Scottish Housing Market Review: Q3 2022

Scottish housing market bulletins collating a range of statistics on house prices, housing market activity, cost and availability of finance and repossessions

Part of

6. Mortgage Interest Rates

In March 2020, Bank Rate was cut by a total of 65 basis points to 0.1% as a result of the Covid-19 pandemic. More recently in response to the rise in inflation, the Bank of England has increased the Bank rate by 15 basis points in December, followed by 25 basis points in February, March, May and June and by 50 basis points in August and September for a cumulative rise of 215 basis points to 2.25%, returning Bank Rate to its highest level since 2008.

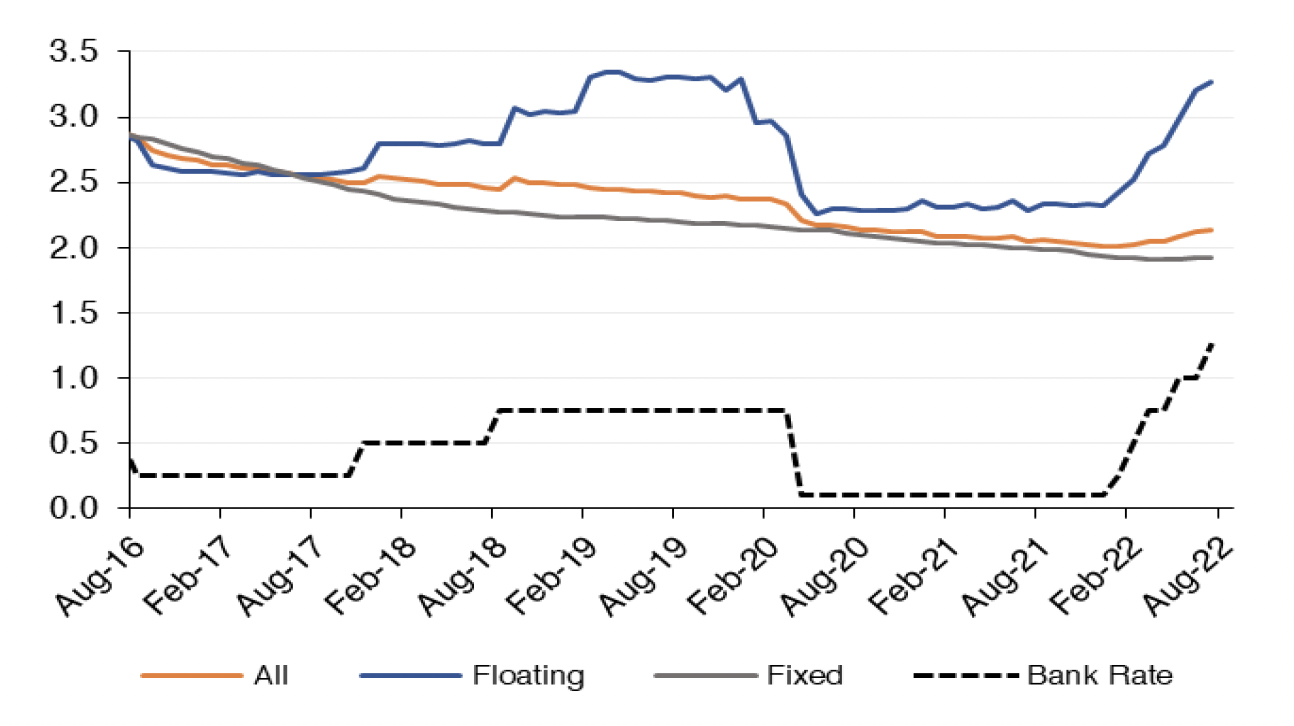

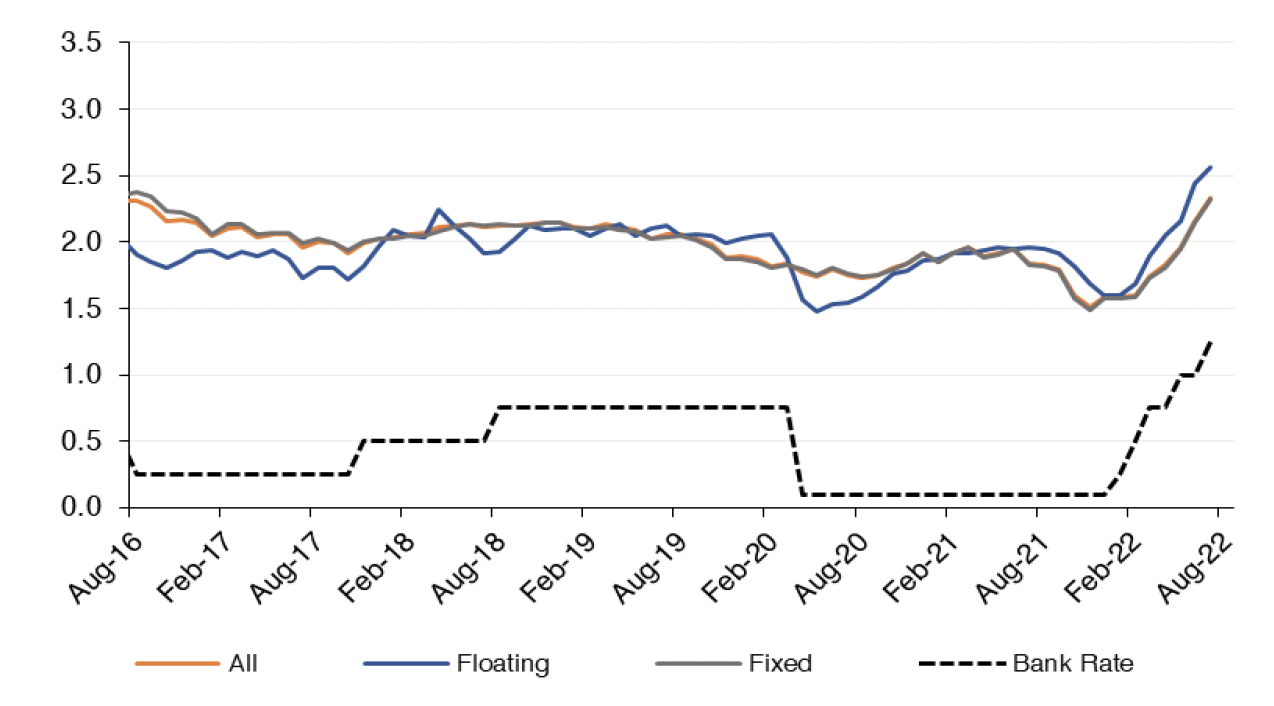

Chart 6.1 and Chart 6.2 show data on the effective (or average) interest rates on outstanding mortgage balances and new mortgage advances, which are available up to August 2022. (Source: BoE). From December 2021 to August 2022, the increases in mortgage rates were below the cumulative 165 basis point increase in Bank Rate during this period: the average variable rate on outstanding mortgages increased by 119 basis points to 3.51%, the average variable rate on new advances increased by 117 basis points to 2.77%, and the average fixed rate on new advances increased by 97 basis points to 2.55%. The average fixed rate on outstanding mortgages was in fact little changed over this period, since even though interest rates on new deals were increasing, they were not above the rates on fixed rate deals which expired during this period.

Effective Monthly Mortgage Interest Rates (UK)

