Land and Buildings Transaction Tax: review

An independent analysis of certain aspects of Land and Buildings Transaction Tax (LBTT) policy.

MDR

Summary

This is a summary of our analysis of Scotland’s MDR.

Objectives

To support buy-to-let investors and large-scale residential property purchases by ensuring that a single transaction involving multiple dwellings is not taxed at a high tax band when the same dwellings purchased individually would have attracted a charge at lower tax bands (Scottish Government, 2013a).

Technical overview

A partial LBTT relief available when a buyer acquires more than one dwelling in a single transaction or a series of linked transactions (Land and Buildings Transaction Tax (Scotland) Act 2013, Sch 5).

Interactions with other reliefs and mechanisms

With non-residential/mixed: A buyer can potentially claim MDR on the dwellings and still pay non-residential LBTT on the non-dwelling part of their property (Revenue Scotland, 2025a interpretation).

With ADS: When a buyer purchases multiple residential properties together, both the ADS and the MDR can potentially apply simultaneously (Revenue Scotland, 2024g interpretation).

With 6+ dwellings ADS exemption: A buyer can benefit from non-residential rates and claim full relief from the ADS, despite benefiting from MDR (Brodies, 2021 interpretation).

With first-time buyer relief: A buyer who qualifies for MDR does not qualify for first-time buyer relief, and they would be subject to ADS (Revenue Scotland, 2024e; Revenue Scotland, 2024c interpretations).

Comparative analysis

While Scotland retained its MDR as originally envisioned, England and Northern Ireland abolished their equivalent MDR under SDLT due to significant abuse (HM Revenue & Customs, 2025b).

Wales continues to offer an MDR but has tightened the circumstances under which it can be claimed. For instance, regulations were passed to limit LTT MDR when the subsidiary dwelling exemption (SDE) from higher rates applies (Welsh Parliament, 2025).

Materiality analysis

MDR accounted for 7-15% of total foregone revenue in the last 10 years, and 1-3% of total LBTT revenue (Revenue Scotland, 2025c).

Compared with the 6+ dwellings ADS exemption and the first-time buyer relief, it accounted for the largest share of LBTT revenues forgone, although the gap between the three has narrowed recently (Revenue Scotland, 2025c).

Findings from stakeholder engagement

Awareness and use of MDR is concentrated among larger landlords, developers, and institutional investors to make multi-property transactions (e.g., build-to-rent, student accommodation schemes) financially viable by reducing LBTT costs.

Smaller landlords and individual investors showed low awareness and limited use of the relief. Most reported that MDR has little influence on their investment decisions, as they generally purchase single properties or are ineligible to claim.

Stakeholders who use MDR felt it fulfilled its purpose by smoothing tax liabilities, but viewed it more as removing a tax disincentive than providing an active investment incentive. Wider housing policies, especially rent controls, were seen as having a stronger effect on investment behaviour.

While some noted the relief’s complexity, misuse in Scotland is minimal. Legal practitioners reported complexity in calculating liabilities and past boundary-pushing around what counts as a “dwelling”; nevertheless, they emphasised that Scotland has seen far fewer avoidance issues than England.

Most stakeholders opposed its removal, arguing it supports development viability and maintains Scotland’s competitiveness. Some suggested reforming MDR to better incentivise large-scale housing delivery.

Objectives

The stated purpose of the MDR was to ensure that a single transaction involving multiple dwellings is not taxed at a high tax band when the same dwellings purchased individually would have attracted a charge at lower tax bands (Scottish Government, 2013a). Without this relief, a bulk purchase could push the buyer into higher tax bands as if it were one large property, thereby discouraging bulk purchases.

Technical overview[9]

Description and administration

- A partial LBTT relief available when a buyer acquires more than one dwelling in a single transaction or a series of linked transactions.

- To claim the MDR, the buyer includes the claim in their LBTT return or amends the return within 12 months.

