Welfare reform - impact on households with children: report

A report that presents analysis of the impacts of UK Government reform on households with children in Scotland.

Part of

3 The £20 uplift and changes to the Universal Credit earnings taper rate and work allowances

Background

We first assess the impact of reforms that have taken place during the COVID-19 pandemic.

The £20 uplift

At the outset of the COVID-19 pandemic, the UK Government temporarily increased Universal Credit standard allowances and the basic element of Working Tax Credits by £20 per week, increasing the disposable incomes of households on these benefits. This, alongside the 'furlough' scheme, was the primary way in which the government supported those who were unable to work, or saw reduced earnings, as a result of COVID-19. The uplift also helped those who were already claiming for these benefits before the pandemic, including those who are unable to work due to disability or caring responsibilities.

The UK Government removed this temporary measure in October 2021. A Scottish Government report found that withdrawing the uplift would have a particular impact on poorer households, including those with children.[9] Meanwhile, people on other legacy benefits, such as Employment and Support Allowance, did not receive the uplift in the first place.

We model the impacts of reinstating the uplift. However, the uplift was intended to be temporary, so this reinstatement would represent a permanent addition to the social security system, not just the reversal of a reform.

The earnings taper rate and work allowances

In the UK Government's Autumn 2021 budget, two significant changes were made to Universal Credit for households in employment.

The Universal Credit award that households are entitled to is partly determined by their earnings. Some households, including those with children, have their award partially protected by a work allowance. Above the work allowance, Universal Credit awards are gradually reduced at a fixed proportion of earnings, known as the taper rate. If there was no taper, there would be a 'cliff edge' where Universal Credit would be fully withdrawn once a household earned more than a certain amount.[10]

In the UK's Autumn budget of 2021, work allowances were increased by £500 per year (£42 per month) meaning that households could earn an additional £500 before their Universal Credit award began to reduce. At the same time the taper rate was reduced from 63% to 55%, meaning that each pound of earnings above the work allowance would reduce the Universal Credit award by 55p rather than 63p.

| 2023-24 | Before | After |

|---|---|---|

| Earnings taper rate | 63% | 55% |

| Monthly work allowance[11] | £551/£313 | £593/£355 |

Both of these reforms can be expected to boost income for Universal Credit claimants in work and to improve work incentives. However, these impacts are complex, particularly when interacting with the withdrawal of the £20 uplift, and the long-term behavioural effect is uncertain.

Despite this reform generally increasing household incomes, this report assesses the impact of reversing the reform rather than its implementation, in line with our treatment of the other policies considered. This means that it can be assessed on a like-for-like basis with other policies, and that the cumulative impact described later is a fair reflection of UK Government policy over the past six years.

