Investing in Scotland's Future: resource spending review framework

This framework document launches the Scottish Government's resource spending review process. It sets the scene for the development of multi-year resource spending plans and opens our public consultation.

2. The Challenge

This chapter explains the fiscal and economic context for the Resource Spending Review. It sets out the funding outlook, which is considered in more depth in the Medium-Term Financial Strategy (MTFS). It models three spending scenarios and outlines the immediate and longer-term pressures on public spending which we need to consider when developing our spending plans to ensure that we meet the needs of our changing population and build resilience for the future. Finally, it compares the funding and spending scenarios to assess the scale of the challenge and the opportunities over the Resource Spending Review period.

2.1 Funding

The MTFS sets out the funding projections for the Scottish Government for the Resource Spending Review period, to 2026-27. The funding projections are built on three main components:

- UK Government spending decisions: through the Barnett formula, the change in the Scottish Government’s Block Grant each year is determined by the change in the UK Government’s spending on areas devolved to the Scottish Parliament.

- Relative growth in Scottish Government and UK Government devolved tax revenues: under the Fiscal Framework, if Scottish devolved tax revenue per person grows relatively faster than in the rest of the UK (rUK), the Scottish Budget is better off and vice versa. This means that Scotland’s budget is influenced not only by tax policy and economic performance in Scotland, but also by tax policy and economic performance in the rest of the UK.

- Relative growth in Scottish and UK social security expenditure: under the Fiscal Framework, if Scottish devolved social security expenditure grows relatively faster than in the rUK, the Scottish Budget is worse off. If UK expenditure grows relatively faster, additional funds are available within the Scottish Budget. Again, this means that Scotland’s budget is influenced not only by policy changes within Scotland, but also what happens in the rest of the UK.

The funding projection sets out a central scenario, based on UK Spending Review announcements to 2023-24 for the block grant, and Office for Budget Responsibility (OBR) forecasts for growth in government spending beyond that. It reflects Scottish Fiscal Commission (SFC) tax revenue forecasts and the OBR’s forecasts for block grant adjustments. Upside and downside scenarios have been modelled to illustrate the potential impact of UK spending decisions (with greater uncertainty after the UK spending review period), and the impact of Scottish tax performance.

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Central scenario | |||||

| Resource funding* | 39.2 | 39.6 | 40.5 | 42.1 | 43.6 |

| Growth compared to 2022-23 budget bill | 0.0 | 0.4 | 1.2 | 2.9 | 4.3 |

| Upside | |||||

| Resource funding* | 39.7 | 40.5 | 42.0 | 44.5 | 47.0 |

| Growth compared to 2022-23 budget bill | 0.5 | 1.3 | 2.7 | 5.3 | 7.8 |

| Downside | |||||

| Resource funding* | 38.9 | 39.0 | 39.5 | 40.3 | 40.8 |

| Growth compared to 2022-23 budget bill | -0.3 | -0.3 | 0.2 | 1.1 | 1.6 |

*Excludes non-domestic rates distributable amount

2.2 Spending

As context for the Resource Spending Review process, it is helpful to understand the existing landscape of public spending in Scotland, and the financial commitments and risks we need to manage over the spending review period.

2.2.1 How has public spending in Scotland evolved?

Scotland’s public finances have undergone a number of radical transformations in the past decade. Today, we have increased powers and responsibility over taxation and public expenditure, with the opportunities that brings to improve the lives of the people of Scotland.

Following the Smith Commission in 2014, a new fiscal framework – which governs the funding arrangements between the Scottish and UK Governments – was agreed.[11] It enabled the transfer of greater tax and social security powers to Scotland while endeavouring to retain the stability of block grant funding.

This has transformed the composition of the Scottish budget. In 2019-20, the Scottish budget allocated £435 million to social security benefits spend. In 2022-23, that has grown to £4.1 billion as responsibility for the disability and carer benefits transferred, and new Scottish benefits, including the Scottish Child Payment, have been introduced.

In parallel, investment in frontline health services has increased to bolster capacity and support the staff who kept the NHS running throughout the pandemic. In 2019-20 we invested £13.9 billion resource in the health portfolio. In 2022-23, that has grown to £17.1 billion, or 44% of the Scottish resource budget. That invests in the recovery of our health and social care system as we emerge from the pandemic and supports vital steps in increasing social care capacity and setting up a National Care Service.

