Fiscal Framework Review: Independent Report

An independent report to consider the Block Grant Adjustment arrangements commissioned by Scottish Government and HM Treasury in June 2022, written by Professor David Bell (University of Stirling), David Eiser (formerly University of Strathclyde) and David Phillips (Institute for Fiscal Studies).

Appendix A: Call for evidence documentation and questions

1. Introduction

1. This note provides background information to help you respond to our survey on the design and operation of the block grant adjustments (BGAs) made to the Scottish Government's funding to reflect recently devolved tax revenues and social security spending.

2. The survey is informing our independent report on the BGAs, commissioned jointly by the Scottish and UK governments, to feed into a wider review of the Scottish Government's fiscal framework.

3. The requirement for an independent report into the BGAs was set out in the 2016 agreement on the fiscal framework between the two governments. The 2016 agreement identifies different approaches to calculating the BGAs, but specifies one approach (known as indexed per capita) that will apply for a 'transitional period'. The transitional period is set to last from the adoption of the 2016 framework until the conclusion of the governments' review of the arrangements. The 2016 agreement specified that the governments' joint review of the arrangements would be informed by an independent report on the BGAs. The agreement states that the identified approach to calculating the BGAs had been agreed for the transitional period and it "does not include or assume the method for adjusting the block grant beyond the transitional period".

4. Throughout this note, we describe the approach to calculating BGAs that has operated during the transitional period as the 'current approach'.

5. This note is structured as follows:

- Section 2 explains Scotland's block grant funding and why BGAs are needed.

- Section 3 sets out the principles that guided the design and calculation of the BGAs as set out in the 2016 fiscal framework.

- Section 4 explains the general approach to calculating the BGAs implied by these principles.

- Section 5 describes the specific approach to calculating the BGAs during the transitional period.

- Section 6 discusses other options, and how they share risks between the Scottish and UK governments.

- Section 7 lists our survey questions.

2. Funding and BGAs

What is the Block Grant?

6. The Block Grant is the money transferred from the UK government to the Scottish Government each year to pay for devolved public services in Scotland, such as health, education, justice, and transport. It is updated each year using the Barnett Formula.

What is the Barnett Formula?

7. The Barnett Formula is used to determine the change in the block grant from one financial year to the next. The size of the change is given by Scotland's population share of the change in funding allocated by HM Treasury to comparable spending programmes, such as health, education, justice and transport, in England. For example, if spending allocated to health in England increases by £1,000m, the Scottish Government would receive an additional £97m since Scotland's population is 9.7% of that in England. The Scottish Government can spend this additional funding as it sees fit. The Barnett Formula does not provide any incentive for the Scottish Government to improve Scotland's economic performance. It receives the same funding change via the Barnett Formula no matter how fast or slow the Scottish economy grows.

What are the block grant adjustments?

8. The Scotland Act 2016 gave the Scottish Government new tax and social security powers. These enabled it, for example, to keep most of the proceeds of income tax raised from Scottish taxpayers. The aim of this was , in line with the Smith Commission recommendations, to better 'deliver prosperity, a healthy economy, jobs, and social justice (pillar two)' and 'strengthen the financial responsibility of the Scottish Parliament (pillar three)..

