The Cost of Living Crisis in Scotland: analytical report

This report draws together analysis from a wide range of sources to provide an overview of emerging evidence on the cost of living crisis. It has been produced by a cross-government group of analysts.

Chapter 5: Households Most Affected

Introduction

While all households in Scotland will be affected by increases in the cost of living, the resulting harms will not be evenly distributed. It is those with lower incomes and little or no savings who will be most impacted. This section of the report describes:

- types of low income households

- why these households are particularly vulnerable when the cost of goods and services increases.

- how recent announcements by the UK government (described in Chapter 3) may, when fully implemented, affect these types of low income households

This chapter draws on routinely available data in Scotland, some bespoke analysis by analysts in the Scottish government, and is also informed by recently published reports from research organisations.

Low income households

There are a number of ways to define low income households. Examples of measures used include relative poverty (after housing costs), or the lowest income decile or quintile or the lowest 30% of households.[70] People on low incomes are not a homogeneous (or permanent) group and encompass different groups at different life stages. Irrespective of which of these measures are used, households with low income are likely to include over representation from the following groups:[71]

- disabled people

- lone parent families

- minority ethnic households

- other child poverty priority group households[72] (3+ children, mother under 25, baby under 1)

- renters (private and social)

- young adults (under 25)

- unemployed adults

- those with no formal qualifications

- recipients of income-related benefit

- people with no recourse to public funds

- people with multiple complex needs

Low income households as a whole are likely to be disproportionally negatively affected by increases in the cost of living due to:

Spending a higher proportion than average on energy, food and transport and therefore being more affected by inflation and having less flexibility in their budget to cope with price rises.

The percentage of net income spent on housing, fuel and food is considerably higher for households in the lowest three income deciles compared to those with higher incomes.[73] Low income households will therefore be relatively more affected by increases in prices. The IFS indicates that lower income households spend almost three times as much of their budgets on gas and electricity as the highest-income tenth on average (11% versus 4%).[74] Because low income households tend to spend more of their budgets on essential goods that have risen in price, the inflation rates they are experiencing are accelerating even faster than those faced by other households. The IFS predicted in August that the poorest fifth will face an 18% inflation rate in October 2022, compared to 11% for the richest fifth.[75]

Being more likely to be financially vulnerable, and entering the cost of living crisis in a position of financial hardship.

The poorest groups were already least financially resilient, with pre-existing hardship, and for some, a backlog of arrears and debt as a result of the austerity, reforms to the benefit system and the Covid-19 pandemic.[76] The Resolution Foundation argue that more than a decade of weak growth combined with high inequality means that the UK's poorer households are particularly exposed to income or spending shocks.[77] Many households went into the crisis already financially struggling, with 30% of households in Scotland not having enough savings to keep them above the poverty line for one month should they lose their income. This figure rises to 50% for the 20% of households with the lowest incomes.[78] Those on the lowest incomes were also most likely to lose their job, at least early in the pandemic.[79] Scotland saw a 108% rise in the number of emergency food parcels distributed in July 2020 compared with July 2019, and one in five households in Scotland with dependent children reported that they were "in serious financial difficulty".[80]

Being disproportionately affected by real-terms reductions in income-related benefits (more detail on this is included in the section below).

