Ideas to impact public sector support for research commercialisation: strengths, ambition and progress report

A progress report on public sector support for research commercialisation in Scotland highlighting our strengths and ambitions for the future.

Barries to Address

Whilst there is commercialisation support available for early career researchers and founders – as evidenced by the continuously evolving ecosystem above – there are still a number of gaps we must work to fill to ensure that there is a steady, healthy pipeline of university research suitably supported to commercialise and scale successfully.

In order to support entrepreneurs within our universities to succeed and to embed more of our commercialisation and spinout success in Scotland, we will work together to address the key barriers at each stage of the commercialisation journey outlined below, with a particular focus on funding gaps preventing scaleup.

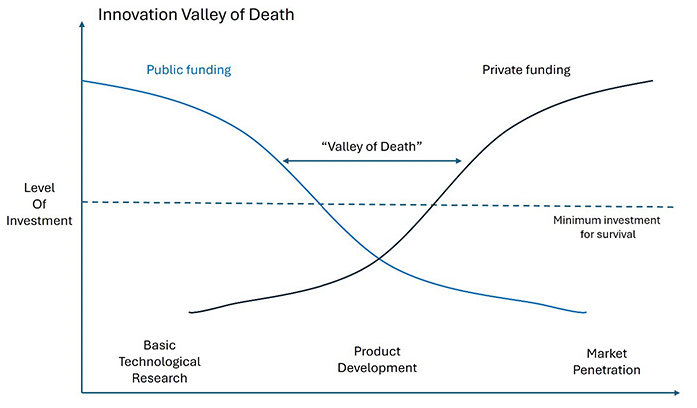

Funding gaps – Proof of Concept and Venture Capital Funding

There is a lack of translational research to turn groundbreaking research into practical solutions with commercial applications. Proof of concept funding, a form of translational funding for early to mid-stage commercialisation activities to de risk new technologies, is lacking in Scotland. Scotland’s entrepreneurial ecosystem is growing, but there remains a significant gap in the availability of seed and pre-seed capital for emerging, high-potential businesses. This funding gap is particularly pronounced for deep-tech and deep-science, where startups often require patient, early-stage investment to scale and commercialise their innovations. Without sufficient funding, many high-impact ventures are at risk of stalling before reaching maturity.

Skills

The re is a skills shortage that comprises of two key groups. For spinout team founders who are academics, there is a lack of entrepreneurial and professional business skills to grow and scale the high value businesses successfully. There is also a lack of available experienced commercial and C-suite talent to support spinout founding teams. Early stage companies, in particular those created from university IP, often struggle to form teams with the right balance of technical expertise, commercial acumen, and effective management practices. Many enterprises lack access to structured training, skills development, tools and supporting commercial talent that could enhance their operational efficiency and long-term sustainability.

There is also a shortage of highly specialised, sector-specific technology transfer officers in Scotland to target and attract investment in priority sectors. Specialists that are present in the system are anchored in the larger institutions where there is more resource and funding available. There is a particular lack of life sciences TTO specialists given the range, specificity and complexity of technologies in this sector.

Infrastructure

We know that infrastructure, including lab space, is a major issue constraining the growth of our most successful spinouts. Despite this there had not been a definitive Scotland-wide review into the issue and, as such, the true scale of the problem remains unknown.

Recent evidence points to a ‘viability gap’ in as the key barrier in the growth. This gap arises from the high cost of capital and construction not being sufficiently offset by the rental values achievable.

As this issue most acutely affects the life sciences industry, that is where we will focus our programme of interventions to ensure our infrastructure enables the growth, scaling and retention of companies that will play the most crucial role in Scotland’s future economy.

Diversity

Attracting, training and retaining top innovative talent depends on sustained investment in postgraduate training and an inclusive, high quality research culture. Addressing variability in researcher experience, short-term funding pressures and international challenges is key to supporting diversity, career stability, progression and responsible research practices.

Des pite a promising talent and relative research performance in Scotland’s universities, a lower number of these female early career researchers go on to commercialise their research in the form of starting a spinout or startup, in comparison to their male counterparts. UK figures demonstrate there is an imbalance of female and ethnic minority founders in the UK as a percentage of total spinout founder numbers. Only 24.6% of companies have at least one female founder, with only 8.57% having all female founding teams.16 Similarly, the most R&D intensive firms (Deep Tech) are similarly dominated by male founders, with just 7.5% of UK Deep Tech companies founded by all-female teams.17

There is also a gap in female entrepreneurs accessing funding at each stage of company growth. Between 2009 and 2019, 68.33% of the capital raised across the seed, early and late venture capital funding stages went to all-male teams, 28.80% to mixed teams and 2.87% to all-female teams. Female teams also raised lower sums of money than their male counterparts at each funding stage, and of the 2020 convertible loan agreements from the British Business Bank, only 1.5% went to all female teams.18

40% of Scottish scaleups have at least one female director,19 and there are five female-founded scaleups with a turnover of about £50 million20 – out of 63 across the whole of the UK, outperforming all other regions apart from the South West.

Those who do succeed in scaling can do so at significant magnitude. For example, female-founded Scottish scaleup company NovaBiotics received the largest InnovateUK grant in the UK in 2022-23, evidencing confidence in capability to scale.21 So the potential is significant.

If we truly want to nurture a system that can harnesses the full capability of all of our innovators and entrepreneurs, whether they are already active in the system or nascent talent with the potential to succeed, then we must target support for those female students and staff looking to commercialise research.

Contact

Email: Spinouts@gov.scot