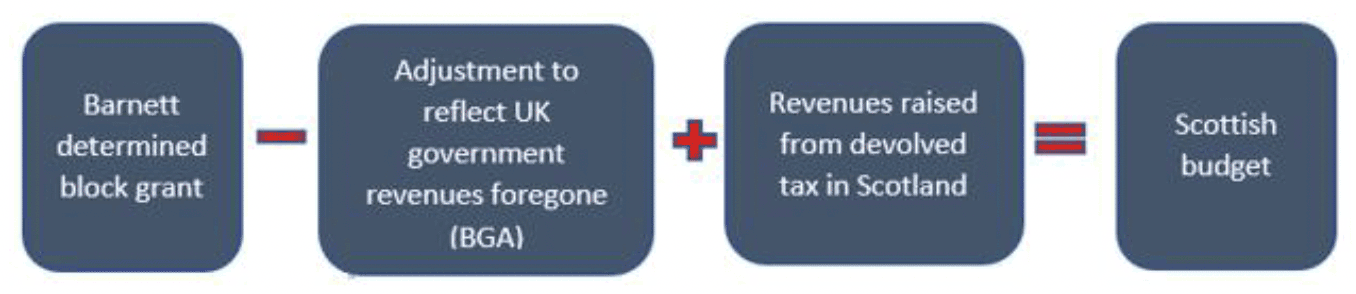

9. Whenever a revenue stream, such as income tax, is transferred from the UK government to the Scottish Government, a deduction needs to be made to the Scottish Government's block grant. This deduction initially reflects the revenues that the UK government has foregone as a result of the transfer of the revenue stream. This deduction is known as a "Block Grant Adjustment (BGA), and is illustrated in the Figure below:

Graphic text below:

Barnett determined block grant minus Adjustment to reflect UK government revenues foregone (BGA) plus Revenues raised from devolved tax in Scotland equals Scottish budget

10. Likewise, when a new social security spending power is transferred from the UK government to the Scottish Government, an addition needs to be made to the Scottish Government's block grant to reflect the transfer of spending responsibility. This addition initially reflects the spending undertaken by the UK government prior to the point of devolution.

11. Separate BGAs are needed for each tax and social security benefit that is devolved. They are required not just in the first year that revenues or social security powers are devolved, but in all subsequent years, to reflect the permanent transfer of revenues/spending from the UK government to the Scottish Government.

12. While it is possible to set the BGAs in the first year of devolution equal to the revenue (or spending) that is devolved, it is not desirable for the BGAs in subsequent years to be set this way. That is because faster or slower growth in revenue (or spending) in Scotland would be offset by faster or slower growth in the BGAs, meaning no net change in the Scottish Government's funding. This would mean it still had no incentive to grow the economy to boost tax revenues and reduce social security spending. Indeed, the Scottish Government would have an incentive to cut tax rates (and increase benefits), knowing that the resulting revenue loss (and spending increase) would be offset by a lower (and a higher) BGA.

13. The key challenge in designing BGAs is therefore how they should be calculated in years following the initial devolution of the revenues or spending that avoids these problems, while being 'fair' to both the Scottish and UK governments.

3. Principles guiding the design of the block grant adjustments

Is there a set of principles that can inform the design of the BGAs?

14. The way that the block grant adjustments are calculated has been informed by a set of principles that were set out by the Smith Commission.

15. The key Smith Commission principles include:

- The UK government should continue to manage the fiscal risks and shocks that affect the whole of the UK ('UK economic shocks').

- The devolved Scottish budget should benefit in full from policy decisions by the Scottish Government that increase revenues or reduce expenditure, and the devolved Scottish budget should bear the full costs of policy decisions that reduce revenues or increase expenditure ('economic responsibility').

- There should be no detriment to the Scottish or UK governments' budget simply as a result of the initial transfer of tax and/or spending powers ('no detriment from the decision to devolve').

- Changes to taxes in the rest of the UK, for which responsibility in Scotland has been devolved, should only affect public spending in the rest of the UK; changes to devolved taxes in Scotland should only affect public spending in Scotland (this has often been referred to as 'taxpayer fairness', although that terminology was not explicitly used by the Smith Commission).

4. Implications for how to calculate the block grant adjustments

What broad approach helps satisfy these principles?

16. These principles suggest an approach involving two components. First, initial adjustments, set at the point of devolution, and indexation mechanisms to update the BGAs in subsequent years.

17. For devolved taxes, the initial deduction is simply the annual revenue raised from the tax by the UK government in Scotland in the year prior to devolution. For social security powers, the initial deduction is the annual amount spent by the UK government at the year prior to devolution.

18. The indexation mechanism is a measure of the subsequent growth in equivalent, 'comparable' UK government revenues or spending in the rest of the UK, for the tax or social security benefit devolved to Scotland.

19. This way of calculating the initial deduction is simple and accords with the Smith Commission's "no detriment" principle because neither the Scottish or UK governments is worse off at the point of devolution as a result of the transfer of fiscal power.

Why is the indexation mechanism calculated on the basis of the growth in comparable UK government revenues or spending?

