Fiscal Framework Review: Independent Report

An independent report to consider the Block Grant Adjustment arrangements commissioned by Scottish Government and HM Treasury in June 2022, written by Professor David Bell (University of Stirling), David Eiser (formerly University of Strathclyde) and David Phillips (Institute for Fiscal Studies).

5. Discussion and conclusions

Devolution of tax and social security responsibilities requires adjustments to be made to the Scottish Government's block grant. The Smith Commission's Agreement, which recommended the tax and social security powers to be devolved, proposed a number of principles it believed should guide the operation of the Scottish Government's fiscal framework following tax and spending devolution, including the calculation of these block grant adjustments (BGAs).

This report has evaluated the current and alternative methods for calculating the BGAs. In particular, it has assessed the extent to which different methods for calculating BGAs are consistent with the Smith Commission's principles. It has also considered the balance of fiscal risks and incentives faced by the Scottish Government under the different approaches, and how these differ from the balance of fiscal risks and incentives for previously devolved spending responsibilities, funding for which is updated each year via the Barnett formula.

No single method for indexing the BGAs can fully achieve all of the Smith Commission's principles

Our overarching conclusion is that it is not possible to fully satisfy all of the Commission's principles for the design of the Scottish fiscal framework. Some of the principles are mutually incompatible with one another. Several approaches to calculating the BGAs can achieve the Smith Commission principles partially, but none can achieve them all in full.

The fundamental tension is between the 'taxpayer fairness' principle on the one hand, and the 'no detriment' principle on the other. Achievement of the taxpayer fairness principle requires that BGAs are calculated using the 'Barnett Formula' approach (also known as Levels Deduction in the case of tax BGAs). This approach – which increases the Scottish Government's BGA in line with a population share of the change in total rUK revenues or spending – best ensures that tax changes in rUK do not affect spending in Scotland, by exactly offsetting changes in funding for pre-existing devolved services via the Barnett formula.

However, the Barnett Formula/Levels Deduction approach is not compatible with the 'no detriment' principle in its dynamic context. It is reasonable to interpret the 'no detriment' principle as having implications beyond the first year of devolution, since the Smith Commission highlighted the need for 'appropriate' indexation when defining this principle. Scotland's lower tax capacity would mean that, for example, revenues per capita would need to grow at a faster percentage rate than those in rUK to keep pace with BGAs that increase by population-based increments. This would mean that the Scottish budget would be expected to suffer detriment as a result of the decision to devolve taxes to Scotland, unless revenues grew at a faster rate per capita in Scotland until they converged with rUK levels.

The IPC and CM methods – which are the arrangements cited in the existing Fiscal Framework for tax BGAs – are more compatible with the 'no detriment' principle, since they do not require Scottish revenues to grow proportionately faster simply for the Scottish budget not to suffer detriment as a result of devolution. However, these methods do not meet the taxpayer fairness principle in full.

The IPC and CM methods account for Scotland's lower overall tax capacity at the point of devolution. This means that when revenues are increasing in rUK, a portion of these is effectively transferred to Scotland. This is because while Scotland would typically benefit from a population-based share of the increase in spending funded directly by those higher revenues (either via the Barnett formula or when they are spent on reserved services), the increase in the BGA would be based on Scotland's tax capacity, which is generally lower than its population share. The increase in the BGA would therefore not fully offset the increase in underlying funding for Scotland. As a result, revenues raised from devolved taxes in rUK would partly be funding spending in Scotland, violating the 'taxpayer fairness' principle.

Different BGA methods achieve the Smith Commission's principles to varying extents

Our second conclusion is that different BGA approaches achieve each of the Smith Commission principles to varying extents.

For example, the IPC and CM methods satisfy the 'taxpayer fairness' and 'no detriment' principles to different extents. While neither fully satisfy the 'taxpayer fairness' principle, the CM method is closer to satisfying it, as it treats population growth in the same way as the Barnett formula. In contrast, the IPC method arguably better satisfies the 'no detriment' principle in the years following devolution as it fully adjusts for the fact that relative population growth – which the Scottish Government may have little control over – is an important determinant of aggregate tax revenue growth.

Similarly, the IPC and CM methods satisfy the 'economic responsibility' and 'economic shocks' principles to different extents. In terms of economic responsibility, the IPC approach insulates the Scottish budget from the effects that its policies might have on revenues via increases or decreases in population, contrary to the 'economic responsibility' principle. In contrast, under the CM method, which does not fully adjust for differential population growth, the Scottish budget would increase if its policies caused population (and hence revenues) to increase.

On the other hand, the IPC method is arguably more consistent with the principle that the UK government should bear the risk of shocks affecting the whole of the UK. This is because a common shock across the UK as a whole is more likely to have a common effect on revenues or spending per capita, rather than aggregate revenues or spending.

As well as examining the IPC and CM methods, this report has also considered the extent to which a number of other BGA mechanisms are consistent with the various Smith Commission principles.