Expenditure

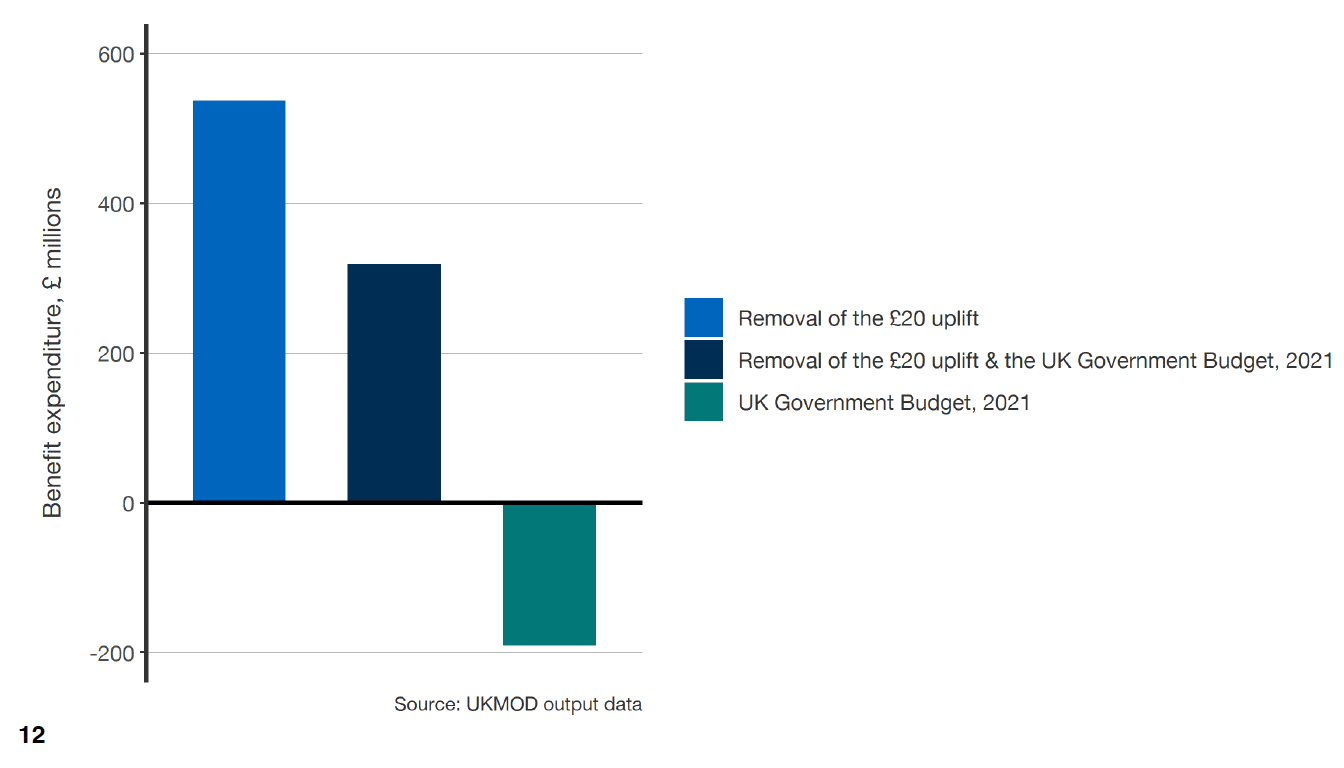

As shown in the graph (figure 3.1), the total cost of reversing recent reforms to Universal Credit would be around £320 million per annum in 2023-24. This is a net figure, with the cost of reversing the removal of the uplift (£540 million) offset by the reduction of the taper rate (£190 million).

These figures include both expenditure made by the UK Government on reserved benefits such as Universal Credit and by the Scottish Government on devolved social security such as the Scottish Child Payment. Further detail is provided in Appendix A, where the implied reduction in expenditure made by the UK Government on households in Scotland is illustrated.[13]

The change in expenditure which would result from reversing both policies at once does not equal the sum of the figures for reversing each of the two policies in isolation. This is a result of the interactions between the two policies, as illustrated in the household example below.

Household example: The Munro household has no Universal Credit award as their earnings have "tapered away" their entitlement to exactly £0. If the £20 uplift was reintroduced, the Munros would now have an award, but would only keep £9 of the uplift due to the 55% earnings taper rate. If the taper rate were higher, at 63%, this would drop further to only £7.40.

Had there only been an increase to the taper rate, there would have been no impact on the Munro household as their award was already £0. It only has an impact when introduced in tandem with the reintroduction of the £20 uplift.

