Fiscal Framework Review: Independent Report

An independent report to consider the Block Grant Adjustment arrangements commissioned by Scottish Government and HM Treasury in June 2022, written by Professor David Bell (University of Stirling), David Eiser (formerly University of Strathclyde) and David Phillips (Institute for Fiscal Studies).

4. Other approaches to calculating block grant adjustments

In Chapter 3 we examined the extent to which the BGA methods cited in the Scottish Government's existing Fiscal Framework are consistent with the principles identified in the Smith Commission Agreement. This chapter appraises a number of alternative approaches to calculating the BGAs. These include:

- Using the Barnett Formula to index the BGAs for devolved taxes. This method, also termed the Levels Deduction method, would fully meet the 'taxpayer fairness' principle when changes in rUK revenues lead to changes in funding for the Scottish Government via the Barnett formula. However, it is arguably not consistent with the 'no detriment' principle in the years following devolution – indeed it would almost inevitably make the Scottish budget significantly worse off as a result of tax devolution given Scotland's lower revenues per capita for the two largest devolved taxes covered by the fiscal framework: income tax and stamp duty land tax.

- Approaches that control for differences in demographic change over time. The demographic structure of the population can influence revenues and spending per capita. Some have argued therefore that the approach to calculating the BGAs should take demographic factors into account, in order that the Scottish budget is protected from the effects of demographic change on revenues and spending. This may help better achieve the 'no detriment' principle in a dynamic sense if one believes the Scottish Government has little influence on demographic change, but may be less consistent with the taxpayer fairness principle

- Approaches that control for differences in tax structure at the point of devolution. The distribution of Scottish taxpayers by income differs from that in rUK. These differences in the distribution of the taxbase can mean that underlying economic trends and changes in tax policy have differential effects in Scotland compared to rUK, in ways that can cause 'detriment' to either the Scottish or UK government. Given that the Scottish Government cannot influence its historic tax revenue structure, adjusting for this would arguably be more consistent with the 'no detriment' principle in the years following devolution. However, again, this may be less consistent with the 'taxpayer fairness' principle.

- Approaches not based on growth of equivalent rUK revenues or spending. It is sometimes proposed that BGAs should not be indexed by reference to what is happening to the equivalent revenues or spending in rUK, but to some other index (such as inflation). Whilst such an approach might be simpler to explain and implement, it would not be consistent with the 'taxpayer fairness', 'economic shock' and 'no detriment' principles.

Finally, we also consider the case for incorporating elements of insurance against divergent revenue or spending trends into the BGA approach. This could help better address the 'no detriment' principle, but would be inconsistent with the 'economic responsibility' and 'taxpayer fairness' principles.

4.1 The 'Levels Deduction' approach

The discussion in chapter 3 showed that neither the IPC nor CM methods fully achieve the taxpayer fairness principle. This is because these methods take account of Scotland's differing levels of revenues per capita when indexing the BGAs in response to changes in rUK revenues, whereas when those rUK revenues are spent, Scotland is likely to receive a population-share. The changes in BGAs therefore do not fully offset the changes in funding via the Barnett formula (or in spending on reserved services), meaning Scotland can still gain or lose somewhat from changes to tax policy in rUK for taxes that are devolved in Scotland

This discussion suggests that there is one approach to indexing tax BGAs that would fully satisfy the taxpayer fairness principle: if the change to the tax BGAs are indexed by Scotland's population share of the change in equivalent UK revenues, this achieves symmetry between the BGA and spending elements of the Scottish budget. This would mean that the population-based increments in the Scottish Government's funding via the Barnett formula – when tax revenues in rUK are spent – would be exactly offset by population-based increments in the BGAs. If the additional rUK revenues were spent on reserved services, the offsetting would not be exactly equal but would likely be closer to equal than under the IPC and CM methods given Scotland's share of spending on reserved services is close to its population share, overall. The approach has previously been referred to as the 'Levels Deduction' approach, since the changes to the BGA are based on cash-terms changes in the level of UK government revenues, rather than proportionate changes. It is an equivalent mechanism to the Barnett formula, used to allocate funding for public services, and referenced in the Fiscal Framework in relation to the BGAs for social security benefits.

To illustrate, lets return to the hypothetical example introduced when discussing the taxpayer fairness principle in section 3.2. In that example, UK government income tax revenues increased by £10 billion. It was assumed that this revenue was spent on services that in Scotland are devolved to the Scottish Government, generating a consequential increase in the Scottish budget (assuming Scottish population was equal to 9.14% of rUK's) of £0.914 billion.

Under the Levels Deduction approach to BGA indexation, the Scottish Government's income tax BGA would increase by a population share of the change in UK government revenues. In this example, the BGA would increase by £0.914 billion, since this represents Scotland's population share of the change in rUK revenues.

The £0.914 billion increase in funding under the Barnett formula is therefore exactly offset by the £0.914 billion increase in the BGA. The taxpayer fairness principle has been achieved in full because the change in tax and spending in rUK has not resulted in any change in funding for Scotland. This contrasts with the outcome under the IPC and CM methods illustrated in Table 3.2, above, where Scotland saw an increase in funding as a result of tax changes applying only in rUK, which does not fully satisfy the taxpayer fairness principle.

However, whilst the Levels Deduction approach better achieves the principle of taxpayer fairness, it is less consistent with the other Smith Commission Agreement principles. In particular, use of this approach would very highly likely cause significant detriment to the Scottish budget over time. This is because the lower tax revenues per capita in Scotland relative to rUK for income tax and stamp duty land tax, the two largest taxes devolved under the Fiscal Framework, mean that under the Levels Deduction approach, Scottish revenues would need to grow substantially quicker in percentage terms than those in rUK to keep pace with the BGAs.

To see this, return to the previous example, introduced in section 3.2. The £10 billion increase in rUK revenues was equivalent to an increase of 5%. But if Scotland's BGA is increased by a per capita share of £10 billion, with no adjustment for its lower tax capacity, the resultant increase in BGA from £15 billion to £15.914 billion implies a growth rate in the BGA of 6.1%. Scottish revenues would therefore need to grow by 6.1% to keep pace with the BGA and avoid detriment to the Scottish budget.

