Scotland's Climate Change Plan: 2026–2040

This Climate Change Plan (CCP) sets out the policies and proposals we will take forward to enable our carbon budgets to be met between 2026 and 2040.

Sectoral Contributions

Below, this section provides a summary of some of the key policies for each sector to meet our carbon budgets. It outlines the emissions pathway for each sector covered by the plan, some of the key actions which will be taken to achieve it and the economic opportunities and benefits this action will support.

Further detail for each sector is set out in the Sectoral Annexes and the Monitoring and Analytical Annex.

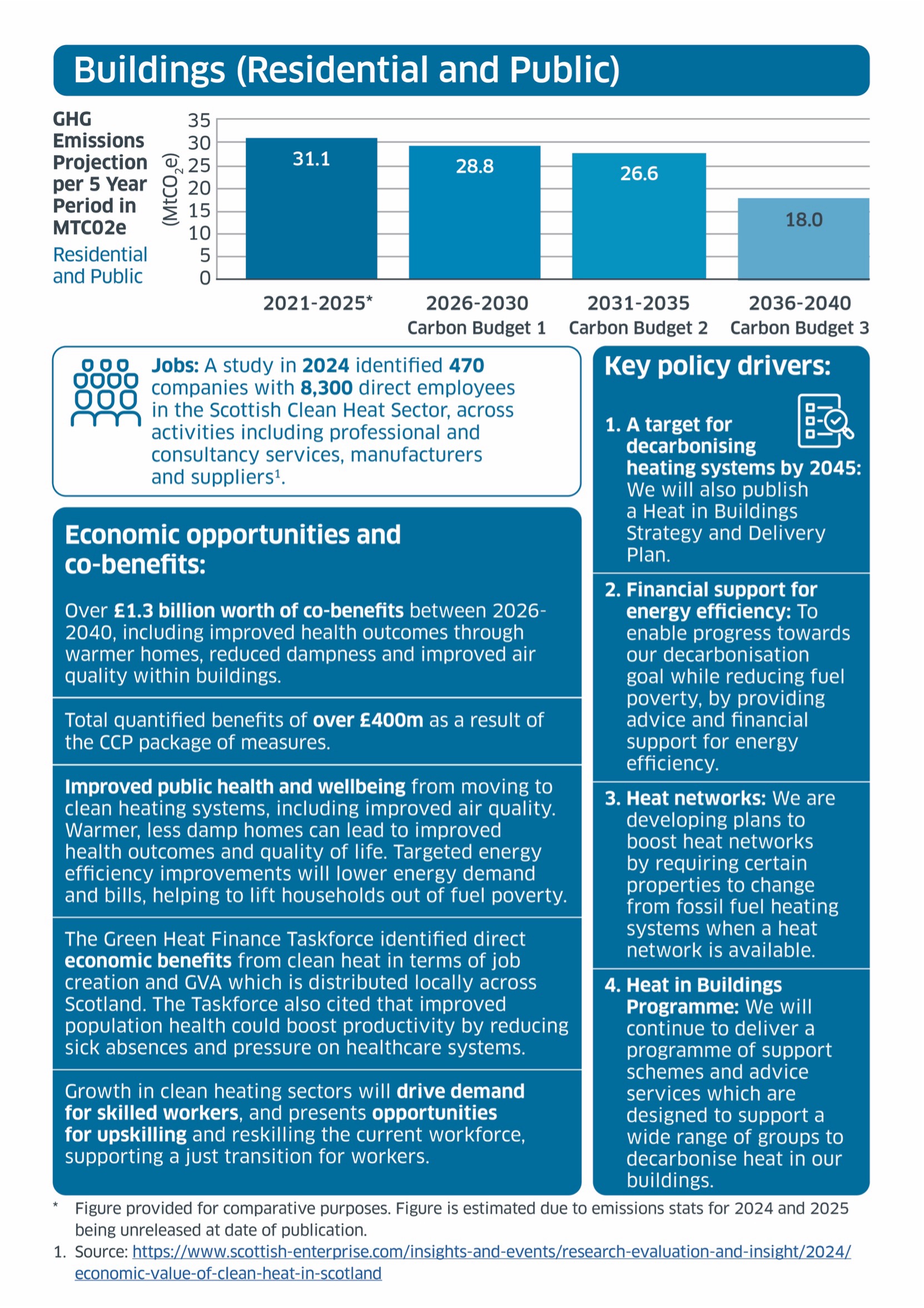

Buildings (Residential and Public)

GHG Emissions Projection per 5 year period in MTCO2e Residential and Public

2021-2025* - 31.1

2026-2030 Carbon Budget 1 - 28.8

2031-2035 Carbon Budget 2 - 26.6

2031-2035 Carbon Budget 3 - 18.0

Jobs: a study in 2024 indentified 470 companies with 8,300 direct employees in the Scottish Clean Heat Sector, across activities including professional and consultancy services, manufacturers and suppliers1.

Economic opportunities and co-benefits:

Over £1.3 billion worth of co-benefits between 2026-2040 including imporved health outcomes through warmer homes, reduced dampness and improved air quality within buildings.

Total quantified benefits of over £400m as a result of the CCP package of measures.