Timeframe and value

- In effect since LBTT’s introduction on 1st April 2015.

- The relief’s value depends on the transaction. With the MDR, LBTT due for a transaction is calculated on the average price per dwelling rather than the total price, and this effective tax per unit is multiplied by the number of dwellings, subject to a minimum total tax requirement known as the “minimum prescribed amount.” The precise calculation relies on detailed formulas, which ensure that a minimum prescribed amount of at least 1/4 of the tax that would be due without the MDR is still paid. The tax rates and bands for residential property are used regardless of the number of dwellings being acquired, and assuming the transaction is not a linked transaction.

Eligibility criteria and limitations

- All of the following conditions must be met: (i) the transaction involves two or more dwellings, (ii) the dwellings are separate, self-contained, and suitable for residential use (regardless of whether the transaction also involves non-residential property), and (iii) the transaction is either a single purchase or a series of linked transactions. Leases are excluded.

- The MDR cannot be claimed if any of the following reliefs are available for a given transaction: (i) crofting community right to buy relief, (ii) group relief, (iii) reconstruction relief and acquisition relief, or (iv) charities relief. The MDR also cannot be claimed if reliefs (ii)-(iv) have been “withdrawn” from a previous return (referring to a situation where the buyer ceased to meet the qualifying conditions or was otherwise disqualified from a claim on the relief).

- If an MDR claim is made and circumstances change (e.g., one of the dwellings is sold off within a prescribed period[10]), the MDR can be withdrawn in part or full.

Interactions with other reliefs and mechanisms

Between non-residential/mixed-use properties and MDR

If a transaction includes multiple dwellings and non-residential property (e.g., an estate with cottages and farmland), the buyer can potentially claim MDR on the dwellings and still pay non-residential LBTT on the non-dwelling part. The formulas for MDR explicitly separate “remaining property” (the non-residential portion) from dwellings to integrate the two regimes, essentially ignoring the non-residential part when calculating the MDR for the dwellings. This interaction ensures that having a commercial element in a transaction does not nullify the benefit of the MDR on the residential part. Conversely, if one of the dwellings in an MDR claim is in fact a commercial unit, it cannot be counted towards the MDR. The overall effect is that non-residential land acquisitions and the MDR interact in mixed transactions to significantly reduce the tax payable on the dwelling part (via averaging on dwellings) while attracting the lower non-residential rates on the non-dwelling part (Revenue Scotland, 2025a interpretation).

Between MDR and ADS

When a buyer purchases multiple residential properties together, both the ADS and the MDR can potentially apply simultaneously. The law provides a formula to integrate them, with the MDR normally computed on the average consideration per dwelling and added up for each average consideration, and then the ADS is added to each average consideration per dwelling for only those dwellings on which the ADS is applicable. If all dwellings in the transaction are subject to ADS (none qualify as replacement of a main home) and the MDR is being claimed, then the ADS payable is effectively a flat surcharge on top of a base LBTT, which has been lowered by the MDR. However, when one or more dwellings are exempt from the ADS (e.g., one of the purchased units is intended as the buyer’s new main residence, replacing an old one), the calculation must separate those out. In such cases, Revenue Scotland advises that the tax be computed for each dwelling individually: the ADS is added only to those dwellings that trigger it, and not to the one replacing a main residence (Revenue Scotland, 2024g interpretation).

Between MDR and 6+ dwellings ADS exemption

The 6+ dwellings ADS exemption adds an additional layer to the interaction described above between the MDR and the ADS. Crucially, even though a transaction eligible for the 6+ dwellings ADS exemption is considered “non-residential” for LBTT purposes, the MDR can still be claimed in this scenario while retaining the benefit of the non-residential rates. More precisely, even though a 6+ dwelling purchase is assessed at non-residential LBTT rates, the buyer is allowed to use the MDR mechanism to compute tax on an average unit price (subject to the 25% minimum) and then pay LBTT accordingly, all at non-residential rates. This presents a highly favourable scenario for the taxpayer, allowing them to benefit from non-residential rates (lower than residential rates), the MDR (enabling them to calculate LBTT using the average consideration per unit), and full relief from the ADS (due to the 6+ dwelling exemption) (Brodies, 2021).

