SG funding (Wholesale, Retail & Motor Trade, Accommodation & Food Services and Arts, Culture & Recreation) also experienced the greatest restrictions on trade and resulting decline in GDP in February to April 2020. Some sectors have recovered to pre-pandemic levels as at May 2021 in terms of GDP, such as Wholesale, Retail & Motor Trade, however the COVID-19 support was mostly aimed at the non-essential retail sub-sector.

Source: Scottish Government

Notes: Schemes have been manually mapped to sectors deemed most appropriate – experimental.

| Scheme | Number supported in Scotland | Amount spent in Scotland (£ million) |

|---|---|---|

| UK Government | ||

| Coronavirus Job Retention Scheme | 906,400 jobs | - |

| Self-employment Income Support Scheme | 553,000 self-employed individuals | £1,500.0 |

| Bounce Back Loan Scheme | 86,062 businesses | £2,496.4 |

| Coronavirus Business Interruption Loan Scheme | 4,144 businesses | £982.5 |

| Coronavirus Large Business Interruption Loan Scheme | - | - |

| Future Fund | 22 businesses | £8.6 |

| COVID Corporate Financing Facility | 2 businesses | £600 |

| Eat Out to Help Out | 4,775 restaurants | £42.9 |

| Scottish Government | ||

| Business Support Fund Grants (Small Business Grant Scheme and Retail, Hospitality and Leisure Business Grant Scheme) | 91,258 awards | £1,019.5 |

| Non-Domestic Rates Relief (100% Retail, Hospitality and Leisure / Airport & 1.6% Universal) | 250,940 properties | £965.0 |

| Strategic Framework Business Fund | 47,658 awards | £344.8 |

| Strategic Framework Business Fund Transition Payment and Restart Grant | 49,222 awards | £444.8 |

| Localised Restrictions Fund | 9,038 awards | £9.3 |

| Local Authority Discretionary Fund | 22,902 awards | £92.4 |

| Hospitality, Retail and Leisure Top Up funds | 33,388 awards | £234.3 |

| Newly Self-Employed Hardship Fund Round 1 | 5,673 self-employed individuals | £11.3 |

| Newly Self-Employed Hardship Fund Round 2 | 8,669 self-employed individuals | £34.6 |

| Creative, Tourism and Hospitality Enterprises Hardship Fund | 1,894 businesses | £23.6 |

| Pivotal Enterprise Resilience Fund | 1,763 businesses | £121.8 |

| Island Equivalent Fund (inc. top-up) | 2,265 awards | £11.7 |

| Mobile and Home Based Close Contact Services Fund | 8,945 awards | £35.8 |

| Support for Small Accommodation Providers Paying Council Tax Fund | 1,481 awards | £8.8 |

| Taxi and Private Hire Driver Support Fund | 21,838 awards | £32.8 |

| Museums and Galleries Scotland Funds | 351 awards | £8.7 |

| Scottish Wedding Industry Fund | 2,808 awards | £25.8 |

| Events Industry Support Fund | 505 awards | £5.0 |

| Events Industry Support Fund 2 | 409 awards | £7.4 |

| Visitor Attractions Support Fund | 340 awards | £9.7 |

| Scotland Coach Operators COVID-19 Business Support and Continuity Fund | 117 awards | £8.4 |

| Business contingency Fund Plus Grants | 345 awards | £5.4 |

| Culture Collective Fund | 26 awards | £5.9 |

| Hardship Fund Creative Freelancers | 4,639 freelance/self-employed individuals | £16.8 |

| Cultural Organisations and Venues Recovery Fund | 233 awards | £13.2 |

| Tour Operators Fund | 189 awards | 14.2 |

| Pivotal Event Businesses Fund | 103 awards | £11.1 |

| Scottish Wholesale Food and Drink Resilience Fund | 41 awards | £5.5 |

| Scottish Government Performing Arts Venues Relief Fund | 79 awards | £12.2 |

| Seafood Resilience Fund | 132 awards | £5.8 |

| Sea Fisheries Intervention Fund | 836 fishing vessels | £8.4 |

| Scottish Seafood Business Resilience Fund | 132 businesses | £5.8 |

| Coronavirus Liquidity Support for SME Housebuilders | 38 businesses | £18.0 |

| Creative Scotland and Screen Scotland Bridging Bursary Funds | 2,293 freelance/self-employed individuals | £4.3 |

Notes:

Data on number of businesses supported and amount spent by schemes cannot be aggregated as data relate to different time periods for each scheme and businesses may be in receipt of support from more than once scheme.

Data is not finalised for some schemes.

Data for the Business Support Fund Grants on the number of grants awarded does not equate to the number of businesses supported as businesses with multiple eligible properties could apply for multiple grants.

"-" data for Scotland not available. Data for the UK as a whole provided in Annex 1.

UK Government Schemes

Coronavirus Job Retention Scheme (CJRS)[17] : £65.9 billion spent across the UK as a whole (data for Scotland not available). 906,400 cumulative jobs furloughed in Scotland since its inception.[18] The take-up rate as at 31st May 2021 (furloughed staff as a proportion of eligible employments) in Scotland was 7%, broadly in line with the other UK nations. 48% furloughed employments in Scotland were fully furloughed with the remaining 52% on flexible furlough. By local authority, Highland (9%) had the highest take-up rate and Shetland Islands had the lowest (5%). Looking at the urban/rural split, 29% of employees furloughed in Scotland were in local authorities (LAs) classed as rural and 71% were in LAs classed as urban, broadly in line with the proportion of Scottish employment in each area. The take-up rate was 7% in rural LAs and 8% in urban. By sector, in Scotland, the highest take-up rate was in Accommodation & Food Services (32%) followed by Arts, Entertainment & Recreation (27%), and Other Services (19%). By gender, the take-up rate was slightly higher for men (8%) than women (7%) in Scotland, broadly in line with the UK. Data on take-up by business size band and age is currently only available at the UK level. By business size band, across the UK a whole, 39% of jobs furloughed were in micro firms, 25% in small, 13% in medium and 23% in large firms. The take-up rate was higher for the younger age groups of under 18 (13%) and 18-24 year olds (10%) compared to the UK average (8%).

Self-employment Income Support Scheme (SEISS)[19] : £1.5 billion spent in Scotland across four rounds. 553,000 self-employed individuals in Scotland made a claim. Scotland accounted for 6% of UK claims reflecting the fact that there are relatively fewer self-employed people, and hence eligible claimants, in Scotland.

