The Cost of Living Crisis in Scotland: analytical report

This report draws together analysis from a wide range of sources to provide an overview of emerging evidence on the cost of living crisis. It has been produced by a cross-government group of analysts.

Chapter 1: Inflation in Context

Introduction

This chapter provides an overview of the latest data on inflation, projections for the economic outlook for the UK and comparisons of the current economic situation with previous periods of high inflation.

Trends in inflation

Economic conditions have rapidly deteriorated since the start of 2022 at a global and domestic level. The war in Ukraine has interrupted the gradual recovery from the pandemic, causing an energy supply and inflationary shock that is expected to push the economy into recession.

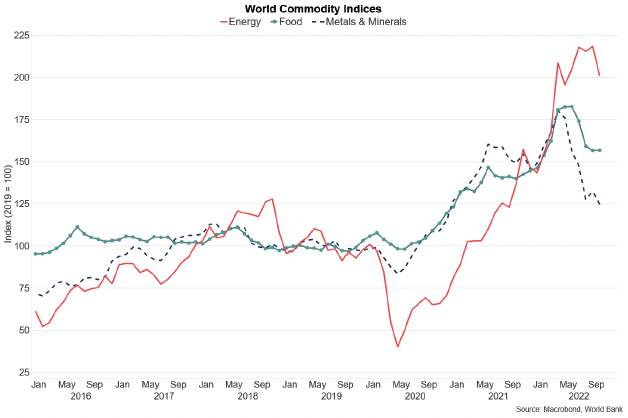

These inflationary pressures were initially expected to be largely temporary as the economy adjusted to post-pandemic conditions. However, the war in Ukraine at the start of 2022 has exacerbated and further destabilised recovery on the supply side, placing further significant upward pressure on international commodity prices across food, metals and particularly energy. While commodity price rises across food, metals and oil have eased slightly in recent months (though remain significantly higher than their levels last year), wholesale energy prices, particularly gas, have remained particularly elevated and volatile (see Figure 1).

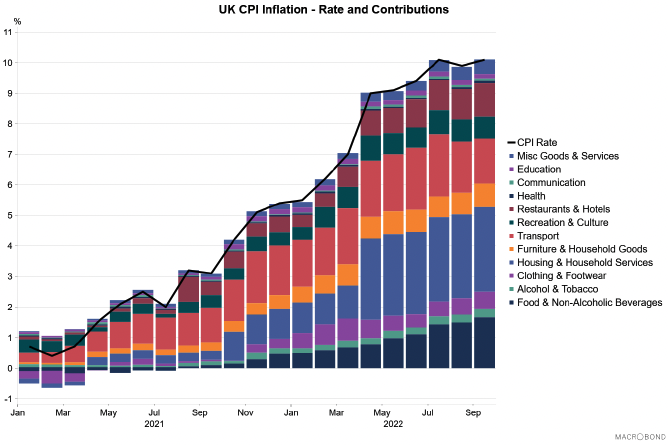

As Figure 2 illustrates, UK inflation has risen sharply over the past year from 0.5% in February 2021 to its current rate of 10.1% in September 2022 – its joint highest rate since the early 1980s.

The rise in inflation has been predominantly driven by increases in the price of electricity, gas and other fuels, up 70.1% over the year to September, driven by the increase in wholesale gas prices, however rising food prices particularly drove the increase in the rate between August and September.

Inflation remains elevated internationally. In September inflation increased in the Euro Area (9.1% to 9.9%) and fell marginally in the US (8.3% to 8.2%).

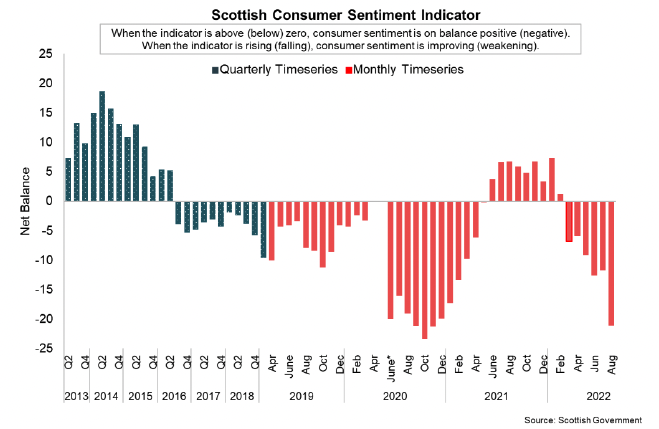

One of the implications of rising inflation is to squeeze household finances. This feeds through to weaker consumer demand and in turn leads to lower demand for goods and services from businesses, particularly in consumer facing sectors of the economy (see Chapter 4). Demand in the economy is weakening - consumer sentiment has fallen sharply since the start of the year and in August 2022 was at its lowest level since November 2020 during the pandemic (consumer sentiment measure is a combination of sentiment on economic outlook, household financial security and how relaxed households feel about spending money (see Figure 3).[3]