Improved public health and wellbeing from moving to clean heating systems, including improved air quality. Warmer, less damp homes can lead to improved health outcomes and quality of life. Targeted energy efficiency improvements will lower energy demand and bills, helping lift households out of fuel poverty.

The Green Heat Finance Taskforce indentified direct economic benefits from clean heat in terms of job creatin and GVA which is distributed locally across Scotland. The taskforce also cited that improved population health could boost productivity by reducing sick absences and pressure on healthcare systems.

Growth in clean heating sectors will drive demand for skilled workers, and presents opportunities for upskilling and reskilling the current workforce, supporting a just transition for workers

Key policy drivers:

1. A target for decarbonising heating systems by 2045: We will also publish a Heat in Buildings Strategy and Delivery Plan.

2. Financial support for energy efficiency: To enable progress towards our decarbonisation goal while reducing fuel poverty, by providing advice and financial support for energy efficiency.

3. Heat networks: We are developing plans to boost heat networks by requiring certain properties to change from fossil fuel heating systems when a heat network is available.

4. Heat in Buildings Programme: We will continue to deliver a programme of support schemes and advice services which are designed to support a wide range of groups to decarbonise heat in our buildings.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

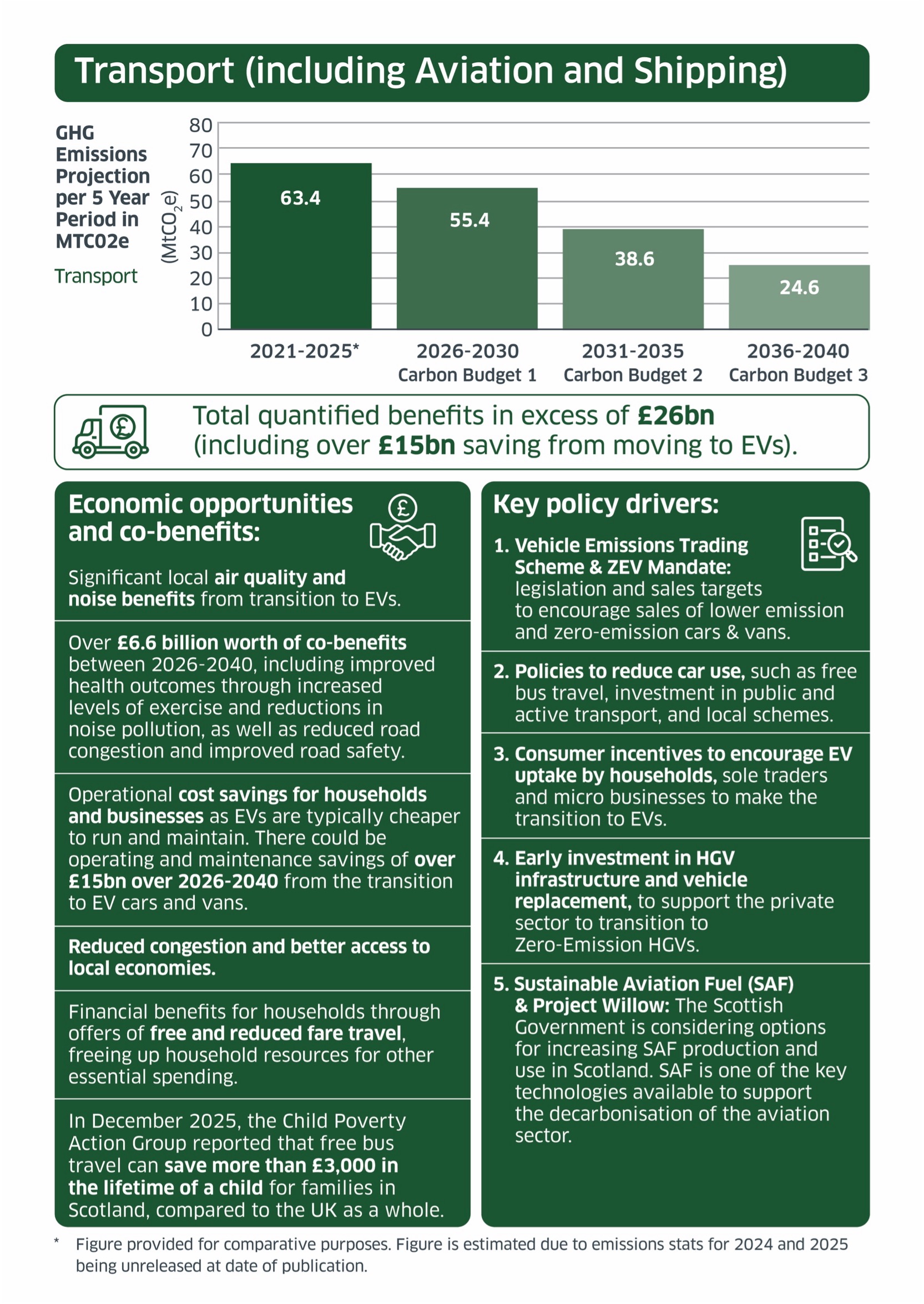

Transport (including Aviation and Shipping)

GHG Emissions Projection per 5 year period in MTCO2e Transport

2021-2025* - 63.4

2026-2030 Carbon Budget 1 - 55.4

2031-2035 Carbon Budget 2 - 38.6

2031-2035 Carbon Budget 3 - 24.6

Total quantified benefits in excess of £26bn (including over £15bn saving from moving to EVs).

