Scottish Budget 2026-27, Spending Review and Infrastructure Delivery Pipeline: strategic integrated impact assessment

Strategic integrated impact assessment considering the impacts that decisions made in the Scottish Budget, Scottish Spending Review and Infrastructure Delivery Pipeline are likely to have on different groups of people in Scotland.

3. Strategic Overview of the Budget 2026-27, Spending Review and Infrastructure Delivery Pipeline

3.1 Overview

The Budget, SSR and IDP are more than just fiscal documents or events, they involve choices about how resources are raised and spent and, as such, reflect Government priorities and values. Over the current parliamentary term, the Scottish Government has used its devolved tax and benefit powers to design a more progressive system compared to the rest of the UK. The decisions taken at the Budget and SSR build upon this approach.

Analysis for the 2026-27 Budget[5] shows that:

- The Scottish Budget redistributes from high-income households to those further down the income distribution, through both the tax and social security system, and through the delivery of public services.

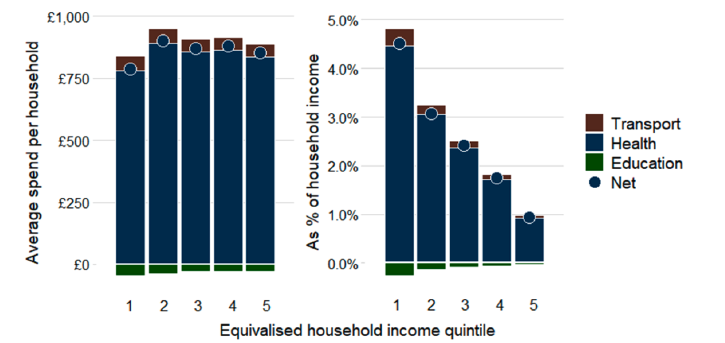

- Health resource spending provides a greater impact for lower-income quintiles, when considered as a share of household income.

- Devolved benefit payments primarily provide targeted support to low-income families to alleviate poverty, and financial support to disabled people. Overall, social security spend is redistributive, with the Scottish Child Payment (SCP) the largest single contributor to the improved financial resources of low-income households relative to the rest of the UK.

The resource allocations for the Budget and the SSR prioritise Health and Social Care and Social Security spending with above inflation increases across all years, recognising their role in supporting living standards, addressing inequality and reducing poverty. These decisions also support access to a number of the children’s rights under the UN Convention on the Rights of the Child (UNCRC) requirements (as incorporated into Scots law), as set out in Annex A.

The real-terms uplift to the Local Government settlement in 2026-27 acknowledges the important role local authorities play in providing services to support several relevant protected characteristics, children, those on lower incomes and more generally consumers of public services.

Distributional analysis shows that the SSR projects a modest real-terms increase in aggregate resource spending by 2028-29, the end of the SSR period. Compared to a baseline where all spending is held flat in real terms, households across the income distribution are expected to gain from this investment in public services.[6] However, when considered as a share of income, gains are proportionally larger for those on lower incomes. Most of the positive effect comes from higher Health spending which grows above inflation. Resource spending on Colleges, Tuition Fees and Higher Education grows more slowly than inflation, creating small losses across all households – slightly larger for lower quintiles, as they receive more of this spending on average and are more impacted by a reduction in real spending. Overall, the net effect remains positive. In addition, households in the bottom quintile benefit the least, in cash terms, as they are less likely to include older people, who benefit from increased Health spending.

Source: Scottish Budget 2026-27 – Distributional Analysis

Social Security

The Scottish Government has deliberately built a radically different system to both tackle the worst impacts of UK Government cuts and to tackle inequality and child poverty, while also providing vital assistance to enable older people to heat their homes and to help disabled people live independent lives.

