Land and Buildings Transaction Tax: review

An independent analysis of certain aspects of Land and Buildings Transaction Tax (LBTT) policy.

Non-Residential and Mixed-use Treatment

Summary

This is a summary of our analysis of the LBTT treatment of non-residential and mixed-use property.

Objectives

To increase competitiveness and attractiveness for business investment in Scotland, and ensure that smaller businesses pay the lowest or zero LBTT rates (Scottish Government, 2017).

Technical overview

Not a relief, but a separate tax structure.

Treats non-residential property (or a mixture of non-residential and residential) as distinct from residential property. Non-residential tax rates were lower than residential rates (Scottish Government, 2017).

Interactions with other reliefs and mechanisms

With MDR: If a transaction includes multiple dwellings and non-residential property, the buyer may claim MDR on the dwellings. and pay non-residential LBTT on the non-dwelling part (Land and Buildings Transaction Tax (Scotland) Act 2013, Sch 5).

With ADS: For purely non-residential transactions with no dwellings involved, no ADS is applied, but may be payable for a mixed transaction (Land and Buildings Transaction Tax (Scotland) Act 2013, Sch 2A).

With the 6+ dwellings ADS exemption: Non-residential tax bands are used, and no ADS is payable (Land and Buildings Transaction Tax (Scotland) Act 201, s 59).

With first-time buyer relief: The relief only applies to purchases of entirely residential property, with a single exception (Land and Buildings Transaction Tax (Scotland) Act 2013, Sch 4A).

Comparative analysis

England and Northern Ireland’s SDLT, and Wales’ LTT, broadly treat commercial or mixed property deals similarly to Scotland’s LBTT.

SDLT and LBTT have the same bands, but there are rate differences, with LBTT rates being lower than or equal to SDLT (e.g., 1% vs 2% for a purchase price between £150,001-250,000) (The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; UK Government, 2025)

LTT and LBTT have different bands and rates. (e.g., LTT has 4 bands with a highest rate of 6% vs LBTT has 3 bands with a highest rate of 5%) (Welsh Government, 2024a).

Materiality analysis

Materiality analysis indicates revenues from residential property transactions have consistently exceeded those from non-residential transactions (Revenue Scotland, 2025c).

A considerably higher proportion of LBTT relief claims arises from residential property transactions than non-residential ones, although the value of revenue forgone due to reliefs has been much greater in the non-residential sector (Revenue Scotland, 2025c).

Impact analysis

Despite the relatively more favourable treatment of non-residential transactions, residential property transactions became relatively more common in Scotland following the introduction of LBTT. This same pattern was not seen in England and Wales (UK Government, 2025).

However, this analysis does not control for the wider set of factors that may have influenced residential and non-residential transactions over this period.

Findings from stakeholder engagement

Most investors and landlords did not believe LBTT rate differences strongly influenced their investment behaviour.

Few landlords or investors had used or were aware of the mixed property rule; awareness was particularly limited among smaller investors, but those familiar felt it simplified transactions involving mixed-use properties and supported Scotland’s competitiveness.

Legal professionals highlighted significant ambiguity in property classification and inconsistencies in available guidance, calling for clearer, more detailed support and alignment with HMRC standards.

Support was expressed across groups for an apportionment approach, taxing each property type at its corresponding rate, despite some concerns over potential valuation challenges.

Objectives

This is a separate rate structure rather than a relief; however, classifying a purchase as non-residential typically yields a lower tax liability than the equivalent residential purchase under LBTT. Early discussions regarding the non-residential regime envisioned a lower top rate of tax for non-residential property to minimise a disproportionate impact on businesses in Scotland (Scottish Government, 2012a). The explicit policy objective behind the 2018 reset of non-residential LBTT bands was to make Scotland’s non-residential rates “the most competitive in the UK” and thereby support Scotland’s competitiveness and attractiveness for business investment. It was also expressed that LBTT’s regime for non-residential transactions would ensure that smaller businesses pay the lowest or zero rates (Scottish Government, 2017).

Technical overview

Description and administration

- While not a relief, the tax payable on a transaction comprising either a non-residential interest or a mixture of residential and non-residential interests (which is treated as a non-residential transaction under LBTT) is calculated using non-residential rates and bands. This typically yields a lower charge than the residential schedule at comparable prices.

- Reported as non-residential on LBTT return.

Timeframe and value

- In effect since LBTT’s introduction on 1st April 2015.

- The non-residential LBTT rates are currently: (i) 0% on the portion of the purchase price up to £150,000, (ii) 1% on the portion from £150,001 up to £250,000, and (iii) 5% on the portion over £250,000.

- For comparison, the residential LBTT rates are currently (i) 0% on the portion of the purchase price up to £145,000, (ii) 2% on the portion from £145,001 to £250,000, (iii) 5% on the portion from £250,001 to £325,000, (iv) 10% on the portion from £325,001 to £750,000, and (v) 12% on the portion over £750,000.

For ease of reference, both schedules are presented in Tables 1 and 2.

Table 1. LBTT schedule for residential properties

Purchase price

Up to £145,000

LBTT rate

0%

Purchase price

£145,001 to £250,000

LBTT rate

2%

Purchase price

£250,001 to £325,000

LBTT rate

5%

Purchase price

£325,001 to £750,000

LBTT rate

10%

Purchase price

Above £750,000

LBTT rate

12%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015

Table 2. LBTT schedule for non-residential and mixed-use properties

Purchase price

Up to £150,000

LBTT rate

0%

Purchase price

£150,001 to £250,000

LBTT rate

1%

Purchase price

Above £250,000

LBTT rate

5%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015

Eligibility criteria and limitations

- A transaction qualifies as non-residential if it involves: (i) commercial property, (ii) forests, (iii) agricultural land, or (iv) six or more residential properties bought in a single transaction (see the 6+ dwellings ADS exemption below). Also treated as non-residential property are buildings used as the following: (i) a home/institution providing residential accommodation for children; (ii) a hall of residence for students in further/higher education; (iii) a home/institution for persons in need of personal care due to age/disability/drug/alcohol dependency/mental health conditions; (iv) a hospital/hospice; (v) a prison or similar establishment; or (vi) a hotel/inn or similar establishment.

- Note that the ADS does not apply to non-residential property transactions. However, where a mixed transaction includes a residential dwelling or dwellings, the ADS will apply to 8% (the current ADS rate) of the chargeable consideration for the corresponding part of the transaction.

