International review of approaches to tackling child poverty: Comparative summary report and key learnings for Scotland

A summary of the evidence on historical approaches to tackling child poverty in Finland, Denmark, Slovenia and Croatia, with the key learnings for policy makers in Scotland.

Policies to increase income through social security

The social security system plays an important role in supporting families with children. Social security support for families takes two broad forms. The first is the provision of cash and in-kind benefits to families (either universally or targeted at specific groups) that address the additional costs of raising children. The second is providing an important safety net for those who may be unable to work.

Attitudes towards social security spending, including on family policies, vary across the case study countries and Scotland. In 2022, Eurobarometer surveyed EU residents on attitude to tax and public spending as part of the Fairness, Inequality and Inter-Generational Mobility series.[124] According to this survey:

- A majority of people in Denmark (58%) and Finland (57%) are supportive of keeping spending on family policies at current levels. This perspective is replicated across other areas of social security, such as income support for low-income earners and socially excluded people and unemployment support through benefits and training schemes. As we will see below, this reflects Denmark and Finland’s already significant levels of spending on family policies and generosity of out-of-work benefits.

- In Croatia, a majority support increasing spending on social security across family policies (57%), income support (60%) and unemployment support (51%). This is reflective of the ongoing development of Croatia’s social security system.

- In Slovenia, attitudes towards spending on social security are more mixed. There is a broadly similar level of support for increasing public spending on family policies (42%) as there is for maintaining current levels of spending (37%). However, only 28% of people support increasing unemployment support, similar to the number of people who would support a reduction in spending on unemployment support. Across all the case study countries, greater proportional taxation is the most popular means of paying for any increase in public spending.

In Scotland, according to the 2023 Scottish Social Attitudes Survey, just under half (47%) of people believed taxes and spending should be increase, whereas under four in ten (38%) wanted levels of taxes and spending to be kept the same.[125] Public support for increasing tax and spending has declined since 2019, from 55% to 47% in 2023. During this period, support for reducing taxes and spending has risen from 4% in 2019 to 12% in 2023. The level of support for keeping taxes and spending the same has remained relatively stable since 2019.