Low income households particularly negatively affected

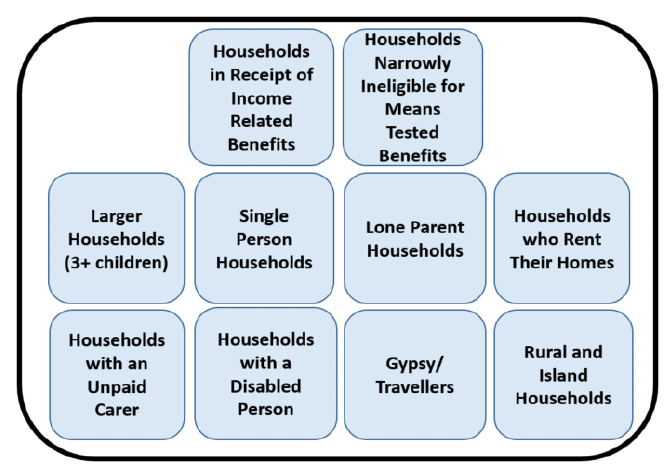

Within low income households there are a number of groups of people who are likely to incur additional costs and / or receive real-terms reduced income because of their particular characteristics and / or circumstances, and are therefore likely to be disproportionately affected by increases in the cost of living.[81] These frequently overlapping groups include sub groups of low income households, as set out below.

Descriptions of these households are included in Annex 2

Minority ethnic groups and women are more likely to live in the types of low income households identified in Figure 13.

Minority ethnic groups are significantly more likely to live in larger households[82], to be unpaid carers and live in private rented accommodation. Minority ethnic households are also more likely to have deeper levels of poverty[83] and so a greater proportion of their income is likely to be spent on essentials which are subject to inflation.

Women are likely to experience indirect effects of cost pressures that are not always apparent in routine data. This can, for example, be due to formal or informal caring responsibilities and loss of income or career progression due to these caring responsibilities and divisions of domestic labour. They are more likely to live in lone parent households, households with an unpaid carer and larger households. The Women's Budget Group produced a recent briefing on the gendered dimension of the cost of living crisis and argued that women are more exposed to cost of living pressures, due to lower earnings and savings (amongst other factors and structural inequalities).[84] [85] In addition, the six child poverty priority family types identified within the Child Poverty Delivery plan, which are more likely to include women, feature prominently within the groups identified above.

It is also important to consider major life events and points of transition, which can affect a range of different types of low income households. For example, additional costs may be incurred due to the arrival of a new baby, a child starting school, parental separation, bereavement, retirement, or the onset of poor health. There are also individuals within households with complex needs that may not be captured within the groups included in Figure 13. In addition, it is important to recognise that people who arrive in the UK as refugees and are seeking asylum also face particular hardship that will be exacerbated by the rising cost of living, as they are on very low fixed incomes and do not have the right to work.

There is also likely to be some overlap in relation to the household types identified above. In addition, people are shaped by their simultaneous membership of multiple social groups. Structural inequalities, reflected as relative experiences of disadvantage and privilege, are the outcome of people's membership of multiple interconnected social categories and the wider context of systems and structures of power (e.g. laws, policies, governments).[86] For example, experiences of disadvantage will compound in different ways for a minority ethnic disabled renter on income-related benefits, or a rural low income, or a lone parent family headed by a mother with caring responsibilities.

Evidence for the selection of households most negatively affected

This section sets out the evidence and rationale for why low income households with particular characteristics are more likely to be disproportionately affected by the cost of living crisis.

Households in Receipt of Income-related Benefits

Households in receipt of income-related benefits are likely to be disproportionally negatively affected, due both to the starting point of financial hardship following a sustained period of austerity and a series of benefit reductions since October 2021. These households are likely to be negatively affected by rising costs as a result of:

1) The removal of the temporary £20 per week uplift to Universal Credit (UC).

In March 2020 the UK government announced a £20 per week increase in UC and Working Tax Credit to "strengthen the safety net" during the pandemic. This uplift was withdrawn in October 2021. This meant a fall in income for over 400,000 households in Scotland.[87] A recent welfare reform report estimated that reinstating the £20 uplift would cost £540 million in Scotland in 2023/24, which is equivalent to the total income lost in that year as a result of the uplift being withdrawn (this includes the knock-on impact on devolved benefits like SCP).[88] Subsequent increases (a reduction in the taper rate and an increase in work allowances) only benefitted claimants in work.

2) Entering the cost of living crisis at a point where they were already struggling, and for some, having their UC reduced to pay off historic debts.