Interactions with other reliefs and mechanisms

Between non-residential/mixed-use properties and MDR

If a transaction includes multiple dwellings and non-residential property (e.g., an estate with cottages and farmland), the buyer can potentially claim MDR on the dwellings and still pay non-residential LBTT on the non-dwelling part. The formulas for MDR explicitly separate “remaining property” (the non-residential portion) from dwellings to integrate the two regimes, essentially ignoring the non-residential part when calculating the MDR for the dwellings. This interaction ensures that having a commercial element in a transaction does not nullify the benefit of the MDR on the residential part. Conversely, if one of the dwellings in an MDR claim is in fact a commercial unit, it cannot be counted towards the MDR. The overall effect is that non-residential land acquisitions and the MDR interact in mixed transactions to significantly reduce the tax payable on the dwelling part (via averaging on dwellings) while attracting the lower non-residential rates on the non-dwelling part (Revenue Scotland, 2025a interpretation).

Between non-residential/mixed-use properties and ADS

A transaction deemed entirely “non-residential” under LBTT is outside the scope of the ADS. For purely commercial transactions with no dwellings involved, this means that no ADS is applied. A notable case is mixed-use transactions, e.g., buying a building that has both a shop and a flat, or a house with substantial land or a commercial element. By statute, a mixed transaction is taxed as non-residential, so the base LBTT is at the lower non-residential rates. However, the ADS may still be payable in a mixed transaction: if the transaction includes a residential dwelling that meets the conditions for ADS to be payable (e.g., the buyer is not replacing their main residence, its value is £40,000 or higher), the 8% ADS is charged on the portion of the consideration attributable to that dwelling. For example, if someone buys a £1 million property that is half commercial, half dwelling, which meets the conditions for ADS to be payable, LBTT is computed under non-residential bands on the £1 million, but the 8% ADS still applies to the £500,000 dwelling portion (Revenue Scotland, 2024c interpretation).

Between non-residential/mixed-use properties and 6+ dwellings ADS exemption

When a buyer purchases six or more separate dwellings in a single transaction, the transaction is treated as non-residential for LBTT purposes. The immediate consequences are twofold: (1) LBTT is calculated using the non-residential tax bands, and (2) full exemption from the ADS is granted, meaning no ADS is payable. This mechanism is effectively a special exemption that large residential portfolio transactions enjoy. However, the 6+ dwellings ADS exemption still applies if the transaction includes a non-residential element, provided that it also involves six or more residential dwellings (as per the conditions of the exemption). In such cases, no ADS is paid on either the residential portion or the non-residential portion – the former due to the 6+ dwellings exemption and the latter due to the ADS not being payable on the non-residential portions of mixed transactions (see above) (Revenue Scotland, 2024d interpretation).

Between non-residential/mixed-use properties and first-time buyer relief

The first-time buyer relief raises the nil-rate LBTT band to £175,000 for qualifying first-time purchases. The relief only applies to purchases of entirely residential property – if the transaction includes any non-residential element or is a linked transaction (part of a series of transactions), it will not qualify for the relief with a single exception. The exception is in the case of a linked transaction involving a residential and a linked non-residential purchase where the latter is either the garden or grounds of the residential property or is land that subsists or is to subsist for the benefit of that property. In such cases, the relief will be available on the total consideration of the linked transaction (Revenue Scotland, 2024e interpretation).

Comparative analysis

This section presents a comparative analysis of LBTT’s treatment of non-residential and mixed-use transactions in Scotland vis-à-vis SDLT in England and Northern Ireland and LTT in Wales.

Key differences between LBTT and SDLT

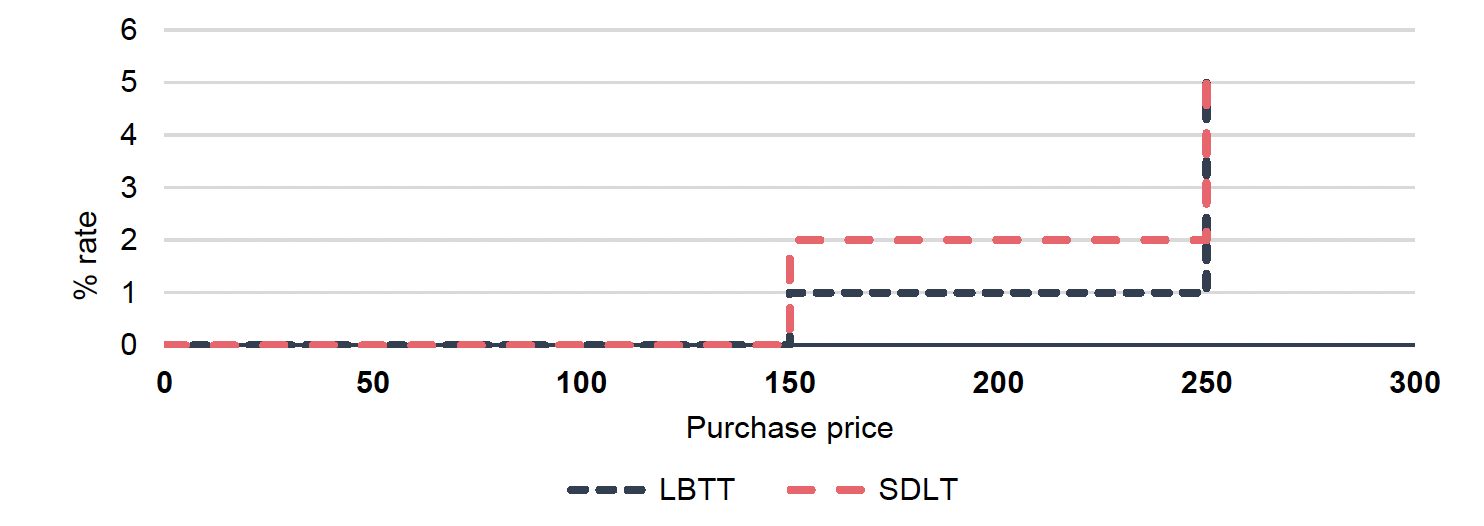

Both Scotland’s LBTT and England and Northern Ireland’s SDLT maintain separate regimes for non-residential and mixed-use transactions, which are shown in the table below. Under LBTT, non-residential purchases (e.g., commercial properties or land) are taxed on a slice basis at 0% up to £150,000, 1% on £150,001-250,000, and 5% above £250,000. SDLT similarly taxes non-residential transactions at 0% up to £150,000 and 5% above £250,000, but imposes 2% on £150,001-250,000 (see table and figure below). Thus, for mid-sized commercial purchases (e.g., £200,000-300,000), LBTT’s 1% middle rate produces a slightly lower liability than SDLT’s 2% rate on the same band, with a maximum variation of £1,000. It was Scotland’s 2019 reform of non-residential LBTT rates that aligned its lower and top rates and thresholds with the SDLT regime. LBTT’s lower 1% middle rate (versus 2% in SDLT) is arguably consistent with the Scottish Government’s stated approach of ensuring smaller businesses pay lower rates of LBTT (Scottish Government, 2017).

