Scotland's Climate Change Plan: 2026–2040

This Climate Change Plan (CCP) sets out the policies and proposals we will take forward to enable our carbon budgets to be met between 2026 and 2040.

Annex 3 – Monitoring and Analytical Annex

Contents

Monitoring and Evaluation of the Climate Change Plan

Analytical Annex

- Section Overview

- Buildings (Residential and Public)

- Transport

- Waste Management

- Energy Supply

- Business and Industrial Process

- Negative Emissions Technologies

- Agriculture

- Land Use, Land Use Change, Forestry

CCP Policy List

- Buildings (Residential and Public)

- Transport

- Waste

- Energy Supply

- Business and Industrial Process (including NETs)

- Agriculture

- LULUCF

Monitoring and Evaluation of the Climate Change Plan

Background and Structure

Introduction

The Monitoring and Evaluation (M&E) framework presented below will be used to assess whether the policies and proposals within the Climate Change Plan (CCP) are being implemented as intended and whether the required emissions reduction and just transition outcomes are being realised in delivery. It provides the primary evidence base through which Ministers assess progress and fulfil their statutory duties to report to Parliament on whether Scotland is on track to meet its emissions-reduction targets.

The framework combines greenhouse gas emissions statistics with quantitative indicators of progress towards policy outcomes and qualitative commentary on policy implementation, to provide a comprehensive picture of progress. This reflects the understanding that emissions reductions depend on a combination of effective policy delivery, technological and behavioural change, and positive enabling conditions. Monitoring therefore extends beyond emissions data to capture evidence of the broader drivers of change.

Delivering net zero in a way that is fair and inclusive is a core commitment of the Scottish Government. A set of cross-sectoral just transition indicators is included within the framework to help assess whether the transition to net zero is supporting good jobs, reducing inequalities, and avoiding disproportionate impacts on particular groups or places. We are grateful to the Just Transition Commission, whose commissioned research and constructive advice has informed the development of these indicators.

The framework is grounded in the best available evidence and is designed to evolve over time as our understanding of delivery improves. As new data sources and analytical approaches emerge, including potential enhancements proposed by the Scottish Science Advisory Council, we will consider these alongside the application of the framework in producing the first annual progress report under the new CCP in 2027. This will provide an early opportunity to refine or expand the indicator set where supported by robust evidence.

Together, the approach to monitoring and evaluation as outlined below is designed to support ongoing scrutiny of the CCP, inform future policy development, and provide stakeholders and the public with a clear and accessible account of progress towards Scotland’s climate and just transition ambitions.

Principles of the monitoring framework

The development of the M&E framework has been guided by the following set of principles to ensure that monitoring and evaluation is robust, transparent, and proportionate, supporting effective delivery of the Plan over time.

1. Monitoring will focus on the most material sources of emissions and the key actions required to deliver emissions reduction in line with just transition principles, avoiding unnecessary complexity while providing sufficient detail to support meaningful assessment.

2. Where possible, indicators and target metrics are defined and evaluated consistently over time, in line with SMART principles (Specific, Measurable, Achievable, Realistic and Time-bound), to support the identification of trends and enable comparison across reporting periods.

3. The information required to evidence outcome attainment is publicly available, published regularly and presented in a clear and accessible way to support scrutiny by stakeholders and the public.

4. The framework is designed to provide timely insight into delivery and emerging risks. It will serve as the primary means with which to assess any risk to achieving our carbon budgets and meeting our just transition commitments. Where risks to budget attainment arise, we will adjust delivery and broaden the ambition of the policy response as needed.

5. Monitoring and evaluation makes use of the best available evidence and is used to inform learning over time. The framework will continue to evolve in response to improvements in data availability, analytical methods, and experience of policy delivery.

6. Monitoring is undertaken in a way that supports consideration of fairness and inclusivity, including through the use of just transition indicators alongside emissions-focused metrics.

What’s changed in this Climate Change Plan

As part of the development of this Climate Change Plan, emissions pathways have been produced for each major sub-sectoral source of greenhouse gas emissions. These pathways set out the expected rate and scale of emissions reduction for individual emissions sources over each Carbon Budget. When sub-sectoral pathways are combined, they form sectoral emissions envelopes, and when aggregated across sectors, as defined in the Climate Change Act, align with Scotland’s overall carbon budget.

Sectoral outcomes have been revised to reflect this approach. Each major sub-sectoral source of emissions now has a quantified outcome formulated around emissions pathways.

Example formulation of a sub-sectoral outcome: 'Emissions from cars should total less than 18 MtCO2e between 2026-2030'.

In this way, outcomes provide a clear means of articulating what success looks like and enables progress to be statistically evaluated consistently over time.

Indicators have been identified to align with these sub-sectoral emissions sources. This helps ensure that monitoring focuses on the key activities, behaviours, and system changes that are expected to deliver the emissions pathways, strengthening the link between policy delivery, outcomes, and emissions reduction.

The monitoring framework also incorporates an expanded set of just transition indicators. These indicators support consideration of whether the transition to net zero is being delivered in a way that is fair and inclusive and provide additional transparency on distributional and socioeconomic impacts.

Components of the monitoring framework

The updated monitoring framework for the Climate Change Plan is built around four complementary elements that, together, provide a comprehensive view of progress in delivering emissions reductions and supporting a just transition:

- Greenhouse gas inventory emissions statistics;

- Emissions-reduction indicators;

- Just transition indicators; and

- The policy tracker.

Greenhouse Gas Emissions Inventory Statistics

Greenhouse gas (GHG) emissions statistics allow progress in reducing emissions to be assessed at national, sectoral, and sub-sectoral levels. These statistics provide the authoritative measure of emissions performance against statutory targets and carbon budgets for all governments across the UK.

Statistics are published annually, typically in June, and two years in arrears. For example, the most recent figures, published in June 2025, cover emissions up to and including 2023. Monitoring reports used to assess the previous Climate Change Plan update were published in May, using GHG data that was effectively lagged by 3 years.

To support more timely and effective monitoring of progress against statutory climate targets, the publication timetable for the CCP monitoring reports has been revised and, going forward, will be published after release of the latest GHG Inventory data. This should strengthen the evidence base available to Ministers, support earlier identification of delivery risks or underperformance, and improve transparency around progress towards targets. It will also benefit stakeholders by bringing together the most up-to-date emissions data, indicator trends and policy delivery information within a single report, while recognising that a structural time lag which is out with the Scottish Government’s control in GHG reporting remains and must continue to be addressed through complementary indicators and analysis.

GHG emissions statistics will be used to assess progress against the sub-sectoral emissions outcomes set out in the Climate Change Plan and to inform judgements about the likelihood of achieving Scotland’s national emissions targets. Emissions data will continue to provide the definitive measure of progress, complemented by indicators and other monitoring evidence described elsewhere in this chapter.

Emissions-reduction indicators

Emissions-reduction indicators complement GHG emissions data. There are two types of emissions-reduction indicators: outcome indicators and enabling indicators. Emissions-reduction outcome indicators track progress in delivering the key actions and changes expected to contribute to emissions reduction (for example, hectares of new woodlands planted). Emissions-reduction enabling indicators provide contextual evidence on the conditions that influence effective policy delivery (for example, the share of short journeys under 5kms made via walking or cycling).

For this Climate Change Plan, the set of outcome indicators used to evidence the 2020 Climate Change Plan update (CCPu) monitoring reports were reviewed to ensure that they reflect revised policy commitments and to improve the quality and clarity of indicators. This has led to new outcome and enabling indicators being identified, others being revised, and several being removed where issues with timeliness of data availability, relevance to the policy package, or ease of interpretation were identified. The overall set of indicators is now 36 including the new Just Transition specific indicators, relative to the 43 previously used for the CCPu.