Distributional analysis shows that, on average, households in the lower half of the income distribution are around £480 better off a year than they would be under UK Government tax and social security policies.[7]

The Budget confirms an uplift for all social security benefits in line with September 2025 Consumer Price Inflation (3.8 per cent) which ensures that recipients will not see their financial support eroded by inflation. Alongside this, unpaid carers, the majority of whom are women, will see an increase in the Carer Support Payment Earnings Threshold. This will improve incomes and access to work for women of working age and those on lower incomes in particular. However, it might have less impact on those with the most intensive caring roles who may be unable to work.

Evidence also shows that women, disabled people and people from minority ethnic communities may be likely to benefit most from new Scottish benefits, such as the SCP.[8] This reflects the additional support required by these disadvantaged groups.

Recent evaluation evidence on the Five Family Payments shows that these have helped families to spend more on supporting their children, including on essentials, school-related items and treat items as well as helping children take part in social and educational activities.[9]

In June, the Government announced that from winter 2025-26, Pension Age Winter Heating Payment will be paid to all pensioners but recovered through taxation from those pensioners with a personal income of over £35,000 per year. Pensioners with relevant protected characteristics are more likely to need additional support with heating expenses because they tend to have lower incomes, higher energy needs because of a health condition or disability as well as lower quality of housing, or lack of central heating.[10] Capping the payment at £35,000 is progressive and benefits the lowest-earning 20 per cent of households most, when considered as a share of income. It also provides cost-of-living support for pensioner households at most risk of fuel poverty, including women and ethnic minority households who are more likely to live in poverty.

Taxation

Tax policy decisions in the Budget and SSR continue the progressive approach taken over previous years, while raising substantial revenues to support the delivery of public services. Scottish Income Tax alone is forecast to increase funding by up to an additional £1.8 billion in 2026-27 compared to if we had matched UK Government policy.

The Income Tax policy package maintains Scotland’s progressive tax system and supports taxpayers on lower incomes by raising the Basic and Intermediate Rate thresholds by 7.4 per cent, significantly more than inflation. This will help ensure that we meet our commitment that more than half of taxpayers are expected to pay less Income Tax than they would in the rest of the UK. Scottish Government analysis based on independent Scottish Fiscal Commission forecasts suggests that 55 per cent of taxpayers can expect to pay less in 2026-27. Distributional analysis shows that lower-income households gain slightly from increased Basic and Intermediate Rate Thresholds, while higher-income households see reduced post-tax income in real terms due to the freeze of the Higher, Advanced and Top Rate Thresholds.[11]

Income Tax applies to taxable income, regardless of relevant protected characteristics or geographical location. Therefore, any differential impact on the relevant protected characteristics will simply reflect their distribution in the taxpayer population.

Non-domestic rates (NDR), also known as business rates, are a tax on non-domestic properties, based on the rateable value of a property minus any reliefs, to help pay for local council services. Tax decisions in this Budget will support businesses by lowering the Basic, Intermediate and Higher Property Rates in 2026-27; providing 15 per cent relief for retail, hospitality and leisure (RHL) properties with up to £100,000 in rateable value on the mainland; providing 100 per cent RHL relief on islands as defined by the Islands (Scotland) Act 2018, and in three prescribed remote areas (Cape Wrath, Knoydart and Scoraig) capped at £110,000 per ratepayer; providing transitional reliefs based on the forthcoming revaluation on 1 April 2026 and continuing the Small Business Bonus Scheme for the next three years.

The NDR system supports business growth, investment and competitiveness, while acknowledging the important role NDR income plays in funding public services, raising over £3 billion in funding in 2026-27. Given the universal nature of NDR, and the lack of information on the characteristics of non-domestic property owners or occupiers, or ratepayers, it is not possible to distinguish any potential differential impact on the relevant protected characteristics, children or socio-economic status.

The differential treatment of the RHL sectors in island communities, compared to the mainland, recognises the specific challenges faced by these sectors in island communities. For example, island businesses report more significant challenges in relation to staffing, costs, profitability and investment than their mainland rural counterparts.[12]

There are an estimated 1,700 properties on islands that will be eligible and benefit from 100 per cent RHL relief that would not otherwise be awarded 100 per cent relief.[13] Since the relief is mandatory and 100 per cent funded by the Scottish Government, it does not reduce island local authorities’ budgets.