The Trussell Trust found that 17% of people receiving UC visited a food bank between Dec 2021 and March 2022.[89] JRF and others have written that benefit deductions are exacerbating this situation.[76] [90]

3) Being subject to a higher real-terms percentage fall in their income than people in employment (on average), by not receiving an uprating of benefits that reflects current rates of inflation.

Due to a range of UK government policy decisions, UK benefit rates have not kept pace with inflation in recent years.[91] In 11 of last 15 years the value of unemployment related benefits (including UC and Job Seekers Allowance) has declined and now have around 14% less purchasing power than they did in 2008[92]. This problem is particularly pronounced in a context of rising inflation due to the lag between the inflation period used (e.g. September) and when it is applied for benefit uprating (e.g. following April). The impact of the long-term approach has been to undermine the confidence that benefits will maintain their real value. In essence, there was already a long-term cost of living crisis for those on benefits which is the context for this current immediate pressure on prices.

The real-terms value of benefits devolved to the Scottish government have held up more than reserved benefits, largely due to the 6% uprating of the Scottish low income benefits in April 2022 compared with 3.1% for most reserved benefits. By way of comparison PAYE data show median monthly nominal pay grew 4.7% over the year in August 2022, however fell 4.4% in real terms (CPI adjusted), the seventh consecutive month of negative annual growth.[93]

In April 2022, UK benefits and state pensions were uprated using the annual rate of CPI to September 2021 (3.1%). However, this was significantly lowerthan the 7.0% recorded in March 2022, just before benefits were uprated, and inflation has risen since then to 10.1% in September. Although households will potentially benefit from these being uprated in April 2023 based on CPI rate in September 2022[94], there is still an issue with households not receiving uplifts to their benefit income when they actually need it. These households will have to wait for uprating to catch up with inflation in order to regain the real value of benefit payments.

As set out in Chapter 3, households in receipt of income-related benefits were specifically targeted for UK government support in the May 2022 Cost of Living Support Package. Despite this, these households are still likely to be disproportionally negatively affected given the latest forecasts for inflation. JRF published analysis that examined the cost rises facing low income working-age households on means-tested benefits this tax year compared to last tax year. They found that these households face a gap of £450 between now and April just to keep up with predicted price rises.[59]

Households Narrowly Ineligible for Means-tested Benefits

Amongst the groups identified by the Poverty and Inequality Commission and their Experts by Experience Panel as missing out, or receiving limited support under the UK government's Cost of Living Support Package, are households just above the benefits threshold, as well as disabled people who face higher energy costs but do not qualify for low income benefits.[95] There could be a significant number of people in Scotland who narrowly miss out on qualifying for the £650 Cost of Living payment for low income households. For example, there could be around 10,000 households in Scotland who earn just too much to qualify for Universal Credit.[96]

This group do not receive the additional £650 payment in the UK government's Cost of Living Supportpackage. The flat rate support to households on benefits, as well not taking account of family size or position in the labour market, represents a "cliff-edge" effect. This means that households who just become ineligible for benefits, for example through extra earnings, may lose that money, and not receive cost of living payments.

Households with an Unpaid Carer

Caring comes with additional costs that can significantly affect a carer's financial situation. For example, having to spend a larger proportion of their income on energy costs to keep the person they care for warm and manage their condition, having higher food bills due to the nutritional requirements to support the person they are caring for, and having higher transport costs because the person they care for needs support to travel or the carer has to travel to provide care.[97]

Carers UK have reported survey findings that found financial pressures for carers were exacerbated in the six months to March 2022, with the number of carers who are worried that they will not be able to manage their expenses more than doubling during that time. Almost half of carers in their survey indicated that increases in energy bills would negatively affect their health or the health of the person they care for.[97] Carers eligible for Carer's Allowance also only received a 3.1% uprating in April 2022.