Source: Bank of England

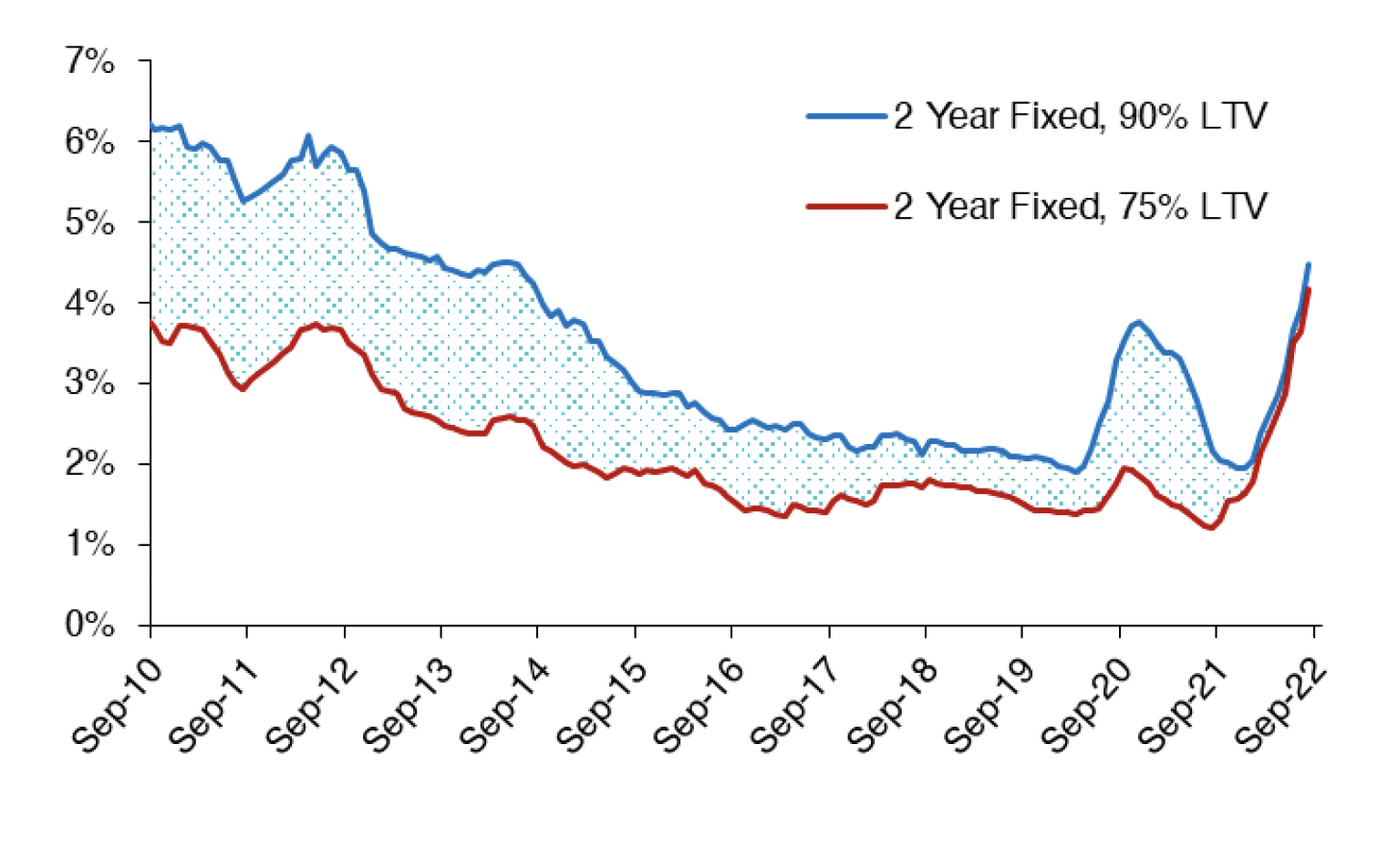

It should be noted that Bank of England data on effective mortgage interest rates (i.e. the average rate on actual lending) does not include the impact of the 50 basis point increase in the Bank Rate on 22 September, as well as the UKG Growth Plan/mini-budget on 23 September which led to significant volatility in interest rates. More recent Bank of England data on advertised mortgages rates, illustrated in Chart 6.3, shows that over the month of September the average advertised 2 year fixed rate increased by 53 basis points to 4.17% for a 75% LTV mortgage and by 55 basis points to 4.47% for a 90% LTV mortgage. These increases both broadly mirrored the increase in Bank rate in September, and also meant that the spread between 2 year fixed 90% and 75% LTV mortgages, which had increased during the pandemic from 51 basis points in April 2020 to 189 basis points in December 2020, before decreasing to 31 basis points in January 2022, continued its recent trend of remaining stable at around 30 basis points.

Source: Bank of England

Moneyfacts' data as at 1 October 2022 shows that the average two-year and five-year fixed rates increased by 119 and 90 basis points relative to 1 September 2022, reaching 5.43% and 5.23% respectively. By 7 October, both of these rates had breached 6%, with the average two-year rate at 6.16%, its highest since November 2008, during the onset of the financial crisis, and the average five-year rate at 6.07%, its highest since January 2010. (Source: Moneyfacts Mortgage Treasury Report and news release).

Moneyfacts data also show that the market turmoil led to the number of residential mortgage products falling by 1,632 from September 2022 to October 2022, the largest monthly fall since April 2020, when the market was struck by the Covid-19 pandemic. At 2,258, the number of residential products is at its lowest level since May 2010. Relatedly, the average shelf life of a mortgage product fell to record low of 15 days due to the number of product withdrawals and significant repricing activity. The number of buy-to-let mortgages also fell sharply, halving from September 2022 to October 2022 to stand at 988, the lowest level since July 2015. (Source: Moneyfacts Mortgage Treasury Report).

A 215 basis point increase in interest rates is estimated to increase the monthly payment by around £180 per month for an average new variable rate and by around £100 per month on the average outstanding variable rate mortgage in Scotland. If the Bank Rate reaches 6% as some market participants have suggested, this is likely to lead to an increase of £550 per month for an average new variable rate and by around £300 per month on the average outstanding variable rate mortgage in Scotland relative to November 2021, immediately prior to the current upward cycle in Bank Rate.

