Land and Buildings Transaction Tax: review

An independent analysis of certain aspects of Land and Buildings Transaction Tax (LBTT) policy.

First-Time Buyer Relief

Summary

This is a summary of our analysis of Scotland’s first-time buyer relief.

Objectives

To help first-time buyers enter the property market (Scottish Government, 2017).

Technical overview

Relief for first-time purchasers of a residential property by exempting the first £175,000 of the purchase price from LBTT (The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018).

Interactions with other reliefs and mechanisms

With non-residential/mixed-use: The relief only applies to purchases of entirely residential property, with a single exception (Revenue Scotland, 2024e interpretation).

With MDR: When a buyer qualifies for MDR, it excludes them from also qualifying for first-time buyer relief (Revenue Scotland, 2024e; Revenue Scotland, 2024c interpretation).

With ADS: First-time relief does not apply whenever ADS applies (Revenue Scotland, 2024e interpretation).

With 6+ dwellings ADS exemption: First-time buyer relief does not interact with the 6+ dwellings ADS exemption, which applies since it categorises the transaction as non-residential (Revenue Scotland, 2024e; Revenue Scotland, 2025b interpretations).

Comparative analysis

Compared to LBTT, SDLT appears to be more generous in its first-time buyer relief in that it exempts the first £300,000 of the price, provided the total purchase price does not exceed £500,000, with any value between £300,000 and £500,000 taxed at 5% (HM Treasury, 2017). However, LBTT’s more progressive overall rate structure lends additional, albeit less targeted, support to Scotland’s first-time buyers beyond its first-time buyer relief (Adam and Phillips, 2021).

Unlike Scotland, Wales does not have a first-time buyer relief; instead, it sets its general residential nil-rate band at a higher level (£180,000 initially, now £225,000) (Welsh Government, 2017).

Materiality analysis

First-time buyer relief accounted for up to 7% of total foregone revenue since 2018/19 (Revenue Scotland, 2025c).

Compared with the 6+ dwellings ADS exemption and MDR, it accounted for the smallest share of LBTT revenues forgone, although the gap between the three has narrowed recently (Revenue Scotland, 2025c).

Impact analysis

The impact analysis did not provide evidence of the introduction of the first-time buyer relief influencing first-time property purchases in Scotland, with the increase in such transactions reflecting a continuation of pre-existing upward trends (ONS, 2025a; ONS, 2025b).

However, it is important to note that this analysis does not account for trends in other factors influencing property purchases in Scotland.

Findings from stakeholder engagement

Stakeholders generally viewed first-time buyer relief as helpful, providing modest but meaningful assistance for those facing deposit and affordability challenges. However, many perceived its influence on purchase decisions as limited, describing the relief as largely symbolic due to complex eligibility and the small maximum saving. Most agreed the £175,000 threshold is outdated, given rising house prices, and advocated for an increase or regional variation to better reflect market conditions.

Survey findings showed relatively low awareness of LBTT and the relief, with the idea of financial support appealing most to prospective buyers. While nearly half of recent buyers reported claiming the relief, many said it made little difference to their decision or felt the benefit was minor compared to overall costs.

Stakeholders recognised that while the relief eases financial pressure and offsets some costs, its impact is often restricted by stagnant thresholds and changes in property values. There was consensus that increasing the threshold, or adjusting it for regional differences, would better support buyers and enhance effectiveness.

Views on imposing a cap for relief eligibility were mixed; some considered it fair to prevent high-value claims, while others cited regional price variation and the limited number of qualifying transactions as reasons against a cap. Overall, the relief was seen as a positive, if limited, measure supporting first-time buyers.

Objectives

The stated policy aim was to help first-time buyers enter the property market, with the wider LBTT residential rates then serving to support people as they progress through it. The relief sought to achieve this by raising the LBTT zero-tax threshold for first-time buyers from £145,000 to £175,000. It was anticipated that an estimated 80% of first-time buyers in Scotland would pay no LBTT at all under the relief[12] (Scottish Government, 2017). Since its introduction, over 100,000 buyers have benefited from the relief (Revenue Scotland, 2025d).

Technical overview[13]

Description and administration

Relief for first-time purchasers of a residential property.

Claimed in the LBTT return upon purchase.

Timeframe and value

Applies to transactions with an effective date no earlier than 30th June 2018 for contracts entered into on or after 9th February 2018.

Exempts the first £175,000 of the purchase price from LBTT, effectively raising the nil-rate band from £145,000. This provides a maximum tax reduction of £600 (for a purchase price of £175,000) and has not been adjusted since the relief was introduced in 2018. See Table 11 below.

Table 11. LBTT schedule for first-time buyers

Purchase price

Up to £175,000

LBTT rate

0%

Purchase price

£175,001 to £250,000

LBTT rate

2%

Purchase price

£250,001 to £325,000

LBTT rate

5%

Purchase price

£325,001 to £750,000

LBTT rate

10%

Purchase price

Above £750,000

LBTT rate

12%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015 https://revenue.scot/taxes/land-buildings-transaction-tax/residential-property

Eligibility criteria and limitations

All of the following conditions must be met: (i) the transaction is an acquisition of a major interest[14] in land, (ii) the land being purchases consists entirely of residential property and includes a dwelling, (iii) the buyer is a first-time buyer (i.e., they do not own and have never previously owned a dwelling or a major interest in a dwelling anywhere in the world) and intends to occupy the property as their only or main residence, (iv) the transaction is not a linked transaction*, and (v) the transaction is not one to which the ADS applies.

* Exception to (iv): the relief can still be claimed where the only reason the transactions are linked is the simultaneous acquisition of land that will form part of the dwelling’s garden or grounds or that subsists for the benefit of the dwelling (e.g., a garage or allocated parking space). In such cases, the relief will be available on the total consideration of the linked transaction.

In the case of joint purchases, the relief is available only if every buyer meets all of the above conditions; if any buyer fails a condition, the first-time buyer relief is not available.

Interactions with other reliefs and mechanisms

Between non-residential/mixed-use properties and first-time buyer relief

The first-time buyer relief raises the nil-rate LBTT band to £175,000 for qualifying first-time purchases. The relief only applies to purchases of entirely residential property – if the transaction includes any non-residential element or is a linked transaction (part of a series of transactions), it will not qualify for the relief with a single exception. The exception is in the case of a linked transaction involving a residential and a linked non-residential purchase where the latter is either the garden or grounds of the residential property or is land that subsists or is to subsist for the benefit of that property. In such cases, the relief will be available on the total consideration of the linked transaction (Revenue Scotland, 2024e interpretation).

Between MDR and first-time buyer relief

First-time buyer relief is not available whenever the ADS applies, as well as in the case of linked transactions outside of specific cases. This results in any realistic scenario where a buyer qualifies for MDR, excluding them from also qualifying for first-time buyer relief. This is because a true first-time buyer purchasing two or more dwellings, whether in a single purchase or a series of linked transactions, so as to qualify for MDR, would end the day owning more than one dwelling while not replacing a previous main residence (by definition). This would result in them being subject to the ADS and thereby disqualified from first-time buyer relief (Revenue Scotland, 2024e; Revenue Scotland, 2024c interpretations).

Between ADS and first-time buyer relief

As noted above, first-time buyer relief is not available whenever the ADS applies (Revenue Scotland, 2024e interpretation).

Between 6+ dwellings ADS exemption and first-time buyer relief

No interaction is possible between first-time buyer relief and the 6+ dwellings ADS exemption, as first-time buyer relief is only available for purchases consisting entirely of residential property. The 6+ dwellings ADS exemption would result in the transaction being classified as non-residential, thereby disqualifying the buyer from first-time buyer relief (Revenue Scotland, 2024e; Revenue Scotland, 2025b interpretations).

Comparative analysis

This section presents a comparative analysis of the LBTT first-time buyer relief in Scotland vis-à-vis SDLT in England and Northern Ireland and Land Transaction Tax (LTT) in Wales.