Economic opportuties and co-benefits:

Significant local air quality and noise benefits from transition to EVs.

Over £6.6 billion worth of co-benefits between 2026-2040, including improved health outcomes through increased levels of excercise and reductions in noise pollution, as well as reduced road congestion and improved road safety.

Operational cost savings for households and businesses as EVs are typically cheaper to run and maintain. There could be operating and maintainance savings of over £15bn over 2026-2040 from the transition to EV cars and vans.

Reduced congestion and better access to local economies.

Financial benefits for households through offers of free and reduced fare travel, freeing up household resources for other essential spending.

In December 2025, the Child Poverty Action Group reported that free bus travel can save more than £3,000 in the lifetime of a child for families in Scotland, compared to the UK as a whole.

Key policy drivers:

1. Vehicle Emissions Trading Scheme & ZEV Mandate: legislation and sales targets to encourage sales of lower emission and zero-emission cars & vans.

2. Policies to reduce car use, such as free bus travel, investment in public and active transport, and local schemes.

3. Consumer incentives to encourage EV uptake by households, sole traders and micro businesses to make the transition to EVs.

4. Early investment in HGV infrastructure and vehicle replacement, to support the private sector to transition to Zero-Emissions HGVs.

5. Sustainable Aviation Fuel (SAF) & Project Willow: The Scottish Government is considering options for increasing SAF production and use in Scotland. SAF is one key technologies available to support the decarbonisation of the aviation sector.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