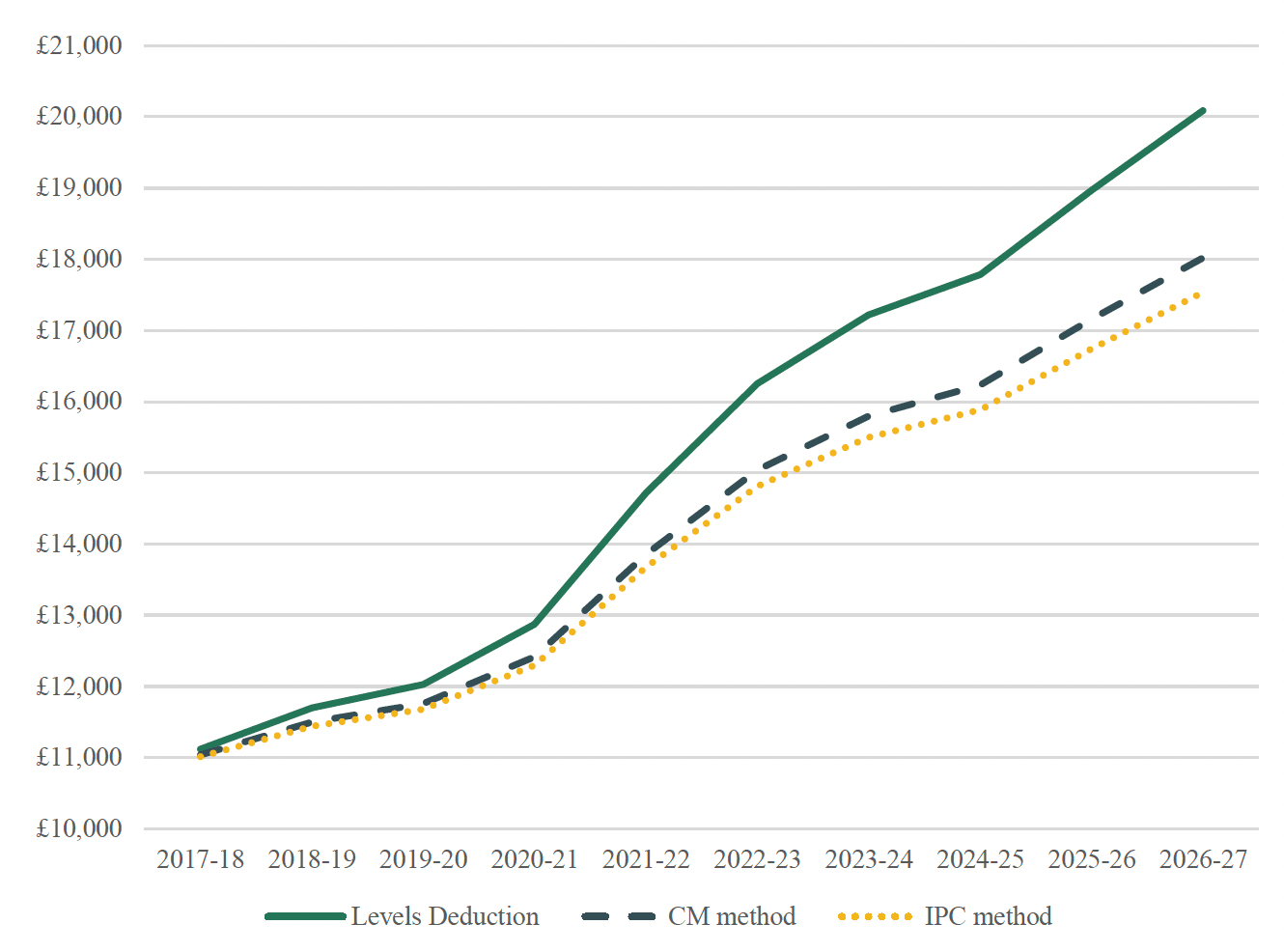

We can also examine how different the BGAs would be in practice under the Levels Deduction method compared to the IPC and CM methods. This is done for income tax in Figure 4.1, which has by far the largest BGA, and combined with a significant difference in taxable capacity, by far the largest cash-terms differences in BGAs between indexation mechanisms (in proportional terms, the effects would be larger for Stamp Duty Land Tax / Land and Buildings Transactions Tax though). The figure shows that relative to the IPC method used in practice, using the Levels Deduction method would have meant the BGA was £0.58 billion higher than it actually was in 2020/21. By the current financial year, this gap would have grown to over £1.4 billion, and by 2026/27, an estimated £2.6 billion. To put this in context, this is roughly double the Police Scotland core funding allocation this year. Relative to the CM method the BGA would be £2.1 billion higher by 2027–28.