COVID-19 had a wider impact on the Scottish budget. Over the course of 2020-21 and 2021-22 the Scottish Government received £13 billion in additional resource funding (with a further £500 million expected but subject to confirmation), which allowed us to support those most affected by the pandemic with financial and practical support for businesses, families and communities across Scotland. That funding has been withdrawn in the most recent UK Spending Review, reducing our funding by 7% year on year in real terms, while the real life impacts of COVID-19 continue to be felt.

At the time of the 2021-22 Scottish Budget, commentators noted that one-off COVID-19 consequentials had been used to fund recurring activity such as mental health support. This reflects the reality of the pandemic: the virus has not gone away, and its effects will not end on 31 March 2022. Many families and businesses are still grappling with rising prices and an uncertain future and children are still living in poverty. There is a continuing need to invest and rebuild our public services for those who need them most.

2.2.2 The spending outlook in December 2021

The Scottish Budget 2022-23 sets out how we will use the £39.2 billion resource funding available to us in 2022-23. Among other investment:

- The Scottish Child Payment will be doubled to £20 a week from April 2022, and extended to under 16s by the end of 2022 to lift 44,000 children out of poverty.

- £10 million will be invested in holiday childcare for low income families and £3 million in early phasing of wraparound childcare to deliver our Covid Recovery Strategy commitment and contribute to tackling child poverty.

- The Scottish Budget 2022-23 includes £110 million to extend free bus travel to under 22’s, £303 million to support bus services, and £150 million to support active travel.

- It provides £6 million for the Climate Justice Fund, as part of our commitment to help the countries most effected by climate change, yet least responsible, and the first £20 million of the 10-year, £500 million Just Transition Fund.

- Business rates measures will invest £726 million to help businesses get back on their feet after the pandemic and £50 million in targeted employment support will help young people who face long-term scarring effects from the pandemic through our Young Person’s Guarantee

The Resource Spending Review will build on this foundation, by focusing public spending on delivering effective services within sustainable financing. The review will underpin how we reform public services to meet the needs of a society altered by the experiences of the pandemic while continuing to face the global challenge of the climate emergency.

2.2.3 Spending scenarios

We have a duty to ensure that our policies and the services we deliver are financially sustainable so we can meet the needs of future generations as well as our own.

While often changes in the needs of service users emerge over a longer time period, sometimes they shift suddenly – as we saw during the pandemic. We have explored the primary drivers of public spending over the spending review period in this section, and modelled high, low and mid spending trajectories to illustrate the pressures and variables we must consider in developing sustainable spending plans.

Demographic change

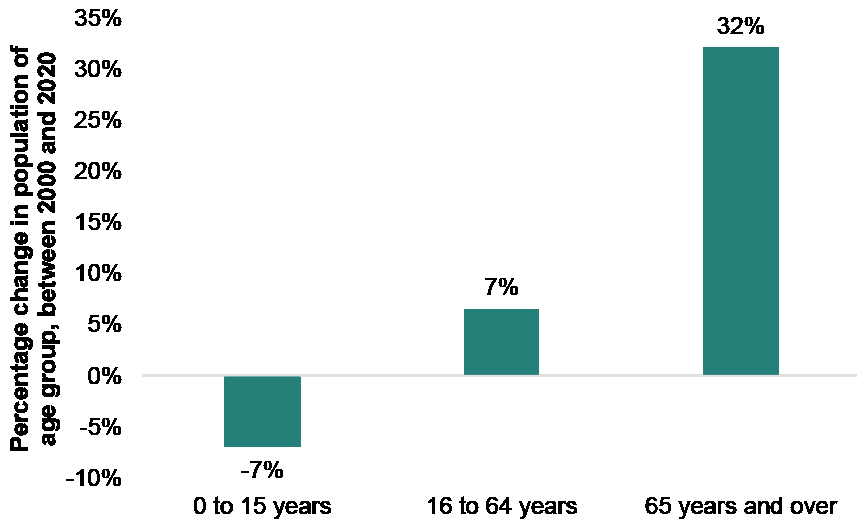

The Scottish population is expected to fall by around 19,000 over the next 6 years, between 2021 and 2027, and the working age population aged 16 to 64 is expected to decline by 60,000 over the same period according to forecasts from the SFC.[12]

This affects both the funding available and the demands on public services. A decline in the working age population slows economic growth and curbs a government’s ability to raise taxes. In Scotland, this effect can be magnified by the Fiscal Framework mechanism which measures the relative performance of Scottish and rUK tax revenues at a time when the total UK working age population is expected to increase.[13]

More pertinently for the Resource Spending Review, the population aged over 65 is expected to grow by 119,000 over the next five years. This is welcome progress, as people in Scotland will contribute in many ways over their longer lifetime. The change entails a shift in patterns of economic participation and in the need for public services across the population. Poor health and complex care needs are more present in an older population which leads to an increased need for health and social care and for financial support through the social security system.