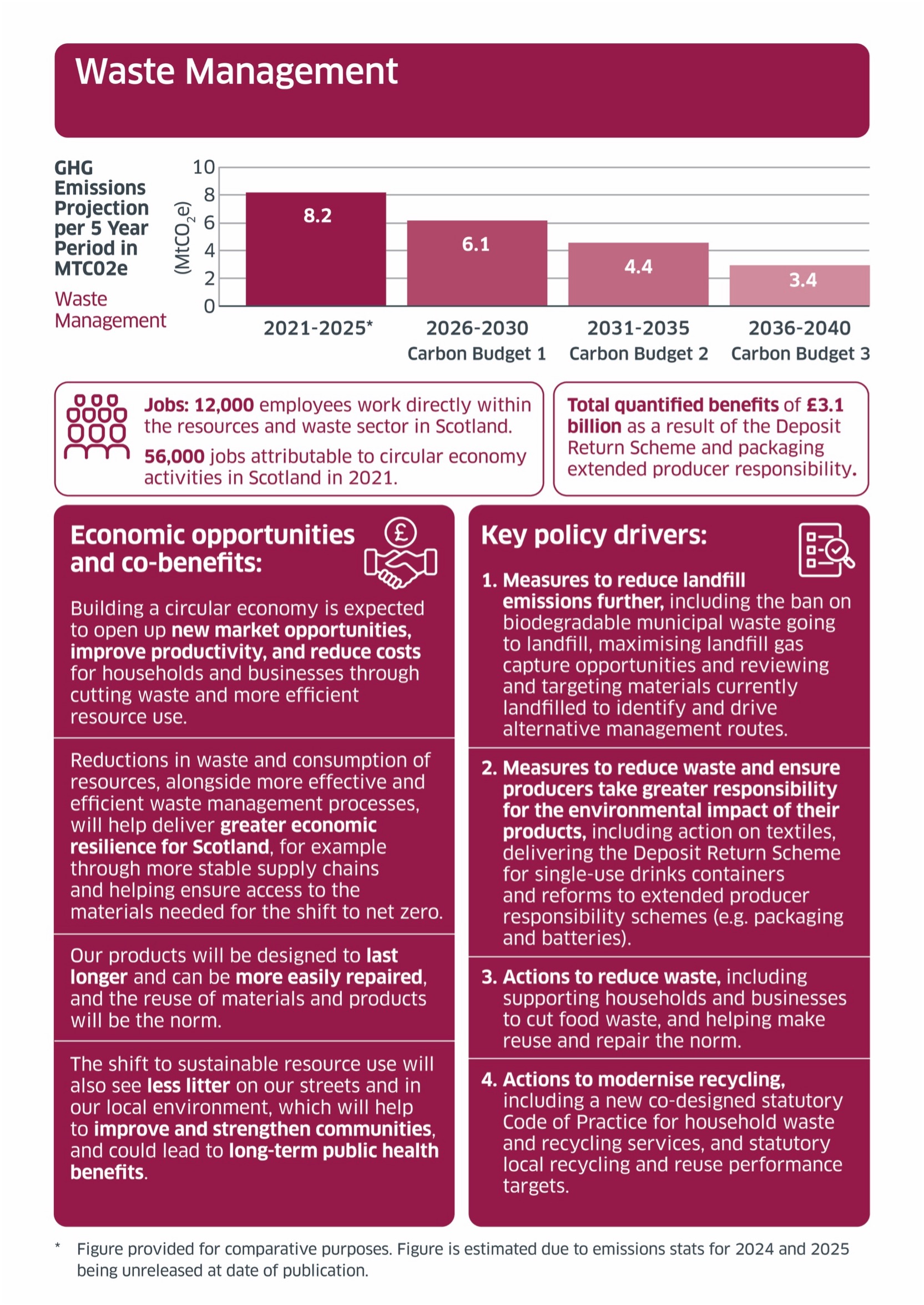

Waste Management

GHG Emissions Projection per 5 year period in MTCO2e Waste Management

2021-2025* - 8.2

2026-2030 Carbon Budget 1 - 6.1

2031-2035 Carbon Budget 2 - 4.4

2031-2035 Carbon Budget 3 - 3.4

Job: 12,000 employees work directly within the resources and waste sector in Scotland.

56,000 jobs attributed to circular economy activities in Scotland in 2021.

Total quantified benefits of £3.1 billion as a result of the Deposit Return Scheme and packaging extended producer responsibility.

Economic opportunities and co-benefits:

Building a circular economy is expected to open up a new market opportunites, improve productivity, and reduce costs for households and businesses through cutting waste and more efficient resource use.

Reductions in waste and consumption of resources, alongside more effective and efficient waste management processes, will help deliver greater economic resilience for Scotland, for example through more stable supply chains and hlping ensure access to the materials needed for the shift to net zero.

Our products will be designed to last longer and can be more easily repaired, and the reuse of materials and products will be the norm.

The shift to sustainable resource use will also see less litter on our streets and in our local environment, which will help to improve and strengthen communities, and could lead to long-term public health benefits.

Key policy drivers:

1. Measures to reduce landfill emissions further, including the ban on biodegradable municipal waste going to landfill, maximising landfill gas capture opportunities and reviewing and targeting materials currently landfilled to indentify and drive alternative management routes.

2. Measure to reduce waste and ensure producers take greater responsibility for the environmental impact of their products, including action on textiles, delivering the Deposit Return Scheme for single use containers and reforms to extend producer responsibility schemes (e.g. packaging and batteries).

3. Actions to reduce waste, including supporting households and businesses to cut food waste, and helping make reuse and repair the norm.

4. Actions to modernise recyciling, including a new co-designed statuory Code of Practice for household waste and recycling services, and statuory local recycling and reuse performance targets.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