1. Emissions-reduction outcome indicators

Emissions-reduction outcome indicators are specific, objective measures closely aligned with achieving the sub sectoral outcome. Where possible, these directly capture the key actions required to deliver the level of emissions abatement consistent with the emissions pathways; for example, hectares of new woodland required to be planted.

In some cases, data limitations mean it has not been possible to identify indicators that directly measure these actions. In such instances, emissions-reduction indicators reflect the changes in the policy environment that are expected to arise from the policies and proposals set out in the Climate Change Plan; for example, measuring emissions from industrial emitters captured within the traded sector of the Emissions Trading Scheme (ETS).

Emissions-reduction indicators underpin monitoring of progress towards sub-sectoral outcomes and are designed to be sensitive to change in the near term. This allows them to complement time-lagged greenhouse gas emissions data, providing earlier insight into whether delivery is progressing at a pace and scale consistent with expectation. Specific milestones are set for indicators, where appropriate, setting out the level of ambition consistent with achieving the sub sectoral outcome.

2. Emissions-reduction enabling Indicators

Enabling indicators track the wider system conditions that support or constrain progress towards emissions-reduction outcomes. They capture behavioural, market, infrastructure and system-readiness factors that influence whether policies can be delivered effectively and at the pace assumed in the emissions pathways.

In transport, enabling indicators focus on modal shift; including the proportion of short journeys made by walking or cycling, the proportion of longer journeys made by bus or rail, and household access to a bicycle. These indicators provide insight into behavioural change and the practical conditions required to reduce car dependency over time.

In energy supply, enabling indicators track renewable generation capacity (both installed and at planning stages) and system reliability through Loss of Load Expectation. Together, these provide a forward-looking view of deployment momentum and energy security as the electricity system decarbonises.

In waste, total waste generation (excluding soils and mineral waste from construction and demolition) is monitored as a directional indicator of resource efficiency and upstream prevention - a key condition for reducing emissions from the sector.

Enabling indicators are assessed on a directional or year-on-year change basis, depending on the metric, and are considered alongside outcome indicators, emissions data and policy implementation evidence. They provide insight into whether the conditions necessary for sustained emissions reduction are strengthening and help identify emerging constraints or delivery risks.

Just transition indicators

Our commitment to a just transition to net zero remains unwavering and, as such, this underpins Scotland’s carbon budget targets. The inclusion of just transition indicators in the CCP M&E framework represents a significant milestone in our commitment to embed the just transition principles across all aspects of climate policy. To our knowledge, Scotland is the first country to include a dedicated set of just transition indicators within annual statutory reporting.

Unlike the emissions-reduction indicators outlined above, just transition indicators are cross-cutting and apply to the Plan as a whole, rather than aligned with specific emissions sources. This reflects the cross-sectoral nature of just transition, which requires a coordinated economy- and society-wide response. Whilst it may be possible to make links between some indicators and specific sectors (e.g. Fuel Poverty with Buildings, or Community Benefits with Energy Supply), the indicators are intended to be considered together to give a holistic assessment of the extent to which the CCP is supporting progress towards a just transition.

Key to monitoring the delivery of a just transition to net zero[272] is understanding how our policies and proposals affect different societal groups and geographic regions across Scotland. The indicators aim to address this need by combining metrics that provide a single whole-of-Scotland measure with those that focus on specific sub-groups of the population, including:

- Communities and workers facing significant impacts as a result of their close connections with particular carbon intensive industries.

- Places with significant local net zero infrastructure and land use change

- Differentiated rural, urban and island community impacts

- Businesses

The indicators draw on an extensive evidence base, developed with key stakeholders, particularly the Just Transition Commission. By reporting on them as part of the CCP monitoring and evaluation, we intend to provide an overview of progress on delivering our emissions reduction ambitions in a way that is fair and just.

The draft Climate Change Plan proposed and sought views on 14 just transition indicators. The most common theme emerging from consultation responses related to the transport affordability indicator, which some respondents suggested should be disaggregated by income level or mode of transport, to give a more meaningful measure of transport poverty. Based on these responses and given the data source does not allow for a breakdown by mode, we have altered the indicator to include a breakdown by household income. In addition, we have re-categorised two of the other draft just transition indicators – covering woodland creation and peatland restoration – as emissions reduction outcome indicators, given this is their primary focus.

There will be room for improvement on the indicators, given this is the first time they will be used. There are gaps in the data required to directly measure key aspects of a just transition and, in several instances, we rely on proxy metrics to provide a best estimate of progress. We have been working to improve data availability, including through the development of the Scottish Climate Survey. This work will continue after publication of the CCP and, as new data sources emerge, we will seek to update and improve these indicators.

We know that it is not possible for a small set of metrics to provide a complete assessment of whether we are delivering a just transition for Scotland. The complex, dynamic and multi-layered range of outcomes that the Scottish Government has identified for Scotland’s wider just transition extend beyond the CCP and the CCP monitoring process. We are therefore developing a dedicated just transition M&E framework, which will incorporate an expanded suite of measures of justice relating to both climate change mitigation and adaptation. We aim to set out proposals for this framework within the next 12 months.

Policy Tracker

The Climate Change Plan sets out a package of specific policies and proposals across sectors to deliver the policy outcomes and emissions reductions required to meet Scotland’s climate targets. As was the case with CCPu M&E, progress in implementing these policies and in developing proposals will be monitored through a policy tracker.

The policy tracker provides a structured overview of delivery status, capturing key milestones such as policy development, consultation, implementation, and ongoing delivery. It supports transparency around progress and helps signal where policies are on track, where delivery is at risk, and where further action or intervention may be required.

As part of annual monitoring reports each of the 163 policies and commitments set out in the CCP will be qualitatively assessed, with progress addressed relative to expectation and specific implementation milestones.

Summary of indicators

The following tables summarise the suite of indicators that will be used to monitor and evaluate progress in delivering the policies and proposals set out in the Climate Change Plan.

Emissions-reduction indicators are aligned to sub-sectoral sources of emissions. This reflects the structure of the annual CCP monitoring reports and is intended to clearly demonstrate the relationship between policy delivery, changes captured by indicators, and progress towards the sub-sectoral emissions outcomes. As discussed above, just transition indicators are applied to the delivery of the Plan as a whole, rather than aligned to specific sources of emissions.

The following information is provided for every indicator in the framework:

- Indicator – a short description of the metric used to track progress.

- Expected trend – an explanation of how trends in the indicator will be interpreted (for example, against a defined target, a pathway-based trajectory, or a basic directional change).

For emissions-reduction indicators, the following additional information is provided:

- Emissions Source – the sub-sectoral source of emissions the indicator is linked to.

- Type – whether the indicator is an outcome indicator (directly linked to achieving emissions reductions) or an enabling indicator (capturing supporting conditions or contextual factors).

Alongside this M&E process, the Scottish Government keeps track of a broad range of other indicators and data to ensure that there is coherence and responsiveness between our climate goals and other priorities such as growing the economy and eradicating child poverty.

