Research Data Scotland – Full Business Case

The Research Data Scotland (RDS) Full Business Case (FBC) sets out proposals for the establishment of a new national service that has the potential to save time, money and lives.

Socio-Economic Case

Introduction

A key part of the business case process is the Socio-Economic Case, in which the potential delivery options for RDS are assessed to identify the one that offers best value. This case builds on and extends the findings and conclusions of the SOC and the OBC, which undertook an initial appraisal of potential options and, in addition to the status quo, identified four potential delivery options. These options were formulated following consultation with internal SG colleagues, including legal teams, and external stakeholders.

In addition to following the standard Her Majesty's Treasury (HMT) guidance on business cases and being aligned to both the Green Book and the "5 cases" model, the FBC is consistent with the wider approach taken by SG in considering the wider socio-economic impacts of spend and policy decisions.

The Socio-Economic Case in the OBC assessed the options available to deliver RDS, identified their costs and benefits including the effect on public welfare, and set out the preferred option. Critical success factors that RDS must meet have been identified and each of the options is scored against these. The options appraisal undertaken in the OBC has been reviewed following the confirmation of the founding partners, and the outcome, restated in this FBC, remains appropriate.

Early discussions with stakeholders ruled out the possibility of including an option to place RDS within a private sector, for-profit company: this would neither align with RDS's public interest mission, nor be acceptable to the Scottish public. The four options that have been considered are all aligned with the seven Founding Principles of RDS.

Summary of Options

Option 1: Retain the status quo (SQ) – this includes "business as usual" for data linkage requests using the SILC model. The status quo for data linkage is based on a series of agreements between various partners and faces several issues relating to the complexity of the current arrangements:

- No clear structure under SILC

- No single financial overview of SILC's activities

- Administration, budgeting and governance sit across numerous organisations.

SILC is not a legal entity in its own right and does not have the capability to enter into contractual arrangements.

SQ for non-linkage projects faces similar issues:

- Inconsistency with data access routes across numerous organisations

- Lack of transparency on data holdings across numerous organisations.

Option 2: Amend the functions of an existing public body (EPB) – this option involves housing RDS as part of an existing public body. Given data protection considerations, there could be a requirement that the existing public body has a health focus. In this option, RDS would not be a separate legal entity and would not be able to enter in contractual arrangements in its own right. RDS would not be the sole focus of the existing public body and it is likely that RDS would have to adhere to the existing public body's operational processes, working culture, and governance requirements.

Option 3: Amend the functions of Public Health Scotland (PHS) – this option relates specifically to the amendment of the functions of PHS, which launched in April 2020 and includes NHS Health Scotland, Health Protection Scotland and Information Services Division. In this option, RDS would be established as a part of PHS. As with Option 2, RDS would not be a separate legal entity and would not be able to enter in contractual arrangements in its own right. RDS would not be the sole focus of PHS and it is likely that RDS would have to adhere to PHS's operational processes, working culture, and governance requirements. Given the health focus of PHS, there may also be a constraint on RDS's ability to focus on non-health related research.

Option 4: Establish a New Public Body, such as a new standalone body (NPB) – in this option, RDS would be created as a new public body in its own right. Delivery of the RDS business plan would be the sole focus of the new public body. It is likely that Scottish Ministers would have control of a new public body although there are options where this could be shared with other stakeholders. To create a new public body, legislation would have to be enacted and this would take considerable time and cost.

Option 5: Establish a Joint Venture (JV) – this option involves a joint venture company being created, in which each of the key current public sector stakeholders could be involved (if they wished to be so). Delivery of the RDS business plan would be the sole focus of the JV. Governance of the JV would include the relevant partners. If RDS were established as a JV, the legal recommendation is that it should be constituted as a Company Limited by Guarantee (CLG), which would allow it to achieve charitable status.

Socio-economic Appraisal

The socio-economic appraisal focuses on the value of the different options including non-cash efficiencies, qualitative benefits and opportunity costs. The status quo would have an ongoing operational cost but would also incur an opportunity cost due to the current arrangement's competitive disadvantage.

Options 2-5 are based on the new RDS service operating as part of an existing public sector organisation, a new public body or in some form of public sector joint venture. All these options are likely to enable RDS to achieve its mission and deliver greater value to Scotland.

The operational and delivery costs of the different options are not materially different with the exception of Option 4, which would have a longer, more constrained and more involved delivery that would require legislation to be enacted and the commitment of considerable resource and time.