Between MDR and first-time buyer relief

First-time buyer relief is not available whenever the ADS applies, as well as in the case of linked transactions outside of specific cases. This results in any realistic scenario where a buyer qualifies for MDR, excluding them from also qualifying for first-time buyer relief. This is because a true first-time buyer purchasing two or more dwellings, whether in a single purchase or a series of linked transactions, so as to qualify for MDR, would end the day owning more than one dwelling while not replacing a previous main residence (by definition). This would result in them being subject to the ADS and thereby disqualified from first-time buyer relief (Revenue Scotland, 2024e; Revenue Scotland, 2024c interpretations).

Comparative analysis

This section presents a comparative analysis of LBTT’s MDR applicable to transactions in Scotland vis-à-vis SDLT in England and Northern Ireland and LTT in Wales.

Key differences between LBTT and SDLT

MDR provides a tax reduction when two or more dwellings are bought in a single transaction or a linked series of transactions. Under LBTT, MDR has been in place since the tax’s inception, mirroring a relief originally available under SDLT. However, a major divergence emerged in 2024: the UK Government abolished MDR for SDLT, effective for transactions completing on or after 1st June 2024 (HM Revenue & Customs, 2025b). This policy change was enacted via the Finance Act 2024. In contrast, Scotland retained MDR for LBTT. A landlord or institution acquiring, for example, five dwellings in Scotland may still claim MDR to reduce LBTT, whereas the same purchase in England now attracts full SDLT without MDR. The abolition of MDR in England and Northern Ireland followed concerns that it was being used aggressively to shrink tax bills in cases that were not consistent with the relief’s intended purpose, as evidenced by the large number of individuals claiming MDR who were losing tax tribunal cases (Tolcher, 2024). A consequence is that LBTT is now relatively more accommodating for bulk residential acquisitions.

Prior to its abolition, SDLT MDR operated identically to LBTT MDR in reducing total liability by taxing the average price per dwelling rather than the total price and then multiplying that tax amount by the number of dwellings. Crucially, both systems enforced a minimum tax floor to prevent the MDR from eliminating tax entirely on low-value transactions: in Scotland, at least 25% of the tax that would be due without MDR must still be paid, while the SDLT rule (prior to 2024) was that the effective rate could not fall below 1% of the total price. It is also notable that LBTT MDR never exempts the transaction from ADS, nor did SDLT MDR exempt the analogous 3% surcharge in England and Northern Ireland before being abolished (Revenue Scotland, 2025a interpretation; HM Revenue & Customs, 2025b).

Key differences between LBTT and LTT

Scotland and Wales both continue to offer a relief on acquisitions of multiple dwellings in their respective land taxes, with largely similar mechanics inherited from the original SDLT design. Under LTT, as in LBTT, a buyer of multiple dwellings in one transaction can elect to have the tax calculated on the average price per dwelling (and multiplied by the number of units), rather than on the aggregate price, potentially lowering the tax due if the dwellings are of uneven or lower individual value. Also like LBTT, Wales’s MDR includes a minimum tax rule, although the precise rule differs from the LBTT equivalent: LTT MDR ensures a minimum effective rate of 1% of the total consideration for the dwellings (Welsh Government, 2025a). This compares to a 25% minimum prescribed amount of the no-relief LBTT in Scotland’s case. Except for the minimum tax rule, LTT’s MDR works identically to its LBTT counterpart: it prevents the purchaser from paying a higher rate of tax than if they had bought the properties separately, while guaranteeing that at least some tax (a floor amount) is paid. For instance, if an investor buys three houses in Wales for £600,000 total (averaging £200,000 each), LTT MDR would compute tax on £200,000 and triple it, subject to not going below 1% of £600,000 (i.e., £6,000). Similarly, LBTT would compute on the average price and ensure that at least 25% of the normal £600,000 tax is paid (£33,500 LBTT would be due on a £600,000 residential purchase, of which 25% is £8,337.50).