| Purchase price | LBTT rate | SDLT rate |

|---|---|---|

| Up to £150,000 | 0% | 0% |

| £150,001 to £250,000 | 1% | 2% |

| Above £250,000 | 5% | 5% |

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; UK Government (2025)

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; UK Government (2025)

The definition of non-residential versus residential property is materially the same under both taxes. In broad terms, “residential property” covers real estate used or suitable for use as a dwelling, whereas “non-residential” encompasses all other land or structures. Crucially, any mixed-use transaction (one that includes both residential and non-residential elements) is treated wholly as non-residential for tax purposes in Scotland, as well as in England and Northern Ireland. This means, for example, the purchase of a building comprising a shop with a flat above is taxed at non-residential rates with no supplement for additional dwellings (HM Revenue & Customs, 2025a; Revenue Scotland, 2025e). Both jurisdictions embed this rule in legislation (UK Government, 2003; Scottish Government, 2013). In practice, this alignment ensures that Scotland’s LBTT and England and Northern Ireland’s SDLT produce broadly similar outcomes for commercial or mixed property deals, aside from the rate differences noted. Neither system attempts to apportion consideration between residential and commercial components; the entire transaction falls into the non-residential schedule by default.

Key differences between LBTT and LTT

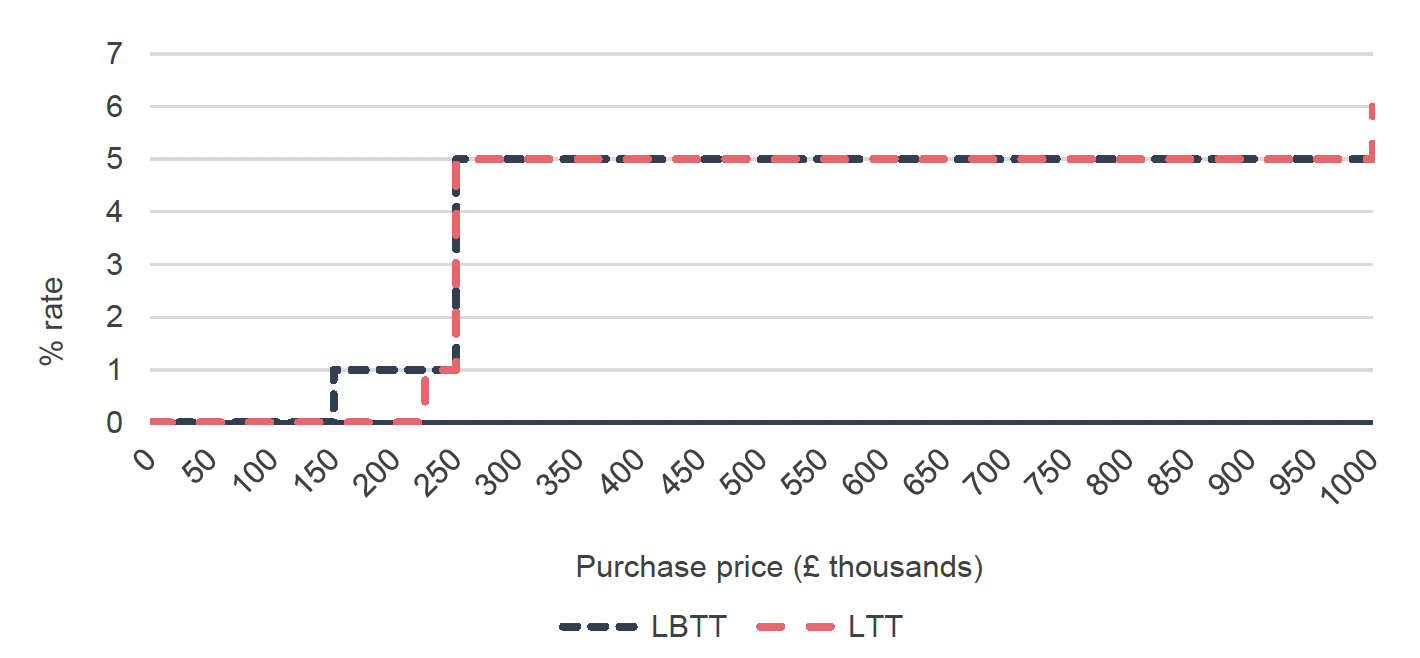

Scotland’s LBTT and Wales’s LTT are relatively similar in their treatment of non-residential and mixed-use transactions, reflecting policy learning and shared objectives between the two devolved systems. Both apply separate non-residential rate schedules and classify any mixed-use deal as non-residential. A chief difference lies in rate bands. As of 2025, Welsh LTT non-residential rates are 0% on consideration up to £225,000, 1% on £225,001-250,000, 5% on £250,001-1,000,000, and 6% on any portion above £1,000,000 (see Table 5 and Figure 3 below). In contrast, Scotland’s LBTT non-residential rates are 0% up to £150,000, 1% on £150,001-250,000, and 5% on anything above £250,000 (see Table 4). Thus, Wales sets a higher entry threshold (£225,000 versus £150,000) before any tax is due on commercial property, but then introduces a 6% rate for very expensive transactions (over £1,000,000). Scotland imposes taxation much earlier (£150,000), affecting smaller purchases (e.g., a £200,000 shop pays £500 LBTT versus £0 LTT), but never exceeds 5% regardless of price. It should be noted that LTT’s nil rate at the time of introduction (1st April 2018) was also limited to purchase prices up to £150,000 and only diverged in December 2020 (Welsh Government, 2024a).