In the OBC the indicative costs of the different options[9] over the first five years of operations were:

- Status quo - £25.2m (£22.7m NPV)

- Amend the functions of an existing body - £28.5m (£25.7m NPV)

- Amend the functions of PHS - £28.5m (£25.7m NPV)

- Establish a new public body - £30.6m (£27.7m)

- Establish a joint venture - £29.0m (£26.2m NV)

At that time, compared to the five-year costs of the status quo, the new options were slightly more expensive, ranging from £3.3m to £5.3m (£2.9m to £4.9m NPV). This equated to a yearly average additional cost of £0.7m to £1.1m (£0.6m to £1.0m NPV) to secure the anticipated benefits that RDS will bring.

Following further refinement of the financial model an updated five year cost profile (see the Financial Case for more details) has been produced for this FBC as follows:

| Status quo | Amend the functions of an existing body | Amend the functions of PHS | Establish a new public body | Establish a joint venture | |

|---|---|---|---|---|---|

| Staff costs | £19,123,437 | £7,306,920 | £7,306,920 | £7,306,920 | £7,306,920 |

| Non staff costs | £3,387,120 | £3,568,657 | £3,568,657 | £3,568,657 | £3,568,657 |

| Commissioning | £- | £23,842,418 | £23,842,418 | £23,842,418 | £23,842,418 |

| Transition costs | £- | £75,000 | £150,000 | £505,000 | £505,000 |

| Legislative costs | £- | £- | £- | £1,300,000 | £- |

| Sub-total costs | £22,510,557 | £34,792,995 | £34,867,657 | £36,522,995 | £35,722,995 |

| Risk contingency[10] | £4,502,111 | £6,958,599 | £6,973,599 | £7,304,599 | £7,144,599 |

| Total (5 years) | £27,012,668 | £41,751,594 | £41,841,594 | £43,827,594 | £42,867,594 |

| NPV (5 years) | £24,077,306 | £37,218,768 | £37,303,862 | £39,158,661 | £38,219,412 |

Compared to the five-year costs of the status quo, the updated option costings are slightly higher than the OBC, ranging from £14.7m to £17.4m (£13,1m to £15.0m NPV). This equates to a yearly average additional cost of £2.9m to £3.5m (£2.6m to £2.0m NPV).

The higher costs are due to a larger RDS core team, which has increased staff costs, refined non-staff costs, and more detailed transition costs. Updates to the financial model were made following the commitment of £5m pa over the next five years from the SG Health portfolio, with funding confirmation allowing more accurate budgeting.

The benefits to government from spending typically fall into four main categories:

1. Cash releasing benefits (CRB). These benefits reduce the costs to organisations in such a way that resources can be re-allocated elsewhere. This typically means that an entire resource is no longer needed for the task for which it was previously used. This can be staff or materials/assets.

For RDS, there are unlikely to be short-term material CRB: this is because the existing SILC data linkage service is being replaced with a new linkage service under RDS (initially on a largely like-for-like basis).

2. Financial but non-cash-releasing benefits (non-CRB). This usually involves reducing the time that a particular resource takes to do a task but not sufficiently to re-allocate that resource to a totally different area of work.

For RDS, the expected non-CRB benefits include quicker and clearer processes for researchers and investment in linkage ready data meaning linkage projects can be processed more efficiently.

3. Quantifiable benefits (QB). These benefits can be quantified, but not always easily. The extent to which QBs are measured will depend on their nature and significance; however, as a general rule every effort should be made to quantify benefits financially wherever possible and proportionate to do so.

The benefits of RDS very much focus on the assumed high level of opportunity cost from the status quo regarding data linkage, with a belief that Scotland is missing out on research opportunities: investment that could be secured in Scotland is currently going elsewhere e.g. a major (£58m) research programme on lung disease went to England.

If RDS were to be established, the investment in service improvements, digital development and specific communications would allow more projects to be progressed more efficiently leading to an increase in the economic value that research projects bring thus avoiding competitive disadvantage and reducing the opportunity cost. In doing so, there could be considerable value to the Scottish economy.

A key metric of the economic value created by linkage projects has been developed by ADR UK and used in their business cases: they state that on average each project generates between £275k and £345k of economic value (2018 prices). Inflating this range by CPI (1.8% in 2019 and 0.9% in 2020) would mean an updated range of £282k and £354k (FY 20/21 prices).