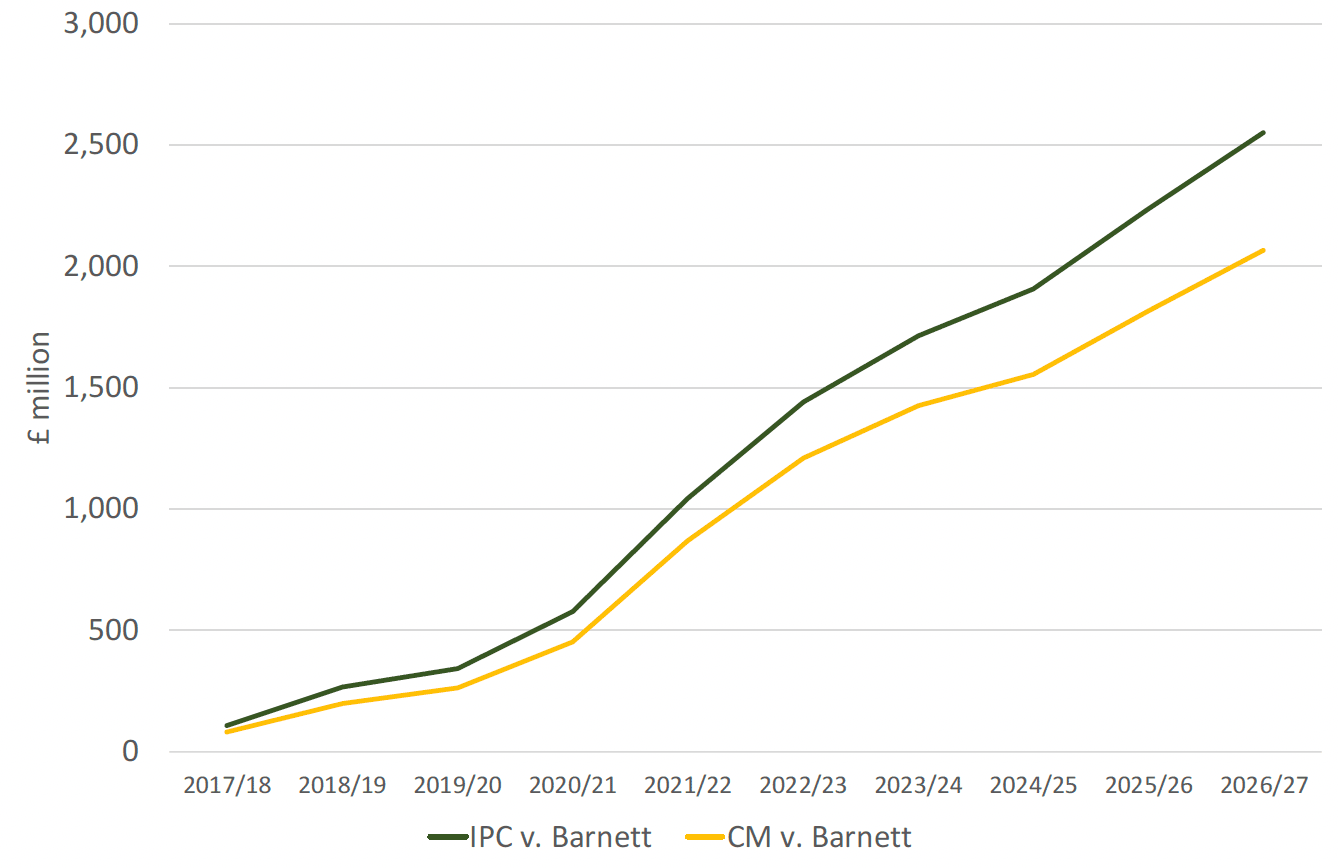

Figure 4.2 shows the same information, but examines more explicitly the difference between the income tax BGA under the levels deduction, or Barnett approach, and the IPC or CM approaches. The gaps here – for example the gap of around £500m in 2020/21 –represents the extent to which tax revenue growth from the rest of the UK is transferred to Scotland under the IPC and CM methods. In other words, the gap is a measure of the extent to which the 'taxpayer fairness' principle, at least according to one interpretation of it, is infringed by the other two methods.

Source: Authors calculations using Block Grant Transparency Data and Fiscal Framework Outturn report data annex.

Source: Authors calculations using Block Grant Transparency Data and Fiscal Framework Outturn report data annex.

If one interprets the no detriment principle as applying beyond the first year of devolution to factors/trends that can confidently be predicted at the time of devolution (which is reasonable given that when defining the 'no detriment' principle, the Smith Commission referred to the need for 'appropriate' indexation mechanisms) the Levels Deduction approach is not consistent with the 'no detriment' principle. This is because, given Scotland's lower tax capacity at the point of devolution, the Scottish budget would be expected to suffer detriment as a result of the decision to devolve income tax and stamp duty land tax, unless Scottish revenues grow more quickly in percentage terms than those in rUK. Indeed, use of the Levels Deduction approach would not just transfer to the Scottish Government the risk of slower or faster growth in revenues post devolution, but slowly over time transfer responsibility for having lower or higher levels of revenues per capita at the point of devolution. This is because successive population-based increments to the BGA would mean that over time the overall level of the BGA would converge to Scotland's population share of rUK revenues, if population growth rates in Scotland and rUK.[8]

The Levels Deduction approach is also less consistent with the principle that the UK government should bear the risk of UK-wide economic shocks than the IPC and CM methods. The Levels Deduction over-insures the Scottish budget against the risk associated with UK-wide shocks. When revenues fall UK-wide, the reduction in the BGA would be larger than the reduction in Scottish revenues, since the former is based on the change in Scotland's population share of rUK revenues which is likely to be greater in revenue terms than the equivalent fall in Scottish revenues in percentage terms. The net effect of a negative UK-wide shock to revenues would therefore be to increase funding for the Scottish Government's budget. Conversely, the net effect of a positive UK-wide shock to revenues would be to reduce funding for the Scottish Government's budget.

On the other hand, the Levels Deduction method is more consistent with the 'economic responsibility' principle than the IPC method. This is for the same reason that the CM method is more consistent: whereas the IPC method fully insulates the Scottish Government's budget for the effects of its policies on relative population, the Levels Deduction method (and CM method) does not do this. Both the Levels Deduction and CM methods do very partially compensate the Scottish Government for population changes induced by its policies though: the population share used for increments to funding is updated when relative population levels change. Whether the effect is bigger for the Levels Deduction method or CM method depends on Scotland's relative levels of revenues and spending per capita. For example, for the main taxes, Scotland's initial revenues per capita (its tax capacity) was lower than that of rUK. This means that increases in the BGA under the CM method, and hence the effect of updating the population share, are likely to be smaller than under the Levels Deduction method. This means less of the induced-population changes will be offset via changes in the BGA for the CM method than the Levels Deduction method: i.e. the CM method will be more consistent with the 'economic responsibility' principle. But for the main devolved social security benefits, where initial spending per capita was higher than in rUK, the Levels Deduction lead to smaller increments in the BGA, and hence is less affected by changes to population shares. In this case, the Levels Deduction method will be more consistent with the 'economic responsibility' principle. It is worth noting that these differences in consistency are likely to be very marginal though.