The following statistics relate to claims to the fourth SEISS grant. In Scotland, 120,000 out of an eligible 207,000 self-employed individuals made a claim in the fourth round of SEISS, representing a 58% take-up rate, in line with the UK as a whole. The total value of claims was £337 million with the average claim value being £2,800 (the same as the UK). By local authority, the highest take-up rate was in West Dunbartonshire (68%) and the lowest in Orkney Islands (35%). By urban rural classification, the take-up rate in LAs classed as rural (51%) was slightly lower than that in LAs classed as urban (62%). By sector, the highest take-up rate was highest in Other Service Activities (includes hairdressing and beauty) (76%) and Transport & Storage (75%) and the lowest was in Agriculture, Forestry & Fishing (25%). Construction received the greatest proportion of the total value of claims in Scotland (32%). By gender, a slightly lower proportion of eligible females claimed (56%) compared to males (59%). The average claim for females was also lower at £2,300 compared to £3,100 for males.

Loan Schemes[20] : Take-up (number of loans approved) and value (value of loans approved) data for Scotland is available for the Coronavirus Business Interruption Loan Scheme (CBILS) and Bounce Back Loan Scheme (BBLS). However, only data at the UK level is available for the Coronavirus Large Business Interruption Loan Scheme (CLBILS).

- Bounce Back Loan Scheme (BBLS): 86,062 loans worth over £2.5 billion have been offered to businesses in Scotland under BBLS. Loans offered to businesses in Scotland accounted for 6% of the total value awarded to the UK as a whole, in line with Scotland's share of the UK business population (6%).

- Coronavirus Business Interruption Loan Scheme (CBILS): 4,144 loans worth over £982.5 million have been offered to businesses in Scotland under CBILS. Loans offered to businesses in Scotland accounted for 6% of the total value awarded to the UK as a whole, in line with Scotland's share of the UK business population (6%).

- Coronavirus Large Business Interruption Loan Scheme[21] (CLBILS): £5.56 billion spent across the UK as a whole. 753 businesses approved out of 1,152 applications, a 65% success rate.

Future Fund[22] : £8.6 million spent in Scotland with 22 businesses supported. Scotland accounted for just 0.7% of the UK total by value while London and the South East together accounted for 72%, broadly in-line with the wider market trends for the distribution of equity investment across the UK. The average loan amount was significantly lower in Scotland (£0.39 million) than in the UK as a whole (£0.97 million). Scotland reported the lowest average loan amount and share of total value of loans approved out of all the UK regions. Data on application success rate and breakdowns by gender and ethnicity of management teams is only available at the UK level. 77% of the total value of loans approved in the UK as a whole went to companies with mixed gender management teams. Only 1% of funding went to all female management team businesses. 56% went to businesses with mixed ethnicity management teams, 38% went to all White management team businesses and 5% went to sole ethnic minority management team businesses.

COVID Corporate Financing Facility (CCFF)[23] : OCEA have matched the names of the businesses supported under the scheme as at 30th June 2021 to the FAME database. Two of the 21 businesses supported are registered in Scotland, both of which are in the transportation and storage sector. The value of commercial paper held by the CCFF for these two businesses was £600m. The majority (71%) of business supported by the scheme were registered in England. It is important to note that while a business may not be registered in Scotland, it may operate in Scotland, which is the case for a number of businesses supported under the scheme. The number of businesses supported in Scotland may therefore be higher in reality than the data based on headquarters location suggests.

Eat Out to Help Out[24] : £42.9 million spent (discount claimed through scheme) in Scotland with 4,775 restaurants with 25 or less outlets supported. Scotland accounted for 8% of total UK claims and 7% total amount of discount claimed. The average amount claimed per outlet in Scotland was £9,000, slightly lower than the UK average of £10,198. By local authority, Edinburgh had the greatest share of restaurants making claims under the scheme in Scotland for which data were available (15%). However, Glasgow had the largest share of meals claimed for (17%) and share of discount claimed (18%) for the scheme in Scotland. In terms of numbers of meals claimed for, Glasgow ranked 7th of 379 UK local authorities, while Edinburgh ranked 11th.

Scottish Government Schemes

Business Support Fund Grants (Small Business Grant Scheme and the Retail, Hospitality and Leisure Business Grant Scheme)[25] : £1,019.5 million paid out. 91,258 grants awarded out of 106,662 applications, a provisional award rate (grants awarded as a percentage of total applications) of 86%.[26] By value, 77% of grants was distributed via the Small Business Grant, 22% via the Retail, Hospitality and Leisure Grant and 1% via grants to businesses who do not pay non-domestic rates directly but lease shared commercial space. By local authority, Fife (94%), East Lothian (91%) and East Dunbartonshire (90%) had the highest provisional award rates while Perth and Kinross (75%) had the lowest. In terms of the geographical spread of the value of funds received from the grants as a whole, Glasgow received the highest proportion (12%). By urban/rural split, non-domestic rates payers in LAs classed as urban received 61% of the total value of grants while those in LAs classed as rural received 39%. The provisional award rate was broadly similar in LAs classed as urban (84%) and those classed as rural (85%).

Non-Domestic Rates Relief (100% Retail, Hospitality and Leisure / Airport & 1.6% Universal)[27] : An estimated £965 million of NDR income was forgone in 2020-21 through both non-domestic rates relief measures (100% RHLA relief and 1.6% universal relief awarded to all properties). 28,400 properties have been supported through the RHL relief while all 250,940 received the 1.6% universal relief. NDR reliefs are administered by local authorities, meaning that the Scottish Government does not have data on applications. In 2020-21 both reliefs were automatically awarded, removing the need for applications to be made at all. By property class, it is estimated that the majority of rates relief went to shops (£618.6 million) while £122.7m went to hotels, £55m to leisure properties, and £51.4m to public houses and restaurants.[28]

By local authority, the proportion of properties on the Valuation Roll receiving RHLA relief ranged between 4% in the Shetland Islands and Na h-Eileanan Siar, to 19% in City of Edinburgh. By value, City of Edinburgh (20%) also saw the greatest share of value followed by Glasgow City (16%).

Strategic Framework Business Fund (SFBF)[29] : £344,783,237 has been paid out to 47,658 premises under the SFBF business restrictions and closure grants (2 November 2020 to 22 March 2021, at scheme close). £419.57 million was allocated to the scheme, therefore 82% of the budget has been spent to date. The provisional application success rate is 69%. 92% (£318.78 million) of funds were paid out under the Temporary Closure Fund with the remaining 8% (£26.00 million) paid out under the Business Restrictions Fund. By local authority, application success rate was highest in Aberdeenshire and Highland (both 91%) and lowest in Midlothian, Glasgow City and East Ayrshire (all 55%). By size (in terms of rateable value), 89% of SFBF funds were paid to businesses with rateable value less than £51,000, the remaining 11% being paid to larger businesses.

Strategic Framework Business Fund Transition Payment and Restart Grant: £431.98 million in Restart grants and transitional payments. In addition to this, small accommodation providers that pay council tax received £12.84 million in Restart grants and transitional payments. Together this totals £444,820,593. Of those premises estimated to be eligible, 98% were paid. The non-essential retail sector was paid a total of £155,259,143 (21,535 premises) and the Hospitality and Leisure sectors were paid a total of £280,717,450 (26,259 premises). Small accommodations paying council tax were paid a total of £12,844,000 (1,428 premises). By local authority, Highland received the greatest share of both the transitional payment (11%) and Restart grant (12%), followed by Glasgow City and City of Edinburgh. Shetland Islands received the lowest share for both funds.