Emissions-reduction indicators

Transport

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Percentage of new car registrations that are Zero Emissions Vehicles | Cars | Outcome | Increase in new EV sales in line with CCC advice, 90% of new car sales to be zero emission by 2030. |

| Percentage reduction in car kilometres | Cars | Outcome | In line with CCC advice, progress towards target of reducing kilometres driven by 4%, relative to the business as usual baseline for car demand |

| Percentage of short journeys (under 2/5km) made via walking or cycling | Multiple | Enabling | Increasing over time |

| Percentage of households with access to a bike | Multiple | Enabling | Increasing over time |

| Percentage of longer journeys (over 5km) made via bus or rail | Multiple | Enabling | Increasing over time |

| Percentage of new van registrations that are Zero Emissions Vehicles | LGVs | Outcome | Increase in new EV sales in line with CCC advice.100% of new van sales to be zero emission by 2030. |

| Percentage of new bus registrations that are Zero Emissions Vehicles | Buses | Outcome | Increasing over time |

| Percentage of new HGV registrations that are Zero Emissions Vehicles | HGVs | Outcome | Increase in new zero-emission vehicle sales in line with CCC advice. 23% of new HGV sales to be zero emission by 2030. |

Business and industrial processes

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Emissions from industry ETS traded sector (industrial sites only) | Industrial processes | Outcome | Emissions to fall by 24% between 2026–2030 |

Energy Supply

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Electricity grid intensity (CO2e per kWh) | Power stations | Outcome | Maintain below 40 g CO2e per kilowatt hour |

| Installed capacity of renewable generation (GW) | Power stations | Enabling | Increasing over time |

| Renewable capacity at planning stages (GW, 3 categories) | Power stations | Enabling | Increasing over time |

| Loss of Load Expectation (hours per year) | Power stations | Enabling | Maintain GB standard below 3 hours per year |

| Household waste incinerated | Energy from Waste | Outcome | Projected to increase until 2028 then gradually reduce[273] |

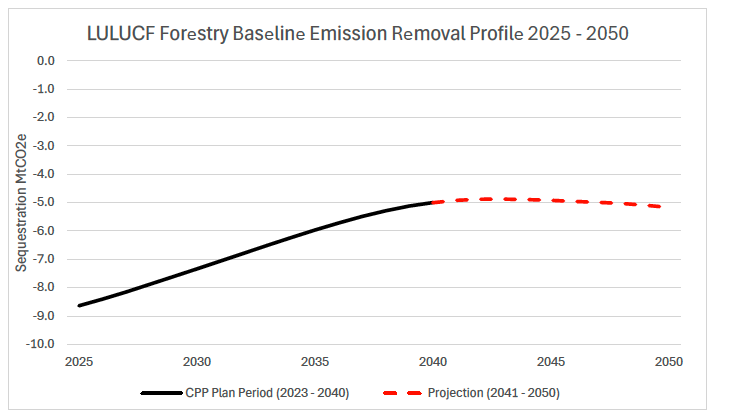

Land Use, Land Use Change and Forestry (LULUCF)[274]

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Hectares of woodland created | Forestry | Outcome | Progress towards target of planting approximately 78,000 hectares between 2026–2030 |

| Hectares of peatland restored | Peatland | Outcome | Progress towards target of restoring 400,000 hectares by 2040 |

Buildings (Residential and Public)

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Number of buildings using low and zero direct emissions heating (LZDEH) systems | Buildings | Outcome | 35,000 additional buildings convert to LZDEH over 2026-2030 |

| Number of homes with EPC C or above (or equivalent) | Buildings | Outcome | 134,900 domestic properties in total to achieve EPC C+ (or equivalent) over 2026-2030 |

Waste Management

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Tonnage of biodegradable municipal waste (BMW) landfilled | Landfill | Outcome | Progress towards zero biodegradable municipal waste being landfilled in 2028 |

| Waste tonnage generated (excluding soils and mineral waste from construction & demolition) | Waste generation | Enabling | Decreasing over time |

Agriculture[275]

| Indicator | Emissions source | Type | Expected trend |

|---|---|---|---|

| Engagement with Farm Advisory Services on environmental issues and climate change | All Sources | Enabling | Increasing over time |

| Use of nitrogen fertilisers | Cropland / soils | Outcome | Decreasing over time |

| Total overall nitrogen application rates | Cropland / soils | Outcome | Decreasing over time |

| Average age at slaughter of prime animal | Livestock | Outcome | Decreasing over time |

| Woodland area on agricultural land | Cropland / soils | Outcome | Increasing over time |

Just Transition indicators

| Indicator | Expected trend |

|---|---|

| Percentage of people satisfied with participation in net zero decision making | Increasing over time |

| Operational capacity of community energy | Increasing over time |

| Average value of community benefits | Meet or exceed the Scottish Government Good Practice Principles for community benefits |

| Percentage of people reporting improvements to their local area as a result of net zero infrastructure or land use change | Maintaining or increasing over time |

| Percentage of dwellings in fuel poverty | Statutory Fuel Poverty targets: ≤5% fuel poverty and ≤1% extreme fuel poverty by 2040 |

| Percentage of people that can afford their transport costs | Increasing over time |

| Employment rate in oil and gas communities | Maintaining or increasing over time |

| Proportion of households managing well financially in oil and gas communities. | Maintaining or increasing over time |

| Number of recipients of the Oil and Gas Transition Training Fund | Fund sufficient to meet demand |

| Number of people employed in low carbon and renewable energy economy | Increasing over time |

| Proportion of small businesses reporting energy prices as an obstacle | Decreasing over time |

| Emissions of the eight priority Air Quality pollutants | Decreasing over time |

Indicator evaluation

The following section provides a detailed assessment of each indicator included in the monitoring framework, using the evaluation criteria set out in Table 9. Applying these criteria to each indicator in turn provides a consistent and transparent basis for assessing the strength and limitations of the monitoring framework. It also helps identify where indicators provide high evidential value, where interpretation should be cautious, and where further development or data improvement may be required.

| Criterion | Description | Low | Moderate | High |

|---|---|---|---|---|

| Relevance | The indicator should relate clearly to the emissions source, pathway or just transition outcome it is designed to monitor | Minimal or indirect relationship to emissions reduction or just transition | Some relationship to emissions reduction or just transition but indirect or partial | Clear and direct relationship to the emissions pathway or just transition outcome |

| Representative-ness | The indicator should capture the key drivers or system changes required to deliver the emissions pathway or just transition outcome | The indicator doesn’t capture the key drivers of the expected emissions reduction or just transition outcome | Represents some important drivers but not the full picture | Represents the key drivers of just transition or emissions change within the sub-sector |

| Data availability | Data should be regularly published, accessible and sufficiently robust | Data unavailable, restricted, irregular or highly uncertain | Data available but with limitations (lag, infrequent updates, quality caveats) | Data regularly published, accessible, and statistically robust |

| Sensitivity to change | The indicator data must be capable of detecting meaningful change relative to expected delivery within a carbon budget period | Changes cannot be reliably detected due to sample size, variability, or infrequent data collection | Some change detectable but small deviations from expectation may not be statistically distinguishable | Data precise and frequent enough to detect small but meaningful changes against expected trajectory |

| Interpretability | The indicator should be understandable to non-expert stakeholders and allow clear interpretation of direction of travel | Difficult to interpret; direction of success ambiguous | Some technical interpretation required | Direction of success clear and easily understood |

| Practicality | Indicator should be cost-effective to use and have low resource requirements for data collection and analysis | Prohibitively expensive and/or impractical to use indicator data | Moderate resource requirements | Cost-effective and low-resource to use indicator data |