20. Indexing the BGAs in subsequent years to the growth in comparable UK government revenues or spending in the rest of the UK ( rUK ) helps at least partially meet the other principles identified by the Smith Commission:

- It ensures that the UK government bears the risks of UK-wide fiscal shocks. For example, if a recession causes revenues to fall across the UK, the BGA will fall. Lower Scottish tax revenues are thus offset by a smaller deduction from the block grant.

- It ensures that the Scottish Government benefits from its own policy decisions. If the Scottish Government were to increase income tax rates in Scotland and this increased tax revenues, then Scottish revenues would exceed the BGA (which is determined by what happens to revenues in the rest of the UK) and the Scottish Budget would be 'better off' to the extent of the difference.

- It helps ensure that the Scottish budget does not benefit from increases in UK government spending that is funded by an increase in tax revenues for a tax that has been devolved in Scotland.

21. This third point is less intuitive to understand than the first two. If the UK government increases tax rates for a tax that has been devolved in Scotland, then that tax increase would not apply in Scotland. The income tax BGA would increase, reflecting the increase in rUK revenues. At first glance, this might not appear reasonable insofar as the treatment of the Scottish budget goes. However, it must be remembered that the UK government's additional revenues would be spent by the UK government. If they were spent on 'comparable' public services in England, this would generate a consequential increase in the Scottish Government's block grant, via the Barnett formula. The higher BGA would act to approximately offset this increase. Without this, the Scottish Government would see an increase in its block grant funded by a tax increase in rUK that didn't apply in Scotland. Indexing the BGA to a measure of comparable UK government revenues is therefore important when we recognise that the revenue effect of tax changes by the UK government can 'flow' to Scotland even when the tax changes apply to a tax that is 'devolved' in Scotland.

22. If the UK government spent the additional revenues on 'reserved' matters (like defence, state pensions, universal credit or debt interest), the BGA ensures that taxpayers in Scotland make a broadly similar contribution to that expenditure as taxpayers in rUK, despite the tax increase not applying directly in Scotland.

How can the growth in comparable UK government revenues or spending be measured?

23. There are many ways to measure growth in comparable UK government revenues and spending, and hence to index the growth of the BGA. These include:

- Accounting for differential population growth compared to Scotland, or not;

- Accounting for other differences in demographic or economic trends, or not;

- Accounting for differences in the nature of tax bases or spending distributions.

24. And in relation to each of these, the change in revenues or spending can either be measured in cash or percentage terms.

25. Each of these would at least partially meet the Smith Commission principles, but they would expose the Scottish and UK governments to different risks, and lead to different BGAs and, in turn, different levels of funding for the Scottish Government.

Should the indexation mechanism account for differential population growth in Scotland?

26. One of the big debates when the Scottish Government's fiscal framework was being negotiated in 2015 and 2016, was about how the indexation mechanism should adjust for differences in population growth between Scotland and rUK. Specifically, whether the BGA should be based on a measure of the change in total rUK revenues/spending; or alternatively, a measure of the change in rUK revenues/spending per capita that is then used in conjunction with growth in Scotland's population.

27. On the one hand, given that one could reasonably expect in advance for Scotland's population to grow less quickly than that of the rUK (this has long been the case historically, and is set to continue according to the latest population projections), one could argue that protecting Scotland from the risk of differential population growth is consistent with the 'no detriment' principle. This is particularly true if one believes there is little the Scottish Government can do to affect the rate of Scotland's population growth relative to that of rUK.

28. Population growth is an important determinant of revenue (and spending) growth, and so to index the BGA to changes in total revenues/spending in rUK, without adjusting for slower population growth in Scotland, means that Scottish revenues per capita would need to grow more quickly than those in rUK simply to match the change in the BGA. (On the spending side, the argument is reversed – failure to take account of Scotland's likely slower-growing population would fund faster growth in spending per capita than is being seen in rUK, benefiting the Scottish Government).

29. On the other hand, calculating the BGAs in a way that adjusts for differential population is creates an asymmetry with how the Barnett Formula treats population growth when calculating the underlying block grant. This takes no account of differential population growth. To see why this may concern some people, consider what would happen if revenues in rUK grew only because of population growth. If Scotland's population was unchanged and the BGAs adjusted for differential population growth, the BGA would also be unchanged. However, Scotland would still receive a share of the spending increase funded by the higher aggregate revenues in rUK via the Barnett formula or reserved spending, meaning it has benefited from increases in devolved tax revenues in rUK. This could be considered to be inconsistent with the 'taxpayer fairness' principle.