Larger Households (3+ children)

The larger the family, the more goods and services need to be purchased. The proportion of children in combined low income and material deprivation is higher than average if they live in households with 3+ children.[98] A recent report from JRF finds that in line with findings from October 2021, families with three or more children were also disproportionately more likely to be in arrears, with 64% in arrears, compared to 27% of households without children.[76]

The Poverty and Inequality Commission and their Experts by Experience Panel identified larger families as one of a number of groups who miss out, or receive limited support, under the UK Government's May support package.[95] Larger households will receive the same lump sum payments as smaller households despite having higher costs.

A recent report from Professor Donald Hirsch -'Is cost of living support enough?'- found that the larger the household, the more the household will lose, and a couple with three children is losing almost as much again from rising prices as they did from last year's cut in the UC uplift.[99] The two-child benefit limit already means that larger families will not receive increasing support to reflect their situation.

Lone parent Households

Lone parent households, which are more likely to be headed by women, are at a much higher risk of poverty than the average household and have the highest living costs relative to their net income of all household types. In 2017-20, they spent on average 46% of their income on fuel, food and housing.[100]

JRF's recently published 'Poverty in Scotland 2022' report highlights the financial position of single parents as "extremely concerning" and "significantly more so than even the average position for all low income households": [101]

- they are significantly less likely to have savings than is seen in Scotland overall, with nearly 60% having no savings at all and almost 70% having either no

savings or savings of less than £250

- 70% have one or more debts and a quarter with debt have more than £2,500 of debt

- nine in ten single-parent families have cut back on a basic and eight in ten have cut back on an essential goods

- nearly half (45%) of single-parent families are behind on at least one bill or payment, nearly one in ten (9%) are behind on three or more

Single Person Households

As highlighted in the above section, the percentage of net income spent on housing, fuel and food is highest for single parent households, followed by single adult households without any children. Households with two or more adults (with or without children) have a lower cost of living.[73]

In May 2022, analysis from the New Economics Foundation (NEF) indicated that single female and black, Asian or other ethnic minority households are experiencing costs that are 50% higher than their male and white counterparts (respectively) as a portion of their income. Single women will see average costs increasing by £1,400 (6% of income) compared to £1,110 (4% of income) for single adult male households. The NEF argue that these outcomes are partly due to pre-existing gender and racial inequalities such as those that contribute to pay gaps in the labour market and unequal responsibility for childcare.[102]

Rural and Island Households & Households using off-gas-grid fuel

Whilst rural areas have lower levels of relative poverty overall, low income households living in rural areas face particular challenges. There is widespread evidence that rural areas, and remote and island communities in particular, experience higher costs of living for some goods and services.[103] A Scottish Government report shows that additional minimum living costs for households in remote rural Scotland typically add 15-30% to a household budget, compared to urban areas of the UK.[104]

Rural households tend to spend more on transport costs and so will be more adversely affected by the increase in fuel prices - in 2019, rural households in Scotland spent, on average, £135 per month on fuel compared with £107 for urban households (26% more).[105]

Energy Action Scotland recently reported that fuel poverty levels in the Western Islands and Highland Council areas are the worst in Scotland.[106] In recent months, fuel prices[107] have increased substantially not just for gas and electricity, but also for liquid fuels, more commonly used in off-gas-grid areas.

Approximately 100,000 off-gas-grid households were considered to be in fuel poverty in 2019, representing a fuel poverty rate of 34%, above the national rate of 24.6%. This is likely to have risen with rising costs.[108] The vast majority (250,000 out of 280,000) of off–gas-grid households live in island or rural communities and use fuel such as oil, gas canisters or solid fuels. The recent cost increases in heating oil prices are likely to see more households fall into fuel poverty.