Transport

TRANSPORT 1 - Zero Emission Vehicle (ZEV) car registration

| Indicator Title | % of new car registrations that are Zero Emission Vehicles |

|---|---|

| Description | Proportion of newly registered cars in Scotland each year that are zero emission vehicles (battery electric or hydrogen fuel cell), indicating the rate of fleet decarbonisation. |

| Data Source | Department for Transport (DfT) and Driver and Vehicle Licencing Agency (DVLA) |

| Expected trend | Following CCC advice, progress towards achieving 90% of new car registrations being zero emission vehicles by 2030, assessed annually against the expected uptake trajectory consistent with the car emissions pathway. |

| Unit | Percentage (%) of new car registrations. |

| Limitations and data development | Indicator reflects new registrations only and does not capture the emissions performance of the existing fleet or total vehicle kilometres travelled. Emissions impacts materialise over time as fleet turnover occurs. Data is robust and population-based, though classification of vehicle types may evolve as technologies develop. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Fleet turnover is a primary driver of long-term emissions reductions from cars. Increasing ZEV share directly supports the car emissions pathway. |

| Representativeness | Moderate | Captures new vehicle uptake but does not reflect the existing fleet, total vehicle kilometres, or modal shift. |

| Data availability | High | Published annually in Scottish Transport Statistics; consistent methodology and good coverage. |

| Sensitivity to change | High | Highly responsive to policy, market and infrastructure changes; year-on-year shifts detectable. |

| Interpretability | High | Simple percentage measure; direction of success (increase) is clear. |

| Practicality | High | Based on existing administrative data; minimal additional resource required. |

TRANSPORT 2 - Reduction in car kilometres

| Indicator Title | % reduction in car kilometres |

|---|---|

| Description | Percentage reduction in total car vehicle kilometres travelled in Scotland relative to the baseline year, reflecting progress in reducing car use consistent with the transport emissions pathway. |

| Data Source | Scottish Transport Statistics (Transport Scotland), based on National Road Traffic Estimates. Published annually. |

| Expected trend | Progress towards achieving a 4% reduction in car kilometres by 2030, relative to the business as usual baseline for car demand; assessed against the expected trajectory consistent with the car emissions pathway. |

| Unit | Percentage (%) reduction relative to baseline year. |

| Limitations and data development | Estimates are derived from traffic count data and modelling that uses UK rather than Scottish specific trends. This may be subject to revision and, should Scottish driving behaviours significantly diverge from UK ones, then the estimates may not properly reflect these differences. Data is published annually, typically with approximately a one-year time lag, which limits real-time assessment. The indicator captures distance travelled but does not reflect vehicle occupancy, vehicle efficiency, or fleet electrification; therefore, it should be interpreted alongside ZEV uptake and modal shift indicators. Short-term volatility (e.g. economic conditions, fuel prices, weather events) may influence year-on-year change. There is uncertainty in baseline forecast demand for car travel, which is influenced by a wide range of factors and may be revised as required across the CCP period. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Total car kilometres travelled is a primary driver of transport emissions and directly affects fuel consumption and tailpipe emissions. |

| Representativeness | High | Captures behaviour across the entire car fleet and reflects one of the largest structural drivers of transport emissions. |

| Data availability | High | Published annually in Scottish Transport Statistics using established national traffic estimates methodology. |

| Sensitivity to change | Moderate | Large-scale changes are detectable; however, small year-on-year changes may fall within modelling uncertainty or natural traffic variability. |

| Interpretability | High | Direction of success (reduction) is clear and easily understood by stakeholders. |

| Practicality | High | Based on existing national traffic monitoring systems; no additional data collection required. |

TRANSPORT 3 - Mode of travel for short journeys

| Indicator Title | % of short journeys (under 2/5km) made via walking or cycling |

|---|---|

| Description | Proportion of short journeys (under 2km or 5km, depending on survey definition) made by walking or cycling in Scotland, reflecting modal shift away from car use for shorter trips. |

| Data Source | Transport and Travel in Scotland (Scottish Household Survey), |

| Expected trend | Assessed on a directional basis, with success understood as an increasing proportion of short journeys being made by walking or cycling. |

| Unit | Percentage (%) of short journeys. |

| Limitations and data development | Based on survey data and therefore subject to sampling variability and confidence intervals. Small year-on-year changes may not be statistically significant. The indicator captures only short journeys and does not reflect total car kilometres or longer-distance travel, which account for a larger share of transport emissions. It measures self-reported behaviour, which may be subject to recall bias. The relationship with emissions outcomes is indirect and dependent on substitution away from car use. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate | Modal shift away from car use reduces emissions; however, short journeys represent only part of total car kilometres and associated emissions. |

| Representativeness | Low –Moderate | Reflects behavioural change for short trips only and does not capture overall car demand, freight, or fleet decarbonisation. |

| Data availability | High | Published annually through Transport and Travel in Scotland. |

| Sensitivity to change | Moderate | Survey-based measure; meaningful changes detectable over time but small annual changes may fall within confidence intervals. |

| Interpretability | High | Direction of success (increase in active travel share) is clear and easily communicated. |

| Practicality | High | Uses established survey data; no additional collection required. |

TRANSPORT 4 – Access to a bicycle

| Indicator Title | Percentage of households with access to a bike |

|---|---|

| Description | Proportion of households in Scotland reporting access to one or more bicycles, indicating the potential capacity for active travel. |

| Data Source | Transport and Travel in Scotland (Scottish Household Survey), published annually. |

| Expected trend | Assessed on a directional basis, with success understood as an increasing proportion of households having access to a bicycle, supporting conditions for modal shift to active travel. |

| Unit | Percentage (%) of households. |

| Limitations and data development | Based on survey data and therefore subject to sampling variability and confidence intervals. The indicator measures access rather than actual use, and does not capture frequency of cycling or substitution away from car travel. Increases in access do not necessarily translate into emissions reductions. The relationship with transport emissions is indirect and dependent on behavioural change. Small year-on-year movements may not be statistically significant. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Low –Moderate | Access to a bicycle may enable modal shift, but the link to emissions reduction is indirect and dependent on behavioural change. |

| Representativeness | Low | Captures one enabling condition only and does not reflect actual travel behaviour, car demand, or fleet decarbonisation. |

| Data availability | High | Published annually via Transport and Travel in Scotland. |

| Sensitivity to change | Moderate | Survey-based; broad trends detectable, but small annual changes may fall within confidence intervals. |

| Interpretability | High | Easily understood measure with clear direction of travel. |

| Practicality | High | Uses established survey data; no additional collection required. |

TRANSPORT 5 – Mode of travel for longer journeys

| Indicator Title | % of longer journeys (over 5km) made via bus or rail |

|---|---|

| Description | Proportion of journeys over 5km in Scotland made by bus or rail, indicating modal shift towards lower-emission public transport for longer-distance travel. |

| Data Source | Transport and Travel in Scotland (Scottish Household Survey), published annually. |

| Expected trend | Assessed on a directional basis, with success understood as an increasing proportion of longer journeys being made by bus or rail, consistent with reducing car dependency and supporting the transport emissions pathway. |

| Unit | Percentage (%) of journeys over 5km. |

| Limitations and data development | Based on survey data and therefore subject to sampling variability and confidence intervals. Small year-on-year changes may not be statistically significant. The indicator reflects modal share but does not directly measure total vehicle kilometres, occupancy rates, service frequency, or the emissions intensity of buses and trains. The emissions impact depends on substitution away from private car travel and the decarbonisation of public transport fleets. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate –High | Modal shift from car to bus or rail for longer journeys can materially reduce emissions, particularly where substitution is direct. |

| Representativeness | Moderate | Captures behavioural change for longer-distance trips but does not reflect total car demand, freight transport, or fleet electrification. |

| Data availability | High | Published annually via Transport and Travel in Scotland. |

| Sensitivity to change | Moderate | Survey-based measure; broader trends detectable, but small changes may fall within confidence intervals. |

| Interpretability | High | Clear directional interpretation - increasing public transport share is understood as positive. |

| Practicality | High | Uses established survey infrastructure; no additional data collection required. |