Key differences between LBTT and SDLT

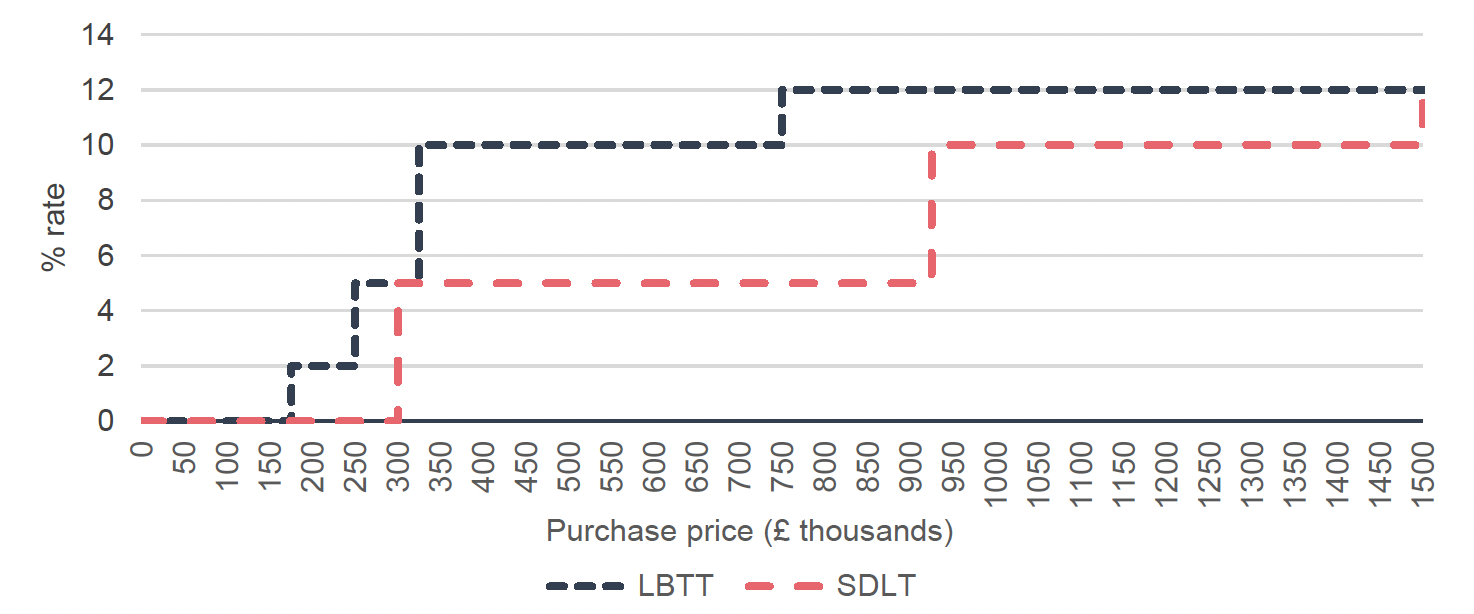

First-time buyer relief is another area where LBTT and SDLT share a general approach – easing the tax burden on new entrants to the housing market – but differ in design and generosity. Scotland introduced LBTT first-time buyer relief in June 2018. As shown in Table 12 below, this relief raises the LBTT nil-rate band to £175,000 for first-time purchasers of their main residence. As a result, an eligible first-time buyer pays no LBTT on the first £175,000 of the purchase price, as opposed to the standard £145,000 threshold. Any value above £175,000 is taxed at the normal marginal rates. There is no maximum purchase price to qualify, but the benefit is capped: the maximum tax saving is £600 per buyer. This £600 saving arises because the 2% LBTT band (normally charged on purchases between £145,000 and £175,000) is waived.

England and Northern Ireland’s SDLT first-time buyer relief, introduced in November 2017, sets a considerably higher threshold. As per Table 13 and the figure below, it exempts the first £300,000 of the price from SDLT for a first-time buyer, provided the total purchase price does not exceed £500,000. Any value between £300,000 and £500,000 is taxed at 5%, and above £500,000, the relief is not available at all (the buyer pays standard rates on the full price) (HM Treasury, 2017). For example, an English first-time buyer of a £400,000 home pays 0% on £300,000 and 5% on the remaining £100,000, totalling £5,000 SDLT; a non-first-time buyer would owe £10,000 on the same purchase. The maximum saving is thus much larger – up to £5,000 at a £500,000 price. In 2022-2023, the UK temporarily enhanced this relief further (raising the nil band to £425,000 and price cap to £625,000), but those changes expired on 31st March 2025 (Masala, 2025). However, although the SDLT provides seemingly more generous relief for first-time buyers than the LBTT, it is important to consider the significant differences in house prices between Scotland and many parts of England. The average price paid by first-time buyers in Scotland is around £157,500, compared with £245,000 in England (HM Land Registry, 2025a; HM Land Registry, 2025b)[15]. In London, where property prices are particularly high, the average first-time buyer property costs around £469,000. These regional variations mean that the higher SDLT thresholds are necessary for the relief to remain relevant across the country.

Table 12. LBTT schedule for first-time buyers

Purchase price

Up to £175,000

LBTT rate

0%

Purchase price

£175,001 to £250,000

LBTT rate

2%

Purchase price

£250,001 to £325,000

LBTT rate

5%

Purchase price

£325,001 to £750,000

LBTT rate

10%

Purchase price

Above £750,000

LBTT rate

12%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015, The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018

Table 13. SDLT schedule for first-time buyers

Purchase price

Up to £300,000

SDLT rate

0%

Purchase price

£300,001 to £500,000

SDLT rate

5%

Source: HM Revenue & Customs (2025b)

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015, The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018https://revenue.scot/taxes/land-buildings-transaction-tax/residential-property; HM Revenue & Customs (2025b)

Comparatively, Scotland’s relief is more modest both in threshold and benefit. One reason may be that LBTT’s standard nil band (£145,000) was already higher than SDLT’s (£125,000) around the time first-time buyer reliefs were enacted, so first-time buyers in Scotland were already slightly better off relative to England. Indeed, Institute for Fiscal Studies (IFS) analysis from 2021 noted that LBTT is more progressive in its overall rate structure, with the majority of purchases either paying no tax (as much as 53% of residential returns in 2015-2016) or being taxed at lower rates than in the rest of the UK (Adam and Phillips, 2021; Revenue Scotland, 2025c interpretation). As noted above, average house prices in England, particularly in the South East and London, are significantly higher than in Scotland, meaning that higher thresholds are necessary under the SDLT.

From a policy perspective, the efficacy of a first-time buyer relief from property transaction tax has been debated in the UK. While it undoubtedly reduces upfront costs for some buyers, the Office for Budget Responsibility has in the past argued that such a relief may simply get capitalised into higher house prices, thus doing little to improve affordability (Office for Budget Responsibility, 2017). The UK and Scottish governments nevertheless introduced the reliefs as a signal of support for first-time homeowners.

Key differences between LBTT and LTT

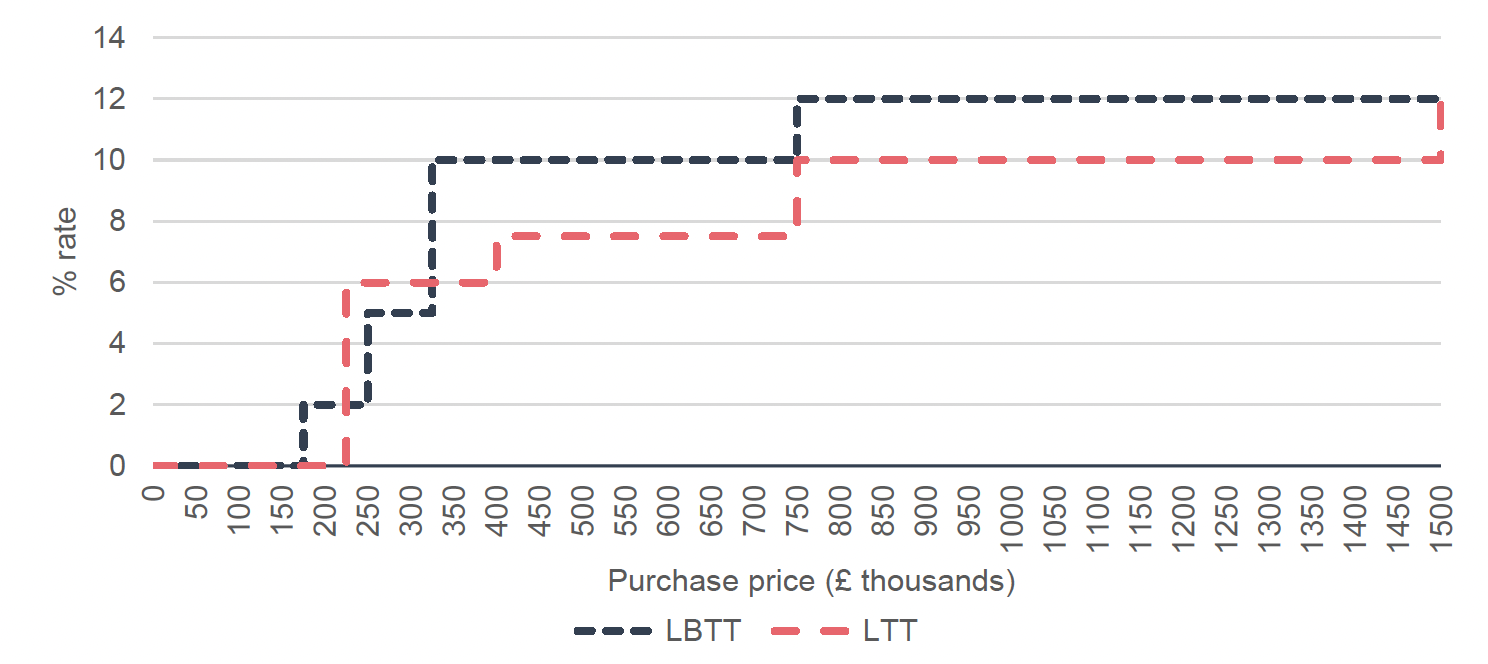

Wales notably does not have a first-time buyer relief for LTT, unlike Scotland’s LBTT. When LTT was introduced in 2018, the Welsh Government decided against a special first-time buyer exemption, opting instead to set the general residential nil-rate band at a high level (£180,000 initially, now £225,000 – see Table 15 and the figure below). The logic was that raising the tax threshold for everyone purchasing lower-priced homes would provide relief for both the majority of first-time buyers, as well as hard-pressed home movers, obviating the need to introduce a separate first-time buyer relief (Welsh Government, 2017). By contrast, Scotland introduced its targeted first-time buyer relief in 2018, as discussed, raising the nil band from £145,000 to £175,000 for first-time buyers (see Table 14).