Table 4. LBTT schedule for non-residential and mixed-use properties

Purchase price

Up to £150,000

LBTT rate

0%

Purchase price

£150,001 to £250,000

LBTT rate

1%

Purchase price

Above £250,000

LBTT rate

5%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015

Table 5. LTT schedule for non-residential and mixed-use properties

Purchase price

Up to £225,000

LTT rate

0%

Purchase price

£225,001 to £250,000

LTT rate

1%

Purchase price

£250,001 to £1,000,000

LTT rate

5%

Purchase price

Above £1,000,000

LTT rate

6%

Source: Welsh Government (2024a)

Sources: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015; Welsh Government (2024a)

As for mixed-use property, both LBTT and LTT legislation adopt the same fundamental rule: if a transaction comprises both residential and non-residential property, it is taxed entirely on a non-residential basis (with no apportionment between residential and commercial components) (Welsh Government, 2021a). As such, the primary difference between the two regimes with respect to non-residential and mixed-use properties is the rate thresholds and the presence of Wales’s 6% top marginal rate on non-residential considerations over £1,000,000.

Materiality analysis

The following section explores how residential and non-residential property transactions differ in their contribution to tax revenues, returns, relief claims, and forgone earnings. Data on total LBTT revenues can be broken down into transactions from residential and non‑residential properties. As shown in Table 20 and Figure 27 in Appendix 2, revenues from residential property transactions have consistently exceeded those from non‑residential transactions. The time series highlights how the difference between revenues from residential and non-residential transactions was relatively small at the start of the series in 2015/16. However, this gap has widened steadily over time, reaching the point where, by 2024/25, residential property transactions account for 77% of all declared LBTT revenue. This is likely partly due to several increases in the ADS rate on residential second homes, which has risen from 3% at its introduction to 8% today. Revenues from the ADS have grown substantially since it was first introduced.

Table 21 presents data on the number of LBTT tax returns, highlighting an even larger disparity between residential and non-residential transactions. Residential transactions consistently make up the bulk of LBTT transactions. Throughout the period between 2015/16 and 2024/25, the residential share of transactions remained high and stable, shifting only marginally from 94% to 93% over the period.

Table 22 displays LBTT relief claims broken down by residential and non-residential transactions. The data show that residential property transactions account for a far greater share of LBTT relief claims than non-residential ones. Over the period, the number of residential relief claims increased sharply, both in absolute terms and as a share of total claims. While residential transactions made up 56% of all relief claims in 2015/16, this proportion had risen to over 95% by 2021/22. It is also notable that both the absolute number of residential relief claims and their share of total claims jumped markedly in 2018/19. This coincides with the introduction of First-Time Buyers Relief in 2018, suggesting that this relief was the primary driver of the shift.

Whilst the number of relief claims has been considerably higher for residential property transactions, the pattern for foregone revenue tells a different story. As shown in Table 23 and Figure 28, the value of revenue forgone due to reliefs was substantially greater in the non-residential sector than in the residential sector. While residential foregone revenue from reliefs represented only around 3-9% of residential revenues over the period, non-residential reliefs accounted for as much as 91% of non-residential revenues. This is primarily attributable to group relief on non‑residential property, which represents by far the largest source of revenue forgone, accounting for 57% of total LBTT revenue forgone in 2023/24 (Revenue Scotland, 2024f).

Impact analysis

The following section undertakes an analysis of the impact of the differing treatment between residential and non-residential properties under LBTT. This element was chosen for this analysis in part due to the availability of relevant time series data predating the introduction of LBTT. It is important to note that the following findings offer only suggestive evidence of impact based on observed trends over time. While we draw on evidence from other UK stamp duty systems, specifically SDLT in England and LTT in Wales, to partially account for factors affecting all three nations, this analysis cannot control for many confounding factors that may have changed over time and influenced property transaction patterns in the Scottish market. As such, these results should not be interpreted as providing definitive causal evidence of impact.

As shown in Tables 6 and 7, the tax payable on a non-residential transaction relative to an equivalent residential transaction is lower, by operation of both lower rates and their application to wider bands. For instance, the top rate for residential property transactions is 12%, whereas the highest non-residential rate is capped at 5%. Similarly, band thresholds are more favourable to non-residential properties; for example, the nil-rate band is set slightly higher. This means that property transactions of the same value typically incur lower LBTT liabilities when classified as non-residential. Finally, it is important to note that where a transaction includes any non-residential element, LBTT treats the entire transaction as non-residential.

Table 6. LBTT schedule for residential properties

Purchase price

Up to £145,000

LBTT rate

0%

Purchase price

£145,001 to £250,000

LBTT rate

2%

Purchase price

£250,001 to £325,000

LBTT rate

5%

Purchase price

£325,001 to £750,000

LBTT rate

10%

Purchase price

Above £750,000

LBTT rate

12%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015

Table 7. LBTT schedule for non-residential and mixed-use properties

Purchase price

Up to £150,000

LBTT rate

0%

Purchase price

£150,001 to £250,000

LBTT rate

1%

Purchase price

Above £250,000

LBTT rate

5%

Source: The Land and Buildings Transaction Tax (Tax Rates and Tax Bands) (Scotland) Order 2015

Given the more favourable treatment of non-residential transactions compared to residential ones, LBTT may create incentives that increase the relative volume of non-residential property transactions. The following analysis draws on evidence from the UK Government (2025), which reports annual numbers of residential and non-residential transactions. These data are used to construct a ratio of residential to non-residential transactions, enabling us to assess whether the introduction of LBTT has been associated with any discernible shifts in their relative proportions.