Family and children benefits

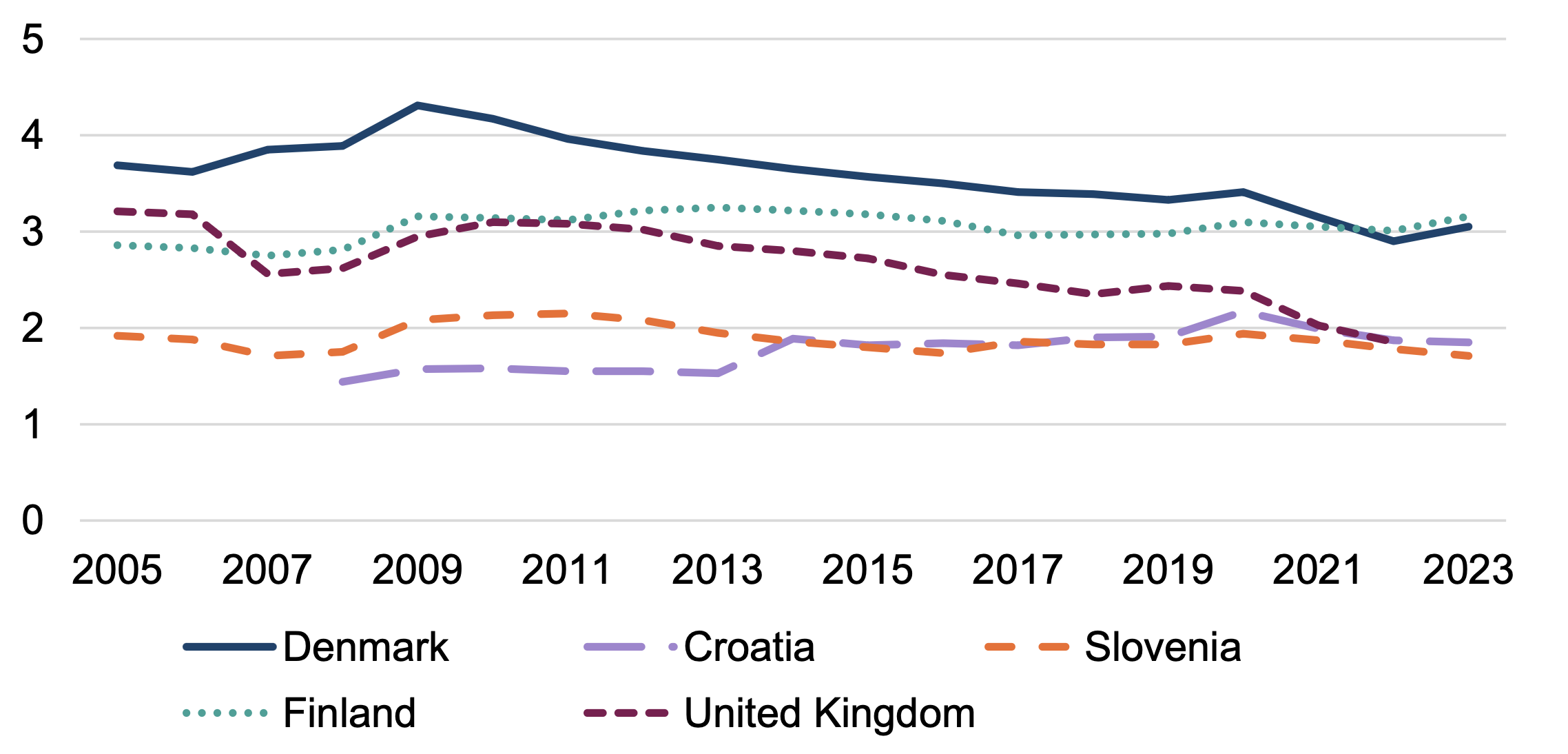

Given their low and stable levels of child poverty, it is perhaps little surprise that Denmark and Finland spend more on family and children benefits than the other case study countries (see Figure 18). Until 2022, Denmark had spent the highest proportion of GDP on family benefits, but the proportion of spend has decreased notably since a peak of 4.3% of GDP in 2009 to 3% of GDP in 2023. This broadly follows a pattern of increasing conditionality and means testing within the Danish social security system (see the case study report for more details). A similar pattern is observable in the UK, with spending falling from 3.1% of GDP in 2010 to just 1.9% in 2022, and reductions in spending especially notable following the implementation of a benefit cap (2013) and two-child limit (2017).

Since 2022, Finland has overtaken Denmark as the highest spender on family benefits amongst the case study countries, spending 3.1% of GDP in 2023. Slovenia’s spending on family benefits has remained broadly consistent between 2005 and 2023 at around 1.7% of GDP, whereas Croatia has seen a modest increase from 1.4% of GDP in 2008 to 1.9% of GDP in 2023. Croatia’s increase in spending has mostly occurred since 2013, as its family-oriented programmes began to develop.

Source: Eurostat, expenditure on social benefits by function, 2005-2023 (spr_exp_func); OECD, Public expenditure on family by type of expenditure (cash and in-kind) in % GDP, 2005-2022

An important part of family policy is the provision of a child benefit for parents, a social security payment that contributes to reductions in poverty amongst families in all countries studied. For example, an International Labour Organisation (ILO) analysis found Slovenia’s child benefit was a significant factor in reducing child poverty rates by at least 40 percentage points in 2013.[126] A child allowance or benefit of some form exists for each of the case study countries.

- Scotland: In the UK, Child Benefit is provided for parents until children turn 16 (or 20 if the child is in education or training). There are two Child Benefit rates: £26.05 for the first child and £17.25 per child for any additional children. Child Benefit is means-tested, and only households where both parents who earn less than £60,000 receive the full amount. If either parent earns over £60,000, the amount is tapered until a £0 payment if either parent earns over £80,000.