Disposable income

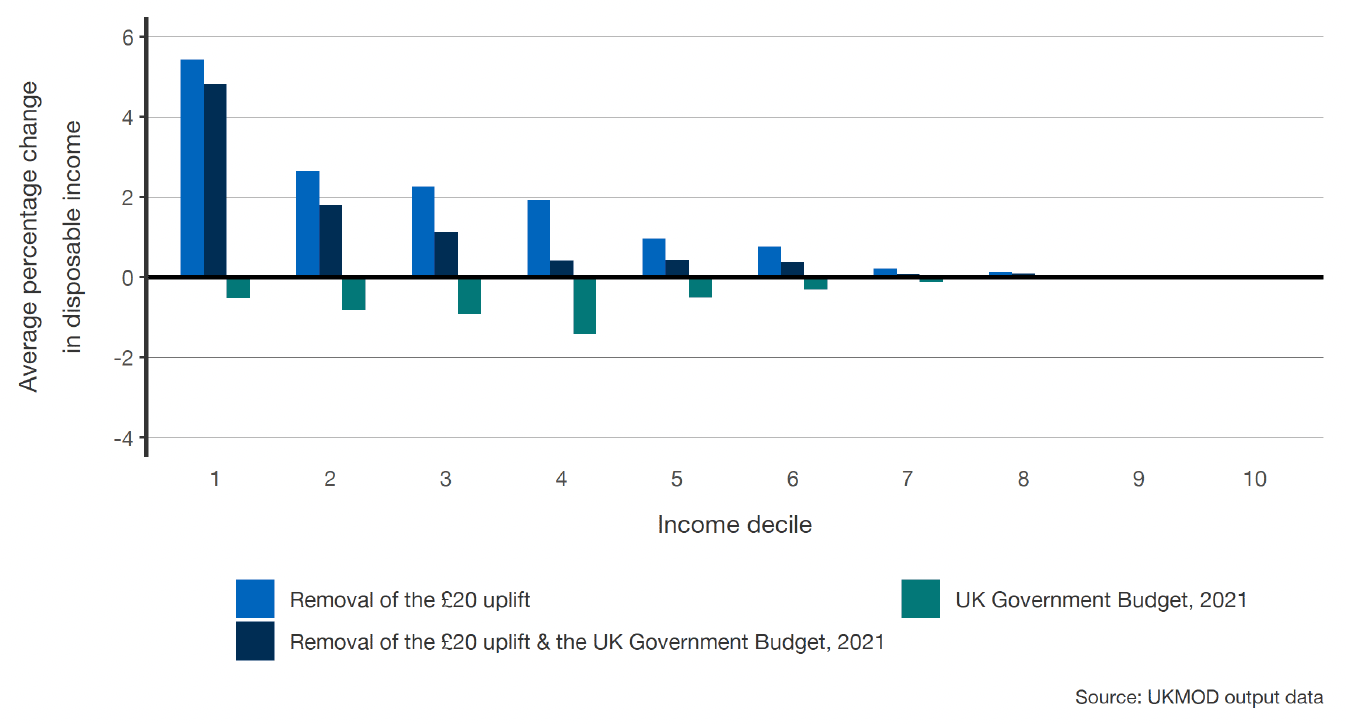

As shown in the graph (figure 3.2), reinstating the £20 uplift would have most impact on those in the lowest disposable income deciles, with the 10% of people in households with lowest incomes seeing increases of around 5% on average. [14]

However, reverting the earnings taper rate to 63% (from 55%) and reversing the increases in work allowances would primarily impact those with relatively higher incomes. As a result, the impact of reversing the £20 cut is significantly mitigated for those in deciles three and four should both reforms be reversed.

Depending on the median income in 2023-24, all households in income deciles one and two and most in decile three will be in poverty. The cumulative impact of reversing both reforms would have a significant positive impact for these households, on average, but some households may experience a negative impact if their household composition and earnings make them more sensitive to the budget measures than to the £20 uplift. Indeed, the poverty rate is highly sensitive to changes in the taper rate and work allowances as they primarily impact on people on or just above the poverty line.