Localised Restrictions Fund: £6,603,200 has been paid out to businesses in the 14 local authorities that remained in Protection level 2 from 5 June 2021. An additional £388,600 has been paid to Moray and £2,308,275 to Glasgow City that remained in Protection level 3 (as at 25 June 2021). In total, this scheme has paid £9.3 million to 9,038 businesses.

- Under the Level 3 restrictions, 2,019 premises in Glasgow City received 86% (£2.3 million) of amount spent and 652 premises in Moray received 14% (£0.4 million). Nearly three quarters (73%) went to businesses with a rateable value (RV) less than £51,000.

- Under the Level 2 restrictions, nearly all (99%, £6.5 million) of the funding was distributed through the Restrictions Fund. The remaining funding (£73,250) was through the Closures Fund. By local authority, Glasgow and Edinburgh received the greatest share of the Restrictions Fund (both 27%). Glasgow (20%) also received the greatest share of funding through the Closures Fund followed by North Lanarkshire (18%).

Local Authority Discretionary Fund[30] : £92,394,065 has been awarded to 22,902 premises through the Local Authority Discretionary Fund. 29,696 eligible applications have been received of which 22,913 were successful. The application success rate is 77% with an average (mean) amount awarded of £4,032. The rejection rate is 22% and 1% of applications were still being processed. The main reasons reported for rejected applications were that applicants were unable to fully evidence criteria for fund, or that they were eligible for a different fund instead. By local authority, the application success rate was highest in Scottish Borders and Perth and Kinross (both 87%) and lowest in East Renfrewshire (50%). Glasgow and Edinburgh received the greatest share of funding.

Hospitality, Retail and Leisure Top Up Payments[31] : £234,301,500 has been awarded to 33,388 hospitality, retail and leisure businesses through the HRL Top-up Funds. 96% of eligible premises in Scotland had been paid through the scheme. By local authority, Glasgow City and City of Edinburgh received the greatest share of both total premises paid and value paid. £35.8 million was awarded to 4,832 premises in Glasgow City and £30.42 million to 3,836 premises in City of Edinburgh. Clackmannanshire, East Renfrewshire, Midlothian and Inverclyde received the lowest share of total premises and value paid.

Island Equivalent Fund[32] : £7,653,700 was paid to 1,660 premises in the main round of the Island Equivalent Payment Scheme. A further 605 premises were paid in the top-up worth £4,068,000. This takes the total to £11,721,700 paid to 2,265 island businesses. The application success rate for the main round of the scheme was 92% and the rejection rate was 8%. The success rate was lower than average in Shetland (81%) and Orkney (85%). The greatest share of funding in the main round went to Argyll & Bute (41%) followed by Orkney (29%).

Newly Self-Employed Hardship Fund[33] : £45.9 million paid out under two rounds. For the first round 5,673 grants awarded out of 8,006 applications, an award rate of 71%. The total value awarded for the first round stood at £11.3 million. For the second round, 8,669 grants were awarded out of 9,668 applications, an award rate of 90%. The total value awarded for the second round stood at £34.6 million.

The following statistics relate to the first round of the scheme: By local authority, Glasgow and Edinburgh received the highest proportion of grants by both number and value awarded. Fife (86%), West Dunbartonshire (86%) and Shetland Islands (85%) had the highest award rates while Orkney Islands (50%) and Glasgow City (56%) had the lowest. By urban/rural split, businesses in LAs classed as urban received around two thirds (64%) of the grants awarded. The award rate was slightly higher in LAs classed as rural (72%) than in LAs classed as urban (70%).

Creative, Tourism and Hospitality Enterprises Hardship Fund[34] : £23.6 million offered to businesses. 1,894 grants approved out of 3,413 valid applications,[35] a 55% award rate. By sector, three quarters (76%) of the value of grants offered were to businesses in the tourism and hospitality sector while around a quarter (24%) went to the creative sector. In terms of value of grants offered by local authority, Edinburgh (15%), Glasgow (14%) and Highland (12%) had the highest proportion of grants offered, together accounting for 41% of the total value of grants offered.

Pivotal Enterprise Resilience Fund (PERF)[36] : £121.8 million offered to businesses. 1,763 grants offered out of 5,069 valid applications, a 35% award rate. Five sectors (Tourism & Hospitality, Other Manufacturing, Construction, Wholesale & Retail and Creative Industries, together accounted for almost two thirds (61%) of grants offered by value and number of businesses. In terms of value of grants offered by local authority, Glasgow (12%), Edinburgh (11%) and Highland (9%) again had the highest proportion of grants offered, together accounting for around a third of the total value of grants offered, broadly reflecting the proportion of registered businesses those areas account for.[37]

Business contingency Fund Plus Grants (Travel Agents, Brewers and Indoor Football Centres)[38] : A total of 345 awards have been paid through the scheme worth £5.4 million.

- Travel agents - £3,670,000 has been paid to 233 premises defined as travel agents. Travel agents received the greatest share of funding (68% of total value and premises).

- Breweries - £1,516,250 has been paid to 102 premises defined as breweries. Breweries received 30% of total value and made up 28% of total premises.

- Indoor football centres - £205,000 has been paid to 10 premises defined as indoor football centres. Indoor football centres received the lowest share of funding (4% of total value and made up 3% of total premises).

Support for Small Accommodation Providers Paying Council Tax Fund[39] : Across the three waves of the funds, 1,481 applications had been awarded with a total value of £8,830,000 million. 348 premises were paid under the first wave with a value of £2,076,000. 133 premises were paid under the second wave with a value of £786,000. 1,000 premises were paid under the third wave with a value of £5,968,000. By local authority, Highland received the greatest share of support for both number of premises and value across the three waves of the support.

Taxi and Private Hire Driver Support Fund (March 2021)[40] : 21,838 drivers have been paid through the scheme out of 33,767 eligible drivers, a success rate of 65%. Total spend under the scheme stood at £32,757,500 as at 25 June 2021. 2,039 applications were rejected (6% of eligible drivers and 9% of applications received). The main reasons for rejection were failure to supply supporting evidence (42%) and duplicate application (38%). By local authority, Glasgow (21%) and Edinburgh (20%) received the greatest share of total value paid through the scheme. Orkney, Aberdeenshire and Shetland received the least in terms of value (all 0%). Looking at the percentage of eligible drivers paid in each local authority, Dundee paid the greatest share (90%).

Coronavirus Liquidity Support for SME Housebuilders[41] : 38 applications had been approved out of 52 submitted, an award rate of 73%. Loans approved to date are worth £18,020,417. 14 applications were rejected, a rate of 27%. The average (mean) loan amount requested was £485,808 and the average loan amount approved was £474,221 (98% of value requested). Glasgow and Edinburgh & Lothians received the greatest number of applications with 12 each.