Table 14. LBTT schedule for first-time buyers

Purchase price

Up to £175,000

LBTT rate

0%

Purchase price

£175,001 to £250,000

LBTT rate

2%

Purchase price

£250,001 to £325,000

LBTT rate

5%

Purchase price

£325,001 to £750,000

LBTT rate

10%

Purchase price

Above £750,000

LBTT rate

12%

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018

Table 15. LTT schedule for residential properties (main rates)

Purchase price

Up to £225,000

LTT rate

0%

Purchase price

£225,001 to £400,000

LTT rate

6%

Purchase price

£400,001 to £750,000

LTT rate

7.5%

Purchase price

£750,001 to £1,500,000

LTT rate

10%

Purchase price

Above £1,500,000

LTT rate

12%

Source: Welsh Government (2024a)

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018; Welsh Government (2024a)

Wales’s policy of a high universal nil rate can be even more generous for first-time buyers at the lower end of the market than Scotland’s targeted relief. For example, a £200,000 first-time purchase in Wales would attract no LTT (since it is under £225,000), while the same transaction in Scotland would incur £500 LBTT (2% of £25,000 above £175,000). The trade-off is that a higher-priced first-time buyer in Wales would not benefit from a relief, as their Scottish counterpart might. For instance, a first-time buyer of a £400,000 house in Wales pays £10,500 LTT, whereas in Scotland they would pay £12,750 LBTT with a £600 relief (£13,350 LBTT if they were not a first-time buyer).

Materiality analysis

The data indicates that all three reliefs within the scope of this review are significant in terms of the overall level of LBTT revenues forgone. Table 24 and Figure 29 present the revenue forgone through each of these reliefs, both in monetary terms and as a share of total LBTT revenues forgone. Among the three, the MDR consistently represents the largest share, accounting for between 7% and 15% of total revenues forgone. The 6+ dwellings ADS exemption has a more modest impact, generally around 3-4%. The first‑time buyer relief typically results in forgone revenues of a similar scale to the 6+ dwellings ADS exemption, though with greater year‑to‑year variation. As illustrated in Figure 29, forgone revenue from both the 6+ dwellings ADS exemption and first‑time buyer relief usually amounts to around half the value of MDR. However, in 2024/25, the difference between the three narrowed noticeably. Table 25 further highlights the significance of these reliefs when expressed as a proportion of overall LBTT revenues.

Additional data from Revenue Scotland (2025f) was available specifically on first-time buyer relief, including the number of claims made under this scheme in each month. Table 28 illustrates that claims for first-time buyer relief accounted for a large share of all relief claims, ranging from 64% to 92% between 2019/20 and 2024/25. When considered as a proportion of total LBTT returns, claims including first-time buyer relief consistently made up around 10-15% of all returns across most years in this period. A particularly notable observation in Table 28 is the sharp decline in first-time buyer transactions in 2020/21, followed by a strong rebound the next year. This unusual pattern is almost certainly attributable to the COVID-19 pandemic, which disrupted property markets and significantly curtailed property market activity during that period.

Impact analysis

The following section undertakes an analysis of the impact of the first-time buyer relief under LBTT. This relief was chosen for this analysis in part due to the availability of relevant time series data predating the introduction of LBTT. It is important to note that the following findings offer only suggestive evidence of impact (or the lack thereof) based on observed trends over time. While we draw on evidence from other UK stamp duty systems, specifically SDLT in England and LTT in Wales, to partially account for factors affecting all three nations, this analysis cannot control for many confounding factors that may have changed over time and influenced property transaction patterns in the Scottish market. As such, these results should not be interpreted as providing definitive causal evidence of impact.

Key findings

Our analysis finds no clear evidence that the introduction of the first-time buyer relief under LBTT had a significant effect on first-time buyer transactions. Graphical trends suggest that the increase in such transactions following the policy’s introduction largely reflects a continuation of pre-existing upward trends, rather than a distinct change as a result of the relief. The relatively modest savings available through the relief of a maximum of £600 may not have been substantial enough to materially influence purchase decisions in the housing market.

Nevertheless, it would be misleading to conclude that the relief had no impact at all. Our dataset cannot fully isolate the effect of the first-time buyer relief from the wide range of domestic and international factors shaping the housing market during the period of analysis. These include global shocks, such as the COVID‑19 pandemic, the Russia-Ukraine conflict, and its inflationary consequences, as well as domestic developments, such as the UK’s exit from the European Union and housing initiatives like the First Home Fund. Given these overlapping influences, it is difficult to draw strong causal inferences about the specific contribution of the relief to first-time buyer activity.

Impact of first-time buyer relief

ONS data (see ONS, 2025a and ONS, 2025b) provides a time series of several indicators, including total first-time buyer transactions, first-time buyers per 1,000 population, and first time buyer transactions as a share of all sales. These series cover the period 2006-2023, spanning both the years before and after the introduction of LBTT first-time buyer relief in 2018. This allows for an assessment of whether any clear shifts in transaction patterns coincided with the policy change. Note that this data is based on first-time buyer mortgage sales rather than tax data and hence will not include first-time buyer transactions for which a mortgage was not taken out.

The first-time buyer relief was introduced to LBTT in 2018 and has seen very limited change since its inception. The only significant adjustment occurred in 2020, when the nil rate band for all residential properties was temporarily increased as part of the COVID-19 response. During this period, the higher general threshold meant that the first-time buyer relief was effectively redundant. Following the withdrawal of these temporary measures in March 2021, the relief reverted to its standard form, with the nil rate band remaining fixed at £175,000. However, given the effects of inflation and rising house prices over this period, the real-terms value of the threshold has gradually eroded. Key changes to the first-time buyer relief are set out in Table 16 below.

Table 16. Changes to LBTT first-time buyer relief

Changes to first-time buyer relief

LBTT introduced

Date

1st April 2015

Changes to first-time buyer relief

First-time buyer relief introduced

Date

30th June 2018

Changes to first-time buyer relief

Temporary COVID‑19 increase in the general nil‑rate threshold (rendering the first‑time buyer relief redundant)

Date

15th July 2020 to 31st March 2021

Changes to first-time buyer relief

Reversion to standard rates after the holiday (restoring the relevance of first‑time buyer relief)