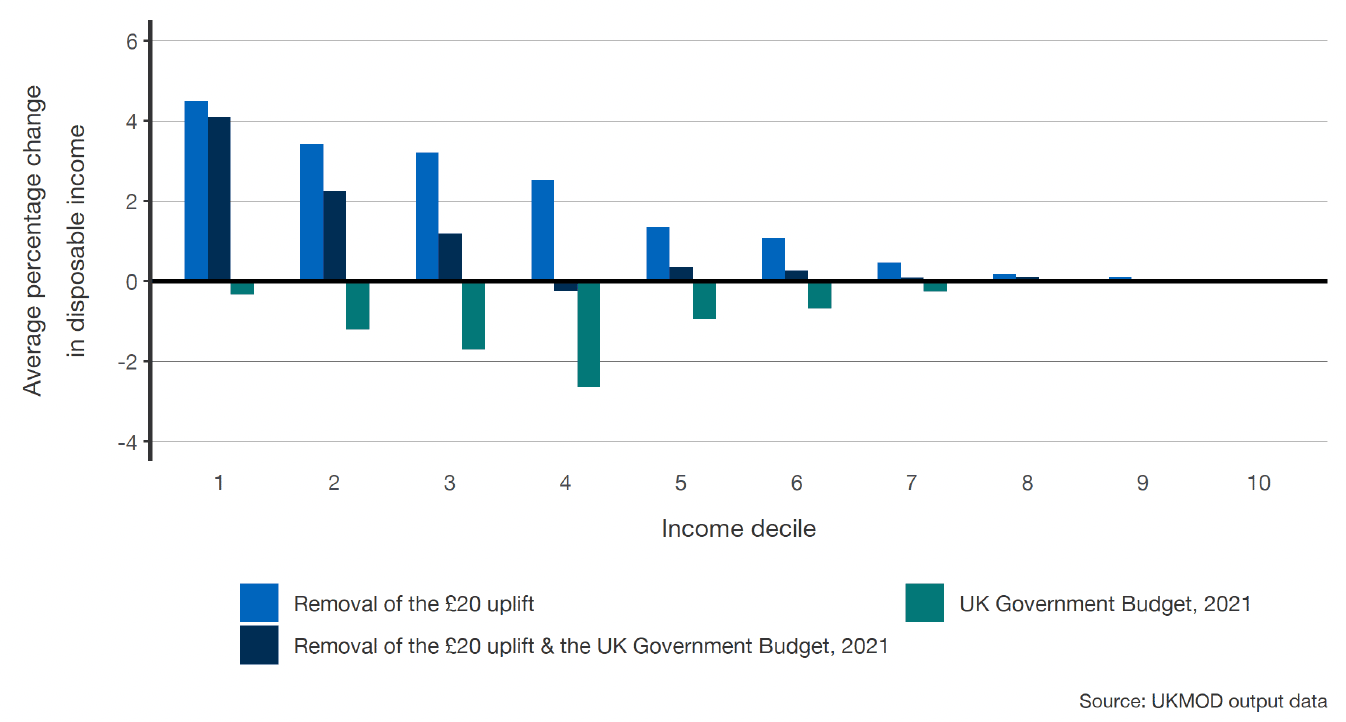

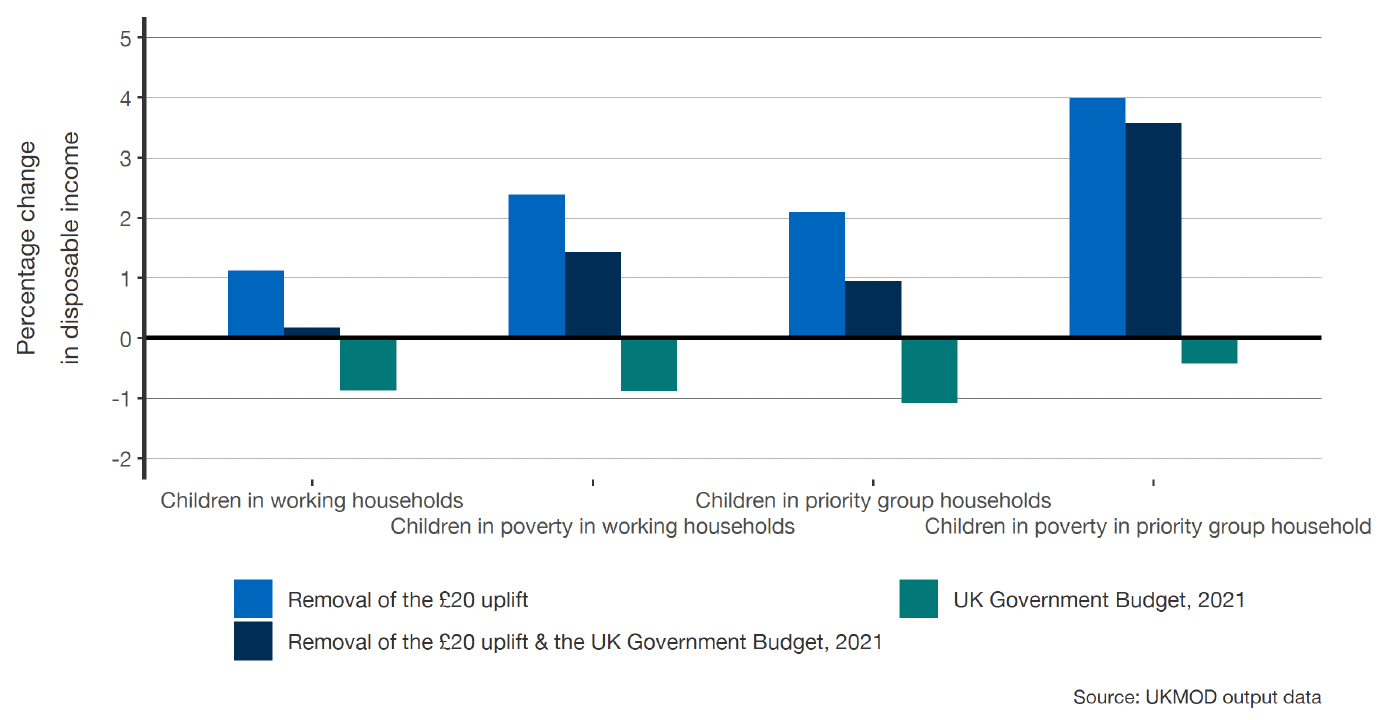

Figure 3.3 demonstrates that reversing the removal of the £20 uplift would have a reduced impact on people in households with children in income decile 1 compared with people generally. However, in all other deciles the impact is greater, demonstrating that households with children in these deciles are more likely to receive Universal Credit or working tax credit.

Reversing the work allowance and taper rate changes in the UK Budget of 2021 would have a more significant impact on families compared with all households. This demonstrates that the incomes of people in lower income deciles and in households with children tend to be more sensitive to earnings-related reform, with people out-of-work more likely to have no children. For those households with children in decile four, the impacts of reversing both reforms would cancel out.