4.2 Demographically-adjusted approaches

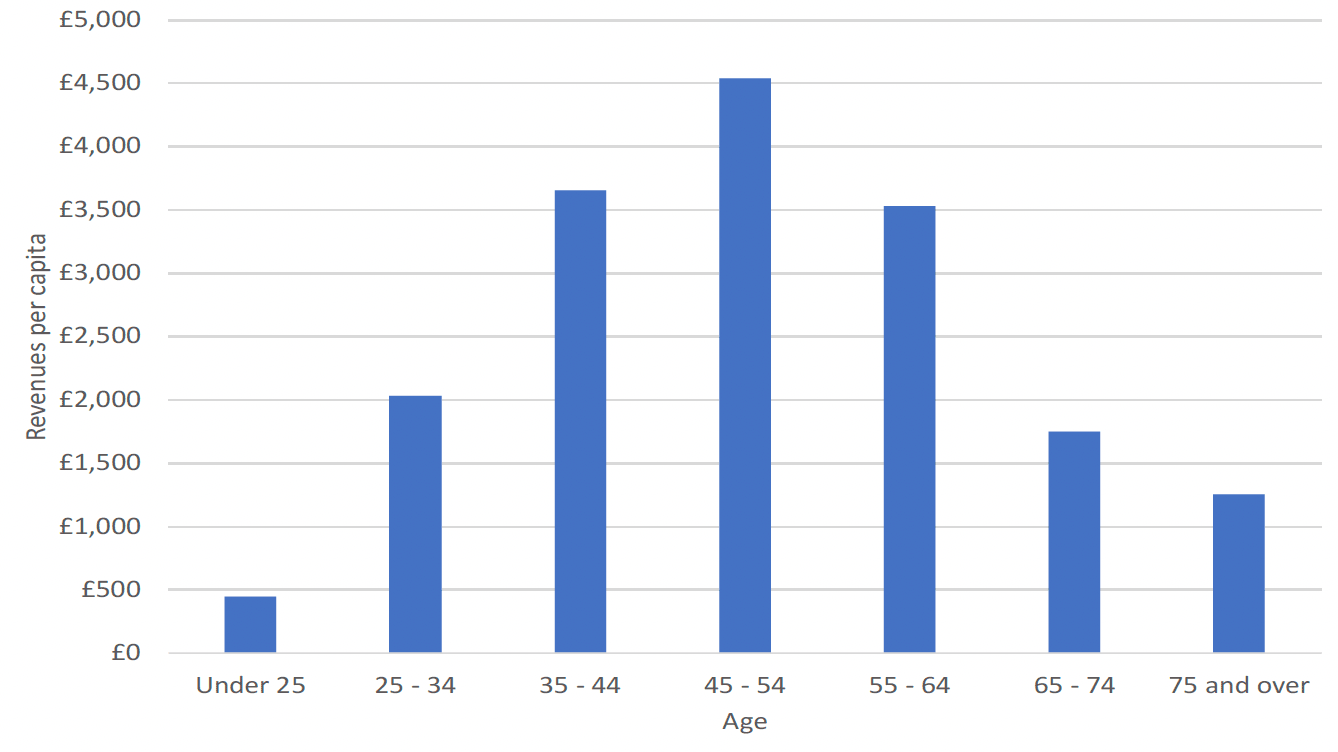

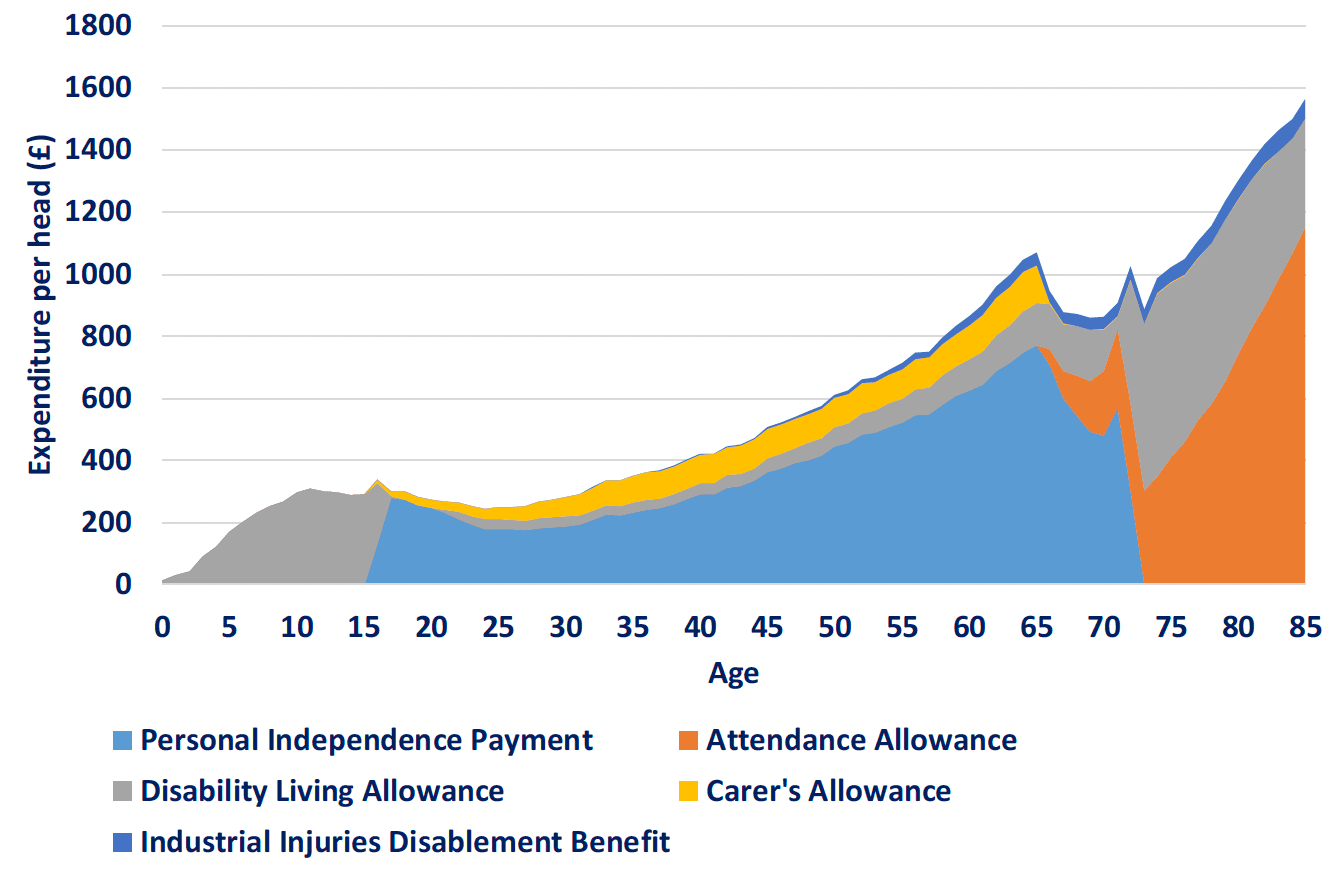

There is a clear relationship between age and average annual income tax liability. On average, tax liabilities are an increasing function of age throughout most of our working lives, as earned and unearned incomes increase. But from people's mid-50s onwards, income tax liabilities fall with age as earnings fall and people retire. This is illustrated in Figure 4.3. There is also a relationship between age and spending on most of the social security benefits that are devolved. Average spending per person on the main benefits being devolved tends to increase with age, driven in particular by PIP and Attendance Allowance. This is illustrated in Figure 4.4.