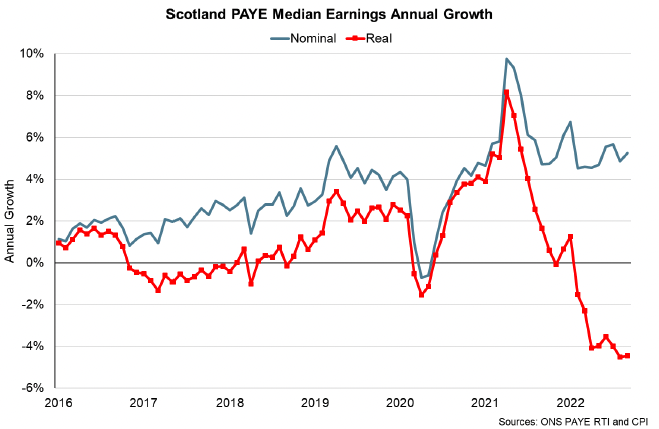

The effects of rising inflation on household budgets is further reflected in its impact on real earnings. As Figure 4 illustrates, while nominal median PAYE earnings grew 5.3% over the year to September, they fell 4.4% in real terms once adjusted for inflation; the eighth consecutive month of decline.

The growth in nominal earnings partly reflects the ongoing tightness in the labour market. Unemployment in Scotland is at a near record low of 3.3% in the 3-months to August 2022, while vacancy rates remain elevated with 42% of firms reporting a shortage of staff into the start of September, placing upward pressure on pay settlements.

Interest rates and the outlook for inflation

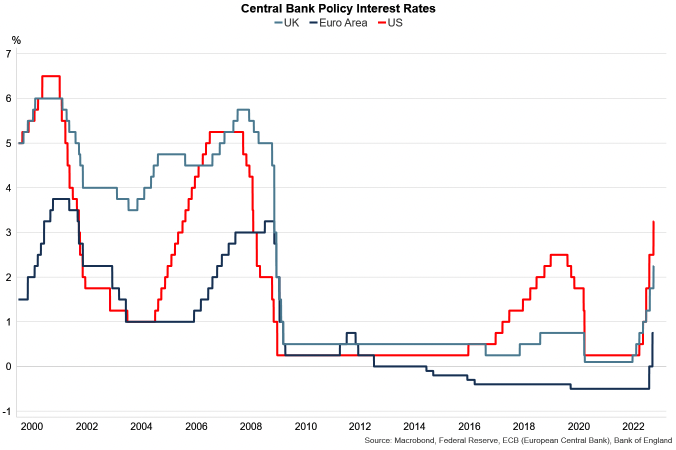

To help to bring inflation back to its target of 2%, the Bank of England's Monetary Policy Committee has implemented seven consecutive increases in the Bank Rate since December 2021, taking it from 0.1% in December 2021 to 2.25% in September 2022, its highest rate since 2008, as shown in Figure 5. Other central banks have also been increasing interest rates. For example, the US Federal Reserve announced a fifth successive rate rise in September, increasing its federal funds rate by 0.75 percentage points to a target range of 3% – 3.25%, while the European Central Bank raised interest rates by 0.75 percentage points to 0.75%.

At the start of August 2022, the Bank of England forecast inflation to reach 13% in Q4 2022, leading to a squeeze in real household incomes, with real post-tax income falling by 1.5% in 2022 and a further 2.25% in 2023, one of the largest sustained falls in real incomes since records began. These forecasts reflected UK Government policy announcements at the time.

Since then, the fiscal expansionary measures announced in the UK Government Growth Plan, many of which have subsequently been reversed, are expected to have material implications for the economic outlook and public finances. It remains unclear how the remaining tax cuts will be funded and the extent to which public expenditure cuts will be forthcoming. The Office for Budget Responsibility are scheduled to publish its forecasts on 17th November alongside the UK Government's Medium Term Fiscal Plan.

The increased scale of uncertainty and risk in the economic outlook has been reflected in significant financial market volatility in September and October, with a sharp rise in UK government bond yields requiring the Bank of England to commence temporary purchases of long-dated UK government bonds to restore market functioning and reduce wider risks to UK financial stability.

The introduction of the Energy Price Guarantee (described in Chapter 3) is expected to reduce the extent to which inflation will rise in the short term. The Bank of England expect inflation to peak at just under 11% in October, however remain above 10% over the next few months due to the increase in energy prices already embedded.