The 2019 Scottish House Condition Survey found that 8% of homes in Scotland did not use mains gas or electricity for heating, with 5% of homes using oil as their primary heating fuel[109]. In their advice to the Scottish Government on the cost of living crisis in August 2022, the Poverty and Inequality Commission state that prices of oil have continued to rise and there is no regulation of off-grid fuel costs such as oil and LPG, although many suppliers are signed up to industry body codes of conduct. The lack of regulation means that there is no price cap and price rises can be passed on to consumers more frequently. Those who use off-gas-grid fuel need to pay upfront, and normally for a fixed minimum amount to guarantee delivery (e.g. for oil this is 500 litres, which currently equates to over £500). Prices are very volatile and can change daily, and between making an order and getting delivery.[95] Fuel prices will need to be monitored to see whether the price of heating oils not covered by the Energy Price Guarantee continues to rise after October 2022 or whether they stabilise alongside gas and electricity prices paid by households.

All households connected to mains electric will receive the £400 energy bill discount announced in May, and almost all households in Scotland have a connection to the electricity grid [110]. However, the Poverty and Inequality Commission state that, as this is applied to electricity accounts, it is of limited help to households struggling to afford to buy oil or other fuel (and that this may be a particular issue for households just above the benefits threshold who are not entitled to any other support).[111]

BEIS announced further detail on energy price guarantee for households on September 21 targeted at some rural households/people using off-gas grid fuel. An additional payment of £100 will be provided to households across the UK who are not able to receive support for their heating costs through the Energy Price Guarantee to compensate for the rising costs of alternative fuels such as heating oil and to compensate off-grid consumers. However, it seems unlikely that £100 will meet the price increases of heating oil and LPG costs seen in the past few months.

Households with a Disabled Person

Households with one or more disabled people are more likely to be in poverty. 23% of people in households with a disabled household member were in relative poverty after housing costs in 2017-20, compared to 17% of people with no disabled household members.[98] The percentage of net income spent on housing, fuel and food is higher for households with a disabled household head.[73] Food insecurity is also more common among adults with a limiting longstanding illness (18%).[112]

Disabled people often use more energy, as many need to keep heating on for medical reasons, or use electricity to charge essential equipment such as mobility aids.[113] Many disabled people have needs which mean that economising on energy can bring severe hardship.[99]

There are high levels of concern about the cost of living crisis amongst disabled people. Recent data from Scotland show that nearly one in four families (23%) where someone is disabled are behind on at least one bill or payment and 4% are behind on three or more.[101] Findings from Disability Equality Scotland's weekly poll on the cost of living crisis show that (for week beginning 18 April 2022) 85% of participants were very concerned about the current cost of living.

Disabled people (receiving qualifying disability benefits) were given an additional £150 as part of the Cost of Living Support Package. However, this will not cover the additional cost of inflation applied to disability-related benefits. For example, on UC, the supplement for someone unable to work or engage in work-related activity rose by around £240 a year less than if it had been CPI-uprated. Similarly, someone receiving the daily living component of PIP is worse off by £185 on the standard rate and £274 on the enhanced rate, as a result of sub-inflation upratings.[99]

Organisations representing and supporting disabled people report that many face above average energy costs associated with their particular disability. The UK government's Cost of Living Support Package provides a flat payment of £150 to disabled people and does not distinguish between disabled people on the basis of additional needs meaning that for many people it is insufficient.[114]

In their advice to the Scottish government in June, the Poverty and Inequality Commission identified disabled people who faced higher energy costs, but were not on low income benefits as one of the groups who missed out under the May Cost of Living Support Package.[111]

Households who Rent Their Homes

Households in the rented sector are more likely to be financially vulnerable than households in other tenures. This reduces their ability to cope with rental increases and other inflationary shocks.[115]

Housing costs have also been a contributor to increases in the cost of living, with private housing rental prices in Scotland increasing by an annual 3.6% in August 2022, compared with 1.0% in March 2021.[116] It is estimated that between 15% and 35% of tenants who have been in their properties for more than 1 year could have faced a rent increase during the initial 6 month period that the Cost of Living (Tenant Protection) Scotland legislation will be in force.[117]