Notes: revenues per capita for each age group are calculated taking taxpayers and non-taxpayers into account.

Source: Author analysis of Survey of Personal Incomes and Registers of Scotland population data.

Source: Internal Scottish Government analysis based on DWP's StatXplore.

The shape of future demographic change – and the extent to which the share of the population by age varies over time – is likely to have an influence therefore on the growth rate of revenues and spending per capita. Note however that this is not as simple as saying that a more rapidly ageing population is disadvantageous, certainly in the case of income tax – the bell-shaped nature of the age-tax relationship in Figure 4.3 shows that the relationship between demographics is more nuanced than simply being about the ratio between working age and non-working population.

The observation that demographic change can influence the rate of revenue and spending growth has led some to suggest that the BGAs could take into account demographic changes over time. One way that this could be done is to adapt the IPC method, effectively estimating different BGAs for different demographic groups and summing these together to arrive at a total BGA for income tax (or one of the social security payments).

For example, the approach to calculating BGAs might involve distinguishing between six different age groups. A BGA could be calculated for each of these age groups, by taking the growth rate of tax revenues per capita for each of those age groups in rUK, and applying these growth rates to the Scottish population in each age group. The total income tax BGA would then be the sum of the six elements.

Such an approach would insulate the Scottish Government from changes in revenues per capita (or spending per capita) associated with differential demographic change. If these changes reduced Scotland's revenues per capita relative to those of rUK, then the Scottish budget would benefit from such insulation. But the reverse is also true: if differential demographic change increased Scotland's relative revenues per capita, insulation from these effects would reduce the Scottish budget. This is perhaps not as unlikely as it sounds. The share of Scotland's population aged 40 – 55, a group which pays relatively more tax per person than other age groups, is projected to grow slightly more rapidly in Scotland than in rUK in coming years.

How consistent would a demographically-adjusted approach to calculating the BGAs be with the Smith Commission Agreement's principles?

First, note that a demographically-adjusted approach would fail to fully meet the 'taxpayer fairness' principle for the same reason that the IPC and CM approaches fail. The fact that changes in the BGA would take account of Scotland's differing levels of revenues per capita at the point of devolution and differing demographic trends, but spending changes via the Barnett formula are based just on Scotland's population share of spending changes in rUK, creates an asymmetry. In particular, tax increases applying only in rUK would, for income tax and stamp duty land tax, increase net spending on Scotland somewhat, while tax decreases for these taxes only applying in rUK would decrease net spending on Scotland, violating the taxpayer fairness principle.

Whether a demographically-adjusted approach would be more or less inconsistent with the 'taxpayer fairness' principle than the IPC method depends on whether demographic trends are likely to reduce or increase Scottish revenues per capita relative to those of rUK. For example, assuming revenues and spending are increasing in rUK, and assuming Scotland's demographic trends are unfavourable in terms of revenues per capita relative to rUK, insulating the Scottish budget from these trends would in effect transfer even more revenue from rUK to Scotland, violating the 'taxpayer fairness' principle by even more than under the IPC method. On the other hand, if Scotland's demographic trends are favourable in terms of revenues per capita relative to rUK, insulating the Scottish budget from these trends would reduce transfers of revenue from rUK to Scotland, reducing the extent to which the 'taxpayer fairness' principle is violated compared to the IPC method.

If one believes that the 'no detriment' principle applies not just in the first year of devolution but in the years following devolution to factors/trends that can predicted with high probability in advance, then demographically adjusted methods would arguably be more consistent with this principle than methods that did not adjust for demographics, In particular, if one believes demographic trends can be predicted with high probability and the Scottish Government has limited ability to materially influence these trends, then it could be argued that failure to account for these trends when indexing the BGAs would cause undesirable detriment to either the Scottish Government (if those trends are unfavourable) or UK government (if those trends are favourable).

Demographic adjustment is also, arguably, more consistent with the principle that the UK government should bear the risk of UK-wide shocks. In particular, one may expect a common shock to affect revenues differently if demographic structures differ: for example, revenues are likely to be less cyclical (falling less in recessions and rising less in expansions) in areas where a higher fraction of the taxpaying population is aged over the state pension age. Accounting for differences in demographic structures and trends when calculating the BGAs would therefore mean the BGAs more closely approximate the shock affecting Scotland as part of a UK-wide shock.

Thus, relative to the IPC and CM methods, demographically adjusted methods are likely to be more consistent with the 'no detriment' and 'economic shock' principles but may be even less consistent with the 'taxpayer fairness' principle. They are also likely to be less consistent with the 'economic responsibility' principle because the Scottish Government would be insulated from the effects of its policies on the demographic structure of its population relative to rUK – and in turn, the effects (positive or negative) on revenues and spending. This would reduce the Scottish Government's incentive to implement policies that may help it attract more young adults (for which devolved social security spending per capita will be lower) or middle-aged adults (for which tax revenues per capita will be higher) to live in Scotland: the potentially beneficial effects to Scotland's public finances will be offset by the demographic adjustments.

It is also worth noting that demographically-adjusted approaches to indexing the BGA would further complicate the calculations, potentially undermining the transparency of the determinants of the Scottish budget. Our consultation indicated that there is considerable concern that the current method for calculating the BGAs is already too complex for people to understand – and indeed, some respondents themselves showed evidence that they did not understand the intentions and implications of the current approach. Given that the intention was for tax devolution and the associated Fiscal Framework to enhance the accountability of Scottish ministers for the size of the Scottish budget (and hence resulting spending power), greater complexity in calculating the BGAs may be undesirable.

4.3 Taxbase-adjusted approaches

All the methods discussed so far take into account Scotland's higher or lower tax capacity at the point of devolution. This is done through the 'initial deduction' – the BGA is initially determined by the revenues actually raised in Scotland in the year prior to devolution, and all subsequent indexation is made in relation to this starting point. As already discussed, this approach ensures the achievement of the 'no detriment' principle – neither UK nor Scottish Government is immediately better or worse off as a result of the decision to devolve a tax – in the first year of devolution.