The Feeley Report on Adult Social Care[14] has estimated that approximately 36,000 people in Scotland would benefit from but do not currently access social care support, and the cost of that unmet need is estimated at £436 million.

The report also emphasised the need for continued investment in social care, and referred to the Health and Social Care Medium Term Financial Framework (MTFF) published in 2018[15]. The MTFF projected that, if the system does not adapt or change, social care expenditure could be expected to grow by 4% per annum. This reflected inflationary and demographic effects, which are intensified in a service which supports the very elderly. This projection pre-dates the pandemic, which we know has exacerbated pressures on social care, so the underlying assumptions do need to be revisited. However, it illustrates potential growth in social care costs over the spending review period driven by the demographic and workforce pressures we are already witnessing:

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Mid scenario[16] | 4% annual growth | ||||

| Adult social care expenditure | 4.0 | 4.1 | 4.3 | 4.5 | 4.6 |

| Growth compared to 2022-23 (mid scenario) | 0.2 | 0.3 | 0.5 | 0.7 | |

| Low scenario | 3% annual growth | ||||

| Adult social care expenditure | 4.0 | 4.1 | 4.2 | 4.3 | 4.5 |

| Growth compared to 2022-23 (mid scenario) | 0.1 | 0.2 | 0.4 | 0.5 | |

| High scenario | 5% annual growth | ||||

| Adult social care expenditure | 4.1 | 4.3 | 4.5 | 4.7 | 4.9 |

| Growth compared to 2022-23 (mid scenario) | 0.3 | 0.5 | 0.8 | 1.0 | |

Policy interventions are required to maintain the affordability of public services over the medium to long-term, and ensure they continue to meet the needs of the people of Scotland. This requires efficient service delivery, as well as a focus on demand management through self-care, prevention and health improvement. The creation of the National Care Service is part of our response to this challenge. We anticipate that social care delivered through the National Care Service will represent a growing proportion of the Scottish budget over the coming years. However, preventative spend and person-centred delivery of support will reduce demand for other public services, and not least on the NHS. A number of measures are being taken forward now to increase capacity while we work to establish the National Care Service.

Another area affected by demographic change is social security. Social security payments currently represent £4.1 billion of the annual Scottish budget (10%), but are expected to reach £5.5 billion by 2026-27. Over 80% of social security benefits expenditure relates to disability benefits. The state pension and universal credit remain reserved.

Expenditure on social security benefits is determined by the number of people who apply for support, with those considered eligible paid at the rate set in the policy. We must meet this expenditure as it arises. That means that getting benefits policy right at the outset is vital to ensure that people receive the support they need within an affordable system that does not impact the quality of wider public services they may also rely on.

It also means that we cannot set a fixed envelope for social security spend each year. Instead, the SFC forecasts social security spend over a rolling five-year period based on confirmed benefits policy of the Scottish and UK governments, the number of people they expect to receive payments (the caseload) and how much they expect people to receive (payment rates).

A degree of error in forecasts is always expected due to the demand-led nature of benefits. Changes in policy also only enter the forecasts after they have been confirmed. The forecasts are a central estimate in a range of possible outcomes. The SFC has calculated that there was a variation of 3% between forecast and actual spend in 2020-21, over half of which reflected new Scottish Government spending decisions during the pandemic: for example, the Coronavirus Carers Allowance Supplement and the Self-Isolation Support Payment were introduced in 2020-21 as a response to the pandemic and could not have been known when SFC prepared their forecast in 2020.

Forecast error generally increases the further into the future analysts project due to the greater uncertainty as we move away from the current position. As the devolved Scottish benefits system is relatively new, we do not yet have the data to assess forecast errors across the benefits over more than one year. Instead, we have analysed variation between UK benefits payments and OBR forecasts over a number of years and applied it to current SFC forecasts to illustrate the potential range of costs over the Spending Review period.