Analysis

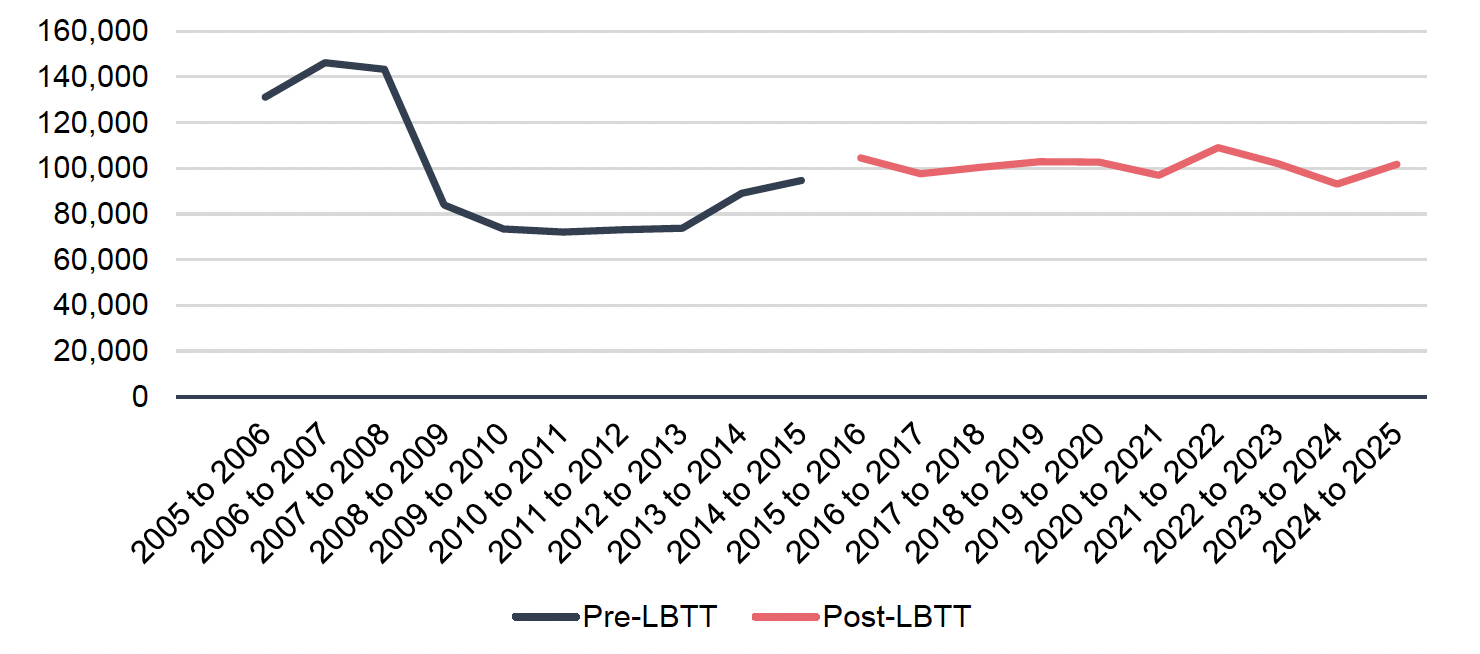

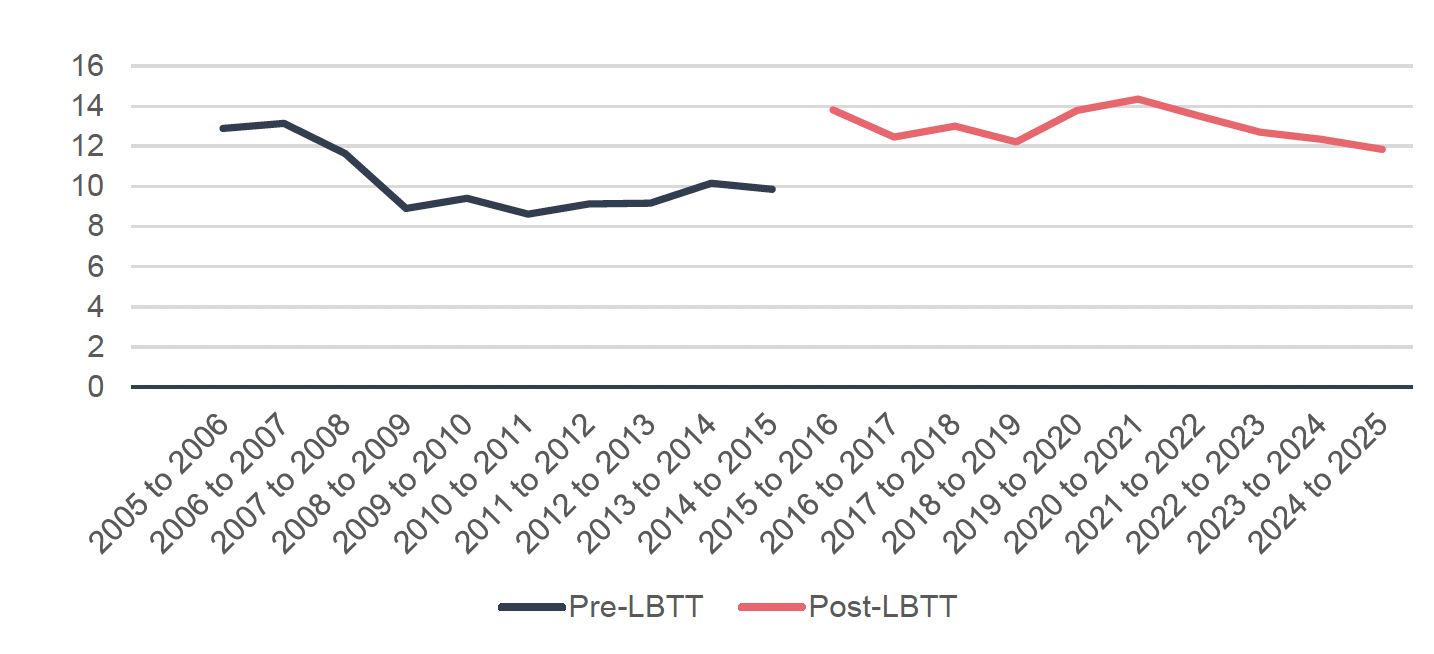

Our analysis suggests that residential property transactions became relatively more common in Scotland following the introduction of LBTT[8]. A simple pre-post comparison, shown in Table 8, indicates that between 2005 and early 2015, there was an average of 10.3 residential transactions for every non-residential transaction. In the period from April 2015, when LBTT was introduced, to early 2025, this ratio rose to 13.