TRANSPORT 6 - Zero Emission Vehicle (ZEV) van registration

| Indicator Title | % of new van registrations that are Zero Emission Vehicles |

|---|---|

| Description | Proportion of newly registered light goods vehicles (vans) in Scotland each year that are zero emission vehicles, indicating progress in decarbonising the LGV fleet. |

| Data Source | Department for Transport (DfT) and Driver and Vehicle Licencing Agency (DVLA). |

| Expected trend | Assessed against the expected uptake trajectory consistent with the LGV emissions pathway, with success reflected in increasing uptake of zero emission vans over time. |

| Unit | Percentage (%) of new van registrations. |

| Limitations and data development | The indicator captures new registrations only and does not reflect the emissions performance of the existing van fleet, which may remain in service for extended periods. Emissions reductions materialise gradually through fleet turnover. The measure does not capture changes in total van kilometres travelled, or operational efficiency. Year-on-year fluctuations may reflect market conditions, supply chain constraints, or fiscal incentives rather than sustained structural change. While based on comprehensive administrative data, further development could include monitoring of total fleet composition and van kilometres to strengthen linkage to emissions outcomes. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Fleet electrification is a primary mechanism for reducing LGV tailpipe emissions over time. |

| Representativeness | Moderate | Reflects new fleet turnover but does not capture total van kilometres or the existing fleet stock. |

| Data availability | High | Based on comprehensive DVLA administrative data, published annually by DfT. |

| Sensitivity to change | High | Full population administrative dataset; capable of detecting small year-on-year changes. |

| Interpretability | High | Clear directional interpretation - increasing ZEV share represents progress. |

| Practicality | High | Based on established administrative data; no additional data collection required. |

TRANSPORT 7 - Zero Emission Vehicle (ZEV) bus registration

| Indicator Title | % of new bus registrations that are Zero Emission Vehicles |

|---|---|

| Description | Proportion of newly registered buses in Scotland each year that are zero emission vehicles, indicating progress in decarbonising the bus fleet. |

| Data Source | Department for Transport (DfT) and Driver and Vehicle Licensing Agency (DVLA). |

| Expected trend | Assessed against the expected uptake trajectory consistent with the bus emissions pathway, with success reflected in increasing uptake of zero emission buses over time. |

| Unit | Percentage (%) of new bus registrations. |

| Limitations and data development | The indicator reflects new registrations only and does not capture the emissions performance of the existing bus fleet. Emissions reductions materialise gradually as fleet turnover occurs. The indicator does not represent total distance travelled by fuel type, and year-on-year movements may be volatile due to the relatively small absolute number of ZEV bus registrations. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Transition to zero‑emission vehicles is a primary mechanism for reducing bus tailpipe emissions over time. |

| Representativeness | Moderate | Reflects new fleet turnover but does not capture total kilometres travelled or the emissions performance of the existing fleet. |

| Data availability | High | Based on comprehensive DVLA administrative data, published annually by DfT. |

| Sensitivity to change | High | Full population administrative dataset capable of detecting small year on year changes. |

| Interpretability | High | Direction of success (increase in ZEV share) is clear and easily interpreted. |

| Practicality | High | Uses established administrative data; no additional data collection is required. |

TRANSPORT 8 - Zero Emission Vehicle (ZEV) HGV registration

| Indicator Title | % of new HGV registrations that are Zero Emission Vehicles |

|---|---|

| Description | Proportion of newly registered heavy goods vehicles (HGVs) in Scotland each year that are zero emission vehicles, indicating progress in decarbonising the HGV fleet. |

| Data Source | Department for Transport (DfT) and Driver and Vehicle Licencing Agency (DVLA |

| Expected trend | Assessed against the expected uptake trajectory consistent with the HGV emissions pathway, with success reflected in increasing uptake of zero emission HGVs over time. |

| Unit | Percentage (%) of new HGV registrations. |

| Limitations and data development | The indicator reflects new registrations only and does not capture the emissions performance of the existing HGV fleet, which typically has long asset lifetimes. Emissions reductions materialise gradually as fleet turnover occurs. Current uptake of zero emission HGVs is low and may be influenced by technological availability, infrastructure readiness, and commercial viability. The indicator does not reflect total freight demand, vehicle kilometres travelled, load factors, or operational efficiency. Year-on-year movements may be volatile due to small absolute numbers of ZEV registrations |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Transition to zero emission vehicles is a primary mechanism for reducing HGV tailpipe emissions over time. |

| Representativeness | Moderate | Reflects new fleet turnover but does not capture total freight demand, total kilometres, or the emissions performance of the existing fleet. |

| Data availability | High | Based on comprehensive DVLA administrative data, published annually by DfT. |

| Sensitivity to change | Moderate | Full population dataset; however, low uptake and small absolute numbers may result in volatile percentage movements year-on-year. |

| Interpretability | High | Direction of success (increase in ZEV share) is clear and easily interpreted. |

| Practicality | High | Uses established administrative data; no additional data collection required. |

Business and Industrial Processes

BUSINESS & INDUSTRIAL PROCESSES 1 - ETS Traded Sector Emissions

| Indicator Title | Emissions from industry ETS traded sector (industrial sites only) |

|---|---|

| Description | Total verified greenhouse gas emissions from industrial installations in Scotland covered by the UK Emissions Trading Scheme (UK ETS). This includes emissions from energy-intensive industrial sites subject to carbon pricing regulation and does not include emissions from non-ETS (non-traded) industrial sources. |

| Data Source | UK Emissions Trading Scheme (UK ETS) registry data, published annually by the UK ETS Authority, covering the previous calendar year. |

| Expected trend | Assessed against the expected reduction trajectory for industrial ETS emissions, including a 24% reduction between 2026-2030, consistent with the industry emissions pathway. |

| Unit | Million tonnes of carbon dioxide equivalent (MtCO2e). |

| Limitations and data development | The indicator covers only installations participating in the UK ETS and therefore does not represent total emissions from the industry sector in Scotland. Emissions from non-traded industrial sources are excluded. However, the vast majority of emissions reductions are expected to occur in the traded sector. Changes in emissions may reflect variations in production output, energy prices, or structural economic change, as well as decarbonisation activity. Changes to ETS scope or installation coverage could affect comparability over time. Data are published annually and verified retrospectively, resulting in a reporting lag. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Direct measure of greenhouse gas emissions from a major industrial sub-sector; directly aligned with the emissions pathway. |

| Representativeness | High | Covers the majority of emissions from energy-intensive industrial installations in Scotland under carbon pricing regulation. |

| Data availability | High | Verified administrative emissions data published annually through the UK ETS framework. |

| Sensitivity to change | High | Based on verified installation-level emissions reporting; capable of detecting relatively small changes in emissions levels year-on-year. |

| Interpretability | High | Direct emissions measure (MtCO2e); direction of success (reduction) is clear. |

| Practicality | High | Uses established regulatory reporting; no additional data collection required. |