The forecast error in UK payments over this period was higher than has historically been the case, particularly further out, due to the introduction of Personal Independence Payment, and the increased forecast uncertainty when new benefits data is introduced. However, we consider this an appropriate benchmark given the SFC will also be forecasting benefits spend for new Scottish policy, without historic data. There is considerable uncertainty in 2022-23 as a result of the launch of the new Adult Disability Payment for example.

Modelling does not yet include the forthcoming Scottish replacements for the Attendance Allowance, Carer’s Allowance, Winter Fuel Payment or Industrial Injuries Disablement Benefit, which are currently delivered on our behalf by the Department for Work and Pensions and forecast based on current DWP policy. Typically, we have found that the differing approach taken in Scotland, based on our core principles of dignity, fairness and respect, has resulted in higher benefits expenditure than the block grant funding provides. For this reason, we consider the low scenario to be extremely unlikely, as current forecasts based on DWP policy are likely to underestimate benefits expenditure once Scottish replacements are fully implemented.

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Mid scenario (SFC forecasts) | |||||

| Benefits expenditure | 4.1 | 4.7 | 5.0 | 5.2 | 5.5 |

| Growth compared to 2022-23 Budget Bill | 0.6 | 0.9 | 1.2 | 1.4 | |

| Low scenario (less OBR forecast error) | -6% | -10% | -16% | -19% | -22% |

| Benefits expenditure | 3.8 | 4.2 | 4.2 | 4.3 | 4.3 |

| Growth compared to 2022-23 Budget Bill | -0.3 | 0.1 | 0.1 | 0.2 | 0.2 |

| High scenario (plus OBR forecast error) | 6% | 10% | 16% | 19% | 22% |

| Benefits expenditure | 4.3 | 5.1 | 5.7 | 6.2 | 6.7 |

| Growth compared to 2022-23 Budget Bill | 0.3 | 1.0 | 1.7 | 2.1 | 2.7 |

Demand on the health service

There is a global tendency for health system costs to rise beyond what can be attributed to demographic change and at a greater rate than economic growth, as set out in the 2019 OECD report: ‘Health Spending Projections to 2030: New results based on a revised OECD methodology’[17]. This is because as medical advancements progress, which we should proudly celebrate, interventions also get more costly, last longer and are needed by a greater number of individuals. This means that just as people live longer, they also have more complex needs for a longer period of time.

Changes in demography (an aging population) are predicted to drive approximately a quarter of growth in health spend to 2030. The OECD identified three other significant drivers of growth:

- Demand for higher quality and more accessible services

- Rising costs, with productivity gains made more challenging by the labour-intensive nature of health care

- Technological advancement extending the scope of health services and driving demographic change as life expectancy lengthens, but people may require long-term support for chronic or multiple illnesses

The OECD recognised that demand without intervention, and therefore costs, will have an upward trajectory over time. It also recognised that the cost of a health system can be reduced through greater cost control, improved health outcomes, and preventative spend.

Similarly, published in 2018 the Scottish Government’s Health and Social Care Medium Term Financial Framework (MTFF), set out drivers of demand for health and social care services and the intended approach to secure financially balanced and sustainable health and care services. It suggested that if the system does not adapt or change, health expenditure could be expected to grow by around 3.5% per annum.

We know that these pre-existing financial and performance pressures within the health and care system have been exacerbated by the pandemic and, as a result, financial assumptions underpinning previous demand trajectories will need to be revisited, along with approaches to balancing the system. The Resource Spending Review will consider this. In the meantime, the MTFF model illustrates the pressures on health funding over the spending review period.

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Mid scenario | 3.5% growth | ||||

| Health expenditure | 17.1 | 17.7 | 18.3 | 19.0 | 19.6 |

| Growth compared to 2022-23 Budget Bill | 0.6 | 1.2 | 1.9 | 2.5 | |

| Low scenario | 2.5% growth | ||||

| Health expenditure | 17.1 | 17.9 | 18.7 | 19.5 | 20.4 |

| Growth compared to 2022-23 Budget Bill | 0.8 | 1.6 | 2.4 | 3.3 | |

| High scenario | 4.5% growth | ||||

| Health expenditure | 17.1 | 17.9 | 18.7 | 19.5 | 20.4 |

| Growth compared to 2022-23 Budget Bill | 0.8 | 1.6 | 2.4 | 3.3 | |

Public sector workforce

Public sector pay is expected to cost around £21.1 billion in 2022-23, which is over half of the Scottish resource budget. As we all saw and recognised during the pandemic, public sector workers play a vital role in keeping the country going during difficult times, and continued investment in our workforce will be essential as we rebuild and refocus on our long-term priorities.