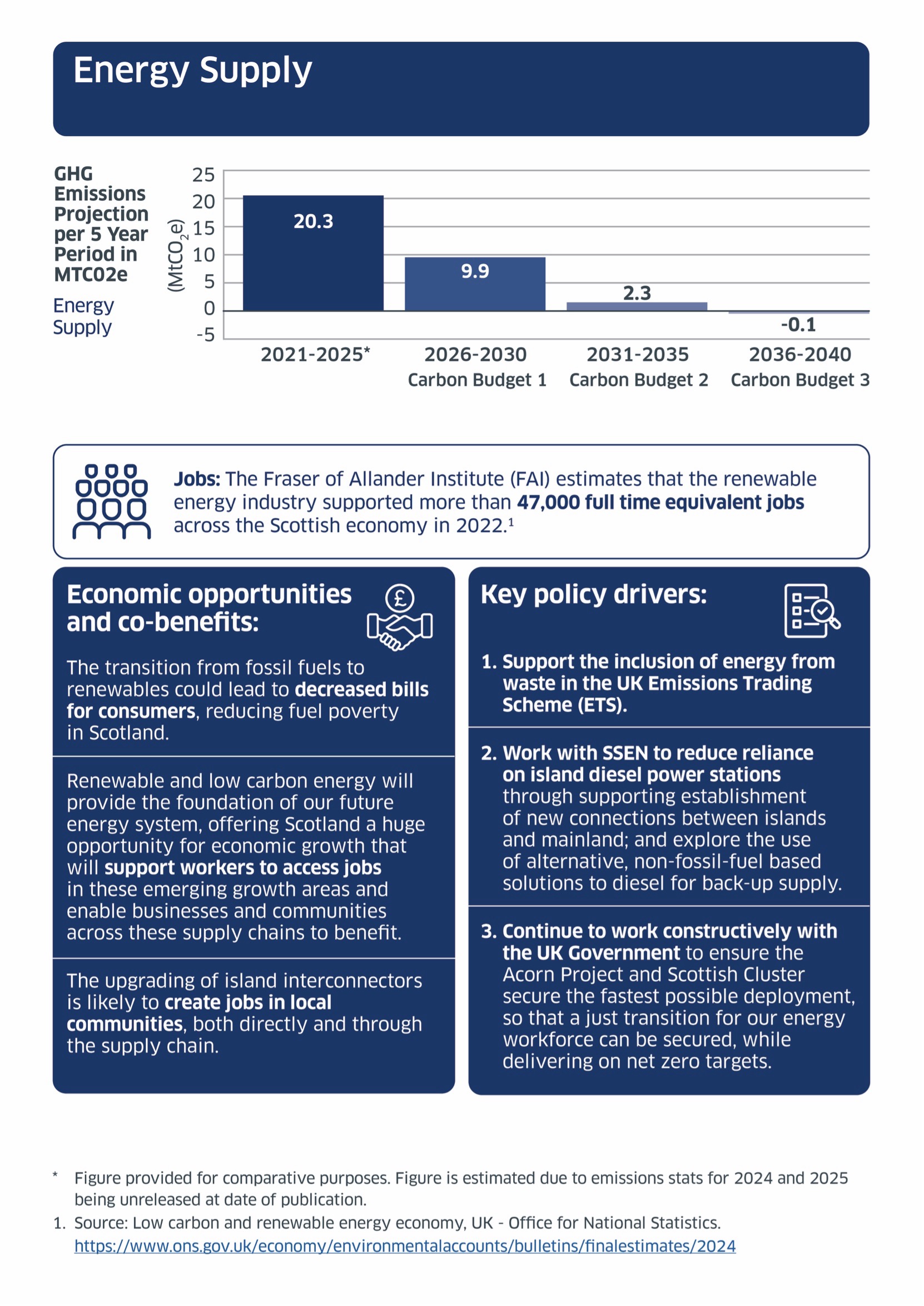

Energy Supply

GHG Emissions Projection per 5 year period in MTCO2e Energy Supply

2021-2025* - 20.3

2026-2030 Carbon Budget 1 - 9.9

2031-2035 Carbon Budget 2 - 2.3

2031-2035 Carbon Budget 3 - -0.1

Jobs The Fraser of Allander Institute (FAI) estimates that the reneable energy industry supported more than 47,000 full time equivalent jobs across the Scottish Economy in 2022.1

Economic opportunities and co-benefits:

The transition from fossil fuels to renewables could leas to decreased bills for consumers, reducing fuel poverty in Scotland.

Renewable and low carbon energy will provide the foundation of our future energy system, offering Scotland a huge opportunity for economic growth that will support workers to access jobs in these emerging growth areas and enable businesses and communities across these supply chains to benefit.

The upgrading of island interconnectors is likely to create jobs in local communities, both directly and through the supply chain.

Key policy drivers:

1. Support the inclusion of energy from waste in the UK Emissions Trading Schee (ETS).

2. Work with SSEN to reduce reliance on island diesel power stations through supporting establishment of new connections between islands and mainland; and explore the use of alternative, non-fossil-fuel based solutions to diesel for back-up supply.

3. Continue to work constructively with the UK government to ensure the Acorn Project and Scottish Cluster secure the fastest possible deployment, so that a just transitionfor our energy workforce can be secured, while delivering on net zero targets.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

1 Source: Low carbon and renewable energy economy, UK - Office for National Statistics. https://www.ons.gov.uk/economy/environmentalaccounts/bulletins/finalestimates/2024