However, as well as having a different initial tax capacity, Scotland has a different initial distribution of taxpayers across the tax base. For income tax for example, Scotland had, at the point of devolution, a greater proportion of taxpayers who paid tax at the basic rate, and a lesser proportion of taxpayers who paid tax at the higher and additional rates.

These differences in the initial distribution of taxpayers can affect the outcome of a BGA indexation process. Given that Scotland has proportionately fewer additional rate taxpayers than the UK, then if the growth of income tax revenues from additional rate taxpayers is higher than the growth of income tax revenues from basic rate taxpayers, the BGA is likely to grow more quickly than Scottish revenues, even if the growth rate of revenues from Scottish taxpayers – at all points of the distribution – matches the growth rate observed for rUK taxpayers.

This type of issue has "emerged in the public domain since implementation of BGAs", as highlighted by one of the respondents to our survey. It can be illustrated with a hypothetical example. Panel 1 of Table 4.1 calculates total income tax revenues in Scotland and rUK for a base year under a scenario where there are 2.5 million Scottish taxpayers, 25 million rUK income taxpayers, where the average tax liability in each tax band is the same in Scotland as in rUK, but where the distribution of taxpayers by band is somewhat different in the two nations.

If the growth of tax liabilities per taxpayer is equal across tax bands – for example, 5% – then both UK government revenues, and hence the BGA, and Scottish Government revenues grow at 5%. The Scottish budget is neither disadvantaged nor advantaged by its different initial distribution of taxpayers. This case is illustrated in Panel 2 of Table 4.1.

However, if the growth rate of tax revenues is not equal across tax bands, the outcome might not be as intuitive. Panel 3 of Table 4.1 assumes that, rather than growing equally across bands, tax liabilities per taxpayer grow at 3% for the basic rate band, 5% for the higher rate band, and 7% for the additional rate band, and that this pattern of growth in revenues by band is observed in both Scotland and rUK . This divergence could come about because of faster income growth amongst higher income earners, or it could come about because income growth is even across the distribution, but tax rates are lowered at the basic rate and increased at the additional rate.

In this case, the fact that rUK has proportionately more additional rate taxpayers causes rUK total income tax revenues to grow more quickly than those in Scotland. Specifically, Scottish Government tax revenues grow 4.5% whereas UK government revenues grow 4.9%. The result is that the BGA will grow more quickly than Scottish revenues, despite the fact that the growth rate of Scottish income tax liabilities at all individual points in the income distribution has matched the growth rate of rUK revenues.

| Panel 1: Base year | |||||

|---|---|---|---|---|---|

| Proportion of taxpayers by band | Mean tax liability per taxpayer | Revenue £m | |||

| Scot | rUK | Scot | rUK | ||

| Basic | 88% | 86% | 2,000 | 4,400 | 43,000 |

| Higher | 11% | 12% | 12,000 | 3,300 | 36,000 |

| Additional | 1% | 2% | 80,000 | 2,000 | 40,000 |

| Total | 100% | 100% | 9,700 | 119,000 | |

| Taxpayers (million) | 2.5 | 25 | |||

| Panel 2: 5% tax liability growth at all points of distribution | |||||

| Basic | 0.88 | 0.86 | 2,100 | 4,620 | 45,150 |

| Higher | 0.11 | 0.12 | 12,600 | 3,465 | 37,800 |

| Additional | 0.01 | 0.02 | 84,000 | 2,100 | 420,00 |

| Total | 10,185 | 124,950 | |||

| Growth on base year | 5.00% | 5.00% | |||

| Panel 3: tax liability growth 3%, 5% and 7% at basic, higher at additional rate | |||||

| Basic | 0.88 | 0.86 | 2,060 | 4,532 | 44,290 |

| Higher | 0.11 | 0.12 | 12,600 | 3,465 | 37,800 |

| Additional | 0.01 | 0.02 | 85,600 | 2,140 | 42,800 |

| Taxpayers (million) | 2.5 | 25 | 10,137 | 124,890 | |

| Growth on base year | 4.51% | 4.95% | |||

Source: Authors' calculations.

Of course, the reverse is also possible. If revenues from basic rate taxpayers grew more quickly than revenues from additional rate taxpayers, in both Scotland and rUK, then this could favour the Scottish budget (since the part of the tax base experiencing the most rapid tax growth accounts for a larger share of revenues in Scotland).

Since the Scottish Government cannot control the distribution of its taxbase at the point of devolution, taking this distribution into account in the way that the BGA is indexed could be argued to be more consistent with the 'no detriment' principle in its dynamic interpretation.

One way of taking these distributional issues into account is to calculate separate BGAs for each tax band. This is the approach adopted in Wales. The 'by band' method is useful in protecting the Scottish budget from the effects of a different starting distribution of taxpayer income. Under the 'by band' approach, the devolved budget is protected from the risks of proportionately faster growth from the additional or higher rates in rUK than from the basic rate – whether that comes about through faster growth in taxpayer incomes in the upper part of the distribution, or tax policy changes that increase the share of tax revenues raised from the higher and additional bands.

Taxbase-adjustment is also, arguably, more consistent with the principle that the UK government should bear the risk of UK-wide shocks. In particular, one may expect a common shock to affect revenues differently if taxbase structures differ: revenues are likely to be affected differently depending on the tax structure in different types of economic shocks.

For example, a big shock to the stock market and finance sector of the economy will likely effect revenue growth from higher income bands more than lower income bands. Conversely, a shock to employment in low-paying occupations is likely to have a bigger effect on overall revenues when there are proportionately more taxpayers in that part of the income distribution, and hence a higher share of revenues come from basic rate taxpayers. Accounting for differences in tax base structures when calculating the BGAs would therefore mean the BGAs more closely approximate the shock affecting Scotland as part of a UK-wide shock.

However, the 'by band' approach is not fully consistent with the 'taxpayer fairness' principle, largely for the same main reason that the IPC and CM methods are not consistent with that principle. Depending on the specific circumstance, the 'by band' approach could be either less consistent or (slightly) more consistent with the taxpayer fairness principle than the IPC approach. For example, if the UK government were to change tax policy in such a way as to increase revenues from additional rate taxpayers, then the effect of the by band method is likely to be that a slightly greater proportion of the additional UK government revenues from this policy would be transferred to Scotland than under the IPC method. (This is because the by band method results in a somewhat lower increase to the BGA, since it takes account of Scotland's lower proportion of additional rate taxpayers). However, if the UK government were to introduce a policy that increased revenues from basic rate taxpayers, the 'by band' approach might lead to a slightly higher BGA than the IPC would do, reducing overall transfers of revenues from rUK to Scotland.