Energy Supply

ENERGY SUPPLY 1 - Grid Intensity

| Indicator Title | Electricity grid intensity (CO2e per kWh) |

|---|---|

| Description | Average greenhouse gas emissions per unit of electricity generated in Scotland, expressed as grams of CO2 equivalent per kilowatt hour. This reflects the carbon intensity of the electricity system and progress in decarbonising power generation. |

| Data Source | Department for Energy Security and Net Zero (DESNZ) and Scottish Greenhouse Gas Inventory statistics. Published annually. |

| Expected trend | Assessed against the objective of maintaining electricity grid intensity below 40 gCO2e per kilowatt hour. |

| Unit | Grams of CO2 equivalent per kilowatt hour (gCO2e/kWh). |

| Limitations and data development | The indicator reflects territorial electricity generation emissions and does not account for imported electricity or lifecycle emissions associated with infrastructure and fuel production. Annual values may fluctuate due to weather conditions, generation mix variability, plant outages, or interconnector flows. While highly representative of power sector decarbonisation, the measure does not directly capture security of supply, system flexibility, or network constraints. Data is published annually with a reporting lag consistent with the GHG Inventory timetable. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Direct measure of emissions intensity of electricity generation; central to power sector decarbonisation. |

| Representativeness | High | Captures overall generation mix and reflects structural changes in the electricity system. |

| Data availability | Moderate | Published annually by DESNZ. Though requires reconciliation with GHG statistics which are reported with a two year lag |

| Sensitivity to change | High | Based on verified generation and emissions data; capable of detecting meaningful year-on-year changes. |

| Interpretability | High | Clear metric with unambiguous direction of success (lower intensity). |

| Practicality | High | Uses established Accredited Official Statistics; no additional data collection required. |

ENERGY SUPPLY 2 - installed capacity of renewables

| Indicator Title | Installed capacity of renewable generation (GW) |

|---|---|

| Description | Total installed renewable electricity generation capacity in Scotland, measured in gigawatts (GW). This reflects the scale of renewable infrastructure deployed and the potential for low-carbon electricity generation. |

| Data Source | Department for Energy Security and Net Zero (DESNZ) Energy Trends Electricity generation and supply data. Published quarterly. |

| Expected trend | Evaluated on a year-to-year change basis, with success understood as increasing installed renewable generation capacity consistent with decarbonisation of the electricity system. |

| Unit | Gigawatts (GW) of installed renewable generation capacity. |

| Limitations and data development | Installed capacity reflects potential generation rather than actual output and does not account for variability in renewable generation due to weather conditions. The indicator does not directly measure emissions reductions or electricity grid intensity. Deployment may be affected by planning timelines, grid constraints, supply chain factors, or policy changes. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate –High | Expansion of renewable capacity supports decarbonisation of electricity generation and reductions in grid intensity, though capacity alone does not determine emissions. |

| Representativeness | Moderate | Captures a key structural driver of power sector decarbonisation but does not directly reflect dispatch, generation output, fossil backup use, or system integration. |

| Data availability | High | Data published quarterly |

| Sensitivity to change | High | Capacity additions are discrete and measurable; year-on-year increases are clearly observable. |

| Interpretability | High | Direction of success (increase in renewable capacity) is clear and easily understood. |

| Practicality | High | Uses established administrative dataset; no additional data collection required. |

ENERGY SUPPLY 3 - Renewable capacity at planning stages

| Indicator Title | Renewable capacity at planning stages (GW, 3 categories) |

|---|---|

| Description | Total renewable electricity generation capacity in Scotland at different stages of the planning and development process (e.g. in planning, consented, under construction), measured in gigawatts (GW). This reflects the future pipeline of renewable deployment. |

| Data Source | Department for Energy Security and Net Zero (DESNZ) Renewable Energy Planning Database. Published quarterly. |

| Expected trend | Evaluated on a year-to-year change basis, with success understood as maintaining or increasing the volume of renewable capacity progressing through planning and development stages, consistent with future decarbonisation of the electricity system. |

| Unit | Gigawatts (GW) of renewable generation capacity. |

| Limitations and data development | Capacity at planning stages represents potential future generation and does not guarantee project delivery. Projects may be delayed, amended, or cancelled due to financing, grid connection constraints, planning decisions, or market conditions. The indicator does not directly measure emissions reductions or actual generation output. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate | Expansion of the renewable pipeline supports future decarbonisation of electricity generation, though it does not directly reduce emissions. |

| Representativeness | Moderate | Reflects the scale of planned system transformation but does not capture generation output, fossil backup, or system integration factors. |

| Data availability | High | Based on administrative planning data, published annually |

| Sensitivity to change | High | Changes in pipeline capacity are discrete and measurable; year-on-year movements are clearly observable. |

| Interpretability | Moderate | Conceptually clear, but interpretation requires understanding that pipeline capacity does not equate to operational generation. |

| Practicality | High | Uses established administrative dataset; no additional data collection required. |

ENERGY SUPPLY 4 - Loss of load expectation

| Indicator Title | Loss of Load Expectation (hours per year) |

|---|---|

| Description | The expected number of hours per year in which electricity demand is forecast to exceed available generation capacity across Great Britain. This indicator reflects system adequacy and security of supply during the transition to a low-carbon electricity system. |

| Data Source | National Energy System Operator (NESO), Winter Outlook Report. Published annually. |

| Expected trend | Assessed against the reliability standard for Great Britain, with success reflected in maintaining Loss of Load Expectation below 3 hours per year. |

| Unit | Hours per year. |

| Limitations and data development | The indicator reflects a modelled expectation rather than observed outages. It applies at a Great Britain level rather than Scotland-specific system adequacy. It does not measure emissions or renewable deployment directly but provides context on the reliability of the electricity system. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Low –Moderate | Does not directly measure emissions; indirectly relevant as maintaining security of supply supports sustainable decarbonisation of the electricity system. |

| Representativeness | Moderate | Reflects overall system adequacy across Great Britain but not Scotland-specific emissions or generation mix. |

| Data availability | High | Published annually by NESO in the Winter Outlook Report; accessible and regularly updated. |

| Sensitivity to change | Moderate | Based on modelling assumptions; meaningful changes detectable, but year-on-year movements may reflect scenario updates rather than structural change. |

| Interpretability | Moderate | Concept requires explanation; interpretation depends on understanding the reliability standard (3-hour threshold). |

| Practicality | High | Uses established modelling and reporting processes; no additional data collection required. |

ENERGY SUPPLY 5 - household waste incinerated

| Indicator Title | Household waste incinerated |

|---|---|

| Description | The amount of Scottish household waste incinerated, expressed in tonnes. |

| Data Source | SEPA annual statistics on household waste generated and managed. |

| Expected trend | Assessed against forecast household waste incineration rates, which has been used to provide an estimate of future energy from waste emissions in the CCP. Household waste incinerated is projected to increase until 2028 (when SEPA will commence full enforcement of the biodegradable municipal waste landfill ban) and then gradually reduce from 2028 onwards. |

| Unit | Tonnes of incinerated waste. |

| Limitations and data development | The indicator captures household waste incinerated only and does not account for waste composition change or commercial/industrial waste, which could mask any changes in emissions. Future development could look to take into account the different types of household waste incinerated and their impact on emissions. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate | Linked to Energy from Waste (EfW) emissions; higher tonnage of household waste incinerated generally associates with increases to the greenhouse gases released associated with EfW |

| Representativeness | Moderate | Reflects a significant portion of waste being incinerated but excludes commercial/industrial waste, so only partially represents sources of EfW emissions. |

| Data availability | High | Published annually by SEPA. |

| Sensitivity to change | Moderate | Sensitive to changes in tonnes of household waste incinerated, but less able to detect shifts from waste composition, efficiency or changes to the amount of commercial/industrial waste incinerated. |

| Interpretability | Moderate |

Interpretation requires some understanding because, as a result of the biodegradable municipal waste landfill ban, an increase in household waste incinerated is expected in the short term. Direction of success would be lower incineration from 2028 levels in the long term. |

| Practicality | High | Uses established administrative dataset; no additional data collection required. |

Land Use, Land Use Change and Forestry (LULUCF)