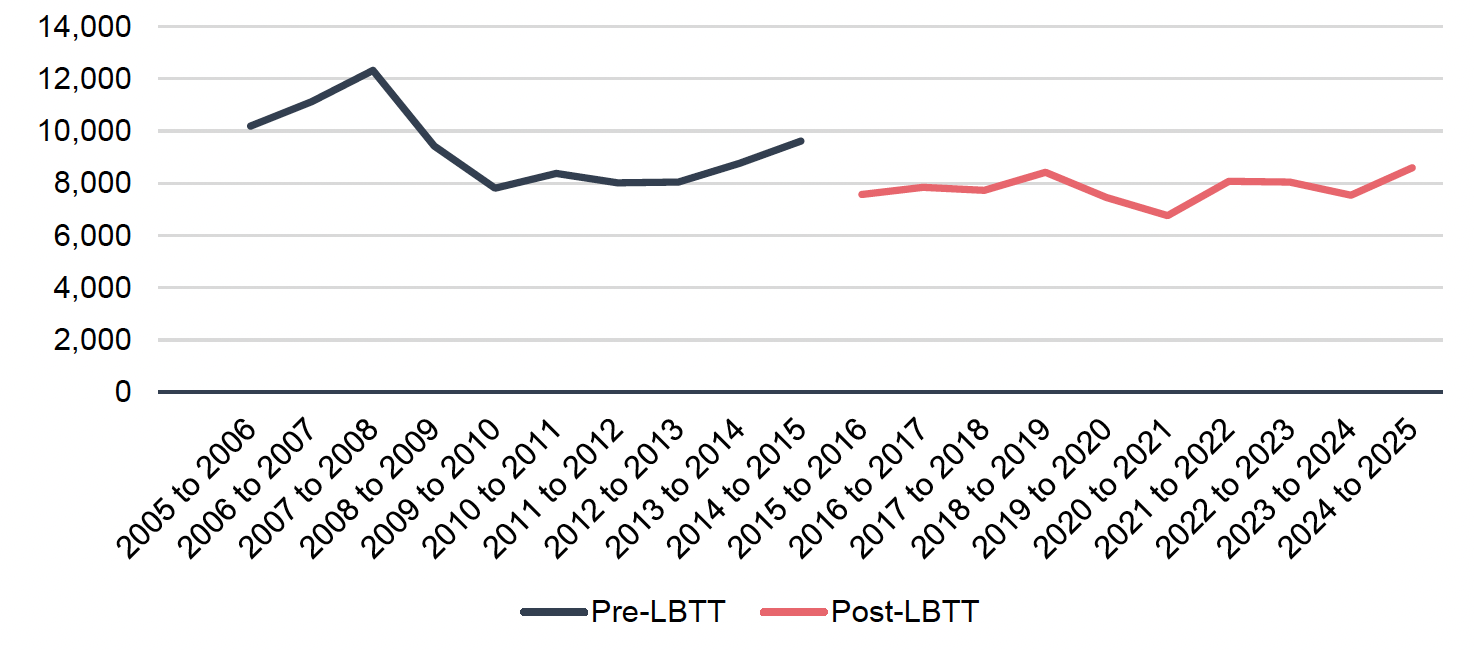

The figures indicate that the decline was largely driven by a reduction in non‑residential property transactions. On average, annual non‑residential transactions in the period following the introduction of LBTT were 17% lower than in the pre‑LBTT period. In contrast, residential property transactions over the same period rose by 3%. It should also be noted, however, that part of the observed decline in non-residential transactions may reflect a shift from property purchases toward leasing arrangements, rather than necessarily indicating a reduction in underlying market activity.

| - | Pre-2015 average | Post-2015 average | Difference | Percentage increase |

|---|---|---|---|---|

| Scotland annual residential property transactions | 98109 | 101,131 | 3,022 | 3% |

| Scotland annual non-residential property transactions | 9,369 | 7,803 | -1,566 | -17% |

| Ratio of residential to non-residential property transactions | 10.29 | 13.00 | 2.71 | 26% |

Source: UK Government (2025)

The graphical representation of total residential and non-residential conveyances shown in Figures 4 and 5 illustrates this shift with a clear decline in non-residential transactions since 2015, while residential transactions have remained relatively stable. Figure 6 shows the ratio between residential and non-residential conveyances over time and highlights a marked increase in the ratio between 2014/15 and 2015/16, coinciding with the introduction of LBTT. This pattern contrasts with the case of first-time buyer reliefs, where differences before and after the policy appeared to reflect an already ongoing upward trend. The distinct shift in 2015 provides suggestive evidence that the introduction of LBTT influenced housing transactions.

This pattern is somewhat counterintuitive given the preferential treatment afforded to non-residential property under LBTT, which might instead have been expected to reduce the ratio. It is important to note, however, that SDLT, the predecessor to LBTT, also included separate rates and bands for residential and non-residential property, with stronger preferential treatment for non-residential transactions. If SDLT provided greater relative advantages for non-residential property than LBTT, this could help explain the observed increase in the ratio in Scotland after 2015. This issue is explored further in the comparative analysis with other UK nations in the section below.

Nevertheless, it must be emphasised that this analysis does not control for the wider set of factors that may have influenced residential and non-residential transactions over the period. The findings should therefore not be interpreted as strong causal evidence of LBTT directly changing the balance between these transaction types.

Source: UK Government (2025)

Source: UK Government (2025)

Source: UK Government (2025)