Thus, relative to the IPC and CM methods, taxbase adjusted methods are likely to be more consistent with the 'no detriment' and 'economic shock' principles but may be even less consistent with the 'taxpayer fairness' principle. As with demographically-adjusted approaches, taxbase-adjusted approaches are more complex, potentially posing issues for accountability and transparency. However, there may be an opportunity to learn from the experience of Wales, where such an approach is in use for income tax.

4.4 Approaches that provide insurance against divergent revenue and spending trends

Setting the initial BGAs equal to the revenues and spending being devolved provides full insurance, at the point of devolution, to the Scottish Government for revenues being lower per capita and spending higher per capita than rUK at that initial point.

As discussed in the sections above, the various methods (IPC, CM, Levels Deduction, demographically-adjusted methods, taxbase-adjusted methods) provide insurance against shocks affecting the whole of the UK – albeit sometimes too little and sometimes too much insurance. However, the methods provide little insurance against divergences in revenue or spending trends post-devolution, except for those related to the specific factors adjusted for: such as differential population (IPC), differential ageing trends (demographically-adjusted methods), and different initial taxbase structures (taxbase-adjusted methods).

Under the IPC method for example, the Scottish Governments bears the full risk of slower or faster percentage rate of growth of revenues or spending than in rUK. Under an approach that adjusted for demographic trends and taxbase structures, the Scottish Government would bear in full the risk that people of a given age and income level saw a slower or faster rate of growth in tax payments or spending receipts, on average, in Scotland than rUK.

If differences in the appropriately adjusted rates of growth in revenues and spending are driven to some extent by factors outside the control of the Scottish Government, there may be a case for providing insurance against the risk of ongoing and growing divergences. In its response to our consultation, the Scottish Government argued that "there is a case for some form of limited fiscal insurance that could be incorporated into the devolved taxes, that could be a revision to the current BGA system or something more akin to the Welsh Government's "funding floor".[9] The Scottish Government also said it thought that this could be done "whilst remaining consistent with the Smith Commission principles".[10]

It is beyond the scope of this report to consider changes to how the underlying block grant itself is adjusted – although we note that the Smith Commission Agreement said that it should continue to be determined by the Barnett formula.

With regards to the BGAs themselves, there are, in principle, two broad approaches available for incorporating insurance in to the Scottish Fiscal Framework: the specification of pre-determined limits on the size of the gap between BGAs and revenues (or spending) that are allowed to open up; and periodically 'resetting' the BGA to account for changes in underlying taxbases or spending needs since the BGAs were initially set (or last reset).

The first approach is to specify pre-determined limits (a 'floor', and to ensure fairness and symmetry, 'a ceiling') on the gap between devolved revenues and spending and the corresponding BGAs that are allowed to appear before there are funding transfers to or from the Scottish Government to limit further divergence. For example, it might be agreed that if the BGA for income tax exceeded devolved income tax revenues by more than a certain percentage or cash amount, the UK government would provide additional funding to cap the Scottish Government's net funding reduction. On the other hand, if devolved revenues exceeded the BGA by more than a certain percentage or cash amount, the Scottish Government would transfer any further net gains to the UK government.

A more nuanced version of this arrangement would also be possible, whereby below and above pre-determined thresholds, the Scottish Government's budget would be exposed to some proportion (between 0% and 100%) of further divergence between devolved tax revenue (or spending) and the corresponding BGA.

The second approach is to periodically update or 'reset' BGAs to account for changes in Scotland's relative tax base or spending needs. For example, after a predetermined period of five or ten years, the Scottish and UK governments could agree to update the BGAs to account partially or fully for changes in tax bases or spending needs in the intervening years. Such an approach would mean that immediately following a reset, the Scottish Government would bear the risk of divergences for the full five or ten years until the next reset, whereas just prior to a reset it would bear the risk for just a year, at which point the BGAs would be reset. This would mean the Scottish Government's incentives to undertake policies that could help increase the tax base and reduce spending needs would vary over time. And indeed, the Scottish Government could have an incentive to engage in actions that temporarily depress the tax base or push up spending needs immediately prior to a reset, so that BGAs were correspondingly adjusted. (For example, the timing of salary payments for government employees could be adjusted, or processing times for fully devolved taxes increased).

A variation on a fixed periodic reset is to reset the BGAs on a rolling basis. For example under a 5-year rolling reset, in the sixth year of devolution, the BGA would be updated based on the taxbase or spending needs in the first year of devolution; in the seventh year, it could be updated based on the taxbase or spending needs in the second year of devolution; and so on. This is the approach that the UK government has previously suggested for resetting revenue baselines for English councils as part of the business rates retention system.

Implementing any of these approaches in practice would be subject to a significant challenge: Changes in tax and social security policy post-devolution in both Scotland and rUK mean it would be difficult to estimate what revenues and spending would be in Scotland if policy had remained in line with rUK. But resets of limits have to be set on the basis of policy being the same in Scotland and rUK, otherwise the Scottish Government would be compensated for tax cuts (and spending increases) and penalised for tax increases (or spending cuts).

For example, a decrease in income tax rates in Scotland relative to rUK would reduce revenues relative to the BGA. But it would not make sense for the Scottish budget to be insured against this policy-induced reduction in revenue as this would mean that Scottish residents would be paying lower taxes but not bearing the full costs. This would be inconsistent with the 'economic responsibility' principle and would incentivise the Scottish Government to reduce taxes and increase social security spending, knowing that it would not bear the full costs.

There are two stages to adjusting revenues and spending for divergences in policy post-devolution: adjusting for the mechanical effects of differences in policy given the tax base and spending needs pertaining; and adjusting for the behavioural effects of policy divergences, which can affect tax bases and spending needs.

To do the first, one would need to calculate what Scottish revenues and social security spending would be if the policy in place in rUK applied in Scotland. For taxes where the only things that have diverged post-devolution are tax rates and bands, such as income tax, this should be feasible. This should also be the case for benefits where all that has changed are payment amounts. However, for taxes where there have been changes to taxbases, and benefits where there have been changes to eligibility criteria and assessment processes, such as disability benefits, this would be a much more difficult challenge.