Date

1st April 2021

Source: See Appendix 1

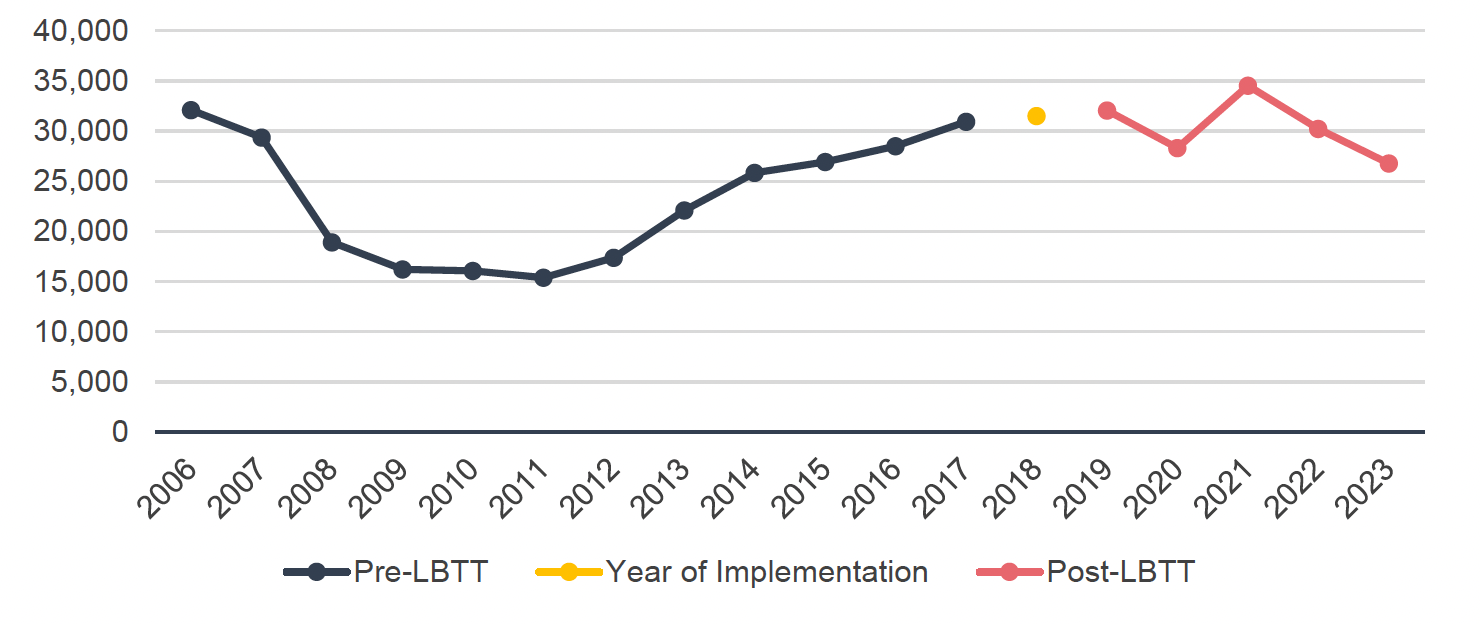

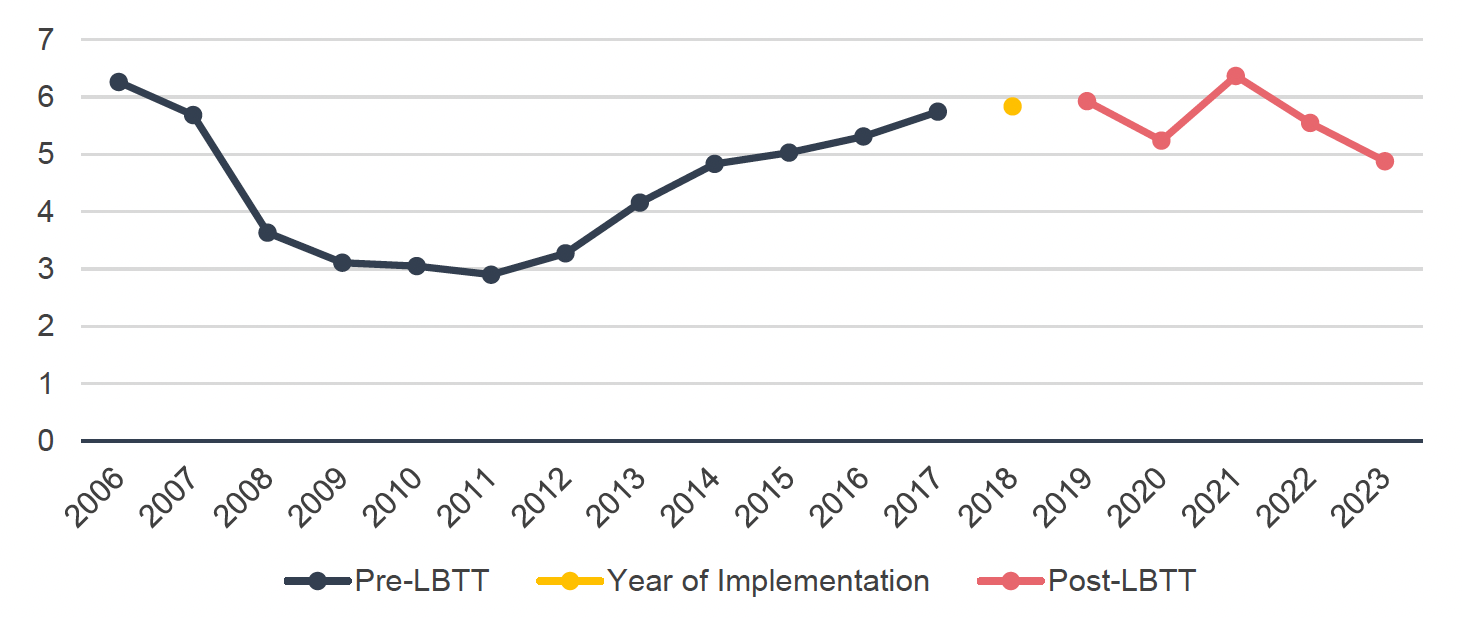

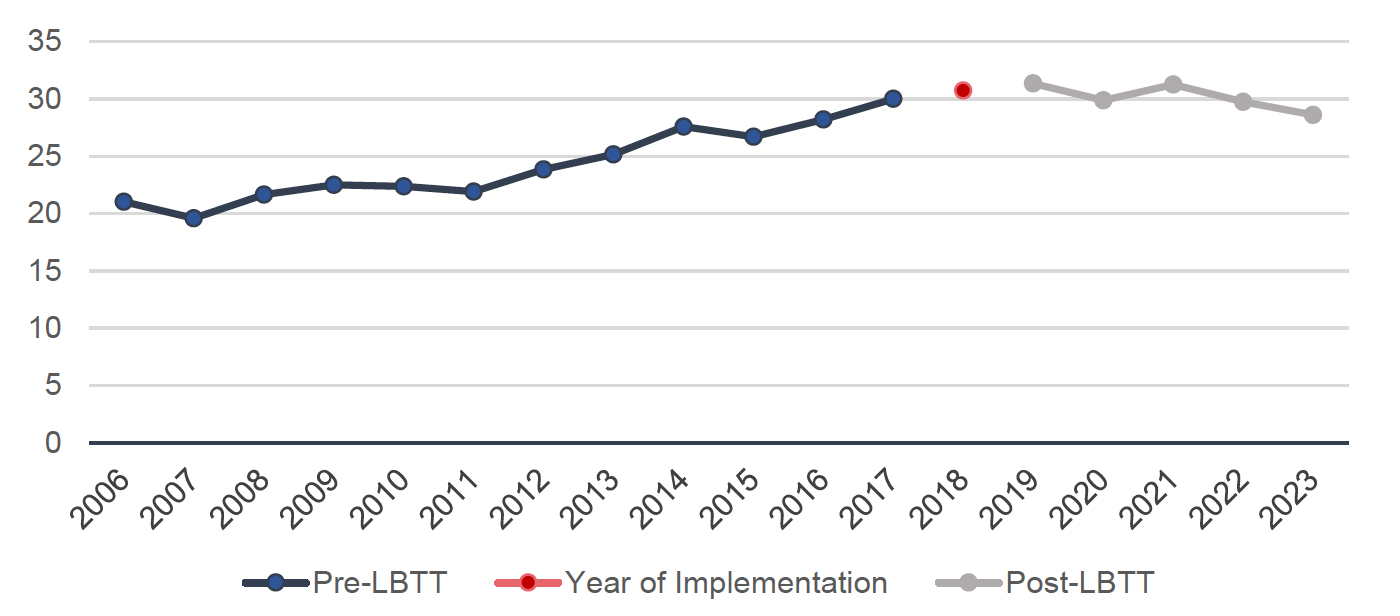

Table 17 presents a simple pre-post comparison of the three indicators, showing their average values before the introduction of the relief in 2018 and after its implementation. The table also provides the absolute and percentage changes between the two periods. Across all three measures, there was a marked increase in first-time buyer transactions, in absolute numbers, relative to population, and as a share of total sales, rising by 30%, 27%, and 25%, respectively.

However, as illustrated in Figures 15, 16, and 17, these increases appear to reflect a continuation of a long-standing upward trend rather than a distinct change from 2018 onwards. All three indicators have been rising steadily since at least 2011, several years prior to both the introduction of LBTT in 2015 and the first-time buyer relief in 2018. The graphs show no clear break or acceleration in this trend immediately following the introduction of the relief. Moreover, wider domestic and international factors, such as the COVID-19 pandemic, likely had a strong influence on market outcomes during this period, making it difficult to ascribe observed changes directly to the policy.

| - | Pre-2018 average | Year of implementation (2018) | Post-2018 average | Difference | Percentage increase |

|---|---|---|---|---|---|

| Scotland total first-time buyer transactions | 23,313 | 31,491 | 30,383 | 7,070 | 30% |

| Scotland first-time buyers per 1,000 population | 4.4 | 5.8 | 5.6 | 1.2 | 27% |

| Scotland first-time buyers per 100 sales | 24.2 | 30.7 | 30.1 | 5.9 | 25% |

Source: ONS (2025a); ONS (2025b)

Source: ONS (2025a)

Source: ONS (2025b)

Source: ONS (2025a)