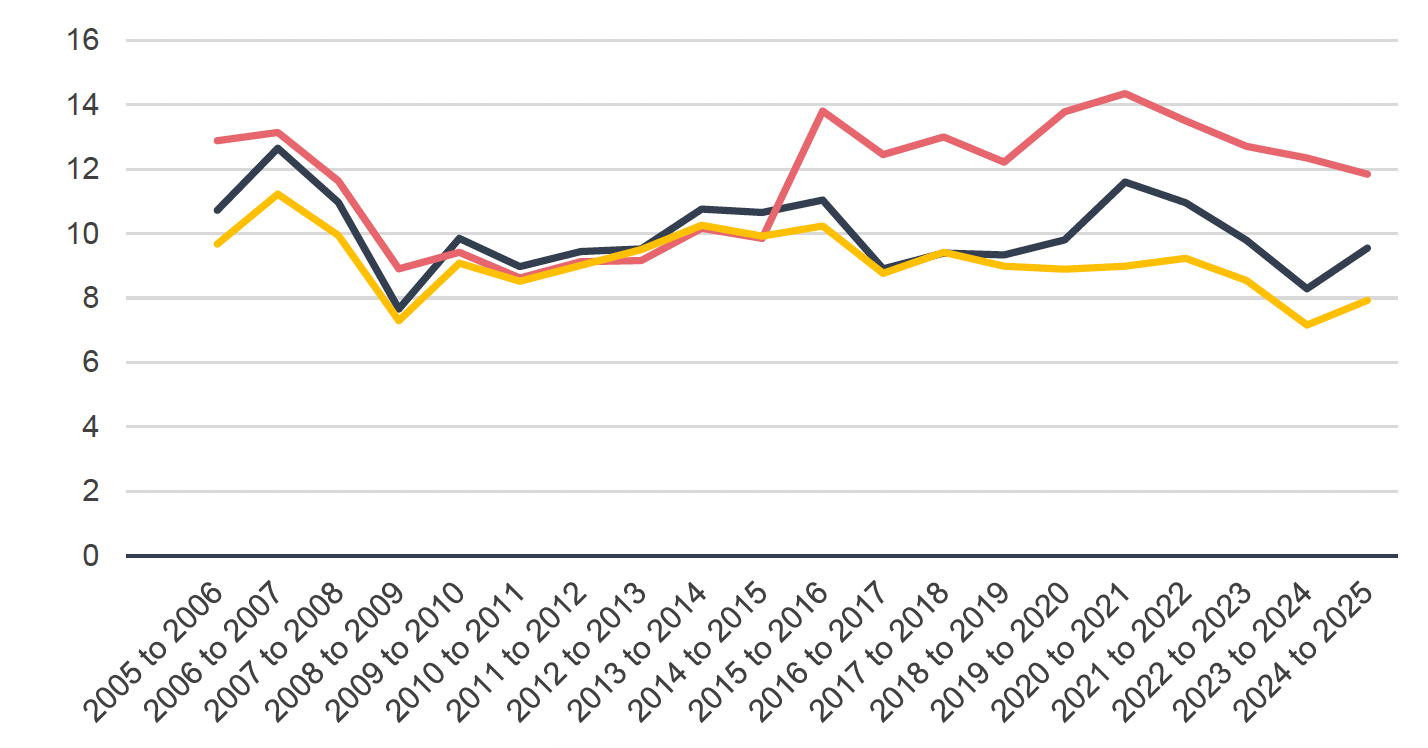

Comparison with other UK nations

In terms of treatment of different property types, the property transaction tax systems in England and Northern Ireland (SDLT) and Wales (LTT) share similar structures to LBTT, with different bands and rates applying to residential and non-residential property transactions. In both SDLT and LTT, non-residential transactions are again generally taxed more favourably, as lower rates typically apply. The detailed rates and bands for each system are shown in Tables 9 and 10 below.

Figure 7 illustrates the ratio of residential to non-residential conveyances across the three nations considered. This comparison makes the rise in Scotland’s rate appear even more pronounced. While the ratios in England and Wales have remained broadly stable or even declined slightly since the introduction of LBTT, Scotland shows a distinct increase. This suggests that the shift to LBTT may have influenced the balance of transactions, raising the relative prevalence of residential property purchases in Scotland. Nevertheless, although cross-national comparisons help control for factors common across countries, many other influences are also likely to have shaped these trends. As such, the evidence should be interpreted as indicative rather than conclusive of a causal impact from the introduction of LBTT. It is also important to caveat that changes in the absolute or relative number of conveyances do not necessarily reflect overall market activity, as shifts may also be occurring within the leasehold market.

|

LBTT (Scotland) Band |

- Rate |

SDLT (England and Northern Ireland) Band |

- Rate |

LTT (Wales) Band |

- Rate |

|---|---|---|---|---|---|

| Up to £145,000 | 0% | Up to £125,000 | 0% | Up to £225,000 | 0% |

| £145,001 to £250,000 | 2% | £125,001 to £250,000 | 2% | £225,001 to £400,000 | 6% |

| £250,001 to £325,000 | 5% | £250,001 to £925,000 | 5% | £400,001 to £750,000 | 7.5% |

| £325,001 to £750,000 | 10% | £925,001 to £1.5 million | 10% | £750,001 to £1.5 million | 10% |

| Above £750,000 | 12% | Above £1.5 million | 12% | Above £1.5 million | 12% |

Source: See Comparative analysis

|

LBTT (Scotland) Band |

- Rate |

SDLT (England and Northern Ireland) Band |

- Rate |

LTT (Wales) Band |

- Rate |

|---|---|---|---|---|---|

| Up to £150,000 | 0% | Up to £150,000 | 0% | Up to £225,000 | 0% |

| £150,001 to £250,000 | 1% | £150,001 to £250,000 | 2% | £225,001 to £250,000 | 1% |

| Above £250,000 | 5% | Above £250,000 | 5% | £250,001 to £1 million | 5% |

| - | - | - | - | Above £1 million | 6% |

Source: See Comparative analysis

Source: UK Government (2025)

Findings from stakeholder engagement

Summary of findings

Stakeholders expressed mixed views on LBTT rate differentials between residential and non-residential properties. Some felt lower non-residential rates encouraged conversions to housing, while others questioned fairness, suggesting rates should reflect land area used rather than property type. Few used the mixed property rule, and it was thought that the current rules primarily benefit larger or mixed-use buyers. Legal professionals highlighted ambiguity in classifying properties and inconsistent guidance from Revenue Scotland. Broad support emerged for an apportionment approach, taxing each property element at its relevant rate.

Differential rates between residential and non-residential transactions

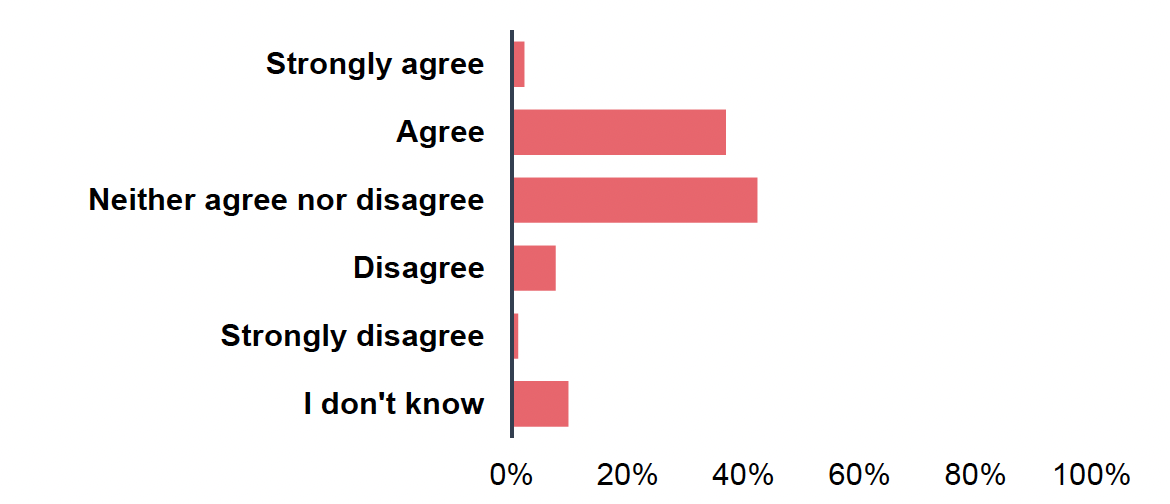

By and large, respondents to the survey of individual investors did not express strong views on the differential rates of LBTT for residential and non-residential properties. In the survey, when investors were asked to what extent they agreed that the lower LBTT rates on non-residential and mixed property transactions enabled them to undertake investments they would otherwise be unable or unwilling to, responses were mixed. While just under 2/5 (37%) agreed and a small proportion (2%) strongly agreed, suggesting that the relief may have had some influence on investment decisions, a similar share (42%) neither agreed nor disagreed (see Figure 8). Meanwhile, only a minority disagreed (8%) or strongly disagreed (1%), and 10% stated that they did not know. Furthermore, out of the 92 investors surveyed, only 6% owned a purely non-residential or a mixed residential and non-residential property.