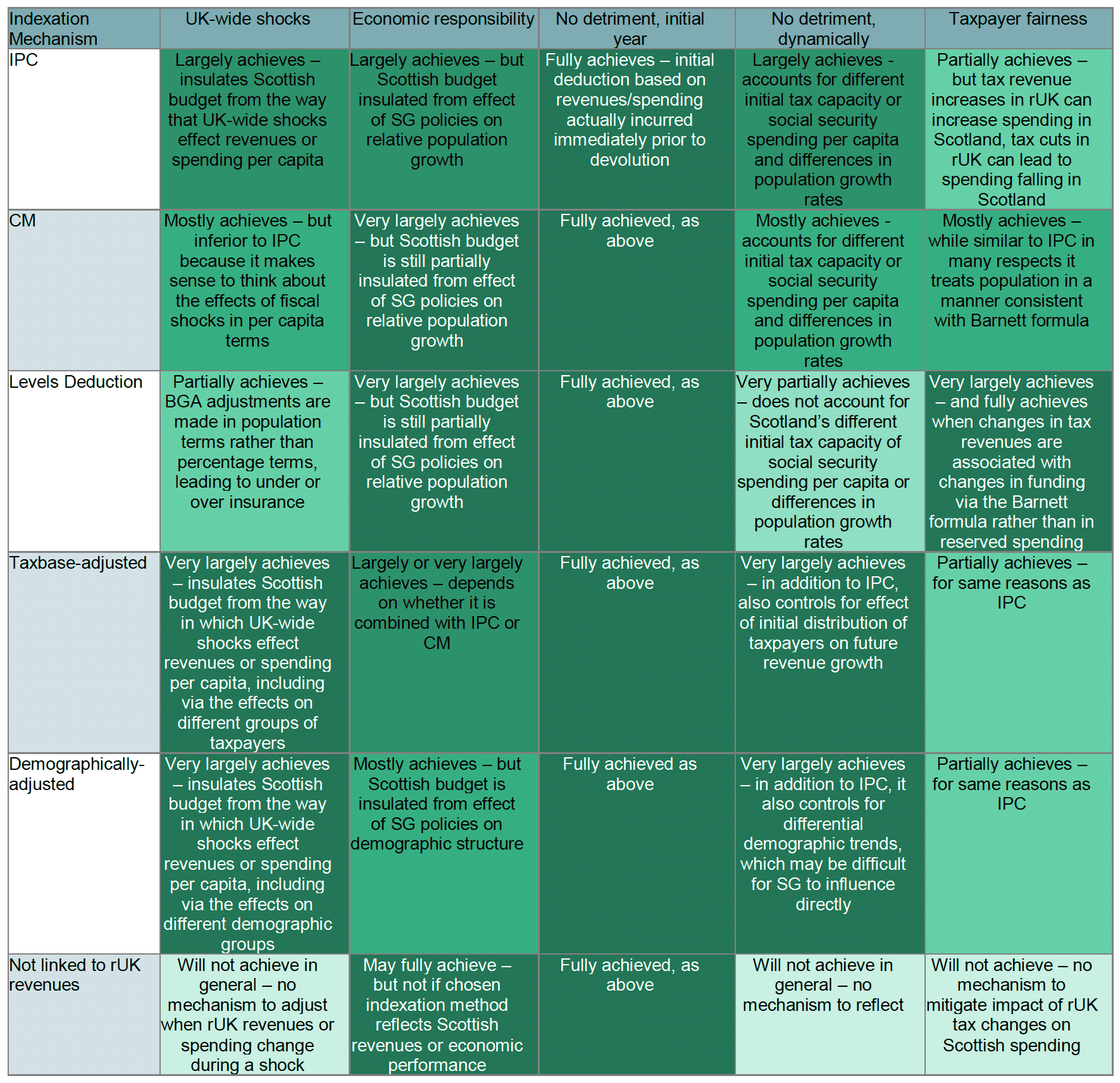

The Table overleaf summarises our conclusions. The more consistent we judge an approach to be for a given principle, the darker the shade of green. For ease of reference in interpreting the table, we reproduce here the Smith Commission principles:

- UK economic shocks: The UK government should continue to manage the fiscal risks and shocks that affect the whole of the UK for the newly devolved revenue streams and spending responsibilities.

- Economic responsibility: The devolved Scottish budget should benefit in full from policy decisions by the Scottish Government that increase revenues or reduce expenditure, and the devolved Scottish budget should bear the full costs of policy decisions that reduce revenues or increase expenditure.

- No detriment from the initial decision to devolve: There should be no detriment to the Scottish or UK governments' budget simply as a result of the initial transfer of tax and/or spending powers. In defining this principle, the Commission also stated that the BGAs should be 'indexed appropriately'. This implies that as well as relating to the initial year in which devolution occurs, the principle also has a dynamic interpretation, i.e. is the existence of particular issues or trends when devolution occurs likely to cause detriment to the Scottish budget in future years?