One distinction is that Wales recently tightened MDR in specific scenarios. In February 2025, regulations were passed to limit LTT MDR when the subsidiary dwelling exemption (SDE) from higher rates applies. The SDE exempts purchases of a main dwelling together with one or more subsidiary dwellings within the same building or grounds from the higher residential rates of LTT (analogous to LBTT’s ADS – see below), provided that the main dwelling component makes up 2/3 or more of the total consideration. The rule change precludes the ability to claim both MDR and SDE at the same time (Welsh Government, 2024b; Welsh Parliament, 2025). Scotland, by comparison, does not have an explicit SDE equivalent. Under LBTT, an annex counts as a separate dwelling only if it is suitable for use as a dwelling; otherwise, it is part of the main dwelling (Revenue Scotland, 2024h interpretation). Where there is assessed to be only one dwelling in the purchase, the MDR is not available, and ADS is not triggered by the presence of the annex. Furthermore, under LTT, taxpayers can classify a 6+ dwelling transaction as either non-residential, in which case MDR cannot be claimed, or residential, in which case MDR may be claimed but the higher residential rates apply (Welsh Government, 2025c). No such choice in classification is available under LBTT.

Materiality analysis

The data indicates that all three reliefs within the scope of this review, including the MDR, are significant in terms of the overall level of LBTT revenues forgone. This report examines three reliefs in particular: the MDR, the ADS exemption for purchases of six or more dwellings, and first-time buyer relief. Table 24 and Figure 29 present the revenue forgone through each of these reliefs, both in monetary terms and as a share of total LBTT revenues forgone. Among the three, MDR consistently represents the largest share, accounting for between 7% and 15% of total revenues forgone. The 6+ dwellings ADS exemption has a more modest impact, generally around 3-4%. First‑time buyer relief typically results in forgone revenues of a similar scale to the 6+ dwellings ADS exemption, though with greater year‑to‑year variation. As illustrated in Figure 29, forgone revenue from both the 6+ dwellings ADS exemption and first‑time buyer relief usually amounts to around half the value of the MDR. However, in 2024/25, the difference between the three narrowed noticeably. Table 25 further highlights the significance of these reliefs when expressed as a proportion of overall LBTT revenues.

Findings from stakeholder engagement

Summary of findings

Interview findings suggest that the MDR is primarily used by large landlords, developers, and investors to make multi-property transactions. Smaller landlords are often unaware of or unaffected by the relief. Stakeholders benefiting from the relief reported that it was important in ensuring multi-property transactions are viable by reducing tax burdens, especially in build-to-rent and student housing projects.

It was, however, noted that other Scottish regulations in the housing market, such as rent controls, have overshadowed its benefits and discouraged large-scale development. While some find MDR complex to apply, misuse is minimal in Scotland. Most stakeholders who have used the relief oppose its removal, suggesting reforms should be made to better encourage large-scale housing delivery.