LULUCF 1 - woodland creation

| Indicator Title | Hectares of woodland created |

|---|---|

| Description | Total area of new woodland created in Scotland each year, measured in hectares. This reflects progress in expanding forest cover and increasing long-term carbon sequestration consistent with the LULUCF emissions pathway. |

| Data Source | Forestry Statistics (published by Scottish Forestry). Published annually. |

| Expected trend | Assessed against the target of planting approximately 78,000 hectares of new woodland between 2026–2030, consistent with the LULUCF emissions pathway. |

| Unit | Hectares (ha) of new woodland created per year. |

| Limitations and data development | Woodland creation reflects area planted rather than immediate carbon sequestration, as sequestration benefits accrue over time as forests mature. The indicator does not capture woodland quality, species mix, permanence, or management practices, all of which influence long-term carbon outcomes. Delivery may be affected by land availability, supply chain capacity, weather conditions, and funding constraints. While data are robust and administratively recorded, annual planting levels may fluctuate due to project timing. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Woodland creation increases long-term carbon sequestration and is central to achieving LULUCF emissions removals. |

| Representativeness | High | Directly reflects a primary driver of emissions removals within the LULUCF pathway. |

| Data availability | High | Published annually through official forestry statistics based on administrative records. |

| Sensitivity to change | High | Area planted is directly measured; annual changes clearly observable. |

| Interpretability | High | Clear directional interpretation — higher planting consistent with pathway delivery. |

| Practicality | High | Based on established administrative reporting; no additional data collection required. |

LULUCF 2 - Peatland restoration

| Indicator Title | Hectares of peatland restored |

|---|---|

| Description | Total area of degraded peatland restored in Scotland each year, measured in hectares. This reflects progress in reducing emissions from degraded peatlands and enhancing long-term carbon storage, consistent with the LULUCF emissions pathway. |

| Data Source | Peatland ACTION data produced by NatureScot. Published annually. |

| Expected trend | Assessed progress toward restoring 400,000 hectares of peatland by 2040, in line with the LULUCF emissions pathway. |

| Unit | Hectares (ha) of peatland restored per year. |

| Limitations and data development |

Restoration area reflects activity undertaken rather than immediate emissions reductions, which depend on site condition, hydrology, and restoration effectiveness. Emissions benefits may take time to materialise and vary across sites. The indicator does not capture long-term maintenance, condition monitoring, or potential re-degradation. Delivery may be influenced by weather, contractor capacity, land access, and funding. Data are based on administrative reporting and are subject to annual publication cycles. This data only captures restoration undertaken via Peatland ACTION. While this represents the majority of restoration in Scotland, other restoration efforts take place, whether through alternative grant schemes or privately funded means. Recent evidence suggests that the area of grassland on peat in Scotland has been significantly overestimated in the UK GHG Inventory. Improved mapping is underway which may result in a baseline revision if any future plan if formally ratified by the GHG Inventory. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Restoration reduces emissions from degraded peatlands and contributes directly to LULUCF emissions reductions. |

| Representativeness | High | Directly reflects a primary driver of emissions reduction within the peatland sub-sector. |

| Data availability | High | Published annually via NatureScot administrative reporting. |

| Sensitivity to change | High | Restoration area is directly measured; year-on-year changes clearly observable. |

| Interpretability | High | Clear directional interpretation - increased restoration consistent with pathway delivery. |

| Practicality | High | Based on established programme reporting; no additional data collection required. |

Buildings (Residential and Public)

BUILDINGS 1 - LZDEH conversions

| Indicator Title | Number of buildings using low and zero direct emissions heating (LZDEH) systems |

|---|---|

| Description | Total number of buildings in Scotland using low and zero direct emissions heating systems (e.g. heat pumps, direct electric heating), reflecting progress in decarbonising heating. |

| Data Source | Scottish House Condition Survey (SHCS), Accredited Official Statistics. Published annually (domestic properties). Non-Domestic Analytics (NDA), dataset maintained by Energy Savings Trust (EST), updated annually (non-domestic properties). |

| Expected trend | Assessed against the target of 35,000 additional building conversions to LZDEH systems over 2026-2030, consistent with the Buildings emissions pathway. |

| Unit | Number of buildings. |

| Limitations and data development |

SCHS estimates are derived from survey data and therefore subject to sampling variability and confidence intervals. Small year-on-year changes may not be statistically distinguishable. The indicator measures heating system type but does not capture actual energy consumption, system efficiency, hybrid systems, or user behaviour. Emissions reductions depend on electricity grid decarbonisation and building fabric performance. Data are published annually but reflect survey-based estimation rather than full administrative coverage. NDA data is maintained by EST and is newer, experimental data which is subject to revision. It uses EPC register data and other sources of data to track the heating system of non-domestic buildings. Modelling is used to fill gaps due to a lack of coverage in key datasets such as the non-domestic EPC register. The dataset is updated annually and is not publicly available. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Decarbonisation of buildings’ heating systems is a primary driver of emissions reductions within the Buildings sector. |

| Representativeness | High | Directly reflects the primary driver of emissions reduction within the buildings pathway |

| Data availability | Moderate | Domestic data based on Accredited Official Statistics and published annually (Non-domestic data, representing a small share of total buildings, updated annually and not published). Survey-based methodology and sample size constrain timeliness and precision for small changes. |

| Sensitivity to change | Moderate | Broad trends detectable over time, but small annual increases may fall within confidence intervals. |

| Interpretability | High | Direction of success (increase in LZDEH uptake) is clear and easily understood. |

| Practicality | High | Uses established survey infrastructure; no additional data collection required. |

BUILDINGS 2 - EPC C attainment

| Indicator Title | Number of homes with EPC C or above (or equivalent) |

|---|---|

| Description | Total number of domestic properties in Scotland with an Energy Performance Certificate (EPC) rating of C or above (or equivalent), reflecting improvements in energy efficiency and building fabric performance. |

| Data Source | Scottish House Condition Survey (SHCS), Accredited Official Statistics. Published annually. |

| Expected trend | Assessed against the target of 135,000 additional domestic properties achieving EPC C+ (or equivalent) over 2026-2030, consistent with the Buildings emissions pathway. |

| Unit | Number of domestic properties. |

| Limitations and data development | Estimates are derived from survey data and therefore subject to sampling variability and confidence intervals. Small year-on-year changes may not be statistically distinguishable. The indicator reflects theoretical modelled energy performance rather than actual energy consumption or occupant behaviour. EPC ratings may not fully capture building condition, heating system efficiency, or retrofit quality. Data are published annually but are survey-based rather than comprehensive administrative records. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Moderate | Improving building fabric efficiency reduces energy demand and is a core driver of emissions reduction in the residential sector. However, the role building fabric efficiency plays is mostly in making clean heat technologies competitive and therefore incentivising the replacement of gas boilers. |

| Representativeness | Moderate | Reflects an important driver of emissions reduction in the residential sector but does not capture heating system transition or behavioural factors that also determine overall emissions performance. |

| Data availability | Moderate | Based on Accredited Official Statistics and published annually; however, survey-based methodology and sample size limit timeliness and precision for small changes. |

| Sensitivity to change | Moderate | Broad trends detectable over time, but small annual improvements may fall within confidence intervals. |

| Interpretability | High | Clear directional interpretation — increasing number of EPC C+ (or equivalent) homes represents progress. |

| Practicality | High | Uses established survey infrastructure; no additional data collection required. |