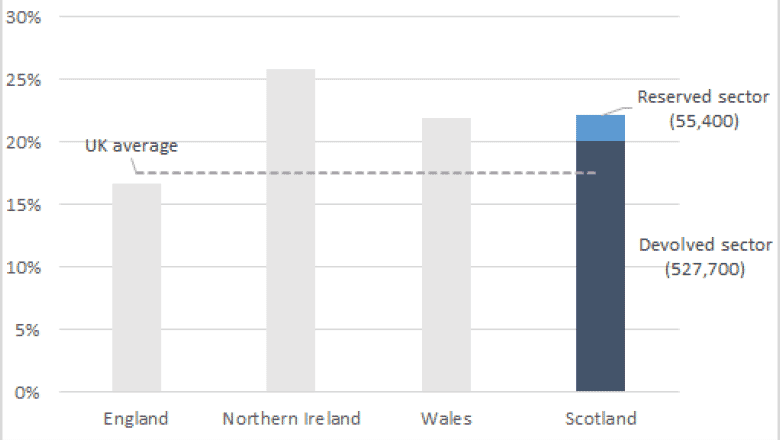

The size and distribution of the workforce in the devolved public sector (which covers those bodies that are the responsibility of the Scottish Government or the Scottish Parliament, such as the local authorities and Scottish health boards, rather than the UK Government, such as HMRC) is therefore a significant driver both of public sector expenditure and the quality of our public services. As of June 2021 583,100 individuals, representing around 22% of all Scottish workers, worked in the public sector. These workers represent roughly 10% of the UK public sector workforce. Around 48% of these workers are in local government and 34% in the NHS, and we are aware that 65% of the public sector workforce are women. Overall, the Scottish public sector is proportionally larger than the UK average of 18%, with the share in England being 17%.

Sources: Public Sector Employment (Office for National Statistics); Public Sector Employment in Scotland (Scottish Government)

Over the last five years the number of public sector devolved workers has increased on average by 1% each year. Over the coming years, we anticipate the public sector will continue to grow to deliver our new social security benefits and invest in our social care workforce through the National Care Service.

To illustrate the potential future costs, based solely on historical trends on growth, we have modelled three scenarios based on assumptions around the pay award and future workforce growth.

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Mid scenario | 2% pay award; 1% workforce growth | ||||

| Public sector pay | 21.1 | 21.7 | 22.3 | 23 | 23.7 |

| Growth compared to 2022-23 | 0.6 | 1.2 | 1.9 | 2.6 | |

| Low scenario | 1% pay award; 0.5% workforce growth | ||||

| Public sector pay | 21.1 | 21.4 | 21.7 | 22 | 22.4 |

| Growth compared to 2022-23 | 0.3 | 0.6 | 0.9 | 1.3 | |

| Upper scenario | 3% pay award; 1.5% workforce growth | ||||

| Public sector pay | 21.1 | 22.0 | 23.0 | 24.0 | 25.0 |

| Growth compared to 2022-23 | 0.9 | 1.9 | 2.9 | 3.9 | |

Inflation

Inflation reached 4.2% in October, the highest rate in almost 10 years. Many economists believe that this high level of inflation is temporary, and reflects short-term supply chain issues and labour shortages as a result of EU Exit and the pandemic.

If high inflation continues, it may put pressure on public finances in a number of ways. We are likely to see increases in the running costs of the Scottish Government and its agencies as suppliers pass on higher costs for goods and services, such as energy or IT. Similarly, we may see the effects through higher demand for public services as the cost of living crisis bites, and an increase in the grant funding required to support our third sector partners in their essential work. In other areas, such as borrowing, rates are directly linked to inflation.

We have modelled three scenarios: inflation at the OBR rate and +/-1%, and applied it to all non-staff costs outside health and social security benefits (which have been modelled separately above).