Urban versus rural local authorities

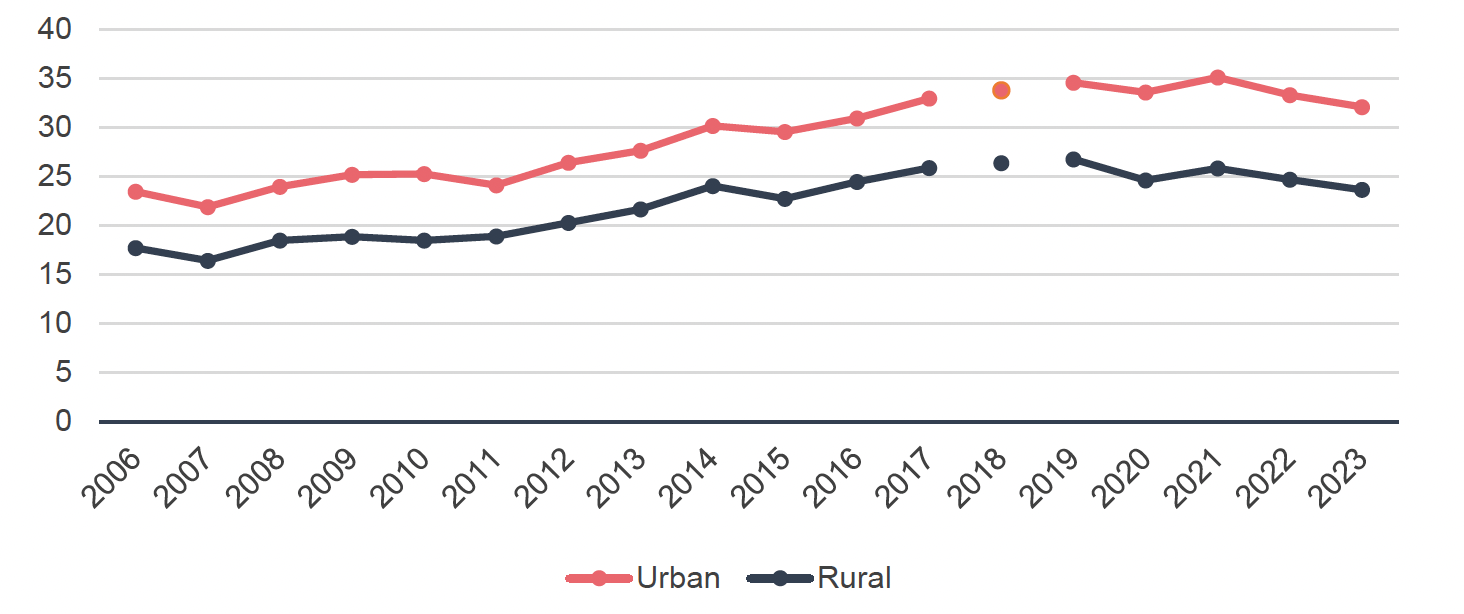

Further analysis was undertaken to examine whether the impact of first-time buyer relief differed between more urban and more rural local authorities. Using data from the Scottish Government (2024a), we calculated the share of each authority’s population living in urban versus rural areas. Using these shares, we categorised local authorities into two groups: an urban group, where a larger share of the population lives in urban areas, and a rural group, where a comparatively smaller share does. Across all Scottish local authorities, the average proportion of the population living in urban areas is 72%. We used this benchmark to classify local authorities with more than 72% of their population in urban areas as urban, and those below this threshold as rural. This approach provides a transparent and easily interpretable distinction between more urban and more rural authorities, enabling us to explore whether outcomes differ between the two groups.

The results indicate that local authorities with urban population proportions above the national average consistently record a higher share of first-time buyer transactions than their more rural counterparts. Across the period, the urban group typically sees around five to ten first-time buyer transactions per 100 sales compared to the rural group. As shown in Figure 18, there is a slight widening of the gap between the two groups, particularly following the introduction of the first-time buyer relief in 2018. This suggests the relief may have had a somewhat greater impact in urban areas compared with rural areas. However, the magnitude of this divergence is small, and overall, the two series exhibit broadly similar trends over time: the share of first-time buyer transactions rose steadily through the early 2010s before stabilising or declining slightly in more recent years.

Source: ONS (2025a); Scottish Government (2024a)

High versus low-income local authorities

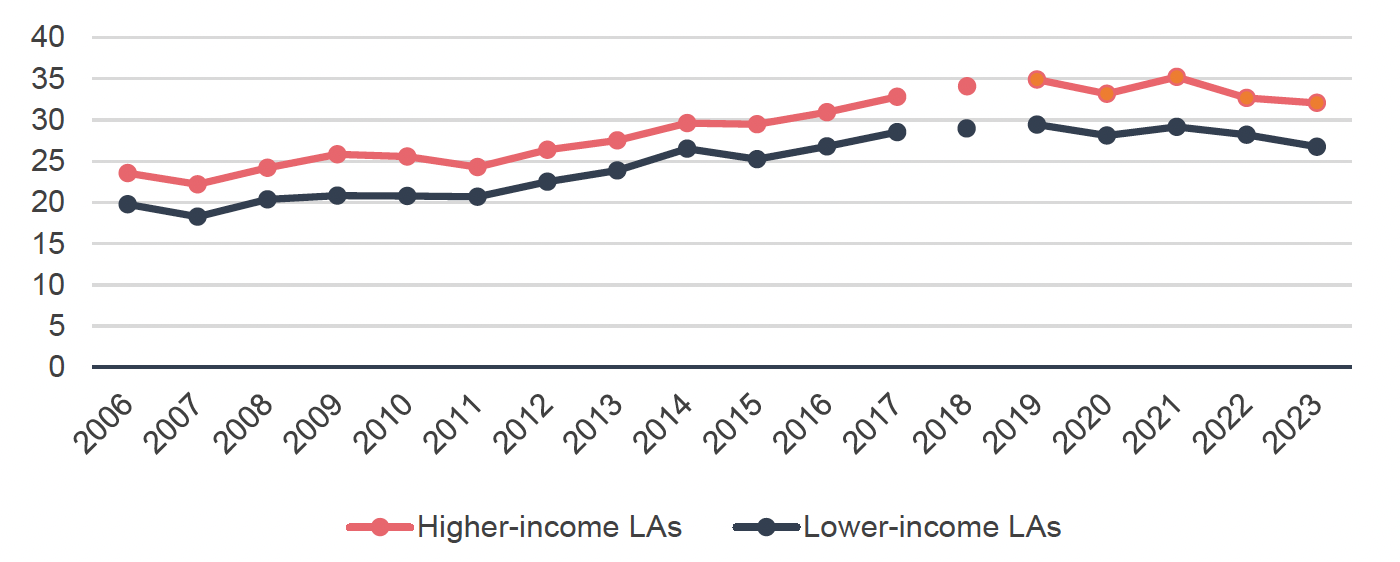

Further analysis compared differences between local authorities with higher and lower income per capita, using ONS data on per capita GDP (ONS, 2019; ONS, 2021). The 2019 Scottish average GDP per capita (£30,560) was used to classify local authorities into high- and low-income groups. Local authorities with an average income above this threshold were categorised as higher-income, while those below it were classified as lower-income. This approach enables a straightforward comparison to assess whether the introduction of the first-time buyer relief had a differential impact on first-time buyer transactions across income groups.

The results show that higher‑income local authorities consistently record a greater share of housing transactions by first‑time buyers. However, the gap between the two groups is smaller than the difference observed between urban and rural areas, with a gap of around three to six first‑time buyer transactions per 100 sales. There is some indication of a slight widening of this gap over time, particularly following the introduction of the first‑time buyer relief, although the magnitude of this change appears limited. Overall, the two groups exhibit broadly parallel trends, with first‑time buyer transactions per 100 sales increasing steadily up to around 2018 before levelling off or declining slightly in subsequent years.

The consistently lower rate of first-time buyer transactions in lower-income local authorities may partly reflect the tenure mix of the housing stock. Areas such as West Dunbartonshire and Inverclyde have a relatively high prevalence of social housing, which limits the size of the owner-occupied market and may reduce the number of sales in which first-time buyers can participate.

Source: ONS (2019); ONS (2021); ONS (2025a)

Comparison with other UK nations

This section provides additional context by comparing first-time buyer transaction trends in Scotland with those in England and Wales. This comparison offers a degree of control for wider factors affecting first-time buyer activity across the UK nations. Examining these trends allows us to identify whether any notable differences emerge, which may offer suggestive evidence of an impact arising from the different treatment of first-time buyers under LBTT relative to SDLT in England and LTT in Wales.

For context, an equivalent first-time buyer relief was introduced in England under SDLT in 2017. This raised the nil-rate band for first-time buyers to £300,000, with a 5% rate applied on the portion of the purchase price between £300,000 and £500,000. However, unlike LBTT relief, no benefit is available for transactions above £500,000. As under LBTT, SDLT first-time buyer relief was rendered largely irrelevant during the COVID-19 stamp duty holiday (July 2020–June 2021), when the nil-rate band was temporarily raised for all purchasers. SDLT nil-rate threshold and maximum property value limit were also increased in September 2022, before returning to their original levels in April 2025. By contrast, under Wales’s LTT, there is no first-time buyer relief offering preferential treatment.