Usage and beneficiaries of MDR

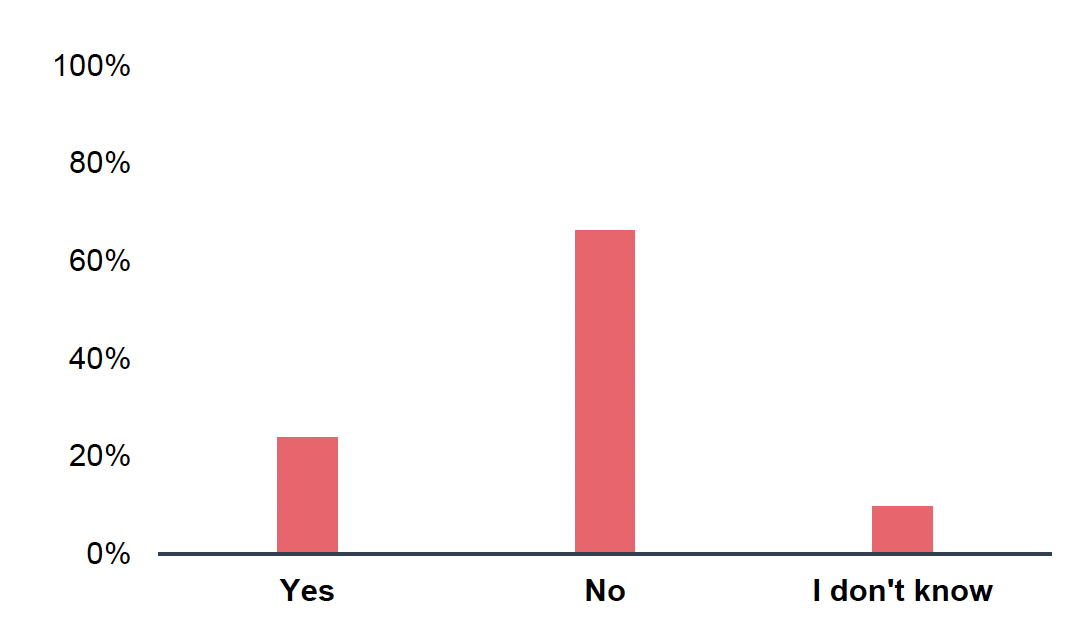

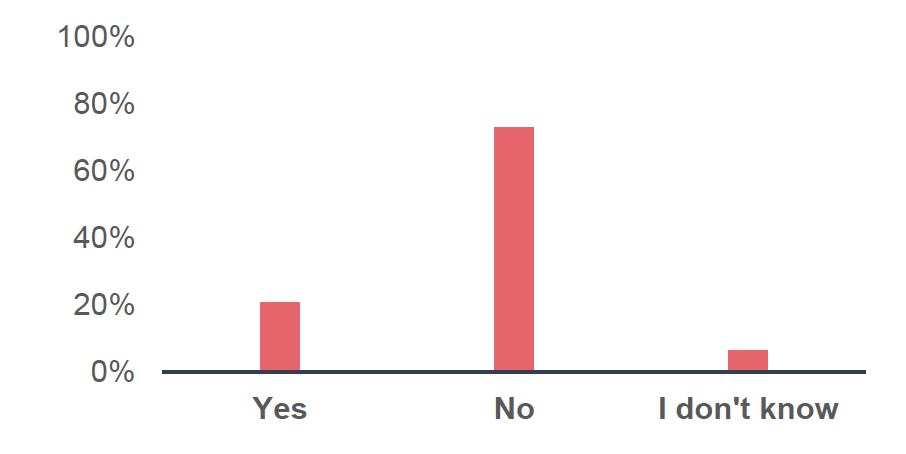

The survey of individual investors highlighted limited awareness and understanding of the relief. As shown in Figure 10, when asked whether they were aware of MDR prior to taking part in the survey, only 21% (19 out of 92) responded ‘yes.’ The vast majority (73%) stated that they were not aware of it, while a further 7% said they did not know. In line with this, only 3% of respondents reported having previously claimed MDR, compared with 92% who had not, and 4% who were unsure (see Figure 11). This suggests that both awareness and actual use of the relief is extremely low.