| £ billion | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Mid scenario | 3.7% | 2.3% | 2.0% | 2.0% | 2.0% |

| All other expenditure | 7.2 | 7.4 | 7.5 | 7.7 | 7.9 |

| Growth compared to 2022-23 Budget Bill | 0.2 | 0.3 | 0.5 | 0.6 | |

| Low scenario | 2.7% | 1.3% | 1.0% | 1.0% | 1.0% |

| All other expenditure | 7.2 | 7.3 | 7.3 | 7.4 | 7.5 |

| Growth compared to 2022-23 Budget Bill | -0.1 | 0.0 | 0.1 | 0.2 | 0.2 |

| High scenario | 4.7% | 3.3% | 3.0% | 3.0% | 3.0% |

| All other expenditure | 7.3 | 7.5 | 7.8 | 8.0 | 8.2 |

| Growth compared to 2022-23 Budget Bill | 0.1 | 0.3 | 0.5 | 0.8 | 1.0 |

2.2.4 What does this mean?

In reality, we know that public spending will mirror the funding forecasts set out in the MTFS, unless there are significant changes to the Fiscal Framework or our tax measures. The UK Spending Review raised the block grant above our pre-pandemic expectations but, compared to 2021-22, it reduced the funding available to Scottish Government for our day-to-day spend every year, despite the continuing effects of the pandemic and the economic impact of the UK’s exit from the EU.

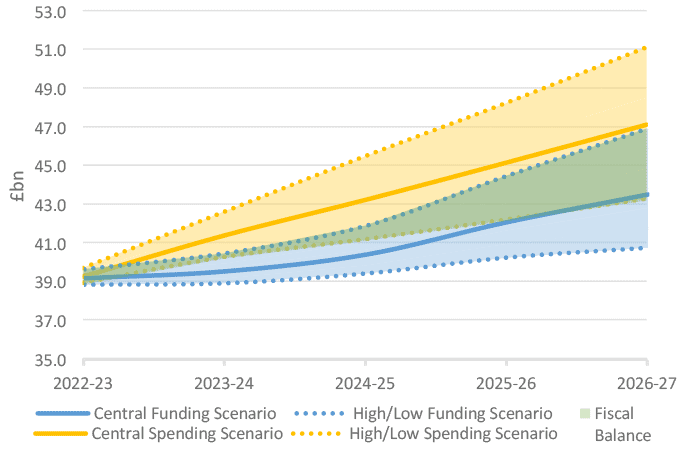

The drivers of public spending identified above illustrate the variable and growing demands on public funding over the spending review period. If we compare our central funding forecast with our mid spending projection, this suggests a growing gap which reaches approximately £3.5 billion in 2026-27. At the extremes, the low funding compared with the high spending trajectory opens an estimated gap of approximately £10.3 billion in 2026-27, while a high funding combined with a low spending trajectory gives a £3.7 billion surplus.

These are not forecasts, and the wide range demonstrates the inherent uncertainties. However, they illustrate the need for a robust Resource Spending Review to help us make informed decisions about how we best use the funding available to meet the evolving needs of the population.

With limited resources, increased investment in the Scottish Government’s priorities will require efficiencies and reductions in spending elsewhere: we need to review long-standing decisions and encourage reform to ensure that our available funding is delivering effectively for the people of Scotland. The Resource Spending Review will, through evidence and consultation, develop four-year spending plans with the aim of managing the financial risks we face and maximising the impact of our available funding.

As a responsible Government, we must rise to the challenges of the future by putting our public finances on a sustainable trajectory. The OECD defines fiscal sustainability as ‘The ability of a government to maintain public finances at a credible and serviceable position over the long term’. Largely this means maintaining sustainable levels of public debt in proportion to the size of a national economy. In the current constitutional settlement, the Scottish Government’s borrowing and reserve powers are tightly constrained. This eliminates some of the risks faced by a sovereign government, such as debt levels becoming unsustainable. It also removes the flexibilities enjoyed by sovereign governments to smooth public funding over a number of years or to borrow to fund recurring expenditure.

The MTFS published alongside this document sets out the fiscal risks we have to manage and our strategy for doing so in the context of limited existing fiscal levers. However, fiscal sustainability is not simply about balancing the budget every year, or even in a multi-year setting. It is about being able to ensure that we use limited resources as efficiently and effectively as possible to make progress towards our priorities and the national outcomes. This is what the Resource Spending Review aims to achieve - ensuring that the medium and longer-term impact of the decisions we make now promote the kind of future we want to build.

Q2. In Chapter 2 we have identified the primary drivers of public spending over the Resource Spending Review period including:

- Changing demographics

- Demand on the health service

- Public sector workforce

- Inflation

We welcome your views on these and any other public spending drivers you think we should consider.

Q3. In Chapter 2 we have identified the growth of the public sector workforce as a key driver of public spending. How can we use policy interventions to maximise the value achieved from the public sector workforce in the effective delivery of public services, while ensuring the sector is an attractive, rewarding place to work?

We welcome your views on this.