Mobile and Home Based Close Contact Services Fund[42] : 8,945 businesses have been paid through the scheme worth a total value of £35.8 million. The award success rate for the scheme is 89%.

Museums and Galleries Scotland Funds[43] : A total of £8,693,756 million was paid out through 351 awards under the following five Museums and Galleries Scotland funds:

- COVID-19 Museum Development Fund - A total value of £805,584 was paid to 22 organisations in Scotland. The average amount paid out through the scheme was £36,617.

- Recovery and Resilience Fund - 90 awards paid through this scheme out of 116 applications, an award rate of 78%. A total of £4.6 million was paid out through this scheme. An additional 59 awards were paid through the top-up of the Recovery and Resilience fund worth £2.3 million. 60 applications were filed for the scheme with an award rate of 98%. A total of 149 awards were paid through the scheme worth £6,877,366.

- COVID-19 Adaptation Fund - 92 awards paid through this scheme out of 97 applications, an award rate of 95%. A total of £300,000 was paid out through this scheme. The average (mean) amount was £3,260.

- Urgent Response COVID-19 Fund - 20 awards paid through this scheme out of 29 applications, an award rate of 69%. A total of £600,000 was paid out through this scheme. The average (mean) amount was £30,000.

- Digital Resilience COVID-19 - 68 awards paid out of 77 applications, an award rate of 88%. A total of £110,806 was paid out through this scheme. The average (mean) amount was £1,629.

Scottish Wedding Industry Fund[44] : 2,817 awards have been successful out of 3,478 applications, an award rate of 81%. A total of £25,800,000 has been paid out through the scheme to date to 2,808 awards.

Events Industry Support Fund[45] : 505 awards have been paid out of 833 applications, an award rate of 61%. A total of £5,000,000 has been paid out through the scheme to date.

Visitor Attractions Support Fund[46] : 340 awards have been paid out of 407 applications, an award rate of 84%. A total of £9,700,000 has been paid out through the scheme to date.

Scotland Coach Operators COVID-19 Business Support and Continuity Fund[47] : 117 awards have been paid out of 147 applications, an award rate of 80%. A total of £8,400,000 has been paid out through the scheme to date.

Hardship Fund Creative Freelancers[48] : 4,639 awards have been paid out of 4,816 applications, an award rate of 96%. A total of £16,800,000 has been paid out through the scheme to date. By region, the greatest share of funding went to Glasgow (39% by number of awards and 38% by value). North East Scotland received the smallest share of funding through the scheme (both 5%).

Culture Collective Fund[49] : 26 awards have been paid out of 64 applications, an award rate of 41%. A total of £5,900,000 has been paid out through the scheme to date. By region, the greatest share of funding went to Lothians (31% by number of awards and 28% by value), followed by Highlands and Islands (19% by number of awards and 24% by value).

Cultural Organisations and Venues Recovery Fund[50] : 233 awards have been paid out of 348 applications, an award rate of 67%. A total of £13,200,000 has been paid out through the scheme to date. The following data is for round 1 of the scheme as at 5th November 2020: by creative sector, the greatest share of value of funding went to the Nightclub sector (27%), which received 33 awards worth £3,151,288. By local authority, Glasgow City (38%) and City of Edinburgh (26%) received the greatest share of value of funding. 71 awards were successful in Glasgow City worth £4,512,618 and 46 were awarded in City of Edinburgh worth £3,104,740. Orkney Islands received the smallest share of funding (0.1%) worth £10,000 to one award.

Pivotal Event Businesses Fund[51] : 103 awards have been paid out of 129 applications, an award rate of 80%. A total of £11,100,000 has been paid out through the scheme to date.

Scottish Wholesale Food and Drink Resilience Fund[52] : 41 awards have been paid out of 113 applications, an award rate of 36%. A total of £5,500,000 has been paid out through the scheme to date. By local authority, the greatest share of awards and funding went to Glasgow (22% of total awards and 21% of value).

Scottish Government Performing Arts Venues Relief Fund[53] : 79 awards have been paid has been paid out through the scheme to date, a total value of £12,200,000. By local authority, City of Edinburgh (16% of total awards and 22% of value) and Glasgow City (both 15%) received the greatest share of awards and value awarded.

Tour Operators Fund (inc. international inbound and larger domestic operators[54] : 189 awards have been paid out of 278 applications, an award rate of 68%. A total of £14,200,000 has been paid out through the scheme to date.

Creative Scotland and Screen Scotland Bridging Bursary Funds[55] : £4.3 million paid out across the two funds. 2,293 grants awarded out of 2,831 applications, an 81% award rate. By LA, Glasgow (41%) and Edinburgh (22%) accounted for almost two thirds of the total value awarded by the Creative Scotland bursary. Glasgow City (49%) accounted for almost half of value awarded by the Screen Scotland bursary.

Fisheries and Seafood Support Funds[56] : 968 applications awarded and £14.2 million paid out across the two funds. (a) Sea Fisheries Intervention Fund: £8.4 million paid out. 836 grants approved out of a total of 867 applications, a 96% award rate. (b) Scottish Seafood Business Resilience Fund: £5.8 million paid out to 132 businesses.

4.2 Impact of Support on Businesses

Summary

- Feedback from the business representative organisations suggests Government support has provided lifeline support for businesses during lockdown, helping most business survive up to this point.

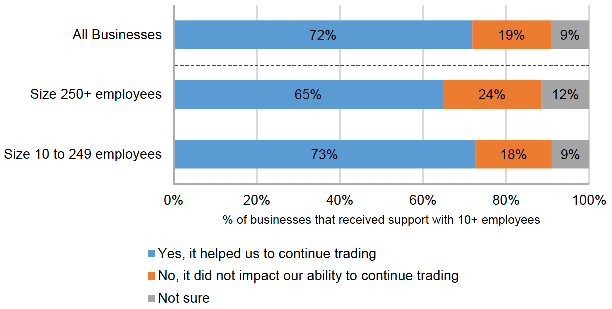

- The BICS data supports this message, indicating that the support received from the Scottish and UK Governments has helped most beneficiaries survive through the immediate crisis. 72% of businesses in Scotland who received support reported that it had helped them continue trading.

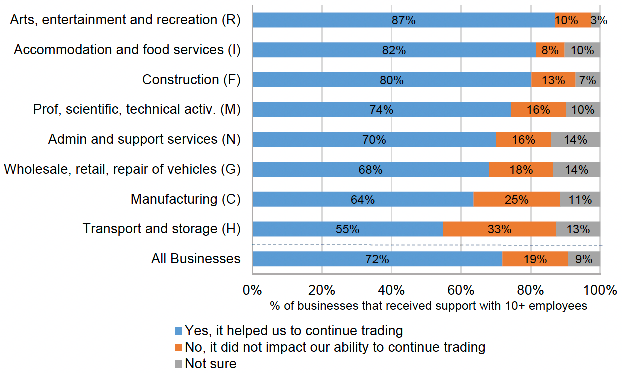

- The sectors that have benefited most from the support provided by the Scottish and UK Governments (those with the highest proportion of businesses reporting the support helped them continue trading in BICS) were: Arts, Entertainment & Recreation (87%); Accommodation & Food Services (82%); Construction (80%); Professional, Scientific, Technical Activities (74%); and Admin & Support Services (70%).