Waste Management

WASTE MANAGEMENT 1 - Biodegradable municipal waste landfilled

| Indicator Title | Tonnage of biodegradable municipal waste (BMW) landfilled |

|---|---|

| Description | Total tonnage of biodegradable municipal waste (including household and similar residual waste) sent to landfill in Scotland each year. This reflects progress towards eliminating landfill disposal of biodegradable waste and reducing methane emissions from the waste sector. |

| Data Source | Scottish Environment Protection Agency (SEPA), Waste landfilled in Scotland statistics. Published annually. |

| Expected trend | Assessed against the projected reduction of biodegradable municipal waste sent to landfill to zero by 2028, consistent with statutory landfill restrictions and the waste emissions pathway. |

| Unit | Tonnes of biodegradable municipal waste landfilled per year. |

| Limitations and data development | Data are derived from regulatory reporting by waste operators and are subject to annual publication cycles. The indicator captures landfill disposal, the main source of greenhouse gas generation in the Waste Management sector, but does not cover landfill gas capture, which acts to reduce landfill emissions. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Landfilled biodegradable waste generates methane, a potent greenhouse gas; reducing landfill volumes directly reduces emissions. |

| Representativeness | High | Captures the principal source of waste-sector methane emissions targeted by policy. |

| Data availability | Moderate –High | Based on regulatory reporting and published annually by SEPA; subject to annual publication lag (typically 10 months after reporting year) but comprehensive in coverage. |

| Sensitivity to change | High | Based on reported tonnage data; capable of detecting small changes in landfill volumes. |

| Interpretability | High | Direction of success (reduction towards zero) is clear and aligned with a defined policy endpoint. |

| Practicality | High | Uses established regulatory reporting; no additional data collection required. |

WASTE MANAGEMENT 2 - Waste tonnage generated

| Indicator Title | Waste tonnage generated (excluding soils and mineral waste from construction & demolition) |

|---|---|

| Description | Total tonnage of waste generated in Scotland each year, excluding soils and mineral waste from construction and demolition activities. This reflects progress in reducing overall waste generation consistent with circular economy and emissions reduction objectives. |

| Data Source | Scottish Environment Protection Agency (SEPA), Waste from all sources. Published annually. |

| Expected trend | Assessed on a downward trend basis, with success understood as a sustained reduction in total waste generated over time. |

| Unit | Tonnes of waste generated per year. |

| Limitations and data development | Excludes soils and mineral waste from construction and demolition, which represent a significant proportion of total waste by tonnage; therefore, it does not capture the full waste system. It excludes these soil and mineral wastes because they are generally landfilled with low emissions, but show significant year-to-year variation which can obscure the overall trend. Other than this, the measure does not differentiate by waste type, carbon impact, or treatment route. Emissions outcomes depend on how waste is managed (e.g. recycled, incinerated, landfilled). Data are based on regulatory reporting and subject to annual publication lag. Economic conditions and population changes may influence total waste generation independent of policy effectiveness. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | Low - Moderate | The indicator gives an overall picture regarding progress towards waste reduction rather than a direct link to emissions. |

| Representativeness | High | Covers all sectors (household; commercial & industrial; construction & demolition) although it excludes soil and mineral waste from construction & demolition for the reasons given above. |

| Data availability | Moderate - High | Based on regulatory reporting and published annually by SEPA; subject to annual publication lag – typically 15 months after reporting year. |

| Sensitivity to change | High | Based on reported tonnage data; capable of detecting year-on-year changes. |

| Interpretability | High | Direction of success (reduction in total waste generated) is clear. |

| Practicality | High | Uses established regulatory reporting; no additional data collection required. |

Agriculture

AGRICULTURE 1 - Engagement with farm advisory service

| Indicator Title | Engagement with Farm Advisory Services on environmental issues and climate change |

|---|---|

| Description | Increased engagement with Farm Advisory Services to ensure more farmers, crofters, land managers and other primary food producers are aware of the benefits and practicalities of cost effective climate mitigation measures. |

| Data Source | Farm Advisory Service annual and lifetime reports. |

| Expected trend | Progress towards maintaining and increasing higher levels of engagement over time. |

| Unit | Percentage change year on year. |

| Limitations and data development | Indicator captures engagement with a specific advisory programme and hence is a partial indicator of wider knowledge and skills amongst farmers and crofters. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Engagement with advisory services is a driver of climate change related skill and knowledge transfer. |

| Representativeness | Moderate | Captures engagement with the service, but does not necessarily capture wider skills and knowledge across farmers, crofters, land managers and other primary food producers. |

| Data availability | High | Monitoring data are updated annually. Farm Advisory Service (FAS) data are published in FAS annual reports. This published source data can be broken-down to align with the CCP reporting period. |

| Sensitivity to change | Moderate | Broad trends detectable; however, smaller year-on-year changes may reflect survey variability or weather-related fluctuations. |

| Interpretability | High | Simple percentage measure with trend to help evaluate direction of travel. |

| Practicality | High | No additional cost or resource requirements – monitoring and evaluation is built into the contracting for the Farm Advisory Service. |

AGRICULTURE 2 - Use of nitrogen fertilisers

| Indicator Title | Use of nitrogen fertilisers |

|---|---|

| Description | Quantities of nitrogen fertilisers used in Scotland. |

| Data Source | British Survey of Fertiliser Practice(BSFP). Published annually. |

| Expected trend | Assessed on a downward trend basis, with success understood as a sustained reduction in nitrogen fertiliser use. |

| Unit | Kilotonnes of nitrogen (kt N) applied per year. |

| Limitations and data development | Published annually as accredited official statistics, based on survey data. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Falling nitrogen usage is a key policy outcome. |

| Representativeness | High | Quantities of nitrogen fertiliser used is a driver of nitrogen usage in agriculture. |

| Data availability | High |

Based on annual survey data; published annually as accredited official statistics. Subject to survey-based limitations and reporting lag – data for crop years are published with around a one year lag. For example, data for crop year 2023-24 (fertiliser consumption period July to June) were published in July 2025. |

| Sensitivity to change | Moderate | Broad trends detectable; however, smaller year-on-year changes may reflect survey variability or weather-related fluctuations. |

| Interpretability | High | Simple percentage measure with trend to help evaluate direction of travel. |

| Practicality | High | Based on existing published data tables, minimal additional resource required. |

AGRICULTURE 3 - Application rates of nitrogen fertilisers

| Indicator Title | Overall nitrogen application rates (kg/ha) |

|---|---|

| Description | Total overall application rates of nitrogen fertiliser per hectare of agricultural land in Scotland. |

| Data Source | British Survey of Fertiliser Practice (BSFP). Published annually. |

| Expected trend | Progress towards reducing average application rates over time. |

| Unit | Kilograms of nitrogen per hectare (kg/ha). |

| Limitations and data development | Published annually as accredited official statistics, based on survey data. |

| Criterion | Assessment | Rationale |

|---|---|---|

| Relevance | High | Falling application rates of Nitrogen usage related directly to key policy outcomes. |

| Representativeness | High |

Precision application of fertilisers can help to reduce greenhouse gas emissions. The overall application rate is a measure of the fertiliser nutrient application rate over the sown area (the area of a field that has been planted with a crop or grass) of all fields, irrespective of whether they received dressing of that nutrient or not. Excludes headlands, field margins, buffer strips and other agri-environment features. |

| Data availability | High |

Based on annual survey data; published annually as accredited official statistics. Subject to survey-based limitations and reporting lag – data for calendar years are published the following summer. For example, data for 2024 were published in July 2025. |

| Sensitivity to change | Moderate | Broad trends detectable; however, smaller year-on-year changes may reflect survey variability or weather-related fluctuations. |

| Interpretability | High | Simple percentage measure with trend to help evaluate direction of travel. |