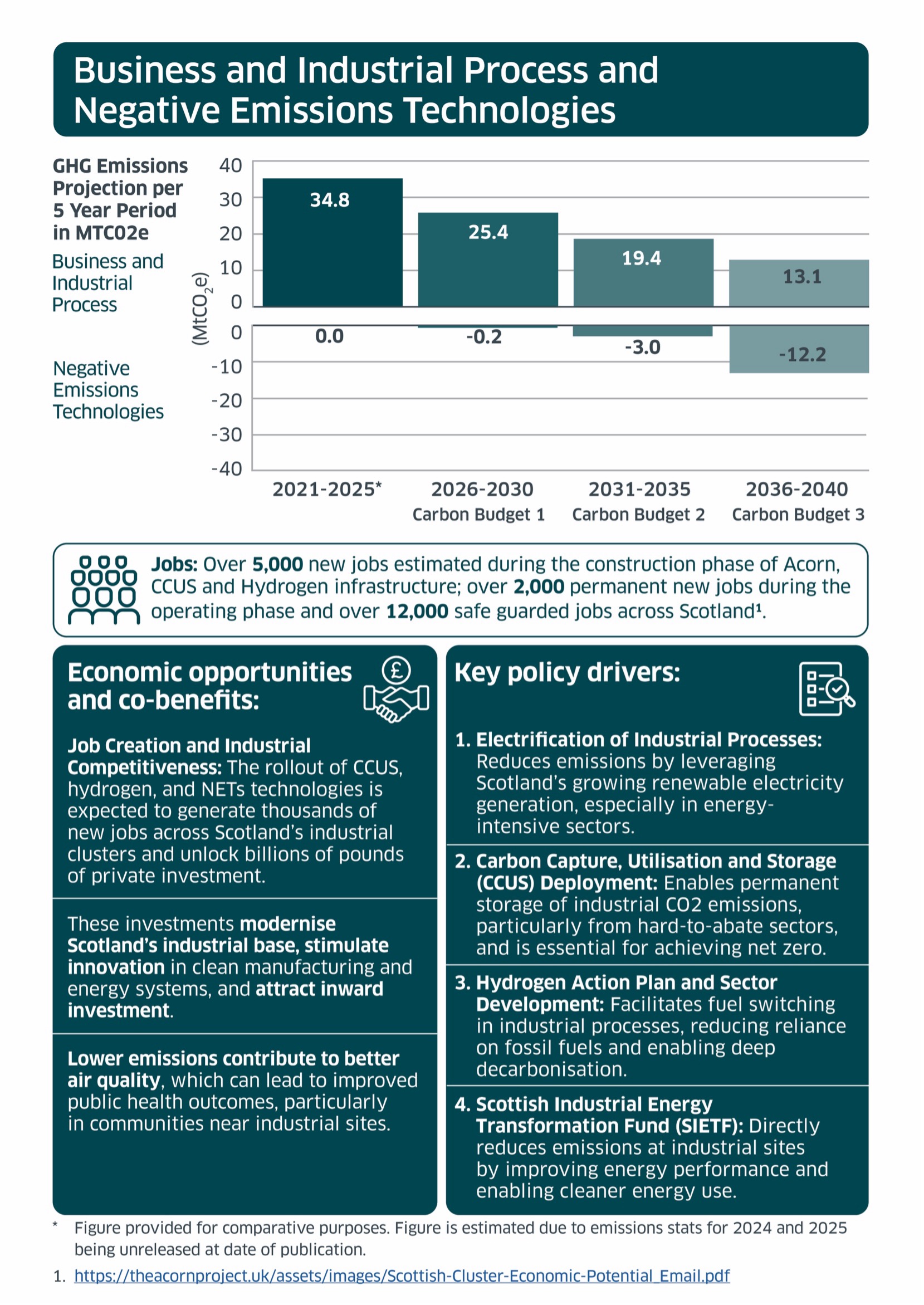

Business and Industrial Process and Negative Emissions Technologies

GHG Emissions Projection per 5 year period in MTCO2e Business and Industrial Process

2021-2025* - 31.8

2026-2030 Carbon Budget 1 - 25.4

2031-2035 Carbon Budget 2 - 19.4

2031-2035 Carbon Budget 3 - 13.1

GHG Emissions Projection per 5 year period in MTCO2e Negative Emissions Technologies

2021-2025* - 0.0

2026-2030 Carbon Budget 1 - -0.2

2031-2035 Carbon Budget 2 - -3.0

2031-2035 Carbon Budget 3 - -12.2

Jobs: Over 5,000 new jobs estimated during the construction phase of Acorn, CCUS nd Hydrogen infrastructure; over 2,000 permanent new jobs during the operating phase and over 12,000 safe guarded jobs across Scotland.1

Economic opportunities and co-benefits

Job Creation and Industial Competitiveness: The rollout of CCUS, hydrogen, and NETs technologies is expected to generate thousands of new jobs accross Scotland;s industrial clusters and unlock billions of pounds of private investment.

These investments modernise Scotland's industrial base, stimulate innovation in clean manufacturing and energy systems, and attract inward investment.

Lower emissions contribute to better air quality, which can lead to improved public health outcomes, particularly in communites near industrial estates.

Key policy drivers:

1. Electrification of Industrial Processes: Reduces emissions by leveraging Scotland's growing renewable electricity generation, especially in energy-intensive sectors.

2. Carbon Capture, Ultilisation and Storage (CCUS) Deployment: Enables permanent storage of industrial CO2 emissions, particularly from hard-to-abate sectors, and is essential for achieving net zero.

3. Hydrogen Action Plan and Sector Development: Facilitates fuel switching in industrial processes, reducing reliance on fossil fuels and enabling deep carbonisation.

4. Scottish Industrial Energy Transformation Fund (SIETF): Directly reduces emissions at industrial sites by improving energy performance and enabling cleaner energy use.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