A full islands impact assessment will accompany the secondary legislation. Previous assessments noted that hospitality relief is appropriately targeted to benefit hospitality businesses – a key sector of island economies and a key source of employment.[14]

From April 2028, the Scottish Government intends to introduce new Council Tax bands for the highest valued residential properties to improve fairness at the top end of the system. It is estimated that fewer than one per cent of households will be affected, maintaining the existing system for the rest of the tax base.

Alongside the development of this policy, the Scottish Government is undertaking a joint programme of engagement with the Convention of Scottish Local Authorities on the future of Council Tax, including a public consultation. That consultation explores a range of potential reform options, including system wide revaluation and redesigned band structures intended to make Council Tax less regressive.

Modelling from an independent analysis report produced by the Institute for Fiscal Studies (IFS) on behalf of the Scottish Government illustrates the impact of less regressive Council Tax systems through increasing relative charges at the top end of the property value distribution on households.[15] These models do not capture this exact policy measure, and are based on whole system change across the property distribution, but they do show a general trend that in more progressive systems, average Council Tax liabilities generally increase for higher-income households and owner occupiers, and generally fall for lower- and middle-income households and renters.

By contrast to the IFS analysis report where reform models apply to the full property distribution, the proposed Bands I and J apply only to properties valued above £1 million. As such, any increase in liability would, by design, be more tightly concentrated than under the models being consulted on. One inference is that the direct impact of the policy is more likely to fall primarily on owner-occupiers of very high value properties. Further, it is more probable that this measure would affect higher income households.

It is important to recognise that income and wealth do not perfectly align and that there will be individual circumstances to consider. Impacts would also be more geographically concentrated in local authority areas and neighbourhoods where such properties are most prevalent, rather than being spread broadly across areas as would be the case under system-wide reform. The IFS analysis on mitigations is particularly relevant to a high value property bands policy, because it distinguishes between different types of households who may face affordability pressures from higher Council Tax bills. In particular it identifies ‘cash poor, asset rich’ households, such as some older owner occupiers with high housing wealth but low liquid income, and ‘cash poor, asset poor’ households with limited income and limited wealth. Such groups are likely to face different affordability pressures and may require different forms of support.

As this policy is developed, and ahead of the introduction of any legislation, the Scottish Government will work with Local Government to further consider the impact of the measure in line with our statutory duties. As part of this, we will consider the evidence and views emerging from the ongoing programme of engagement, including the current consultation The Future of Council Tax in Scotland.[16] This will include exploring appropriate safeguards and mitigations, such as deferral arrangements and the potential expansion or adaptation of the Council Tax Reduction scheme, to ensure that affordability is protected and the approach remains fair, proportionate and deliverable.

3.2 Setting Priorities

Difficult choices about where to invest and spend now or in future years, and whether to raise additional funding through taxation or reallocate across spending priorities, are necessary against a backdrop of constrained resources and rising demand for public services. These choices involve trade-offs which might result in real-terms reductions or constrained growth in resource funding for some portfolio spend which low-income and disadvantaged households rely upon. It also means that we will need to scale back, or not proceed, with some capital projects to ensure we continue to live within our means.

This means that for some portfolios, resource funding has not kept pace with inflation or service demand in 2026-27. Some small reductions, in real terms, are seen in, Climate Action and Energy; Rural Affairs, Land Reform and Islands; and Finance. The Local Government settlement sees a real-terms uplift in 2026-27 but similar to other portfolios sees a constrained funding envelope in 2027-28 and 2028-29. This, alongside a planned 0.5 per cent reduction in the devolved public sector workforce, could have potential negative implications for consumers of public services as well as public sector workers. This is expected to be mitigated through service redesign, automation, and smarter resource use since the approach is designed to protect frontline services while reducing corporate costs and improving productivity.