In addition to Child Benefit, the Scottish Government provides Five Family Payments for low-income families on certain means-tested benefits, with Universal Credit Child Element the most common passporting benefit. Scottish Child Payment is the most notable of these payments, and from 1 April 2025 is £108.60 every four weeks per child. The other four payments are designed to help towards the costs of being pregnant or looking after young children. Best Start Grant – Pregnancy and Baby Payment provides families with £754.65 on the birth of their first child and £377.35 on the birth of any subsequent children and can be claimed up to six months after the birth. Best Start Grant – Early Learning Payment is a £314.45 payment to help with the costs of early learning when a child is between two and three-and-a-half years old. Best Start Grant – School Age Payment is a £314.45 payment to help with the costs of preparing for primary school. Best Start Foods is a pre-loaded payment card to purchase food that amounts to £21.20 every four weeks during pregnancy, £42.40 every four weeks from birth until a child is one year old and £21.20 every four weeks between the ages of one and three years of age.

- Croatia: Child allowance is a means-tested monthly payment granted until the child turns 15. Child benefit is means-tested and granted to children in households where the average monthly income per member does not exceed €618.02. The child benefit amount in Croatia varies, and it is based on average monthly income and calculated as a proportion of a base amount of €441.11. The benefit can range from €30.90 to €61.80 per child.

- Denmark: Child benefit in Denmark is an age-dependent payment to all families with children below the age of 18 paid quarterly until 15, and monthly for 15–17-year-olds. Parents need to have lived or worked in Denmark for at least six of the last ten years. The benefit amount is tapered depending on the length of time lived or worked in Denmark. Since 2014, those who pay the top rate of tax see their benefit reduced by 2% of the income that exceeds the tax threshold. The benefit amount varied depending upon the age of the child: 0-2 (DKK 5,124), 3-6 (DKK 4,056), 7-14 (DKK 3,192), 15-17 (DKK 3,192)

- Finland: Child benefit is a universal allowance paid for all children under 17 years if their parents or guardians live permanently in Finland. Different rates are paid for each child in the household. For the first child this is EUR 94.88 per month, increasing to EUR 192.69 per month for the fifth and each additional child. An additional EUR 26 per month is paid for children under three years old.

There are three important observations for how child benefits are administered in the case study countries.

1. Firstly, child benefits are mostly means-tested. Only Finland provides a child benefit on a universal basis by design, whereas the other case study countries have a financial eligibility criterion. In Croatia and Slovenia, this is theoretically targeted at lower-income families but, given the wage distribution in Slovenia, the benefit is effectively universal despite means-testing since 2012. In Denmark, child benefit is tapered based upon both residency history and for those parents who pay the top rate of income tax. Scotland’s five family payments are means-tested to low-income households in receipt of certain benefits, whereas UK child benefit is tapered if either parent earns over £60,000 to a £0 payment if either parent earns £80,000 or more.

2. Secondly, most of the case study countries take an approach of increasing the value of child benefit payments for additional children. This is in contrast to the UK child benefit – which provides a reduced payment for any additional children – and the Scottish Government’s Five Family Payments which are flat rates regardless of the number of children. Denmark takes a novel approach in providing more generous payments the younger a child is, and Finland provides a top-up payment for children under three. This age-based policy decision has contributed to the especially low child poverty rates amongst younger children in Denmark and Finland. Scotland’s Best Start Grants similarly acknowledge the additional costs of raising young children.

3. Thirdly, additional allowances can be provided to support at-risk groups. Slovenia operates a large-family allowance for low-income families with three or more children, and in Finland the child benefit rate paid for a fourth or each additional child is around double that paid for a first child. The policy of targeted additional allowances for at-risk groups is provided most extensively in Denmark, where an additional child allowance on top of child benefit is provided for single parents as well as a series of special child allowances for parents with certain vulnerabilities (multiple births, older parents, the death of a parent, unknown paternity and adoption). Similar targeted payments do not currently exist in Scotland.

Social protection schemes

For those who are unable to work, it is important that the social protection schemes in place ensure a good standard of living relative to any previous earnings through paid employment. One of the ways to assess this is through the net replacement rate of out-of-work benefits, which is provided in Tables 10, 11, 12 and 13. Here we explore the replacement rate for different family types of unemployment benefits and social assistance / minimum income benefits across both the short term (3 months’ unemployment) and longer term (one and two years).