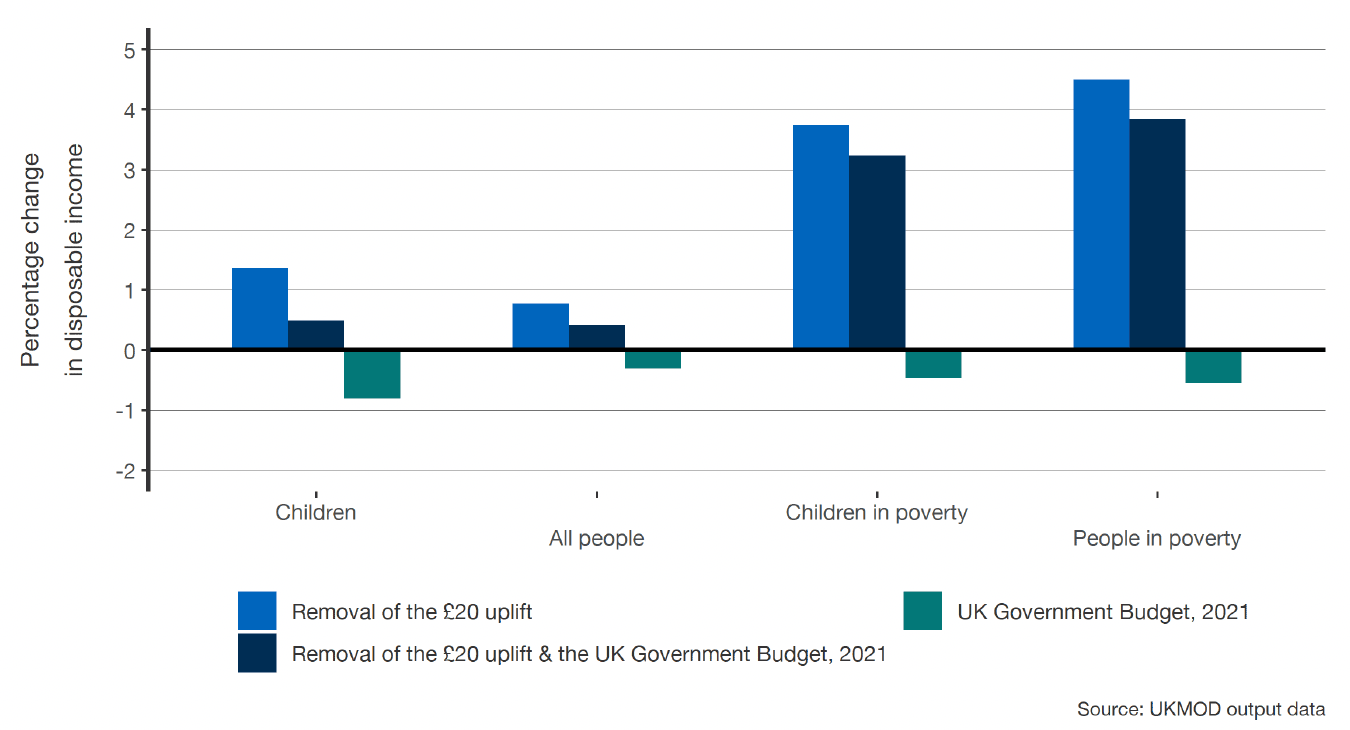

Figure 3.4 shows how reversing either of these recent reforms will have a marginal impact on disposable income on average. However, there will be a significant change for people under the poverty line in 2023-24 if the £20 uplift were reversed.

Despite how sensitive poverty rates are to changes in the Universal Credit earnings taper rate, this graph shows that, on average, the taper rate change has little impact on disposable income. As shown in the graph below (figure 3.5), this is the case even for working households, with the £20 uplift more important. There is not necessarily a clear cut relationship between policies that are effective in helping people who in poverty and policies that are effective in moving people out of poverty, since the latter depends on the proximity of households to the poverty line.

Poverty

The cumulative impact of reversing recent welfare reforms would be to reduce poverty in 2023-24. The table below (figure 3.6) shows how the removal of the £20 uplift more than offsets the positive impact of the 2021 Budget reforms, which only had a minor impact on poverty rates.

| Removal of the £20 uplift | UK Government Budget, 2021 | Both | |

|---|---|---|---|

| All people | -1 | * | -1 |

| Children | -1 | * | -1 |

| People in working households | * | * | * |

| Children in working households | * | 1 | * |

| Children in single households | -2 | * | -2 |

| Children in couple households | * | * | * |

| Children in priority group households | -1 | * | -1 |

| People in absolute poverty | -1 | * | -1 |

| Children in absolute poverty | -2 | * | -1 |

Reversing the removal of the £20 uplift would have a significant impact on the poverty rate for children in single adult households and on the absolute poverty rate for children. We also find that the absolute poverty rate for children is more sensitive than the relative poverty rate.

| Removal of the £20 uplift | UK Government Budget, 2021 | Both[17] | |

|---|---|---|---|

| All people | 30,000 | -10,000 | 30,000 |

| Children | 10,000 | * | 10,000 |

| People in working households | 10,000 | -20,000 | 10,000 |

| Children in working households | * | * | * |

| Children in single households | 10,000 | * | * |

| Children in couple households | * | * | * |

| Children in priority group households | 10,000 | * | * |

As mentioned above, the change to the earnings taper rate and work allowances has a large impact on those near to the poverty line. The table above (figure 3.7) shows that 10,000 people in working households would be moved into poverty should it be reversed in 2023-24.

Reinstating the £20 uplift to Universal Credit would move 30,000 people out of poverty, including 10,000 children. The change would particularly affect the number of children in single households in poverty.