30. The Smith Commission's principles do not explicitly address whether or not the approach to indexing the BGAs should or should not control for relative population growth. People's views on this depend on exactly how they interpret the Smith Commission principles, and the weight accorded to some principles over others.

5. The approach to calculating the block grant adjustments during the transitional period

What is the Comparable Model and how does it fit in?

31. As well as the IPC method, another approach to indexing the BGAs for tax is referenced in the existing Scottish Government fiscal framework. The other method is known as the Comparable Model.

32. The Comparable Model increases the BGA by Scotland's population and tax-capacity adjusted share of the cash-terms change in revenue from equivalent taxes in rUK. Tax capacity is measured as Scotland's revenues per capita as a share of rUK's revenues per capita prior to devolution. For example, Scotland's revenues per capita for income tax prior to devolution were 79.8% of the level in rUK. Thus, if rUK income tax revenues increased by £1,000m, Scotland's income tax BGA would increase by around £73 million (£1,000m*9.2 %*79.8%). This is consistent with how the Barnett formula treats population (with no adjustment for differential population growth).

33. The main practical difference between the Comparable Model and the IPC method is that the Comparable Model does not take account of relative population growth.

34. However, the Comparable Model, while referenced in the Scottish fiscal framework, is not used in practice to determine the BGAs. This is because the 2016 fiscal framework says:

"For a transitional period covering the next Scottish Parliament, the Governments have agreed that the block grant adjustment for tax should be effected by using the Comparable Model (Scotland's share), whilst achieving the outcome delivered by the Indexed Per Capita (IPC) method for tax and welfare."

35. Of course, if it is the IPC outcome that is delivered, it is the IPC method that is being used.

How are the BGAs for social security payments indexed?

36. For social security benefits the 2016 fiscal framework begins by saying that the approach to be used is to increase the BGAs by Scotland's population share of the cash-terms change in spending on equivalent benefits in rUK. This is the same as the Barnett formula which applies to devolved public service spending.

37. Similar to tax however, the fiscal framework states that for a transitional period up to and including 2020/21, the social security BGAs will for practical purposes be calculated using the IPC method.

Why are these alternative methods mentioned if they are not used?

38. The alternative methods are mentioned in the fiscal framework agreement because of differences in opinion about which methods are more consistent with the Smith Commission principles between the Scottish and UK governments.

39. The Scottish Government favoured the IPC method, in order to protect its budget from the effect of differential population growth on devolved tax revenues.

40. The UK government favoured the Barnett Formula and Comparable Model for the transitional period because using these approaches for devolved public spending and the tax BGAs, respectively, would treat risks associated with differential population growth in a consistent manner on both the spending and revenue sides of the Scottish Government's budget.

41. Both methods were included in the agreement to reflect the fact that while the IPC approach is being used in practice for the transitional period, these differences in opinion have not been resolved.

6. Other approaches and how they share risks

What other risks could the BGAs take account of?

42. In 2016, the main debate around BGAs boiled down to the question of whether or not the BGAs should take account of differential population growth. But there are a number of other fiscal risks that BGAs could be designed to take account of.

Should the BGAs be designed to take account of demographic change?

43. One of these is demographic change after devolution has occurred. Differences in the share of population growth driven by the working-age and pensioner-age populations can matter if spending or revenues per capita for these groups differ. The BGAs could be calculated to protect the Scottish Government's budget from the effects of a more rapidly ageing population on its revenues (because its tax BGAs would be lower to offset this). However, they would also mean the Scottish Government would not benefit from the higher revenue associated if its various policies helped it attract more working-age people to live in Scotland (because its tax BGAs would be higher to offset this).

Should the BGAs be designed to take account of the structure or characteristics of tax bases?

44. Another is the structure of the tax-base at the point of devolution. The IPC and Comparable Model both take account of Scotland's lower tax capacity (revenues per capita) and higher spending per capita at the point of devolution, and do not disadvantage the Scottish budget as a result of its starting point. But there is a slightly separate risk which neither method takes account of. This is the risk associated with having a tax base which differs in structure or characteristics from the equivalent rUK tax base.