When asked to expand on these responses, the qualitative findings from the survey align closely with the quantitative results, showing that most investors did not perceive the differential LBTT rates between residential and non-residential or mixed-use properties as having a strong effect on their investment behaviour. The majority of respondents said the tax treatment has little to no impact on their decisions, often because they only invest in residential properties or are not in a position to purchase additional assets. Many also admitted to a limited understanding of how the rules work, stating that they would rely on accountants or solicitors to advise them. For these investors, other factors such as market opportunities, affordability, and long-term returns are more influential than the relative tax rates.

Furthermore, in the stakeholder interviews, some landlords and property developers observed that non-residential properties generally have a lower value per square foot, alongside lower LBTT rates. They suggested that this can create incentives for purchasing non-residential properties and converting them into residential use. Anecdotal evidence supported this view, indicating that such conversions are seen as a viable investment strategy compared with buying residential properties outright. Several stakeholders mentioned either having considered this approach themselves or knowing others who had undertaken such conversions.

Some investors, however, disagreed with the current rate differentials. One described it as difficult to justify the variation in rates when both types of property occupy the same amount of land, suggesting instead that LBTT should be calculated based on land area rather than property use. Stakeholders also noted that, compared with SDLT, the Scottish LBTT system imposes higher taxes on mid- to high-value properties. A few respondents linked this to wider challenges in the Scottish housing market, arguing that current LBTT rates may deter residential investment and that more could be done to encourage residential development through tax policy.

Mixed property rule

Findings from the interviews and the survey of individual investors indicated that stakeholders had not themselves made use of the mixed property rule. As shown in Figure 9 below, limited awareness and understanding of the relief among smaller landlords were identified. When landlords were asked whether they were aware of the relief prior to taking part in the survey, only 24% (22 out of 92) answered ‘yes.’ The majority of respondents (66%) stated that they were not aware of the relief, while the remaining 10% were unsure.

Interviews with some stakeholders suggested that the rule helps maintain simplicity for taxpayers by classifying properties entirely as either residential or non-residential. Some viewed this as less burdensome than applying apportionment, under which the residential and non-residential parts of a property transaction would be charged different rates. Stakeholders also explained that the relief may avoid discouraging investment in non-residential property that includes a minor residential element, such as high street properties, and help to keep Scotland competitive with the rest of the UK.

Some stakeholders noted potential issues with the rule not always being used as intended. Concerns were raised about taxpayers claiming mixed property treatment where there is no clear non-residential element in the transaction, such as where part of the property is open to public access. Reference was made to significant avoidance activity under SDLT in parts of the UK, where some taxpayers have fabricated a small non-residential element to secure lower rates. One stakeholder described it as a “bit ridiculous” that a minimal non-residential component could cause an entire transaction to be treated as non-residential. However, most stakeholders agreed that avoidance activity of this type is far less common in Scotland, and they were generally unaware of examples where non-residential elements were deliberately added to transactions to benefit from lower rates.

Beneficiaries of current treatment

Many stakeholders did not believe that the current tax treatment particularly benefits any specific group. A small landlord observed that higher rates for residential properties discourage individuals from becoming landlords. Another stakeholder suggested that the current system tends to favour larger landlords and those involved in mixed property transactions, who can make use of the mixed property rule to pay lower rates of LBTT. It was generally recognised that the main beneficiaries are those purchasing mixed-use properties, as this rule allows them to be taxed at the lower non-residential rate. Larger transactions, such as former farms, are more likely to include elements of non-residential property and can therefore qualify as mixed-use, unlike smaller purchases, such as a three-bedroom semi-detached house. Another stakeholder added that buyers of large estates often benefit from similar reasons, since such estates typically contain some commercial land use that enables them to pay LBTT at the lower non-residential rate.

Complexities

Respondents, particularly those from the legal profession, noted complexities arising from the differential treatment of residential and non-residential property, including challenges in determining where the boundary between these classifications lies. Lawyers reported spending considerable time establishing whether a property should be classified as residential or non-residential in order to establish which rate of LBTT should apply. Several examples of confusion were noted, such as whether operating a home office from a private residence could make the property commercial rather than residential. A recurring concern was the lack of a clear and consistent definition distinguishing residential from non-residential property. Another stakeholder also acknowledged this as a problematic area, describing significant ambiguity and subjectivity in interpretation. They claimed that litigation cases have helped clarify definitions and provide greater clarity, but uncertainties persist.

Lawyers further raised concerns about the guidance available on residential and non-residential classifications, and on LBTT rules more broadly. They observed inconsistencies between Revenue Scotland and HMRC guidance, despite the underlying legislation often being identical. Some stakeholders felt that Revenue Scotland’s guidance lacks the detail and nuance found in HMRC’s materials. Stakeholders also reported difficulties in obtaining advice from Revenue Scotland on specific circumstances. They described instances where Revenue Scotland staff were unable or unwilling to offer definitive guidance, instead directing them back to published guidance. Many felt that Revenue Scotland could improve its guidance, aligning it more closely with HMRC’s SDLT guidance and providing clearer examples. A specific issue cited was the treatment of holiday homes, which are classified as residential properties under LBTT, even where occupation is restricted to short periods.

Use of apportionment

Across all participant groups, support was expressed for exploring an apportionment approach that better reflects the mixed nature of many property transactions. Under such a system, the residential element would be taxed at the residential rate, and the non-residential element at the corresponding non-residential rate. While some stakeholders acknowledged potential valuation challenges, interviewees noted that comparable processes already exist within ADS calculations, where the ADS is applied only to the residential portion. This was seen as evidence that the additional administrative burden could be manageable.

Contact

Email: devolvedtaxes@gov.scot