Across all family types, the UK has considerably lower out-of-work replacement rates than the case study countries. This is most notable for both single and couple households without children (Tables 11 and 13). Across all case study countries and the UK, the presence of children in a household increases a family’s replacement rate for out-of-work benefits. In Croatia, Denmark and Finland, the generosity of out-of-work benefits decreases the longer someone is unemployed – most notably as they approach two years being unemployed – whereas in Slovenia and the UK the replacement rate is constant regardless of the length of time unemployed.

| 3 months’ unemployment | 12 months’ unemployment | 24 months’ unemployment | |

|---|---|---|---|

| Croatia | 66% | 40% | 41% |

| Denmark | 68% | 61% | 61% |

| Finland | 66% | 66% | 41% |

| Slovenia | 75% | 75% | 75% |

| UK | 34% | 34% | 34% |

Source: OECD, Net replacement rate in unemployment database, 2024

| 3 months’ unemployment | 12 months’ unemployment | 24 months’ unemployment | |

|---|---|---|---|

| Croatia | 70% | 35% | 13% |

| Denmark | 60% | 51% | 51% |

| Finland | 53% | 53% | 22% |

| Slovenia | 44% | 31% | 31% |

| UK | 12% | 12% | 12% |

Source: OECD, Net replacement rate in unemployment database, 2024

| 3 months’ unemployment | 12 months’ unemployment | 24 months’ unemployment | |

|---|---|---|---|

| Croatia | 64% | 36% | 37% |

| Denmark | 84% | 84% | 58% |

| Finland | 60% | 60% | 52% |

| Slovenia | 72% | 72% | 72% |

| UK | 40% | 40% | 40% |

Source: OECD, Net replacement rate in unemployment database, 2024

| 3 months’ unemployment | 12 months’ unemployment | 24 months’ unemployment | |

|---|---|---|---|

| Croatia | 66% | 33% | 17% |

| Denmark | 64% | 64% | 54% |

| Finland | 53% | 53% | 33% |

| Slovenia | 47% | 47% | 47% |

| UK | 18% | 18% | 18% |

Source: OECD, Net replacement rate in unemployment database, 2024

Social Insurance entitlements

One of the most notable features of the case study countries – and other European countries – is the more widespread use of contributory insurance-based social protection, either privately or through social security.[127] These systems are often more generous than non-contributory, means-tested minimum income systems discussed below.

- Scotland: Scotland (and the UK more widely) has seen an erosion of the contributory, insurance-based nature of its social security system. The exception is contributory New Style Jobseeker’s Allowance and New Style Employment and Support Allowance, but these are currently a small part of the UK’s social security system.

The UK Government’s Social Security Advisory Committee has previously noted that the small caseload of these contributory allowances is largely due to investment and policy attention being focused on implementing and reforming the Universal Credit system at the expense of these contributory benefits.[128] However, the UK Government’s 2025 Pathways to Work Green Paper has sought to give more attention to contributory benefits, with a proposal to replace the New Style Jobseeker’s Allowance and New Style Employment and Support Allowance with a new, simple and clear Unemployment Insurance Benefit that will provide a higher rate of time-limited financial support (£138 per week) during periods of unemployment.[129]

- Croatia: Croatia’s social insurance system forms a key pillar of its overall social protection system. It covers old-age, family[130] and disability pensions, unemployment benefits, parental leave and health insurance. Primary health insurance in Croatia is managed by the Croatian Health Insurance Fund and provides coverage for health services as mandated by law. These services include workplace injury and profession-related illness, compensation for loss of pay during sick leave, maternity or paternity leave, and transportation costs related to treatment. The Croatian Pension Insurance Institute manages the implementation of the pension system, which is largely funded by mandatory contributions during working age.[131] Unemployment benefit offers cash support to individuals who are out of work, provided they have been in employment for at least nine months in the past two years.[132]

- Denmark: In Denmark, it is the norm to join a voluntary unemployment insurance scheme which provides a contributory, non-means tested and insurance-based unemployment benefit. Around four in five Danish workers are members of an employment insurance scheme.[133] In order to be eligible for unemployment benefit, a worker has to have worked at least 12 months of employment before accessing unemployment benefit. Unemployment benefit can be claimed for a maximum of two years (incrementally reduced from eight years since the 1990s) and can cover up to 90% of former earnings, up to a ceiling of DKK 20,359 per month in 2024. However, a worker can receive 118.86% for the first three months if the recipient has been a member of the unemployment fund for at least four years and employed for at least 24 months before claiming.[134] Those under 25 receive 50% of their maximum award if they have received unemployment benefit within the last six months.