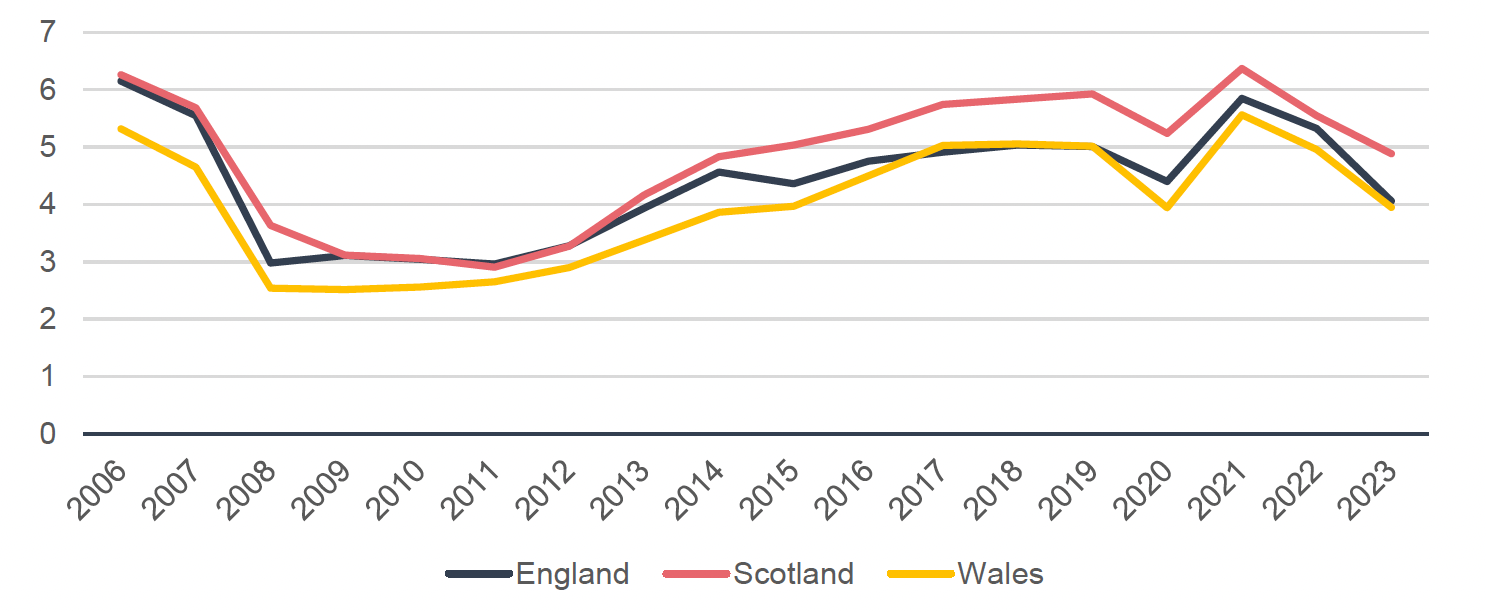

The graph of first-time buyers per 1,000 population in Figure 20 shows very similar trends across the three nations over the period. Scotland consistently records a higher number of first-time buyers per 1,000 population, but this was already the case before the introduction of LBTT and the Scottish first-time buyer relief, meaning it cannot be attributed to the relief. Overall, the close alignment of trends across nations suggests little evidence of any significant increase in first-time buyers as a result of the relief.

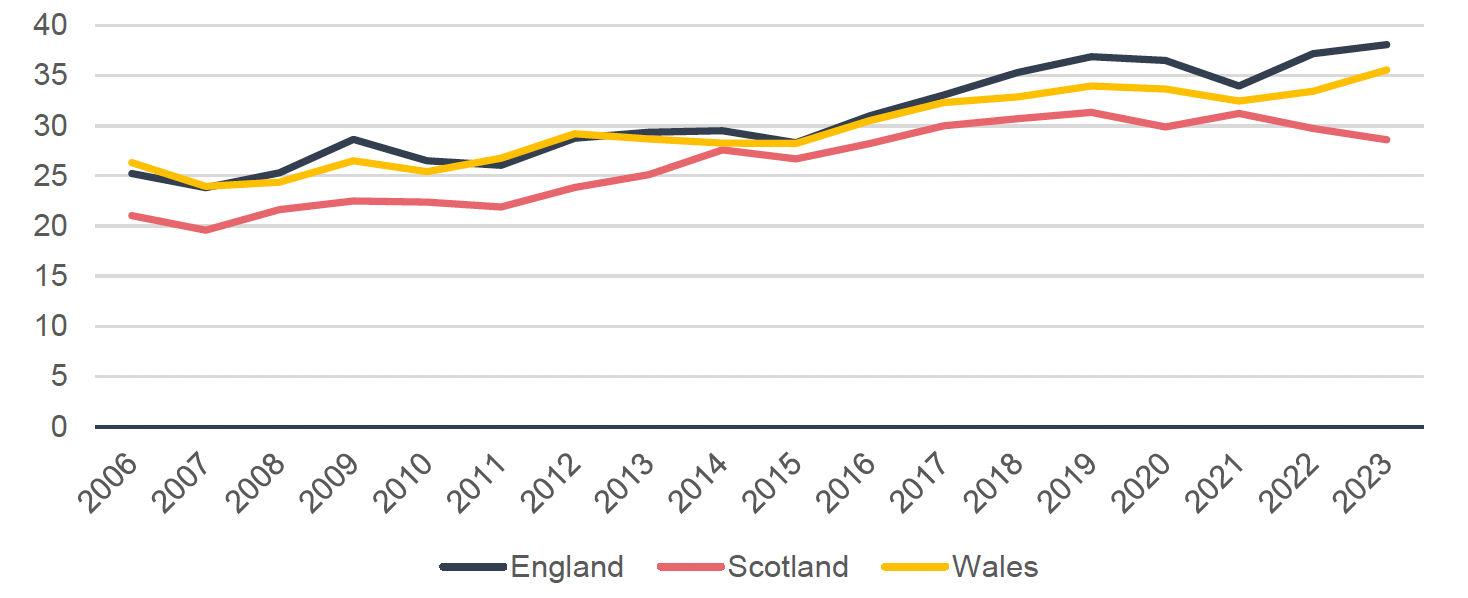

The graph in Figure 21, showing first-time buyer transactions per 100 property sales, again indicates broadly similar patterns across the three nations, though the alignment is less tight than for buyers per 1,000 population. Unlike the first measure, Scotland consistently has a lower proportion of transactions accounted for by first-time buyers. Looking specifically at the period following the introduction of first-time buyer relief in 2018, there is no sign of a positive effect. Scotland’s share of first-time buyer transactions has declined relative to both England and Wales.

Source: ONS (2025b)

Source: ONS (2025a)

Findings from stakeholder engagement

Summary of findings

Stakeholders viewed the first-time buyer relief as helpful but limited in impact. Many agreed it eased costs for buyers already struggling with deposits and competition from wealthier generations, with the savings offering modest but welcome support. However, others saw it as largely symbolic, with minimal influence on purchase decisions and overly complex eligibility rules. Most believed the £175,000 threshold is outdated, given rising house prices, and urged its increase or regional adjustment to reflect market variations. Opinions on imposing a property value cap were mixed; some saw it as fair, others unnecessary or difficult to implement.

Impact on first-time buyers

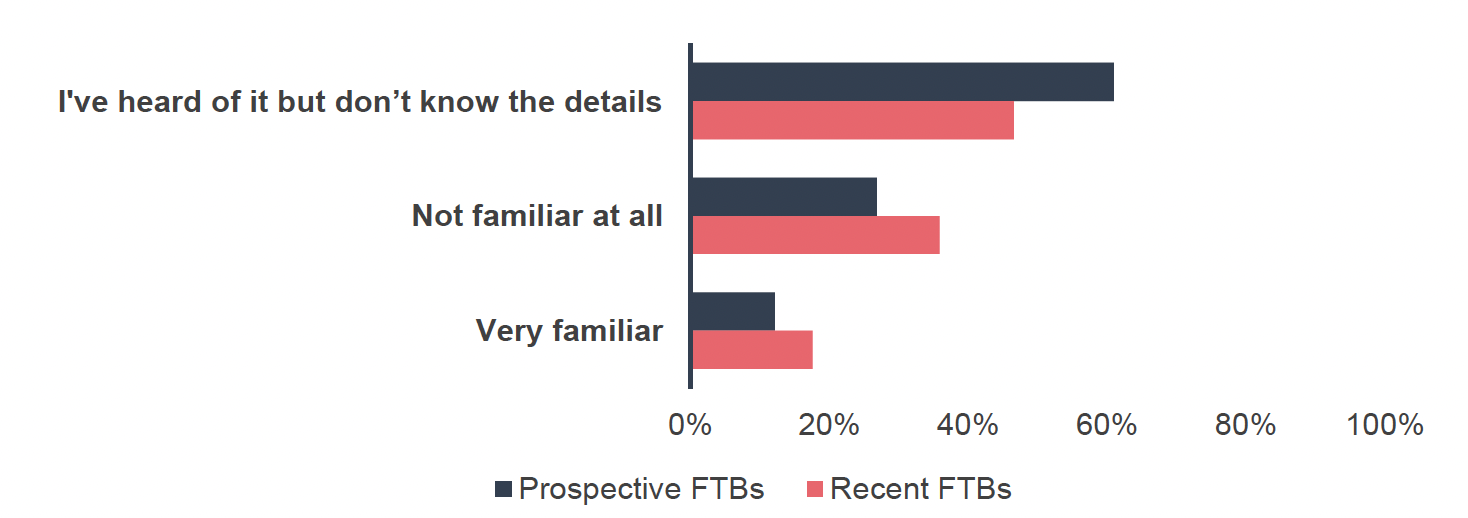

In the survey of recent and prospective first-time buyers, awareness of LBTT varied across both groups, as shown in Figure 22. Among prospective first-time buyers, 61% had heard of the tax but did not know the details, while 27% were not familiar with it at all, and only 12% described themselves as very familiar. Awareness levels were higher among recent first-time buyers, with 47% indicating they had heard of LBTT but lacked detailed knowledge, 36% saying they were not familiar, and 18% reporting they were very familiar. This suggests that direct experience with purchasing a property increases understanding of this tax, although less than one in five recent buyers felt very familiar even after the process.