Figure 10. Prior to this survey, were you aware of the multiple dwellings relief (MDR) under the LBTT? (n=92)

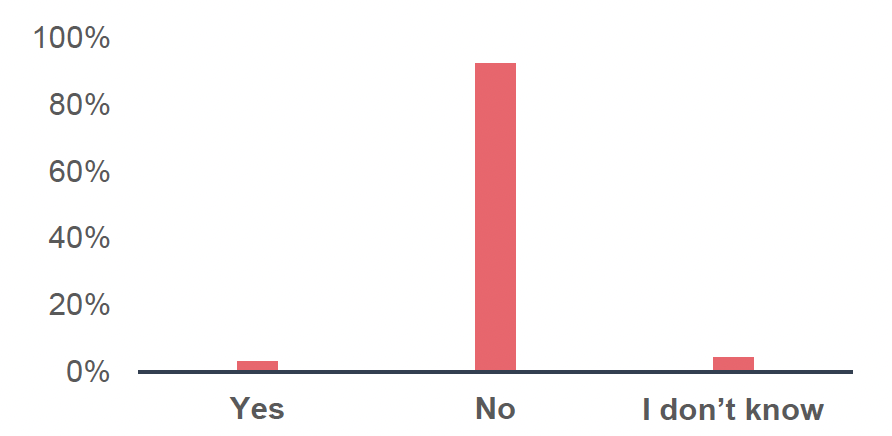

Furthermore, when asked to what extent investors agreed that the availability of MDR enabled them to undertake investments that they would otherwise be unable or unwilling to, responses were mixed but generally noncommittal. Around 25% either agreed (23%) or strongly agreed (2%), indicating that some investors perceived MDR as a supportive factor in investment decisions (see Figure 12 below). However, nearly half (49%) neither agreed nor disagreed, and a combined 10% disagreed or strongly disagreed, while 16% stated that they did not know.

When asked to expand on these answers, the qualitative responses reinforced the quantitative findings, showing that awareness among individual investors is generally low and its influence on investment decisions is limited. The majority of respondents said MDR does not affect their investment choices, either because they were unaware of it, are not eligible, or mainly invest in commercial or single-dwelling properties where the relief does not apply. Several admitted to having little understanding of how MDR works, with some confusing it with unrelated terms. Many noted that other factors, such as market conditions, financing, and long-term returns, play a far greater role in shaping their decisions. Overall, this indicates the relief’s influence on investment decisions among investors with small portfolios is limited.

From the interview findings, there was a clear division in the use of MDR among stakeholder groups. Larger landlords, developers, and investors described the relief as essential in making many multi-property transactions financially viable. One landlord highlighted the numerous costs involved in purchasing an already rented property, such as higher mortgage payments, insurance, compliance checks, and transaction taxes, which can sometimes exceed rental income. Applying MDR helps to reduce the overall tax burden, making it financially feasible to purchase multiple rented properties that might otherwise fail to meet lenders’ mortgage stress tests. A solicitor observed that the relief is particularly helpful in transactions involving build-to-rent and student accommodation developments, noting that it often influences purchase decisions in those markets. Overall, stakeholders generally agreed that MDR primarily benefits larger commercial landlords, developers, and investors, and that it is especially valued by those who are able to make frequent use of it.

In contrast, many smaller landlords showed limited awareness or understanding of the relief. Estate agents and solicitors with smaller-scale clients also reported minimal exposure to MDR, describing it as rarely relevant to their typical transactions since few clients purchase multiple properties at once. Several interviewees commented that most landlords are too small to benefit from the relief, as they typically buy and sell one property at a time. Some landlords also appeared to confuse MDR with the 6+ dwellings ADS exemption, suggesting low awareness and understanding of the relief’s specific purpose. Another stakeholder noted that the number of MDR claims is relatively low and agreed that the relief may not be well understood by many taxpayers.