45. An example is income tax. Scotland has proportionately fewer high-income taxpayers than rUK. This means that, if tax revenue growth was being driven by high income taxpayers, the income tax BGA would likely grow more quickly than Scottish revenues, even if the growth in income of both high- and low-income taxpayers in Scotland matched that of rUK – because Scotland's smaller proportion of higher-income taxpayers would generate less growth in overall revenues.

46. The BGA can be designed to mitigate this risk (as it is in Wales). However, such methods would also prevent the Scottish Government from benefiting in cases where more of the growth in revenues is being driven by low-to-middle income taxpayers.

47. The BGAs can therefore be designed to account for these (and other) fiscal risks. Protecting the Scottish budget from any one risk always implies that the Scottish budget would not benefit if the risk went in its favour. It also implies that the approach to calculating the BGAs becomes increasingly divergent with the approach to the Barnett formula (because the Barnett formula does not account for these risks).

Can any BGA mechanism fully achieve the taxpayer fairness principle?

48. Neither the IPC nor Comparable Methods fully achieve the UK government's view of the taxpayer fairness principle. The Barnett Formula allocates Scotland a population share of increases in comparable spending by the UK government, whereas the BGA is increased in a way that takes account of Scotland's (generally lower) tax capacity,[12] and in the case of the IPC method, its slower population growth too.

49. This means that if the UK government's tax revenues increase and are used to fund public spending, the Scottish budget would receive a population share of the spending increase, but its BGA would increase by less than a population share of the tax increase. Hence there is scope for the Scottish budget to benefit from an increase in rUK tax revenues for taxes that are devolved. The flipside is that the Scottish budget could be worse off if a UK government were to cut tax rates and reduce spending.

50. If tax BGAs are calculated by indexing them on the basis of a population share of the change in rUK tax revenues (but not a tax-capacity adjusted population share), then the taxpayer fairness principle can be achieved. However, such a method would require Scottish revenue growth per capita to significantly and persistently exceed rUK revenue growth per capita in order for the Scottish budget to avoid being worse off as a result of tax devolution. This could be considered to be inconsistent with the 'no detriment' principle.

Should the BGAs be periodically reset, or include aspects of fiscal insurance?

51. Any BGA method will protect the Scottish budget from certain specific fiscal risks, but leave it exposed to other risks indefinitely. For example, the IPC method protects the Scottish budget from the effect of relatively slower population growth. But if the Scottish tax base declines (e.g. due to structural changes in the economy) persistently over time relative to rUK, there is in theory no limit to the extent to which the tax BGA could grow relative to Scottish revenues. Conversely, there is no limit on the extent to which the Scottish Government could gain if its tax base grew consistently relatively faster than that of rUK.

52. The approach to the design of the BGAs could in principle incorporate some checks to limit the extent to which the Scottish budget could deteriorate as a result of a slower growing tax base. This could occur through establishment of some kind of 'floor', or a periodic 'reset' of the BGA.

53. However, such mechanisms would also mean the Scottish Government would not benefit in full from the higher revenue associated if its various policies helped it increase the rate of economic and underlying tax-base growth (because its tax BGAs would be higher to offset this). This could be considered inconsistent with the 'economic responsibility' principle of the Smith Commission.

7. Survey questions

a. What do you consider to be the strengths and weaknesses of the current approach to calculating block grant adjustments for devolved taxes and social security spending for Scotland?

b. To what extent do you think that the various approaches to calculating the Scottish block grant adjustments, outlined in the background note, are consistent with the Smith Commission's principles? How could the calculation of the BGAs be made more consistent with the Smith Commission principles?

c. To what extent do you think the various approaches to calculating the Scottish block grant adjustments shares risks between the Scottish and UK governments appropriately? To what extent do you think it is important that the allocation of risks implied by the BGA mechanism aligns with the balance of risks held under the Barnett formula?

d. Do you have any other suggestions for how the block grant adjustments should be designed beyond the transition period?

e. Do you have any suggestions for how understanding of block grant adjustments among stakeholders can be improved?

Contact

Email: matthew.elsby@gov.scot