- Finland: Finland has a comprehensive system of social insurance which provides income security for households facing adverse circumstances through earnings-related benefits provided by private-sector insurance companies. This includes insurance for unemployment, sickness, work-related injury, health and parental leave. Social insurance has a preventative impact on poverty by providing greater levels of income replacement than typically provided by social security during periods of unemployment or sickness. Employee and employer contributions help facilitate greater generosity of support – for example, only 30% of all spending on social services and pensions was from state funds during the ‘golden age of the welfare state’ in the early 1980s and employers contributed 40%.[135]

- Slovenia: Slovenia’s social insurance system has its origins in the former Yugoslavia and has existed since its independence. It is financed by employer and employee contributions. Employees contribute 22.1% of their wages to social insurance contributions, whilst employers contribute 16.1%.[136] This is deducted in addition to personal income taxes and corporate taxes. Included in social insurance contributions is pension and disability insurance, health insurance, injury insurance, unemployment insurance, and parental insurance. Slovenia’s social insurance system is comprehensive and has prevented many households from being in poverty.

Social Assistance and Minimum Income Protection

As well as social insurance, all of the case study countries provide some form of non-contributory, means-tested minimum income scheme. These are often less generous than a contributory insurance-based system, but they provide an important last-resort safety net for people who have insufficient access to other sources of income – including those who are not eligible or have exhausted their entitlement to social insurance benefits.[137]

- Scotland: In Scotland (and the UK more widely), Universal Credit (UC) is the primary social security benefit people can access. UC supports people who are out of work as well as topping up wages of those who are in low-paid employment through the work allowance (£411 a month), although every £1 earned above the work allowance sees UC payments reduce by 55p.[138] Standard allowances are dependent upon age (those under 25 receive less) and household composition (couples receive more), and additional elements are provided for children, disability, childcare costs, caring responsibility and housing costs.[139]

Policy on UC is mostly set by the UK Government, although Universal Credit Scottish Choices gives people living in Scotland the option of being paid UC twice a month rather than monthly and having their Universal Credit housing element being paid directly to their landlords.[140] In addition, the Scottish Government announced in the 2025-26 Budget plans to mitigate the impact of the two-child limit on UC Child Element introduced in 2017, with the specific aim of tackling child poverty amongst larger families.[141]

- Croatia: Croatia offers social assistance to those in need in the form of non-contributory means-tested programmes. These include child allowance, disability benefits, education allowance and guaranteed minimum benefit (GMB). All these programmes have an income threshold and take into account other factors such as household size, number of incomes and the age of beneficiaries, depending on the programme.

- Denmark: Individuals who do not have social insurance (or do not meet the eligibility criteria for unemployment benefits) can access social assistance: a non-contributory, means-tested “benefit of last resort”. Full social assistance is only available to those over 30 years of age, with a lower rate and stricter activation (work or training) requirements placed on younger people.[142] In 2016, twenty-nine additional housing and children payments within the social assistance system were subject to a benefit cap, and a minimum work requirement of 225 hours a year was introduced to avoid being sanctioned.[143] These reforms had a disproportionate impact on larger families, and a temporary child subsidy was introduced in 2019 for those impacted by the benefit cap.[144] This cap was made permanent from 2023. The social assistance system in Denmark had become incredibly complicated, and from July 2025 will be radically reformed with the explicit policy aim of simplification and supporting children.[145] This new social assistance system will comprise of three rates (determined by age, residency and working history); one targeted housing benefit cap for couples; a simplified additional payment for parents and single households; and a generous work allowance to incentivise work.

- Finland: Social assistance provides a backstop to those not eligible for social insurance or whose payments do not meet their basic costs of living. Single parents receive a higher rate, and an additional amount is paid for all children in the household. This plays an important role in reducing child poverty. Local authorities can also provide ‘supplementary or preventative social assistance’ for types of expenses not covered by basic social assistance on a case-by-case basis which can cover, for example, activities for children with special educational needs or housing costs for households at-risk of homelessness.

- Slovenia: Individuals can claim income support if their income is not enough to live on. Income support is means-tested, with the value depending on factors including income, household size, number of dependent children and the net value of an individual’s assets.

Contact

Email: TCPU@gov.scot