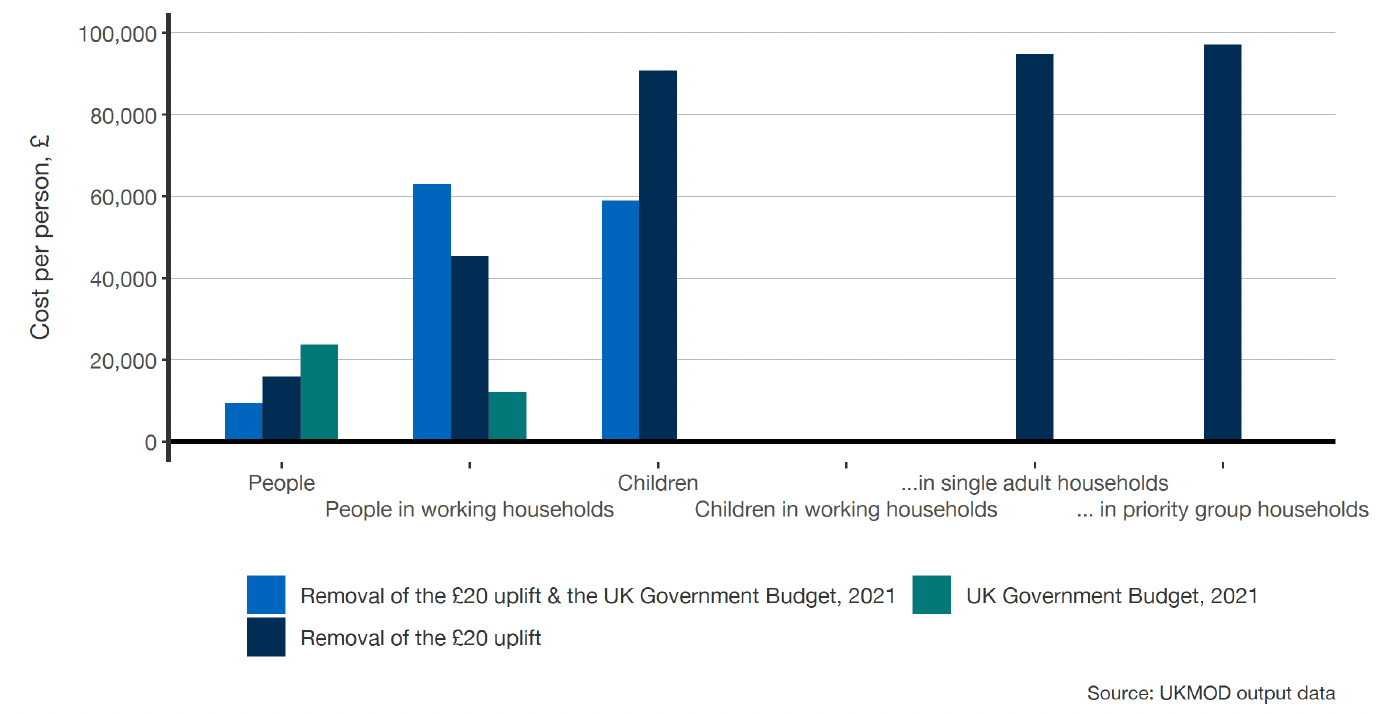

We can combine our analysis of additional expenditure and poverty rates to find which policies are most cost-efficient for moving people above (or below) the poverty line. As shown in the graph (figure 3.8), reversing the removal of the £20 uplift and the 2021 budget measures would cost less than £10,000 per person taken out of poverty, with a cost-efficiency gain by reversing both policies together.

Given the lower number of people in working households and children, it generally costs more to bring them out of poverty. However, the graph does show that the budget was highly cost-effective for bringing people in working households out of poverty; for other groups, such as children in single adult households, reversing both reforms tends to be the most efficient way to reduce poverty.

Given the interactions between the policies and the non-linear income distribution of households in Scotland, no inference can be drawn about the cost-effectiveness of a partial reversal of the reforms (for example, a £10 uplift to Universal Credit).

There are a number of types of household, such as children in working households, where few people were brought in or out of poverty. These results have not been included in the chart, and demonstrate where reversing the reform would have no discernible impact on poverty rates for that group.

Household example: The Corbett household is a working household with children. They are among a small number of families for which the change to the work allowance and the earnings taper rate has lifted them out of poverty. A similar number of working families with children, including the Grahams, would also be lifted out of poverty if £20 uplift was reinstated.

If the uplift was reinstated but the earnings reforms reversed, there would be a small but similar number of working families with children moving above and below the poverty line, despite a significant increase in government expenditure.

Work incentives

There are several mechanisms through which an increase in earnings does not translate one-for-one into an increase in disposable income, including income tax, National Insurance contributions, and the withdrawal of benefit payments.

The possible combined tax rate could be over 85%, depending on which income tax bands apply to working household members. At some earning increases, such as when they bring a household out of eligibility for Universal Credit and thus other benefits such as the Scottish Child Payment, the marginal tax rate could extend above 100%.

Household example: The Graham household has one child. Their earnings mean that their Universal Credit award is small, but they are still entitled to the Scottish Child Payment.

The household decides to change their working patterns to earn an extra £100 per week. They pay income tax of £21 and National Insurance of £13.25 on this additional earnings. Furthermore, what remains of their weekly Universal Credit award, £55 per week, is fully tapered away. Now ineligible for the Scottish Child Payment, they lose an additional £25 per week (in 2023-24).