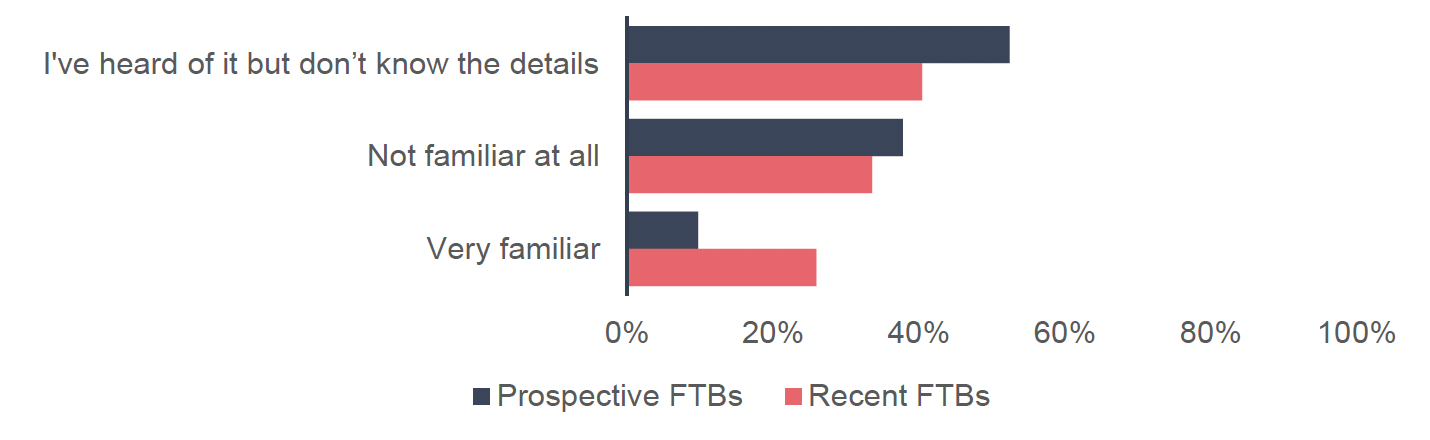

Familiarity with the first-time buyer relief on LBTT showed a similar pattern among prospective buyers (see Figure 23). Just over half (52%) had heard of the relief but did not know the details, 38% were unfamiliar, and 10% were very familiar. Among recent buyers, when asked about their awareness at the point of purchasing their property, 26% said they were very familiar with the relief, 40% had heard of it but lacked a detailed understanding, and 34% were not familiar at all.

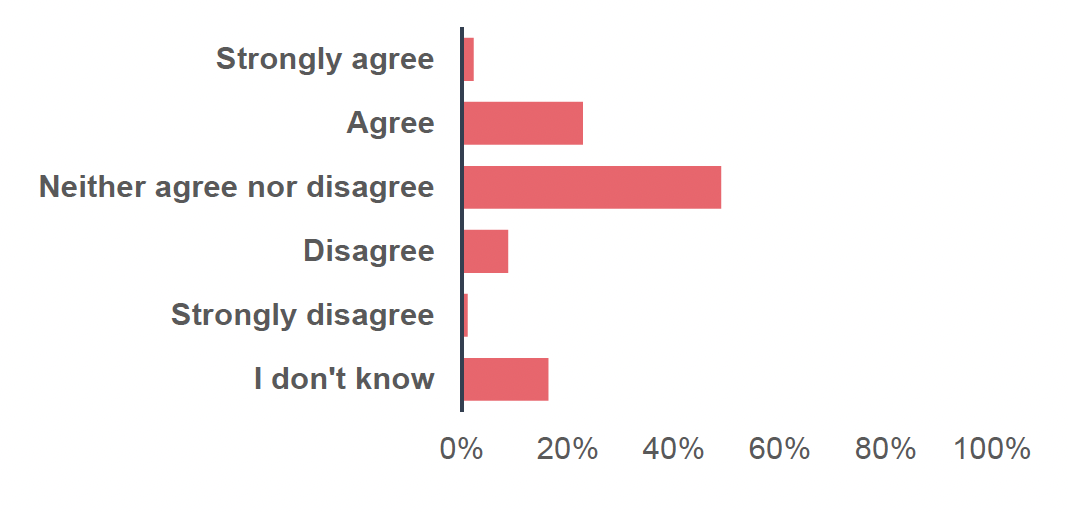

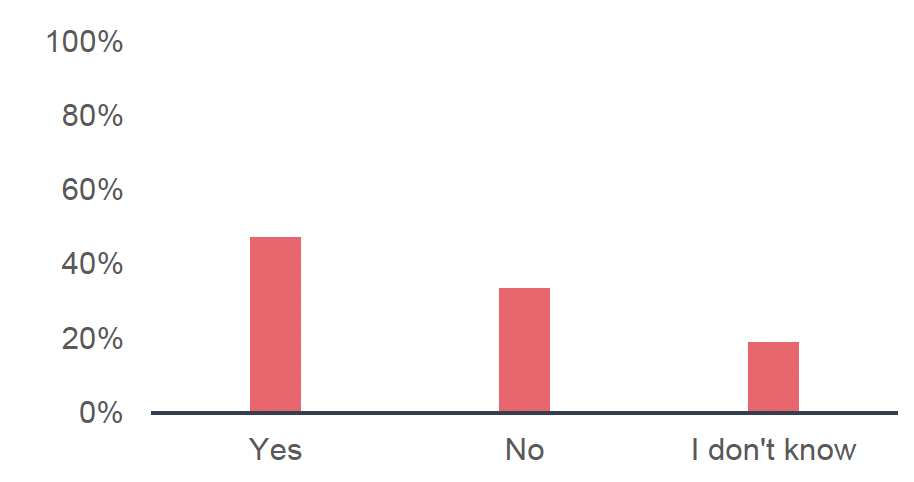

Despite these knowledge gaps, nearly half of recent buyers (47%) reported claiming the first-time buyer relief when purchasing their property (see Figure 24). A third did not claim it, and 19% were unsure, indicating that some buyers may be unclear about how the relief applies or how to access it.

Alt Bar chart showing survey responses from recent FTBs (n=131) on whether they claimed the first-time buyer relief when purchasing their property. Around 47% answered "Yes," around 34% "No," and around 19% "I don't know."

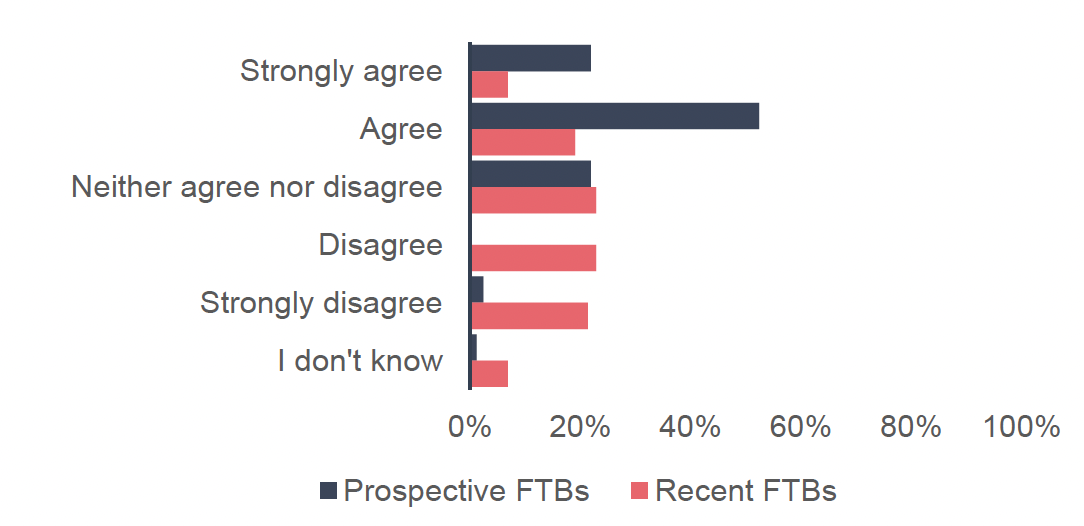

Perceptions of the influence of the first-time buyer relief on purchasing decisions also differed notably between the two groups (see Figure 25). Among prospective buyers, nearly 3/4 (74%) agreed the relief would make them more likely to buy a home, while only 2% disagreed, and the rest were neutral or unsure. When asked to expand on their answer, the most frequent theme among prospective buyers was that the first-time buyer relief made home ownership feel more attainable and reduced some of the financial pressure associated with buying a property. Many described it as an incentive that would help them purchase sooner or with greater confidence, particularly by offsetting upfront costs like legal fees or allowing them to increase their deposit. Several said the relief encouraged them to consider properties slightly above their original budget, while others talked about it making the overall process seem more manageable or realistic. A common sentiment was that “every saving helps,” especially when faced with multiple financial barriers, such as high deposits, interest rates, and the general cost of living.