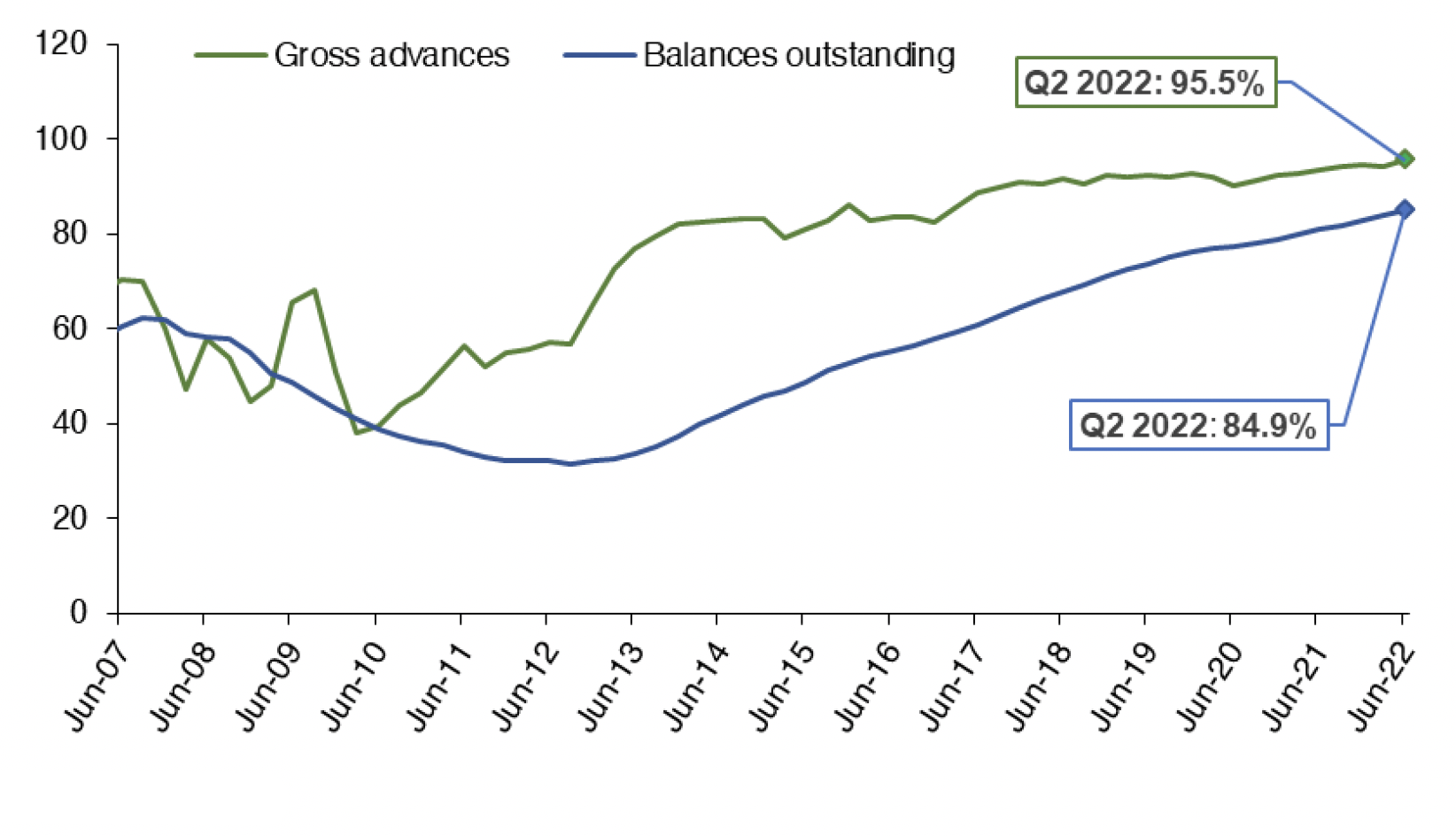

Chart 6.4 shows that the trend for an increasing share of regulated[1]mortgages to be at fixed rates has continued, with 95.5% of new mortgages and 84.9% of outstanding mortgages on fixed rates as of Q2 2022. The corresponding figures for unregulated[2] mortgages are 95.9% and 73.3%.(Source: FCA)

Source: FCA

Contact

Email: William.Ellison@gov.scot