- Since the initial evaluation, the Arts, Entertainment & Recreation sector has seen an increase in the share of businesses reporting that the support had helped them continue trading while the Accommodation & Food Services sector has seen a decline in the share of businesses reporting that the support had helped them.

- A third (33%) of businesses in the Transport & Storage sector reported that the support did not have an impact on their ability to continue trading, followed by a quarter (25%) of Manufacturing businesses and 18% in the Wholesale, Retail & Repair of Vehicles sector (though still a majority in each felt it had helped continue trading).

- OCEA's Strategic Framework Sector Viability Modelling, which models the impact of the CJRS and non-domestic rates (NDR) relief on business viability, suggests Accommodation & Food Services has been the sector most impacted by COVID-19 restrictions over the course of the pandemic. Construction, Transport & Storage, Admin & Support Services, and Other Service Activities are also modelled to have been significantly affected.

- Findings from BICS indicates that the support received from the Scottish and UK Governments has had a bigger impact on SMEs (73% felt it had helped them continue trading) than on larger businesses (65%), largely reflecting the targeting of Scottish Government support at smaller businesses.

- Reflecting the high uptake of the CJRS, feedback from the business representative organisations highlighted the fundamental role the scheme has played in maintaining business viability and the likely impact that its unwinding will have on redundancies if demand remains weak and businesses' turnover is insufficient to cover wage bills. This is supported by results of OCEA's Strategic Framework Sectoral Viability Model which indicate that business support – CJRS in particular, was crucial in maintaining a degree of profitability in the worst affected sectors at crucial stages in the pandemic.

- OCEA's Strategic Framework Sectoral Viability Model found that business support (CJRS in particular) was effective in softening impacts of the pandemic, but did not restore viability close to pre-COVID-19 levels in the worst affected sectors (e.g. Accommodation & Food Services) over the course of the pandemic so far. Grants schemes (e.g. Business Support Fund) are most effective for micro businesses.

- Of the Scottish-specific schemes, the two core grant funds (Small Business Grant and Strategic Framework Business Fund) appear to have had the biggest impact, reflecting their scale relative to the other interventions. These funds had the greatest reach with the highest proportion of businesses in Scotland applying and receiving the grant support according to BICS. Feedback from the business representative organisations also indicates that grant support, particularly the Business Support Fund Grant, have been more popular than other support measures offered to businesses.

- Feedback from the business representative organisations indicated that the loan schemes were less popular than grant schemes, with many businesses reluctant to take on new debt given the uncertainties they face. The number of businesses receiving financial support from the UKG government-backed loan schemes has increased significantly since the initial evaluation undertaken in summer 2020 indicating that businesses are taking tentative, but necessary measures to survive in subsequent lockdowns.

- Where debt has been taken on, evidence suggests fears that it may hamper business recovery and growth for many businesses. This indicates that the loan schemes may potentially have a lower net benefit to businesses than the grant schemes.

Whereas the previous section focused on the uptake of the support schemes in Scotland, this section considers the impact of the support in terms of businesses' ability to survive and maintain employment in the short-run. It draws on qualitative evidence from business representative organisations, intelligence gathered by the enterprise agencies from their account-managed firms as well as evidence from BICS and OCEA's Strategic Framework Sectoral Viability Model.

Feedback from the business representative organisations and enterprise agencies suggest that government schemes have provided lifeline support for businesses during periods of lockdown restrictions, helping most business survive up to this point. This is echoed in data from BICS which indicates that the support received from the Scottish and UK Governments has helped most beneficiaries survive through the immediate crisis. BICS data for the period 17 to 30 May 2021 (wave 31) shows that almost three quarters (72%) of businesses in Scotland (who had not permanently stopped trading at the time of the survey and had received support from Scottish or UK Government schemes or initiatives) reported that the support helped them to continue trading. 19% felt the support received had not impacted their ability to continue trading and 9% were not sure. Compared to the last wave of BICS with comparable results (wave 16 – 19 Oct to 1 Nov 2020), less businesses felt that the support had helped them continue trading (77% compared to 72% in wave 16). It should be noted the varying levels of restrictions placed on businesses during these period which may influence businesses' responses to this question.

Impact by Sector

BICS data suggests that the sectors that have benefited most from the support provided by the Scottish and UK Governments (in terms of having the highest proportion of businesses that received support reporting the support helped them continue trading were: Arts, Entertainment & Recreation (87%), Accommodation & Food Services (82%); Construction (80%); Professional, Scientific & Technical Activities (74%); and Admin & Support Services (70%) (Chart 26).

The Accommodation & Food Services, Admin & Support Services, and Transport and Storage sectors all saw a significant decline in businesses reporting that the support package has helped them continue trading compared to the previous wave of BICS (wave 16). The Arts, Entertainment & Recreation sector has seen an increase since the last comparable wave of BICS, and are now the sector with the greatest share of businesses reporting that the support had helped them continue trading. 87% in the sector stated that it helped them in wave 31 (17 to 30 May 2021) compared to 77% in wave 16 (19 Oct to 1 Nov 2020).

A third (33%) of businesses in the Transport & Storage sector reported that the support did not have an impact on their ability to continue trading, followed by a quarter (25%) of Manufacturing businesses and 18% in the Wholesale, Retail and Repair of Vehicles sector.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

Note: Reliable data on the Water Supply, Sewerage, Waste (E), Information and Communication (J), Real Estate Activities (L), Education (P), Health and Social Work (Q), Other Services Activities (S) and Mining and Quarrying (B) sectors is not available.

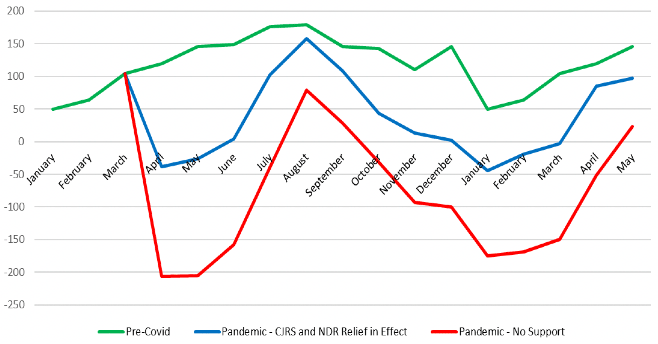

OCEA's Strategic Framework Sectoral Viability Model corroborates BICS findings on impact for the most part. By comparing the level of government support provided by two key schemes, the CJRS and non-domestic rates (NDR) relief,[57] and the financial losses that businesses have incurred across the sectors of the Scottish economy, the model identifies those sectors where viability has been most impacted by the pandemic, and the extent to which it has been restored by support.