To identify the economic value added by RDS, a baseline position based on the FY 20/21 status quo (including increased demand due to Covid 19) is compared to the RDS position. This includes a prudent level of growth based on improved knowledge of available databases, greater efficiency and a more streamlined process allowing quicker throughput of projects. The comparison is shown over the first five years of RDS in the following table:

| FY 21/22 | FY 22/23 | FY 23/24 | FY 24/25 | FY 25/26 | Total | |

|---|---|---|---|---|---|---|

| Baseline number of projects issuing fees | 60 | 64 | 68 | 74 | 81 | 346 |

| Baseline projects ending (SG/ADR) | 5 | 6 | 6 | 6 | 7 | 30 |

| Baseline total projects | 65 | 69 | 74 | 80 | 88 | 377 |

| Baseline EV lower range | £18.5m | £19.5m | £20.9m | £22.7m | £32.6m | £104m |

| Baseline EV upper range | £23.2m | £24.5m | £26.3m | £28.5m | £40.9m | £134m |

| NPV EV lower range | £96m | |||||

| NPV EV upper range | £120m | |||||

| Assumed reduction - ave proj duration | 20% | |||||

| RDS number of projects issuing fees | 60 | 84 | 90 | 97 | 106 | 437 |

| RDS baseline projects ending (SG/ADR) | 5 | 7 | 8 | 9 | 9 | 38 |

| RDS total projects | 65 | 91 | 98 | 106 | 115 | 476 |

| RDS EV lower range | £18.5m | £25.8m | £27.7m | £29.9m | £32.6m | £134m |

| RDS EV upper range | £23.2m | £32.3m | £34.7m | £37.6m | £40.1m | £169m |

| NPV EV lower range | £120m | |||||

| NPV EV upper range | £151m | |||||

| Difference EV lower range | £0m | £6.7m | £7.2m | £7.2m | £7.9m | £28m |

| Difference EV upper range | £0m | £8.4m | £9.0m | £9.0m | £9.9m | £35m |

| Difference NPV lower | £25m | |||||

| Difference NPV upper | £31m |

This analysis shows that during its first five years of operations, RDS is expected to add economic value of between £134m to £169m (£120m to £151m NPV).

Compared to the status quo, this is an increase of £28m to £35m (£25m to £31m NPV). This equates to between £5.0m and £6.2m of economic value each year. It should be noted that year one is assumed to be a transition year with no difference to the baseline.

- 4. Non-quantifiable benefits (non-QB). These are the qualitative benefits, which are of value to the public sector but cannot be quantified.

For RDS, these include:

- Increased public trust in handling of personal data, and reductions in risk of data being misused;

- Potential for further quantifiable benefits from the streamlining of existing data collections, for example household surveys can be shorter (or collect different information) through linkage to administrative data;

- This opens new possibilities for value adding data services, for example enabling a digital clinical trials service, which helps organisations understand their effectiveness.

Option Appraisal Criteria: Critical Success Factors

To achieve the anticipated benefits from RDS, there are several critical success factors (CSFs), which RDS will have to meet, and these are shown in the following table:

Table 3: RDS critical success factors

Critical Success Factors - Service

Rationale

This will ensure consistency in the level and quality of data access and a linkage service with smoother research user journeys. The timeliness of service delivery. The extent to which RDS will be the sole focus of the organisation.

Critical Success Factors - Safety & security

Rationale

Compliance with legal, IG and ICT requirements. Does the option promote a continued focus on the specialist processes and systems of IG, information assurance and cyber security that underpin the research data holding of RDS?

Critical Success Factors - Public trust & transparency

Rationale

A key element of delivering RDS is ensuring trust and public acceptability. People should trust their data is used appropriately. How people's data is processed will be clear and readily understandable by users and providers of services as well as the public at large.

Critical Success Factors - Sustainability

Rationale

This aims to address the need to ensure that RDS data access and linkage model is a sustainable business model operationally and financially.

Critical Success Factors - Cost effectiveness

Rationale

RDS should maximise Value for Money (VfM). VfM should also be considered when making decisions, and allocating roles, responsibilities and resources amongst service delivery partners.

Critical Success Factors - Accountability

Rationale

RDS needs to be held to account through external scrutiny and audit adopting a strategic, proportionate and risk-based approach. Good governance is also an important consideration.