On balance, the Graham household is worse off after increasing their earnings, with an effective tax rate of 109%. However, the effective tax rate for the next £100 of earnings is only 34%.

To explore this impact of policy reform on marginal tax rates, we have developed a number of illustrative households. These households are set out in detail in Appendix D.

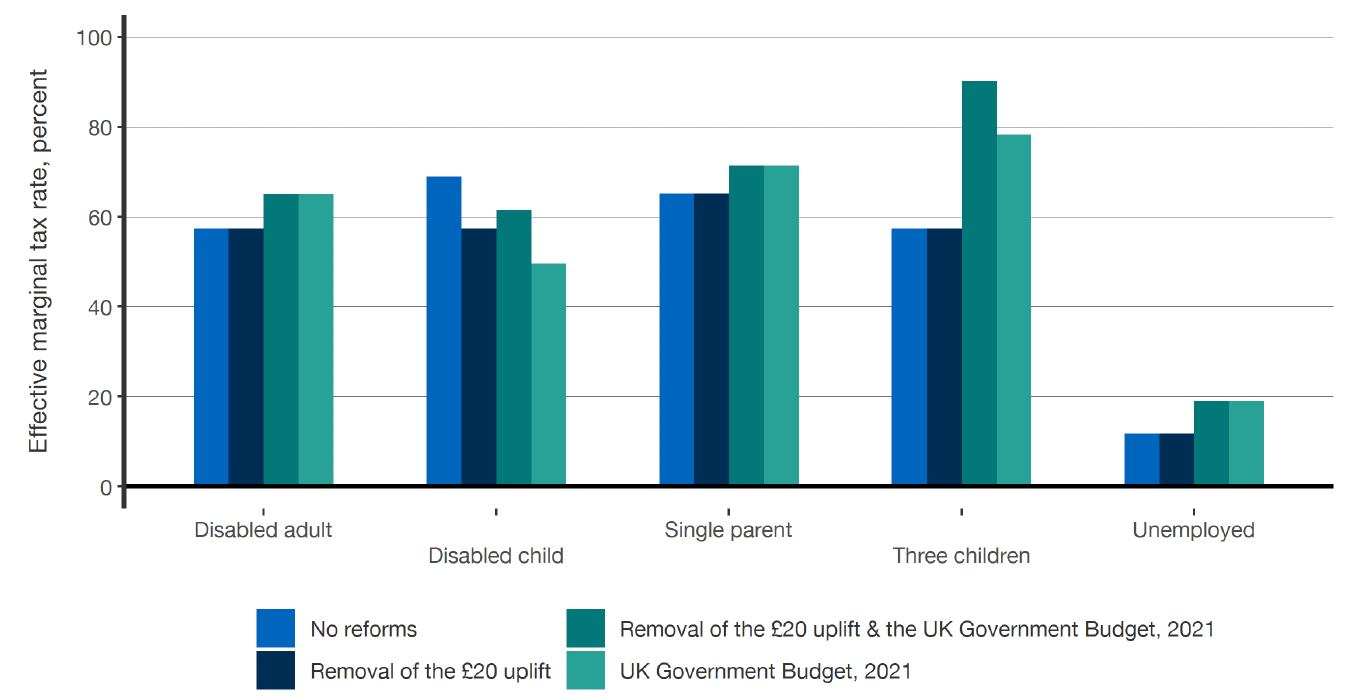

The graph above (figure 3.9) demonstrates that for some households the effective marginal tax rate is above 50%. It shows how reversing the change to the Universal Credit earnings taper rate from 63% to 55% and the work allowance would further increase the effective tax rate for most households.

However, for some households (disabled child, in this instance) the effective marginal tax rate will actually decrease as a result of reversing the change to the earnings taper rate. This is because they now have a larger Universal Credit award, and thus more of their earnings would be offset by the reduction of this award through the taper rate. This perverse outcome only affects households with smaller awards for which earnings reduces their award to zero.

For most working households with earnings over £10,000, changes to the taper rate represent only a small adjustment to the effective tax burden as at this threshold they also begin to pay income tax and National Insurance contributions.

For the unemployed household with children considering work, only compulsory workplace pension contributions and the earnings taper rate reduce disposable income. This is because their earnings would remain below the income tax and national insurance contribution allowances.

Contact

Email: spencer.thompson@gov.scot