Table 5 shows, for each sector from March 2020 to May 2021 based on 2018 Scottish Annual Business Statistics data: modelled pre-COVID-19 profitability; modelled profitability without government support; modelled profitability with support from the CJRS and NDR relief.

| Modelled Profitability by Sector - March 2020 to May 2021 | |||||

|---|---|---|---|---|---|

| Pre-Covid (£m) | No Support (£m) | CJRS and NDR Relief in Effect (£m) | No Support (% of Pre-Covid) | CJRS and NDR Relief in Effect (% of Pre-Covid) | |

| Agriculture, forestry and fishing | 555 | 504 | 566 | 91% | 102% |

| Mining and quarrying | 15,111 | 10,833 | 11,476 | 72% | 76% |

| Manufacturing | 7,359 | 5,779 | 6,696 | 79% | 91% |

| Construction | 4,848 | 2,547 | 3,465 | 53% | 71% |

| Wholesale, retail, repair of vehicles | 7,473 | 5,678 | 7,461 | 76% | 100% |

| Transport and storage | 3,199 | 917 | 2,062 | 29% | 64% |

| Accommodation and food services | 1,902 | -1,228 | 644 | LOSS | 34% |

| Information and communication | 3,575 | 3,004 | 3,329 | 84% | 93% |

| Prof, scientific, technical activ. | 6,304 | 5,048 | 5,778 | 80% | 92% |

| Admin and support services | 4,338 | 2,408 | 3,352 | 56% | 77% |

| Other service activities | 861 | -211 | 30 | LOSS | 3% |

Source: OCEA Strategic Framework Viability Model

Findings indicate that every sector has been adversely impacted by the pandemic; some to a greater degree than others. With no support, the sectors (at SIC section level) identified as having had their viability most significantly impacted are:

- Construction

- Transport & Storage

- Accommodation & Food Services

- Admin & Support Services

- Other Service Activities

It should be noted, however, that there is significant variability at sub-sector (division) level within the broad sectors (sections). For example, it is recognised that non-essential retail businesses have suffered significantly more than essential retail businesses, or that the aviation component of Transport & Storage is likely to have suffered significantly worse than the sector as a whole.

Of CJRS and NDR Relief, CJRS has been the most significant. Given the nature of CJRS, those sectors which have been most affected are also those likely to benefit most from this type of support. Those sectors modelled to have been most adversely affected are also those for which viability has been restored to the greatest extent by this support package.

The model finds Accommodation & Food Services to be the sector most significantly impacted by the pandemic. As shown in Chart 27 below, it finds that while profits remained depressed throughout the pandemic, the sector experienced a return to some level of profitability over the summer of 2020. In June to October 2020, with key support packages in place, profits were estimated to exceed estimated breakeven levels, approaching pre-COVID levels in August 2020 before the introduction of further restrictions. Business support has helped to reduce losses across the sector, but the modelling results suggest that viability is more dependent on recovery of trading opportunities and relaxation of restrictions. CJRS in particular has been effective in softening the impact of the pandemic, but has not restored profits to pre-COVID levels in the sector.

Source: OCEA Strategic Framework Viability Model

Impact by Business Size

Data from BICS indicates that the support received from the Scottish and UK Governments has had a bigger impact on SMEs' survival (73% of SMEs felt the support received helped them continue trading) than on larger businesses (65%). This, however, is less of a difference compared to the last comparable wave of BICS (wave 16) where 79% of SMEs felt the support had helped them continue trading compared to 60% of large businesses.

Even as a sector moves back into profitability, sustained losses incurred over the course of the pandemic could still be an issue, with balance sheets significantly weakened. OCEA's Strategic Framework Sectoral Viability Model suggests that this could be especially the case for larger businesses in the worst affected sectors. By comparison, the model finds that grant schemes are typically most effective for smaller businesses.

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

Impact by Scheme

The qualitative feedback received from the business representative organisations and enterprise agencies for account managed firms is consistent with the BICS findings that government support has provided lifeline support during lockdown, helping most business survive up to now. SCC reported that the "the packages of business and wider fiscal support have been invaluable to businesses". The measures of support that were deemed to have had the most significant impact are the ones that have eased the most considerable costs that businesses face: covering the cost of employees' wages and business taxation.

The feedback highlighted the fundamental role of the CJRS and the potential impact that its unwinding will have on redundancies. The feedback suggested that, of all the schemes, the CJRS has had the biggest impact by far, preventing tens of thousands of business closures and redundancies in the short term. Protecting staff through furlough has aided the retention of essential skills within industries. This is line with the feedback collected in summer 2020 following the first lockdown. CBI Scotland reported that CJRS "has for many been described as a 'life-saver' for their business." This reflects the scale and blanket coverage of the CJRS where all businesses with employees in the UK were eligible since its inception in March 2020. Businesses have praised the government for extending schemes such as CJRS when necessary as the country faced continued lockdown restrictions throughout 2020 and 2021. The success of the furlough scheme also highlights the effectiveness of offering flexible support packages to businesses as nearly half of employees on furlough in Scotland are on it part-time.

Accordingly, businesses were still concerned about the winding down of the CJRS scheduled for September 2021 given the share of people still furloughed. More than 2 in 5 businesses (43%) reported staff on furlough in the two week period 28 June to 11 July 2021[58] and 1 in 10 (11%) eligible employments were furloughed in Scotland as at 30 April 2021.[59] Even in October 2020, at the point where restrictions on economic activity were most relaxed and a contribution to costs was required, 9% of the workforce were furloughed. As the scheme is phased out, while demand across many sectors of the economy remains weak and for many businesses, turnover remains insufficient to cover their wage bills, the business representative organisations highlighted the uncertainty they face for the future. Businesses worry that the economy will not have rebounded sufficiently enough by September, and that restrictions will not have eased enough to empower businesses to bring furloughed staff back to the workplace. This feedback supports the BICS findings and management information on the high uptake of the scheme relative to other schemes.

In regards to UK Government support, the VAT reduction was welcomed, but the STA noted that it only offered real value to those businesses able to trade and recommends that it is extended to make a significant impact. VAT repayment deferral was also seen as a necessary measure that helped a lot of businesses survive by easing cash flow pressures. SEISS was also flagged as having a significant impact on the self-employed, however the Scottish Government's Newly Self-Employed Hardship Fund was noted as being vital in filling in the gap for those recently self-employed. On UKG sector specific support, the Eat Out to Help Out Scheme available in August 2020 was valuable to the food and beverage services sector in stimulating demand. Businesses were keen for the scheme to be repeated if demand subsides later in 2021.