These criteria have been used as the basis of assessing the short list of potential options for RDS. The methodology for the options appraisal has included:

- Weighting the relative importance of each of the attributes listed in Table 3

- Scoring each of the short-listed options on the basis of its ability to deliver the CSF attributes on a scale of 0 (worst score) to 10 (best score)

- Deriving a weighted benefits score for each option (i.e. score x weighting)

Based on this methodology, scoring of the options was undertaken independently by two senior members of the RDS project team with a subsequent meeting held to justify and moderate scores. An average of the scores was then input into an options appraisal tool that had been developed for the purpose. The options appraisal assessed how well each option would support RDS in achieving its CSFs, which principally focus on the benefits that RDS would bring to Scotland, the public sector and the Scottish research community.

The scores for each of the RDS critical success factors and justification for the scores are shown in the next few pages followed by a summary of all the scores.

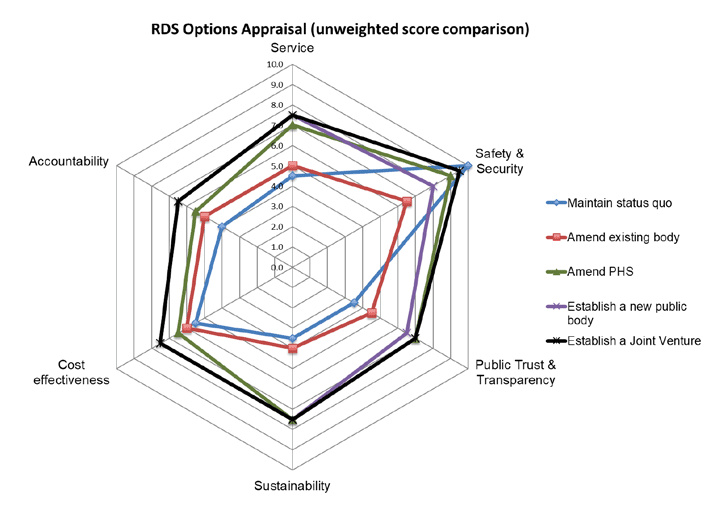

Criteria 1: Service

Consideration of the likely service provision from the different options included an assessment of whether there would be consistency in the level of service, the quality of service, a clear user journey, equality of health and non-health data, whether data would be accessed in a timely manner, and whether the option would enable process improvements.

Relative to the other options, option 1, the SQ, scored less well across all the questions. This was because of its greater focus on health data, an unclear user journey, and the complexity of the current arrangements, based on Memoranda of Understanding. Option 2 (EPB) and option 3 (PHS) scored only slightly higher than option 1 (SQ) with justification based on their greater focus on health data, RDS having to adhere to the existing organisations' operational processes, function and have a lower level of autonomy. Option 4 (NPB) and option 5 (JV) scored well due to having a single focus on RDS, offering a 'blank canvas' that could be used to develop bespoke arrangements specific to RDS's service requirements, and being able to adopt a more balanced approach to health and non-health data.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 4.0 |

| Option 2: Amend existing public body (EPB) | 4.9 |

| Option 3: Add to Public Health Scotland (PHS) | 5.3 |

| Option 4: New public body (NPB) | 7.4 |

| Option 5: Public sector JV (JV) | 7.5 |

Criteria 2: Safety & security

This criterion assessed the extent of the options' legal compliance (including 1978 Act, state aid and data protection), compliance with IG requirements, and compliance with ICT requirements.

The SQ is already compliant with the 1978 Act and data protection so had a maximum score; however, the SQ was considered to have neither efficient processes, nor to meet IG or ICT requirements optimally and, consequently, received a lower overall score. Placing RDS in an existing body had mixed scores depending on whether it was assumed the body had current obligations under the legislation.

The fact that these organisations would not have a sole focus on RDS, again, prevented them scoring higher. Although legal, IG and ICT compliance would not happen immediately, the NPB and JV options scored well as it was considered that they would achieve compliance quickly, particularly as this would be a priority in organisations with a sole focus on RDS.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 6.9 |

| Option 2: Amend existing public body (EPB) | 6.1 |

| Option 3: Add to Public Health Scotland (PHS) | 7.1 |

| Option 4: New public body (NPB) | 7.9 |

| Option 5: Public sector JV (JV) | 8.2 |

Criteria 3: Public trust & transparency

This critical success factor related to assessment of the public trust and transparency relating to the different options. The appraisal assessed the options' ability to earn and retain the trust of stakeholders, scored how well they would enable RDS to build itself as a brand, and how well they would promote a culture of transparency and openness within RDS.