1 Source: https://www.theacornproject.uk/assets/images/Scottish-Cluster-Economic-Potential_Email.pdf

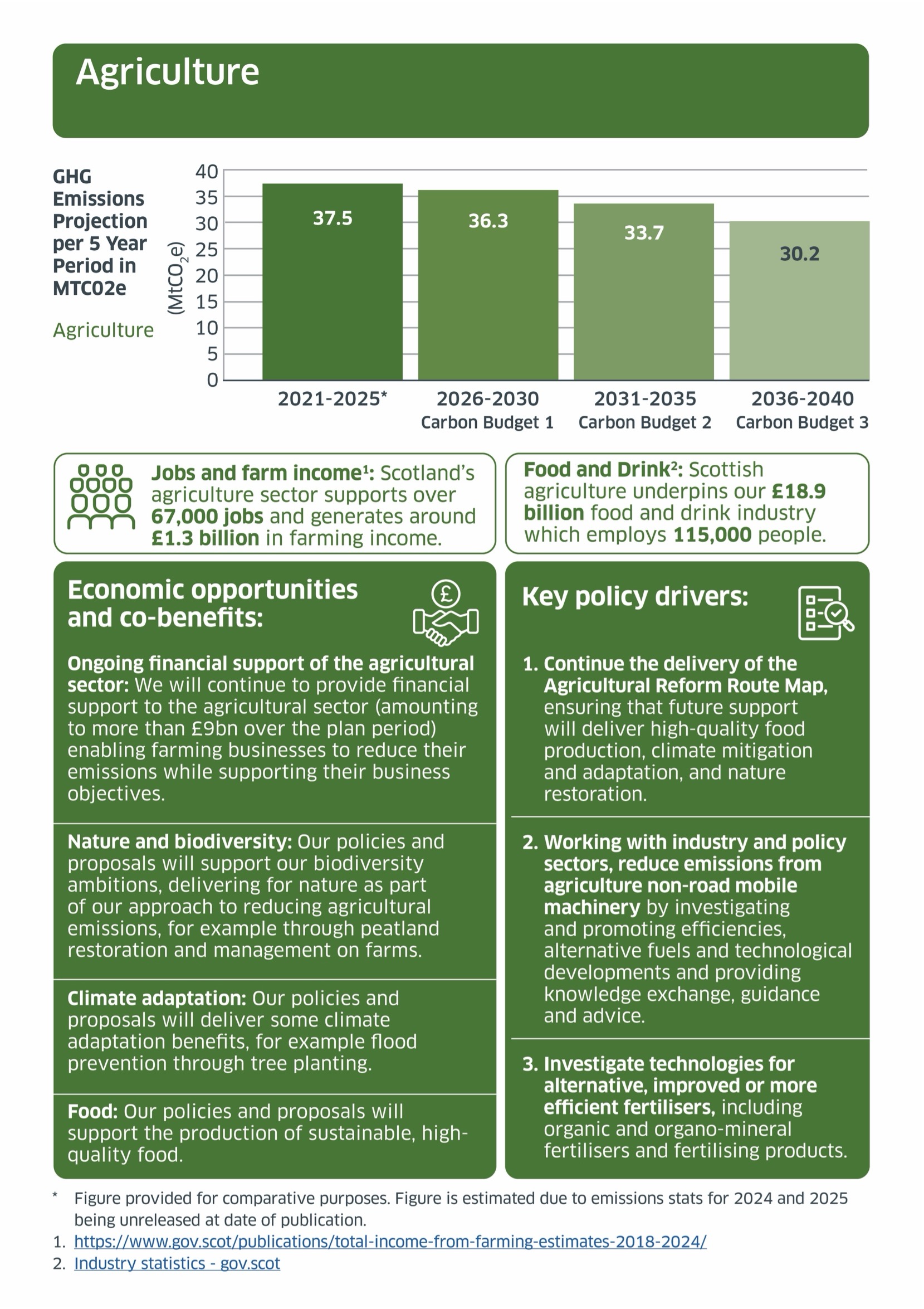

Agriculture

GHG Emissions Projection per 5 year period in MTCO2e Agriculture

2021-2025* - 37.5

2026-2030 Carbon Budget 1 - 36.3

2031-2035 Carbon Budget 2 - 33.7

2031-2035 Carbon Budget 3 - 30.2

Jobs and farm Income1: Scotland's agriculture sectore supports over 67,000 jobs and generates around £1.3 billion in farming income.

Food and Drink2: Scottish agriculture underpins our £18.9 billion food and drink industry which employs 115,000 people.

Economic opportunities and co-benefits:

Ongoing financial support of the agricultural sector: We will continue to provide financial support to the agricultural sector (amounting to more than £9bn over the plan period) enabling farming businesses to reduce their emissions while supporting their business objectives.

Nature and Biodiversity: Our policies and proposals will support our biodiversity ambitions, delivering for nature as part of our approachto reducing agricultural emissions, for example through peatland restoration and management on farms.

Climate adaption: Our policies and proposals will deliver some climate adaption benefits, for example flood prevention through tree planting.

Food: Our policies and proposals will support the production of sustainable, high-quality food.

Key policy driver:

1. Continue the delivery of the Agricultural Reform Route Map, ensuring that future support will deliver high-quality food production, climate mitigation and adaption, and nature restoration.

2. Working with industry and policy sectors, reduce emissions from agriculture non-road mobile machinery by investigating and promoting efficiencies, alternative fuels and technological developments and providing knowledge exchange and guidance and advice.

3. Investigate technologies for alternative, improved or more efficient fertilisers, including organic and organo-mineral fertilisers and fertilisng products.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