The intelligence gathered found many businesses are reluctant to take on new debt during the pandemic, and the loan schemes offered by the UK Government were resultantly not suitable for many businesses in affected sectors given future uncertainty to repay. Those that did benefit from the loan schemes reported that they were useful for cash flow purposes. The Bounce Back Loan Scheme introduced in May 2020 offered more favourable terms for small businesses and the share of businesses using the loan schemes has increased since its inception.

Following the first lockdown, businesses felt that the UK Government's Coronavirus Business Interruptions Loan Scheme (CBILS) had not delivered the intended volumes of short-term bridging finance that were envisaged at the time, however this was not as much of an issue for this round. Feedback from the FSB last summer indicated that "the major difficulties experienced by the Coronavirus Business Interruption Loan Scheme (CBILS) has not helped alter the view held by many that traditional debt finance is not a viable option for them." This reflects the scheme management information data presented in section 4.1 which showed that CBILS has supported just 5% (4,144 loans) of the number of businesses that the Bounce Back Loan Scheme supported (86,062 loans), which appealed more to smaller businesses. Nevertheless, BICS findings show that an increased share of business have applied for loan schemes (35%) when compared to the last comparable wave (26%).

Where debt has been taken on, the evidence gathered from the business representative organisations suggested that it is likely to hamper business recovery and growth for many businesses. The FSB noted that "debt had fallen on the shoulders of small businesses for a 'force majeure' while, according to some evidence, large businesses increased cash reserves." Intelligence from SE also states that "many businesses have delayed debt repayments over the last year and accrued even greater levels of debt – and now fear repayment coming due before revenue fully recovers". This issue was emphasised for the tourism sector and the long-term implications of debt for the competitiveness of the Scottish sector. Recent estimates by officials and bankers report that as much as £5bn of state-backed government COVID-19 emergency loans are at risk of not being repaid in the UK, however this is not as significant as first feared. The first few months of debt servicing shows that, so far, between 5% and 10% of SME beneficiaries of the Bounce Back Coronavirus Support Scheme have missed repayments.[60]

An Institute of Directors (IoD) survey found that 51% of IoD members surveyed in May 2020 thought debt taken on during the crisis would have a negative impact on their recovery over the next two years. 57% thought the debt taken on would hold back their investment plans over the next two years. More recent SE intelligence echoes this - "many smaller businesses expect to operate with high debt levels for the foreseeable future and are unlikely to invest in their business for some time as a result". This suggests that, when the potential adverse impacts on future performance are taken into account, the loan schemes may potentially have a lower net benefit to businesses than the grant schemes, even though they would have offered many businesses an opportunity to smooth out their cash flow challenges.

Of the Scottish-specific schemes, feedback from the business representative organisations suggests that the Business Support Fund Grants have had the biggest impact for the first lockdown in 2020. This reflects its scale and reach in terms of number and value of grants provided relative to the other interventions as highlighted in section 2.1. FSB Scotland reported that "for many local businesses, interventions such as the £1.2bn Coronavirus Business Support Fund have been the difference between closing temporarily and closing for good."

Business Rates relief was also seen as a scheme with great impact on Scottish businesses' ability to survive and retain employment. Rates relief was reported to have been particularly helpful for the hospitality and tourism sectors.

Tailored sectoral packages of support were very welcomed by majority of sectors, however it was noted these did not provide universal coverage (see "Perceived gaps in support" below). While many businesses report that the support has allowed them to survive, they feel it has not been enough for business to feel secure and competitive for future trading. A survey of aquaculture and sea fisheries businesses undertaken by Marine Scotland, a sector that received sector specific support by SG, found that over half (55%) of respondents partly relied on government support during COVID-19 restrictions while 18% of businesses solely relied on the support to continue operating.[61]

More recent support packages made by the Scottish Government, such as the COVID-19 Restrictions Fund and top up payments to furlough support, designed to cover periods of national lockdowns were seen as an important source of support in some of the most challenging times of businesses going through cycles of stop and start lockdowns, according to the SCC.

The business representative organisations welcomed the discretionary funding delivered by local authorities which they viewed as successful in addressing gaps in support, despite the delay in getting funding to businesses in need. Similar feedback was provided for the support delivered by the enterprise agencies such as the Pivotal and Hardship Funds.

While the support was welcome, some feedback indicated discontent with the Strategic Framework Support offered by SG due to its varying impact across sectors and business size. A survey of 350 businesses conducted by SCC found that over half (53%) did not feel that the Strategic Framework Support provided the financial support they needed.[62] A quarter (24%) reported that the support did cover their financial needs, while 23% did not know.

Despite the scale of financial support for businesses, feedback from business representative organisations suggested there is nevertheless a feeling that many small businesses were not supported sufficiently. The FSB noted a common perception that some businesses 'unfairly' received more support than others who were similarly deserving. Similarly, the feedback suggests many small businesses feel the support they received has allowed them to survive in the short term, but has been well below that which would be needed to fully offset income lost over the past year.

While the schemes with the greatest reach, such as the CJRS, are highlighted as having the greatest impact in terms of wider impact on the economy, smaller schemes targeted at certain businesses by sector, size or area have also had an important impact based on the circumstances of each business. The support package shaped over the course of the pandemic as circumstances evolved has allowed businesses to benefit from targeted financial support. Feedback indicated that the support package been most beneficial when businesses have taken advantage of multiple schemes to protect both the business and its employees e.g. CJRS and Business Grants.

4.3 Additionality of Scottish Government Support

Summary

- BICS data shows that a higher proportion of businesses that received Scottish Government support (including those also receiving support from UK Government) felt it helped them continue trading compared to those that received UK Government support only. This suggests Scottish Government support had an 'additional' impact, over and above the impact of the UK Government schemes.

- The share of businesses that received SG support (including those that also received support from the UKG) that reported it helped them continue trading has declined slightly compared to the last comparable waves of BICS in 2020, while those that received UKG support only has been relatively stable.

- Feedback from the business representative organisations suggests that Scottish Government support had filled many gaps in UK Government support but only for a limited number of businesses and sectors.

- The extent to which OCEA's Strategic Framework Sectoral Viability Model methodology can be applied to assess the relative impacts of SG support is relatively limited. However, the modelling results indicate that the support provided by the Business Support Fund Grants, on their own are effective in softening the impacts of restrictions, but for the average business will not have been enough to restore profits close to pre-COVID levels.

Whereas the previous section considered the impact of the Scottish and UK Government support package as a whole, this section focusses on the 'additional' impact the support provided by the Scottish Government had, over and above that of the UK Government support. It draws on qualitative evidence from business representative organisations and intelligence from the enterprise agencies on account managed firms as well as evidence from BICS and OCEA's Strategic Framework Sectoral Viability Model.