The SQ had a relatively low score due to its complexity and the feeling that stakeholders do not have complete trust because few know the full extent of the infrastructure and the intricacies of the current arrangements; and that the SILC brand was undeveloped. Scoring higher than the SQ, the EPB and PHS options scored similarly in questions relating to potential conflict between the RDS brand and the host organisation's brand; however, there were also some differences with the PHS option scoring better for stakeholder trust and IG.

The NPB did not score as well as PHS on trust at it would take time to build trust in a new organisation. The JV scored better in trust, as the partners would already have existing stakeholder trust on which to build. The NPB and JV options, again, scored well because of their single focus on RDS.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 3.5 |

| Option 2: Amend existing public body (EPB) | 4.8 |

| Option 3: Add to Public Health Scotland (PHS) | 6.0 |

| Option 4: New public body (NPB) | 7.3 |

| Option 5: Public sector JV (JV) | 7.4 |

Criteria 4: Sustainability

This part of the options appraisal assessed the potential sustainability of RDS (financially and operationally). The SQ scored less well due to the current deficit funding position in SILC, which is likely to worsen over time as grant income reduces. Although the SQ is closely tied to stakeholders, there is not a single central budget for SILC and there is uncertainty over the actual funding situation, which is complex and reliant on grant funding. The cost structures of the EPB and PHS options mean that, as RDS would not be the sole focus, although deficits could be absorbed, surpluses could be transferred elsewhere within the organisations. The NPB and JV options scored well as RDS would be their sole focus and this would provide greater control over the RDS budget. Although a deficit would not be absorbed into a parent body, any surplus must be reinvested into developing the service.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 3.6 |

| Option 2: Amend existing public body (EPB) | 4.4 |

| Option 3: Add to Public Health Scotland (PHS) | 6.1 |

| Option 4: New public body (NPB) | 7.6 |

| Option 5: Public sector JV (JV) | 7.6 |

Criteria 5: Cost effectiveness

This critical success factor related to consideration of VfM when making decisions and allocating roles, responsibilities and resources. The lower SQ score was based on the complexity and uncertainty of the current SILC budget, which projects a deficit position. The EPB and PHS options scored only slightly higher as, although these options would allow soft budgeting, there was the possibility of resources being transferred to higher priority areas within the parent bodies. The NPB and JV options scored slightly higher because, despite hard budgets, RDS would be the sole focus.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 5.5 |

| Option 2: Amend existing public body (EPB) | 6.0 |

| Option 3: Add to Public Health Scotland (PHS) | 6.5 |

| Option 4: New public body (NPB) | 7.8 |

| Option 5: Public sector JV (JV) | 7.8 |

Criteria 6: Accountability

This criterion related to accountability, specifically external scrutiny, the support of good governance, and the inclusion of relevant stakeholders in that governance.

The SQ does not score well as there is not a great deal of scrutiny evident at present: stakeholders are not included in governance satisfactorily and there are insufficient data controllers on the SILC senior management board. Improvement in this area of data linkage is a fundamental driver for RDS.

Whilst EPB and PHS would provide increased scrutiny, RDS would be controlled by the parent body and would be subject to its governance, which may have more of a health focus, and may see some stakeholders excluded. Whilst NPB and JV would have a sole focus on RDS, the JV scores higher due to its inclusive nature and the fact that relevant stakeholders are coming together as equal partners.

| Option | Unweighted score (out of 10) |

|---|---|

| Option 1: Status quo (SQ) | 4.2 |

| Option 2: Amend existing public body (EPB) | 5.0 |

| Option 3: Add to Public Health Scotland (PHS) | 5.2 |

| Option 4: New public body (NPB) | 6.8 |

| Option 5: Public sector JV (JV) | 7.3 |

Mandatory considerations

In addition to the above criteria, there are two mandatory stop/go considerations for the RDS service delivery option: whether the options will allow RDS to become a legal entity and give it the ability to contract in its own right: Only the NPB and JV options enable RDS to perform these functions.