Adjusting for behavioural effects is also difficult. For example, if the tax base or number of people eligible for a benefit has grown more or less in Scotland than in rUK post-devolution, to what extent is this driven by differences in policy, versus being driven by other underlying socio-economic factors. This is an important question to address, because while we may want to insure the Scottish Government against risks associated with the latter, we would want it to bear the behavioural as well as the mechanical effects of its policies on its revenues and spending. For example, if the Scottish Government were to have a substantially higher tax rate on incomes above £150,000 (a highly responsive group of taxpayers), we would want it not only to gain revenues as a result of the higher tax rates, but also to lose as a result of behavioural responses undertaken by taxpayers to reduce their tax liabilities (such as reducing the work effort, engaging in greater tax avoidance or evasion, or migrating). If the Scottish Government does not bear these costs, its incentives are skewed towards setting higher tax rates and more generous benefits policies than would otherwise be the case.

However, even after a policy is implemented, one cannot know for sure what the behavioural response to it is – one can only estimate it statistically, and such estimates are subject to both measurement error and methodological difficulties. For a tax such as income tax, even relatively small differences in estimates of the scale of behavioural response can mean differences of tens of millions of pounds in revenue. Agreeing the size of the behavioural adjustments to make to estimates of the tax revenue capacities of the devolved governments would therefore likely be very politically difficult. It is for this reason that the 2016 Fiscal Framework suggests that behavioural 'spillover' effects of one government's decisions on the revenues or spending of other governments should only be compensated for in exceptional circumstances.

Thus, implementing insurance via the BGAs in a way that is consistent with the principle of 'economic responsibility' is likely to be difficult in practice. It will prove difficult to adjust for even the mechanical effects of policy divergences for taxes and benefits where there have been major changes in the design post-devolution; and adjusting for the behavioural effects of policy divergence would require agreement on uncertain behavioural elasticities.

How would the provision of insurance relate to the other Smith Commission Agreement's principles?

With regards to the principle that the UK government should bear the risk of UK-wide shocks, the implementation of floors/ceilings or resets to the BGAs would not adversely affect this.

With regards to the 'no detriment' principle, if one believes that this applies dynamically beyond the first year of devolution, then in principle, insurance against long-term divergences in tax base and spending needs growth could make the BGAs more consistent with this principle. This is because it would stop the Scottish Government or UK government suffering detriment over time from factors outside of the Scottish Government's control.

With regards to the 'taxpayer fairness' principle, the effect of insurance will depend on how Scottish taxbases and spending needs evolve relative to rUK. As discussed above, the methods considered so far would likely violate this principle over time by transferring to Scotland part of the revenues raised from devolved taxes in rUK. This is because the BGAs take account of Scotland's lower initial revenues per capita, whereas Scotland will in general benefit from a population-based share of higher spending funded by those higher taxes. If post-devolution, Scotland's tax base was to decline relative to that of rUK (as it has done so far for income tax, for example), implementing a floor or updating the BGAs would result in further transfers of revenue from rUK to Scotland, further violating the taxpayer fairness principle. In contrast, if post-devolution, Scotland's tax base was to grow relative to that of rUK, implementing a ceiling or updating the BGAs would result in reduced transfers of revenues from rUK to Scotland, meaning that the taxpayer fairness principle would be less violated.

In summary therefore, providing insurance via the BGAs is technically difficult, especially in a way fully consistent with the 'economic responsibility' principle. Insurance arguably would be consistent with the 'no detriment' principle. And whether it further reduced or increased consistency with the 'taxpayer fairness' principle would depend on whether Scotland ended up benefiting from or losing from the insurance system.

4.5 Approaches not based on revenues or spending in rUK

It is sometimes suggested that the growth of BGAs should be indexed not to the growth of equivalent revenues or spending but to some other measure instead. Mooted candidates have included nominal GDP, inflation or earnings.

Such an approach might be relatively simpler to understand and interpret. But it would not be consistent with the Smith Commission Agreement's principles.

Such an approach would not meet the 'taxpayer fairness' principle. If the UK government changed tax policy in a way to raise revenues and spending, the Scottish budget would benefit from the increased spending but there would be no commensurate increase in its tax BGA, if this were indexed to something other than comparable revenues. Conversely, if the UK government cut tax rates and spending, the Scottish budget would be reduced despite the tax cut not applying in Scotland.

More generally, whenever rUK revenues were increasing more rapidly than the alternative index (whether that is GDP, earnings, inflation, or something else), the outcome would be detrimental to rUK taxpayers (since the BGA would increase less quickly than the increase in rUK revenues and spending). If rUK revenues increased more slowly than the alternative index, the result would be detrimental to Scottish taxpayers.

Indexing to an alternative measure would also be unlikely to meet the principle that the UK government should manage the fiscal risks of UK-wide economic shocks. A UK-wide shock that reduces tax revenues across the UK (or that increases social security spending across the UK) may not have proportionately similar effects of alternative indexes.

In 2020/21 for example, revenues from property transactions taxes fell by nearly one quarter, and revenues from income tax revenues grew by 1%. Nominal GDP fell by 5%, earnings grew by around 2.6%, and CPI inflation was about 0.6%. None of these alternative indexes would therefore have done a good job at protecting the Scottish budget from the effects of the fall in LBTT revenues across the UK (including Scotland). On income tax, the Scottish budget would not have been protected from the effects of weaker revenue growth if the BGA had been indexed to earnings, but would have been significantly 'over-insured' had the BGA been indexed on the basis of GDP.

Indexing the BGAs to an alternative measure would be unlikely to achieve the 'no detriment' principle in its dynamic sense. Whether or not the Scottish budget ended up better or worse off as a result of tax devolution would largely be arbitrary, and would depend on the extent to which revenues or spending grew differentially to whatever index had been chosen.

The alternative approaches would largely meet the 'economic responsibility principle' though. For example, suppose that the BGA is indexed to the growth in GDP, or earnings. If the Scottish Government implemented a tax policy which increased revenues, it would gain from the increase in its revenues at the margin, relative to a decision not to implement the tax increase. However, as noted above, the baseline on which this marginal effect is considered is essentially arbitrary. And if the alternative index was related to Scottish (rather than rUK ) revenue or economic performance, this principle would be significantly violated.

In summary, indexing the BGAs to changes in equivalent, or comparable, rUK revenues and gets much closer to the achievement of the Smith principles than any of these alternatives would achieve.

Contact

Email: matthew.elsby@gov.scot