1 Source: https://www.gov.scot/publications/total-income-from-farming-estimates-2018-2024/

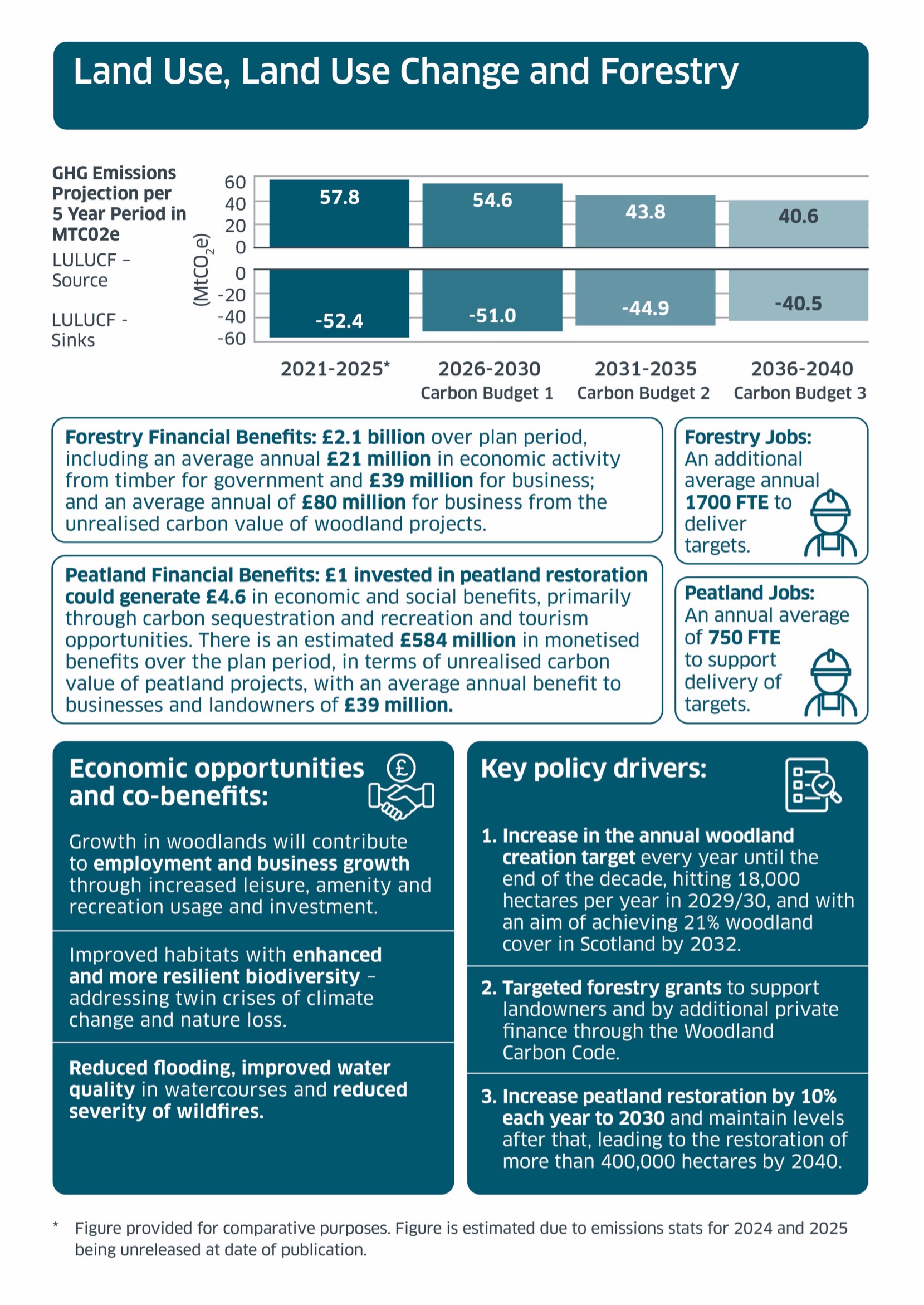

Land Use, Land Use Change and Forestry

GHG Emissions Projection per 5 year period in MTCO2e LULUCF Source

2021-2025* - 57.8

2026-2030 Carbon Budget 1 - 54.6

2031-2035 Carbon Budget 2 - 43.8

2031-2035 Carbon Budget 3 - 40.6

GHG Emissions Projection per 5 year period in MTCO2e LULUCF Sinks

2021-2025* - -52.4

2026-2030 Carbon Budget 1 - -51.0

2031-2035 Carbon Budget 2 - -44.9

2031-2035 Carbon Budget 3 - -40.5

Forestry Financial Benefits: £2.1 billion over plan period, including an average annual £21 million in economic activity from timber for government and £39 million for business; and an average annual of £80 milion for business from the unrealised carbon value of woodland projects.

Peatland Financial Benefits: £1 invested in peatland restoration could generate £4.6 in economic and social benefits, primarily through carbon sequestration and recreation and tourism opportunities. There is an estimated £584 million in monetised benefits over the pln period, in terms of unrealised carbon value of peatland projects with an average annual benefit to businesses and landowners of £39 million.

Forestry Jobs: An additional average annual 1700 FTE to deliver targets.

Peatland Jobs: An annual average of 750 FTE to support delivery of targets.

Economic opportunities and co-benefits:

Growth in woodlands will contribute to employment and business growth through increased leisure, amenity and recreation usage and investment.

Improved habitats with enhanced and more resilient biodiversity - adressing twin crises of climate change and nature loss.

Reduced flooding, improved water quality in watercourses and reduced severity of wildfires.

Key policy drivers:

1. Increase in the annual woodland creation target every year until the end of the decade, hitting 18,000 hectares per year in 2029/30, and with an aim of achieving 21% woodland cover in Scotland by 2032.

2. Targetd forestry grants to support landowners and by additional private finance through the Woodland Carbon Code

3. Increase peatland restoration by 10% each year to 2030 and maintain levels after that, leading to the restoration of more than 4000,000 hectares by 2040.

* Figure provided for comparitive purposes. Figure is estimated due to emissions stats for 2024 and 2025 being unreleased at date of this publication.

Contact

Email: ClimateChangePlan@Gov.Scot