The EPB and PHS options would not allow RDS to exist as a legal entity in its own right, and would not allow it to enter into its own contractual arrangements: consequently, these options should be discounted. Similarly, the status quo could not legally be a stand-alone entity and in the current arrangements, RDS cannot contract in its own right. Consequently, options 1, 2 & 3 are not credible and should be discounted.

A summary of the weighted scores from the options appraisal and the mandatory questions is shown in the following table.

| Critical Success Factors | Weight | Option 1 | Option 2 | Option 3 | Option 4 | Option 5 |

|---|---|---|---|---|---|---|

| Status quo (SQ) | Amend existing public body (EPB) | Add to Public Health Scotland (PHS) | New public body (NPB) | Public sector JV (JV) | ||

| Service | 30% | 4.0 | 4.9 | 5.3 | 7.4 | 7.5 |

| Safety & security | 25% | 6.9 | 6.1 | 7.1 | 7.9 | 8.2 |

| Public trust & transparency | 20% | 3.5 | 4.8 | 6.0 | 7.3 | 7.4 |

| Sustainability | 10% | 3.6 | 4.4 | 6.1 | 7.6 | 7.6 |

| Cost effectiveness | 5% | 5.5 | 6.0 | 6.5 | 7.8 | 7.8 |

| Accountability | 10% | 4.2 | 5.0 | 5.2 | 6.8 | 7.3 |

| Weighted score /10 | 100% | 4.7 | 5.2 | 6.0 | 7.5 | 7.7 |

| Rank | - | 5 | 4 | 3 | 2 | 1 |

| Legal stand-alone entity? | - | No | No | No | Yes | Yes |

| Contract in own right? | - | No | No | No | Yes | Yes |

| Final position | - | N/A | N/A | N/A | 2 | 1 |

Therefore the decision as to which option should be the preferred option is between NPB and JV. These options have similar scores but one difference is in the legal structure of these options: a new public body would have its main control resting with Scottish Ministers whereas the JV would not have this restriction and all relevant stakeholders could be included in the governance.

It is because of this distinction, and a marginally higher score, quicker implementation and slightly lower cost, that Option 5, Establish a Joint Venture company remains recommended as the preferred option for RDS. Overall, on strategic fit, legal advice and outline delivery terms, this is the preferred option.

The relative scores of the different options for RDS are shown in the following diagram. It should be noted that the diagram shows un-weighted scores.

Under the preferred option, a joint venture can take on a number of different legal forms as described in the following table:

Table 11: Potential structures for RDS

Structure - Company Limited by Shares

Remarks

This option would not allow RDS to achieve charitable status and so would not be seen as a viable option. An example of a public sector company limited by shares is SFT, which has 100% of its shares owned by Scottish Ministers.

Structure - Company Limited by Guarantee (CLG)

Remarks

Different stakeholders would hold "membership", with liability limited to a nominal amount (often £1 or £5). This model is suited to charitable status or CIC status and is a viable option for RDS. A public sector example is the James Hutton Institute (which also has charitable status).

Structure - Scottish Charitable Incorporated Organisation (SCIO)

Remarks

The organisation must at all times be a charity. This may be a viable option instead of a CLG if charitable status is required. An example of a SCIO is LAR Housing.

Structure - Limited Liability Partnership

Remarks

This option would not allow RDS to achieve charitable status and so is not a viable option.

Structure - Community Interest Company (CIC)

Remarks

When a CIC is formed, a specific "community of interest" must be defined (e.g. community public health researchers) with the CIC's assets and surpluses locked in. There is CIC regulator. CIC status can be given to a CLS or a CLG.

The two structures that are most suitable for RDS are CLG and SCIO. Legal advice sought by the RDS project team recommended that RDS should be established as a CLG.

Risk Analysis

There are some key risks relating to the socio-economic case as follows:

- A full economic cost benefit appraisal has not been conducted on all the options due to the degree of uncertainty associated with delivery. Rather, the approach taken identifies the likely key attributes and strengths of each option and potential constraints/weaknesses as per the success criteria

- The discussion focuses on benefits and costs relative to the counterfactual – this is the Do Nothing option

- The Office for National Statistics (ONS) may classify RDS as a public body which would have the potential to limit how RDS operates.

Conclusion

The socio-economic case lays out the options available for establishing a central administration for accessing public sector data. The option of establishing a Joint Venture is the preferred approach with the joint venture having charitable status as a CLG.

Contact

Email: researchdata@gov.scot