The extent to which the policy will mitigate energy price inflation in the economy is uncertain beyond its scheduled 6-month review in April 2023. The overall level of uncertainty around the path for inflation is high and will continue to be influenced by the monetary and fiscal policy response[4]. Despite the risk of recession, monetary policy is being tightened by central banks, as they seek to address underlying inflationary pressures and to reduce the risk that they become embedded more widely in the economy and persist for longer. The Bank of England will publish their next Monetary Policy Report and forecasts on 3 November.

Comparison with previous periods of high inflation

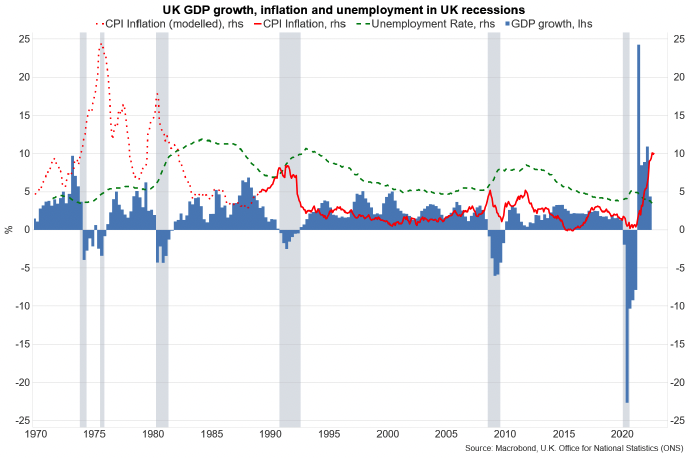

Comparisons with periods of higher inflation and economic downturns can be made to draw key similarities and differences. Figure 6 below shows previous UK recessions denoted by the grey bars. These periods were in the mid 1970s, early 1980s, early 1990s, 2008/09 (global financial crisis) and 2020 (pandemic).

Figure 6 also illustrates that rising inflation and falling output is a similar pattern to the recessions of the mid 1970s, early 1980s (particularly the link to energy price volatility) and early 1990s. There are important differences between the current economic situation and previous recessions. For example, the Bank of England expect inflation to peak at just under 11%. This is higher than its peak in the early 1990s (c.8%), but is notably below the peak inflation rates of the mid 1970s (c. 25%) and early 1980s (c.18%). Unemployment is currently at a record low rate and is forecast to rise to slightly above 6% in 2025, but remain below the +10% rates of the 1980s and early 1990s.

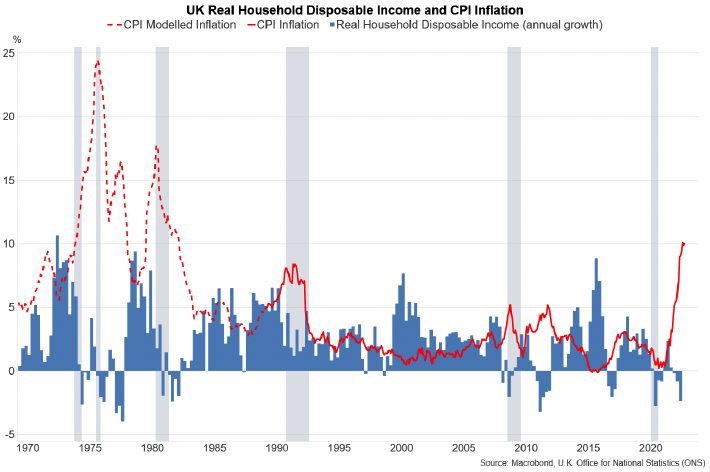

Periods of higher inflation have tended to result in periods of falling real disposable household income (the amount of money that individuals in the household sector can spend or save after income distribution measures and adjusted for inflation), as Figure 7 illustrates. This was evident in the 1970s and early 1980s. The rise in inflation in the early 1990s and recession saw household disposable income growth slow but remain positive. Compared to periods of high inflation in the 1970s and 1980s, changes to labour market structure means there is less scope for wages to keep pace with inflation and for a subsequent wage price spiral.

Conclusion

The war in Ukraine has led to elevated energy prices and high rates of inflation: as at September 2022 UK inflation was 10.1%. The Bank of England forecast for inflation is to peak at just under 11% in October 2022 and remain above 10% over the following few months, before starting to fall back. If this transpires then inflation would be higher than in its peak in the early 1990s (c.8%), but notably below the peak inflation rates of the mid 1970s (c. 25%) and early 1980s (c.18%). These forecasts predate the full range of developments since the UK Government Growth Plan in September (see Chapter 3), the reversal of many of its announcements and the period of significant market volatility. As with previous periods of high inflation, the current high rate of inflation will lead to falling real disposable household incomes. In turn this will feed through to weaker consumer demand in the economy and lower consumption.

Contact

Email: socialresearch@gov.scot