Objectives

Some investors and developers believed that the MDR had largely accomplished its goal by fostering investment in the private rented sector through smoothing tax liabilities and reducing the overall tax burden. Stakeholders who had used the relief felt it aligned institutional investors with private individuals and homeowners, thereby levelling the playing field. They also highlighted that, due to the progressive structure of LBTT, the most significant benefits of MDR accrue to higher‑value properties, where the absolute tax relief is greatest. Several investors noted that MDR helps reduce the upfront costs associated with investment transactions, which can, in turn, support activity across the private rental sector. They explained that higher tax burdens constrain the prices investors can offer for portfolios or blocks of flats while maintaining target yields, which may discourage both investment and seller participation. A solicitor interviewed also commented that the relief acts as a useful mechanism to encourage large-scale investment.

However, some investors who had used the relief did not view MDR as a positive incentive, but rather as the removal of a barrier, an absence of a disincentive rather than an active stimulus to invest. Many stakeholders acknowledged the benefits of the relief but stressed that its potential positive effects have been overshadowed by wider policy developments, most notably rent controls introduced by the Scottish Government. These measures were regarded as having a far greater impact on investor behaviour, dampening interest in large‑scale residential investment and reducing confidence in the Scottish market. It was noted that it could take “five years of sensible tax policy to enable people to build back up confidence to invest in new developments in Scotland.” One stakeholder also questioned the fairness of excluding multiple purchases made across the year from MDR eligibility, when equivalent transactions linked in a single event would qualify for the relief.

Complications and avoidance

A few stakeholders observed that calculating the amount of tax due can be complex and requires a degree of expertise to claim correctly. One stakeholder from the legal sector explained that many conveyancers are encountering particular circumstances for the first time and are unfamiliar with all of the complexities of LBTT legislation. They described undertaking substantial advisory work for smaller firms, often to determine either the appropriate LBTT liability or the optimal approach in complex cases, given the legislation’s complexity. They suggested that clearer and more detailed guidance could help address some of these challenges.

Another issue discussed was tax avoidance, particularly activities observed in England under SDLT. One stakeholder noted a previous history of compliance cases and boundary-pushing by agents regarding MDR. Stakeholders provided examples of individuals stretching the definition of a dwelling to claim MDR, for instance, treating a shed or annex as a separate unit, contrary to the policy’s intent. It was noted that the equivalent SDLT relief had been withdrawn in England due to widespread misuse, with very few legitimate claims. However, stakeholders emphasised that the situation in Scotland differs significantly, with far lower levels of avoidance activity and no evidence of similar practices being reported.

Alternative approaches

Stakeholders who had made use of the relief were strongly opposed to its removal, as has occurred in England and Northern Ireland under SDLT. They argued that abolishing MDR and increasing tax liabilities would seriously undermine development viability in Scotland. Several stakeholders cited the removal of MDR in England as having caused significant challenges to the viability of new investment schemes there. One stakeholder mentioned they were preparing case studies to support a campaign advocating for its reinstatement. A number of investors noted that the continued availability of MDR in Scotland currently provides a competitive advantage over England, albeit one of the few remaining advantages Scotland enjoys. One stakeholder remarked that “if it were removed, it would be another nail in the coffin of residential development viability in Scotland.” Another criticised the removal of MDR from SDLT as an excessive anti-avoidance measure, likening it to “a sledgehammer to crack the wrong nut.”

One solicitor commented that they had not yet observed clear evidence of negative investment impacts following MDR’s removal in England. However, they acknowledged that it would be difficult to prove a negative impact, as one cannot know whether certain projects would have gone ahead without MDR. Nonetheless, they concluded that, given current property market problems, in particular rent control policies in Scotland, this would be an especially poor time to remove MDR.

Some investors offered alternative ways to reform MDR to better support private rental investment. They suggested the relief could be redesigned to accelerate large-scale homebuilding, incentivising developers to build at scale to meet housing demand. One proposal was to structure MDR so that tax relief grows with the number of homes built, encouraging larger schemes that can drive housing supply. Another investor proposed linking LBTT to the definition of build-to-rent properties used for rent control exemptions. Under this model, build-to-rent developments would attract a separate LBTT rate, removing the need for MDR altogether.

Contact

Email: devolvedtaxes@gov.scot