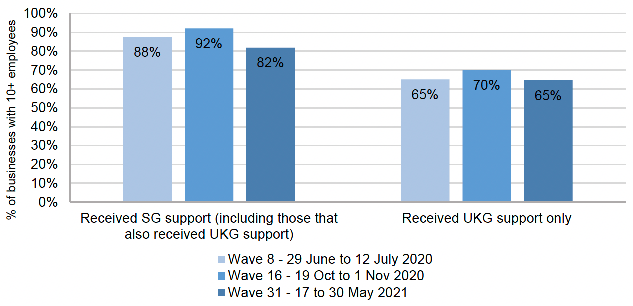

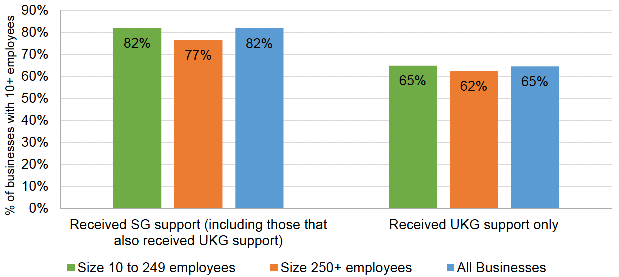

Data from BICS for the period 17 – 30 May 2021 (wave 31) shows that a higher proportion (82%) of businesses that received Scottish Government support (including those that also received support from UK Government) felt it helped them continue trading compared to those that received UK Government support only (65%). This suggests that the support provided by the Scottish Government had an 'additional' impact, over and above the impact of the UK Government schemes.

Chart 29 shows that the proportion of businesses that received SG support (including those that also received support from UKG) reporting the support helped them to continue trading was at its lowest level in the most recent wave of BICS (17 to 30 May 2021) compared to comparable waves from summer and autumn 2020.

Source: ONS: Business Insights and Conditions Survey (BICS)

Source: ONS: Business Insights and Conditions Survey (BICS) Wave 31

This is supported to some extent by the intelligence from the business representative organisations. Feedback received found that Scottish Government support has filled some of the gaps in UK Government support, but only for a limited number of businesses and sectors. The SCC recognised that the Scottish Government provided "bespoke schemes that were not available in other parts of the UK". The FSB echoed this: "The Scottish Government was able to 'plug' some gaps in support, initially via PERF and newly-self-employed funds but most notably the wide range of sectoral schemes that became available."

The SCC offered some criticisms amongst its broadly positive feedback for the SG in that "while the delivery and mechanisms of certain sectoral schemes from the Scottish Government could have been improved, they did address some critical gaps in business support not being filled by the UK Government". The STA were less positive in their feedback for the tourism sector stating that the Scottish Government's "level of support is still way below the basic fixed costs most businesses are having to incur. SG support helped narrow the gap but there remain gaps in support for many in the sector and the supply chain and the need for more to manage through recovery."

The discretionary fund delivered by local authorities was commended among the business representative organisations for filling the gaps in the main schemes, for example for businesses not directly impacted by restrictions, but experiencing supply chain issues or lack of demand from travel bans. The Newly Self-Employed Hardship Fund was also deemed successful in its goal to cover the key gap in the UK Government SEISS of it not being able to support those more recently self-employed.

Sector specific schemes delivered by the Scottish Government and its partners were seen to have had an additional impact on top of the support offered by the UK Government. Funds for accommodation and childcare providers and taxi drivers were highlighted along with the range of grants for the tourism and creative sectors. BICS data corroborates the improvement of the sector-specific support for the Arts, Entertainment & Recreation sector in helping businesses survive and maintain employment since the initial evaluation.

The IoD reported that larger businesses have relied mostly on support provided by the UK Government. This is expected given the targeting of Scottish Government support to SMEs. Furthermore, UK Government and Bank of England support such as CJRS, CCFF and the loan schemes were eligible for larger companies in any sector. It should be noted that support for large businesses is likely to feed through to support smaller businesses in larger businesses' supply chains.

In summary, of the Scottish-specific schemes, the Newly Self-Employed Hardship Fund, Discretionary Support Funds and certain sector specific schemes were seen to provide crucial support that was not covered by the UKG initiatives and schemes.

The extent to which OCEA's Strategic Framework Sectoral Viability Model methodology can be applied to assess the relative impacts of SG support is relatively limited. However, by modelling the annual profitability of the average firm in each sector split by size, and making assumptions about eligibility for the Business Support Fund Grants (i.e. micro and small businesses are eligible for a £10,000 grant and micro, small and medium-sized businesses in the retail, hospitality and leisure sectors are eligible for a £25,000 grant), it is possible to make some projections about the proportional impact of the Business Support Fund Grants.

The results, shown in Annex 2, demonstrate that for the most part, the support provided by the Business Support Fund Grants on their own, is not sufficient to return the worst affected businesses to pre-COVID levels of profitability. As with Business Support Fund Grants, the extent to which OCEA's Strategic Framework Sectoral Viability Model can be used to assess impacts of sector specific grants is limited, and attempts to use this method have not yielded conclusive results.

4.4 Application Processes for Scottish Government Schemes

Summary

- Businesses remained somewhat happy with the level of advice and support available, although this was less positive than the initial feedback collected in summer 2020 for the previous evaluation.

- Feedback from the previous evaluation undertaken in the summer of 2020 found that business representative organisations recognised that the SG and delivery partners were working at pace and therefore that some of the issues encountered were understandable given the timescales involved; however, some of these issues continued to be highlighted in this exercise.

- Businesses described a confusing landscape and difficulties in finding information on the schemes available. Some businesses were unaware of the support available to them.

- Businesses felt the applications process for some schemes was cumbersome and inefficient. Some businesses report not having received any explanation for having their application rejected.

- Feedback on application processing times was mixed. A noted complaint following the first lockdown was the perceived inconsistencies of approach across local authorities when appraising applications for the Business Support Fund Grants and differences in the efficiency at which applications were processed, however this appeared to not be as much of an issue for the subsequent grant schemes.

- Feedback from businesses in receipt of the Seafood Business Resilience Fund in 2020 indicates businesses were deeply appreciative of the grant, the speed at which applications were processed and the wider support provided. This perhaps reflects the smaller scale of the scheme relative to the significantly larger scale schemes where more processing issues were understandably found.

This section draws on feedback from the business representative organisations and enterprise agencies to assess businesses' perceptions about the delivery of the schemes based on their experiences at the application stage and on the processing of applications and payments.

As the pandemic context evolved throughout 2020 and 2021, businesses reported finding it difficult to navigate and understand information about the eligibility criteria for the schemes available. The Scottish Chambers of Commerce reported that many businesses "have not known what they were entitled to, saying that the process is too complex and slow" and the FSB echoed this stating that "many businesses were unaware of the support available". While businesses appreciated the urgency in getting funds to businesses, they were keen to have financial support and guidance as simplified and accessible as possible. Some businesses were unaware of the name of the schemes they had applied to or been awarded due to the sheer number of schemes made available. This was not necessarily a problem specific to Scottish Government support as there was criticism for UK Government also, but the majority of examples were in relation to SG schemes.