JRF find that of those on low incomes across the UK, 75% of private renters and 73% of social renters are going without at least one essential, compared to 39% of those who own their homes outright.[76]JRF's more recently published Poverty in Scotland 2022 found that renters in Scotland were at a higher risk of arrears, with around one in three renters being behind on one or more bills, and that renters feel more financially insecure than homeowners.[101]

Citizens Advice Scotland have reported that advice to renters (either social or private) about threatened homelessness due to possession action has increased by 17% between April to June 2021 and April to June 2022, while queries about private sector rents as a proportion of all private rented sector queries has increased by 28% across the same time period.[118]

Households in the rental sector are also more likely to be in fuel poverty. Under the energy price guarantee it is estimated that around 54% of households in the social rented sector and 48% in the private rented sector will be in fuel poverty. By comparison it is estimated that 24% of owner occupiers will be fuel poor.

Details on the impacts households who rent their homes privately and social renters, can be found in Annex 2.

BEIS announced further detail on the energy price guarantee for households on September 21 that will benefit some renters. From 1 October 2022, the £400 Energy Bills Support Scheme (EBSS) discount will now be available to the 1% of households who did not previously receive it such as park home residents and tenants whose landlords pay for their energy via a commercial contract. The UK government intends to introduce legislation that will ensure landlords pass the EBSS on to tenants who pay all-inclusive bills.

Gypsy/Travellers

Among Gypsy/Traveller communities, low incomes, poorly insulated accommodation and the way some members of the community pay for their energy, mean that fuel poverty can be a particular issue, with feedback suggesting that some existing accommodation is cold, difficult to heat and prone to condensation.[119]

The Charity Friends, Families and Travellers recently highlighted the high prices of heating mobile accommodation with gas cylinders or generators, and raised concerns that travelling households in park homes may not be individually eligible for the UK government scheme of £400 support towards energy bills.[120]

However, BEIS announced further detail on energy price guarantee for households on September 21 that may support Gypsy/Travellers. From 1 October 2022, the £400 EBSS discount will now be available to the 1% of households who did not previously receive it such as park home residents and tenants whose landlords pay for their energy via a commercial contract.

Conclusion

All households are now reporting an increase in their cost of living. This chapter has outlined how low income households and those with particular characteristics are likely to be most negatively affected by increases in the cost of living. Chapter 6 outlines how this is likely to lead to worse health outcomes for these groups and increase demand for public and third sector services.

This chapter presents a summary of current evidence on the characteristics of low income households most negatively affected by the cost of living crisis. As new evidence emerges it will be important to re-appraise this assessment. For example, mortgage interest rates have been rising, with particularly sharp increases in recent weeks following the UK Government's mini-budget. Around 85% of households with mortgages in the UK are on fixed rate deals[121] and these households will currently have some protection from the increased monthly mortgage payments, as will private rented households following the passage of the Cost of Living (Tenant Protection) Scotland legislation. However, home owners on variable rates, as well as home owners whose fixed rate deals expire in the coming months, may face very large increases in mortgage payments.

Whilst an additional £650 of the UK Government Support Package announced in May was targeted towards low income groups on means-tested benefits it falls short of fully compensating them for rising costs.[99]

The September Energy Price Guarantee was untargeted and low income households will struggle to meet rising energy costs which have more than doubled over the last year.

The UK Government's one-off payments are inadequate in addressing the needs of these families and do not reflect the different levels of need within the benefit system or different levels of energy usage. These payments also fail to adequately support particular households, for example larger families, disabled people with above average energy costs due to the nature of their disability and households who marginally fail to qualify for benefits and are not supported by social security.

The low income groups highlighted within this chapter are similar to those identified within the Covid Recovery Strategy[80], such as women, disabled people and people from minority ethnic groups who have been disproportionately affected by Covid-19.[122] There is also significant overlap with the priority family types identified within the Child Poverty Delivery Plan[123].

Contact

Email: socialresearch@gov.scot