Any reductions in allocations also have to be considered in the context of the Public Service Reform (PSR) Strategy which commits us to deliver a more preventative, joined-up and efficient system and optimising every pound of public spend. Portfolio Efficiency Plans published alongside the budget set out details of around £1.5 billion cumulative efficiencies over the SSR period, delivering on corporate functions and workforce savings to free up funding for investment in frontline public services. A reduction in spend, or costs, is therefore not always equal to a reduction in service provision.

Re-prioritisation is inevitable in order to direct spend where it is most impactful. Any reductions should therefore be seen in the wider context of a Budget that continues to fund the social contract that is at the heart of this Government’s approach, with an overall positive, or neutral, impact across disadvantaged groups. Additional mitigation measures are set out in Section 4, as well as in the CRWIA at Annex A.

A transfer of funding from resource to capital, for example to fund the dualling of the A9, will leave less funding for delivering day to day public services, while providing a boost to longer term infrastructure investment, and so represents a trade-off.

On the one hand, spending on day-to-day public services through the resource budget can play a vital, and immediate, role in advancing equality and fairness. For example, the social security system plays a crucial part in keeping people out of poverty and redistributing income. Similarly, although spending on public services, such as Health, Transport or Education, is not necessarily aimed at redistributing income, research has shown that spending on such public services can also be highly redistributive and has become more so over the past 35 years.[17]

However, it has also been extensively documented that public investment in infrastructure provides a wide range of community and economic benefits. The IDP points out that infrastructure underpins the crucial public services that people rely on every day. Similarly, Audit Scotland has emphasised the importance of infrastructure in supporting inclusive economic growth, improving the efficiency and effectiveness of public services, and generally promoting wellbeing and quality of life.[18] International evidence also emphasises the role of infrastructure in addressing challenges in society.[19]

3.3 Overall Impact

Overall, the decisions taken at the Budget, SSR and IDP are expected to have a positive or neutral impact across the five statutory duties considered.

Budgeting decisions advance equality of opportunity, eliminate discrimination and foster good relations in line with the PSED (and the related Scottish specific duties) and the Fairer Scotland Duty, ensuring that people with relevant protected characteristics and those experiencing socio-economic disadvantage benefit equitably from public services and support. No disproportionate impacts, positive or negative, have been identified for some of the relevant protected characteristics, including religion or belief, pregnancy and maternity, sexual orientation and gender reassignment. However, there is also more limited evidence concerning these equality groups.

The substantial investment in the child poverty package and spending that benefits all children is likely to be positive for child rights. This includes investment in social security; measures to support families with the cost of living such as the universal free breakfast offer or the Summer of Sport; free school meals; free bus travel for those under the age of 22; early learning and childcare; Employability programme; and additional investment in further education colleges alongside above inflation uplifts to Health and Social Security expenditure. Any negative impacts from individual policy decisions are likely to be offset by overall positive impacts and mitigations applied as necessary.

The overall impact on consumers is also broadly neutral with both positive and negative impacts and reflecting the dual role consumers play as taxpayers and service users.

For island communities, there is no significant differential impact between island communities and the mainland or between different island communities. For example, the highest-spending portfolios of Health and Social Care, Local Government, Social Security, Justice, and Education, all broadly benefit people across Scotland equally. The above-listed spending areas collectively account for over 90 per cent of the resource budget. Where funding is allocated on a geographical basis, for example to territorial health boards or to Local Government, the majority of this is done using pre-existing formulae based on a range of social and economic criteria. With regard to specific budget programmes which disproportionately impact island communities, some are constrained, while others are maintained or increased, for example through investment in inter-island connectivity and the removal of peak fares on ferries to the Northern Isles for residents. Within the context of the overall budget, the above items are relatively small in scale. In addition, islands RHL businesses will benefit from a more generous NDR relief than their mainland counterparts.

Contact

Email: ScottishBudget@gov.scot