By contrast, among recent buyers, fewer felt it had influenced their decision: 26% agreed or agreed strongly, 44% disagreed or disagreed strongly, 23% were neutral, and 7% were unsure. When expanding on their answers, recent buyers were much less likely to say the relief had influenced their decision. The dominant theme among this group was that the relief made little or no real difference to whether or when they bought a property. Many said they were unaware of the scheme at the time of purchase, did not qualify for it due to their circumstances, or found the savings too small to meaningfully affect their decision. Several noted that the scale of the relief, often described as modest compared with overall purchase costs, was insignificant against larger considerations like affordability, mortgage approval, and finding a suitable home. A few did acknowledge that while the relief was welcome, it acted more as a “bonus” than a deciding factor, helping slightly with affordability or easing financial stress but not altering their fundamental decision to buy.

Overall, these findings suggest that while awareness of LBTT and the first-time buyer relief is relatively low, the idea of financial assistance is appealing to those yet to buy. However, the relief appears to have a more modest effect on the actual decisions and experiences of recent purchasers.

The impact of the first-time buyer relief was also discussed in the stakeholder interviews, and interviewees differed in their views on its effectiveness in influencing buyers’ decisions to purchase a home. Stakeholders generally recognised the relief as something familiar to first-time buyers, though they differed in their views on its effectiveness in influencing these buyers' decisions to purchase a home. Many stakeholders across different groups felt that LBTT can pose a barrier to homeownership, and any measure that removes a substantial tax burden is likely to be appreciated. Several stakeholders highlighted that first-time buyers are already financially stretched, saving for a deposit, making affordability a significant challenge. Stakeholders noted that first-time buyers face the challenge of competing with older, more asset-rich generations and praised the relief for helping to level the playing field and easing their access to the housing market. While some acknowledged that the maximum saving of up to £600 was modest, many believed even this small amount could provide valuable assistance, offering a helpful boost for entry into homeownership. Given the difficult current circumstances, the relief was seen as likely to have some positive influence on first-time buyers’ decisions. Legal professionals specifically noted that the £600 saving could help offset other costs associated with buying a home, such as legal or conveyancing fees.

Some stakeholders observed that by the time first-time buyers are ready to purchase, they have usually accumulated a sufficient deposit, meaning the relief was not a decisive factor in their decision. However, they felt that even if the relief did not directly influence the decision to buy, it remained a worthwhile measure. They pointed out that while the relief might not sway whether to purchase or not, it may reduce the time buyers need to save for a deposit. Many agreed there is value in aiding first-time buyers by returning some money at the start of their housing journey, regardless of the relief’s impact on their decision-making. One stakeholder also emphasised that any policy helping to stimulate the property market and attract buyers is positive.

However, these views were not held by all stakeholders. Several argued that a maximum saving of £600 is insignificant compared to the overall costs of purchasing a home and has little impact on first-time buyer decisions. One described the relief as more of a “token gesture” than a meaningful incentive, while others noted its political appeal rather than practical effect, suspecting its impact on buyers is marginal at best. An estate agent recommended abolishing the relief in its current form, reporting no instances where LBTT had deterred anyone from buying or selling property.

A legal sector respondent raised concerns about the complex eligibility criteria for the relief, noting that many applicants mistakenly believe they qualify when they do not, for example, due to prior residential property ownership. They observed that because the savings are so limited, the legal fees required to verify entitlement can outweigh the relief’s value, and they sometimes advise clients against pursuing it. Another stakeholder pointed to potential unintended consequences, suggesting that the relief might increase demand and thus drive up house prices, making it harder for future buyers to enter the market. They also questioned whether buyers truly save money or if sellers simply increase prices to offset the relief.

Appropriateness of level of first-time buyer relief

As shown in Figure 26, prospective and recent first-time buyers had broadly similar views on whether the current level of relief is appropriate. Around four in ten respondents in each group (41% of prospective and 40% of recent buyers) considered the current level of relief to be appropriate. However, roughly 1/3 in both groups (34% of prospective and 36% of recent buyers) felt the relief is too low and should be increased. Very few believed it was too generous (7% of prospective and 3% of recent buyers), while 17% of prospective and 21% of recent buyers were unsure. Overall, the results suggest that most view the current level of support as reasonable, though a notable share would welcome an increase, even recognising this would need to be funded through higher general taxation.

When asked to expand on their answers, the most common view among both prospective and recent first-time buyers was that the current level of first-time buyer relief is too low, given rising house prices and the increasing cost of living. Many respondents commented that property values, particularly in cities like Edinburgh and Aberdeen, often exceed the £175,000 threshold, making it difficult for buyers to benefit from the relief in practice. Several felt that while the relief is a helpful gesture, it makes only a small difference relative to overall housing costs, describing it as “a scratch on the surface.” Many suggested that the threshold should be raised to reflect market conditions or inflation, with some recommending aligning it with the average first-time buyer property price, closer to £200,000.

A smaller but significant group viewed the current level of relief as appropriate and fair. These respondents often reasoned that it provides meaningful help to those purchasing lower-cost homes, without placing an excessive financial burden on taxpayers. Some highlighted that the relief strikes a balance between supporting first-time buyers and maintaining fiscal responsibility, especially given that any increase would be funded through higher general taxation. Others noted that for a typical first home, the threshold remains suitable and offers a modest but worthwhile level of support.

A minority felt the relief was too generous or unnecessary, arguing that higher relief levels would either exacerbate housing demand and price inflation or unfairly shift costs onto taxpayers. A few respondents expressed uncertainty, saying they did not know enough about the policy or its impact to make a judgment.

The appropriateness of the relief was also discussed in stakeholder interviews. Stakeholders generally felt that the current threshold for the first-time buyer relief was no longer appropriate. They highlighted that the zero-tax threshold of £175,000 has remained unchanged since the relief was introduced in 2018, despite considerable inflation and substantial increases in house prices. As a result, many properties that would previously have qualified for relief now fall into higher tax bands, reducing the number of homes fully exempt from LBTT for first-time buyers. A majority of stakeholders believed the threshold is now too low and should be increased to reflect current market conditions. Some noted that a higher threshold would better support first-time buyers, as £175,000 is often insufficient to cover typical first-time buyer homes in many areas. One stakeholder suggested that raising the threshold could not only assist buyers but also stimulate market activity and encourage new housebuilding. Another suggested that a temporary LBTT holiday for first-time buyers could further boost market movement.

Several stakeholders emphasised the importance of accounting for regional variation in house prices. They noted that rural areas typically have lower prices than urban centres such as Edinburgh and Glasgow, where the relief has become less effective. For example, one organisation observed that the average house price in Fife is around £150,000, compared with about £220,000 in Edinburgh. This means that first-time buyers in places like Fife are more likely to find a home fully exempt from LBTT, whereas buyers in the capital often exceed the relief threshold. In contrast, one estate agent suggested removing the relief entirely, stating that most first-time buyers in their area purchase homes below the main LBTT nil-rate threshold of £145,000, rendering the relief redundant. To address regional disparities, some stakeholders proposed introducing zonal LBTT and relief thresholds that reflect local market conditions, for instance, setting higher thresholds in areas with higher average house prices.

One interview respondent noted that the issue of outdated thresholds extends beyond the first-time buyer relief and applies to all LBTT bands. Adjusting thresholds is challenging because they are set in primary legislation and would require a lengthy parliamentary process. The stakeholder, however, also warned that static thresholds risk generating fiscal drag, as rising property values push more transactions into higher tax bands. However, another participant pointed out that the progressive design of LBTT mitigates this effect, since buyers pay tax only on the portion of the property price above each threshold. They added that first-time buyers still benefit from relief on the portion of the purchase price below £175,000, even if the total property value exceeds that level. Some stakeholders also observed that increasing relief threshold or lowering rates for first-time buyers would reduce tax revenues and could therefore impact public finances.

Need for cap on first-time buyer relief

Most stakeholders did not express strong views on whether there should be a cap on the maximum property value eligible for first-time buyer relief. In England and Northern Ireland, such a cap exists under SDLT, where the first-time buyer relief cannot be claimed on transactions over £500,000. There is no equivalent limit under Scotland’s LBTT. Some stakeholders considered a cap fairer, aligning with the SDLT approach. It was also noted that recently, several high-value transactions had claimed first-time buyer relief, suggesting some claimants possessed sufficient means and did not necessarily need the support. Unpublished data from Revenue Scotland provides evidence on the extent to which the first-time buyer relief is being used in higher-value property transactions. In the first two quarters of 2025/26, approximately 11,400 claims were received for the relief. Of these, over 15.7% related to properties valued above £300,000, including more than 1.5% with values exceeding £500,000.

Others highlighted that a £500,000 threshold would rarely be exceeded in Scotland due to generally lower property values. A few contributors opposed the idea of a cap altogether, with one solicitor arguing it would be difficult to design a fair system given regional house price differences. For instance, properties in larger cities, such as Edinburgh, tend to be significantly more expensive than elsewhere. Another stakeholder proposed offering greater relief for lower-value properties but questioned whether the added complexity would be worthwhile.

Contact

Email: devolvedtaxes@gov.scot