- Taxpayer fairness: Changes to taxes in the rest of the UK, for which responsibility in Scotland has been devolved, should only affect public spending in the rest of the UK; changes to devolved taxes in Scotland should only affect public spending in Scotland.

Note: Darker shades indicate greater consistency with a given Smith Commission principle.

Source: Author's analysis of the BGA indexation mechanisms.

Graphic text below:

Indexation Mechanism: IPC

UK-wide shocks: Largely achieves – insulates Scottish budget from the way that UK-wide shocks effect revenues or spending per capita

Economic responsibility: Largely achieves – but Scottish budget insulated from effect of SG policies on relative population growth

No detriment, initial year: Fully achieves – initial deduction based on revenues/spending actually incurred immediately prior to devolution

No detriment, dynamically: Largely achieves - accounts for different initial tax capacity or social security spending per capita and differences in population growth rates

Taxpayer fairness: Partially achieves – but tax revenue increases in rUK can increase spending in Scotland, tax cuts in rUK can lead to spending falling in Scotland

Indexation Mechanism: CM

UK-wide shocks: Mostly achieves – but inferior to IPC because it makes sense to think about the effects of fiscal shocks in per capita terms

Economic responsibility: Very largely achieves – but Scottish budget is still partially insulated from effect of SG policies on relative population growth

No detriment, initial year: Fully achieved, as above

No detriment, dynamically: Mostly achieves - accounts for different initial tax capacity or social security spending per capita and differences in population growth rates

Taxpayer fairness: Mostly achieves – while similar to IPC in many respects it treats population in a manner consistent with Barnett formula

Indexation Mechanism: Levels Deduction

UK-wide shocks: Partially achieves – BGA adjustments are made in population terms rather than percentage terms, leading to under or over insurance

Economic responsibility: Very largely achieves – but Scottish budget is still partially insulated from effect of SG policies on relative population growth

No detriment, initial year: Fully achieved, as above

No detriment, dynamically: Very partially achieves – does not account for Scotland's different initial tax capacity of social security spending per capita or differences in population growth rates

Taxpayer fairness: Very largely achieves – and fully achieves when changes in tax revenues are associated with changes in funding via the Barnett formula rather than in reserved spending

Indexation Mechanism: Taxbase-adjusted

UK-wide shocks: Very largely achieves – insulates Scottish budget from the way in which UK-wide shocks effect revenues or spending per capita, including via the effects on different groups of taxpayers

Economic responsibility: Largely or very largely achieves – depends on whether it is combined with IPC or CM

No detriment, initial year: Fully achieved, as above

No detriment, dynamically: Very largely achieves – in addition to IPC, also controls for effect of initial distribution of taxpayers on future revenue growth

Taxpayer fairness: Partially achieves – for same reasons as IPC

Indexation Mechanism: Demographically-adjusted

UK-wide shocks: Very largely achieves – insulates Scottish budget from the way in which UK-wide shocks effect revenues or spending per capita, including via the effects on different demographic groups

Economic responsibility: Mostly achieves – but Scottish budget is insulated from effect of SG policies on demographic structure

No detriment, initial year: Fully achieved as above

No detriment, dynamically: Very largely achieves – in addition to IPC, it also controls for differential demographic trends, which may be difficult for SG to influence directly

Taxpayer fairness: Partially achieves – for same reasons as IPC

Indexation Mechanism: Not linked to rUK revenues

UK-wide shocks: Will not achieve in general – no mechanism to adjust when rUK revenues or spending change during a shock

Economic responsibility: May fully achieve – but not if chosen indexation method reflects Scottish revenues or economic performance

No detriment, initial year: Fully achieved, as above

No detriment, dynamically: Will not achieve in general – no mechanism to reflect

Taxpayer fairness: Will not achieve – no mechanism to mitigate impact of rUK tax changes on Scottish spending

The Table shows that indexing the BGAs in a way that accounts for different initial taxbase structures would be more consistent with the 'no detriment' principle in the years following devolution. This is because, at the point of devolution, the Scottish Government did not have a meaningful ability to influence its tax base structure. (Although arguably, different policies in the years before devolution could have influenced it).

Indexing the BGAs in a way that accounts for differential demographic trends would be more consistent with the 'no detriment' principle in the years following devolution if one believes that the Scottish Government has little ability to influence relative demographic trends. However, if such adjustments were to lead to slower increases in the BGA than otherwise, additional revenues would be transferred from rUK to Scotland, further violating the taxpayer fairness principle.

Using the Levels Deduction method would be most consistent with the taxpayer fairness principle, and would like the CM method be more consistent with the economic responsibility principle than the IPC approach. But because it does not account for differences in tax capacity or spending per capita, it would be less consistent with the 'no detriment' principle in its dynamic form, and would 'over-insure' Scotland's budget against UK-wide economic shocks.

The Table also shows that, with the exception of the 'economic responsibility' principle, indexing the BGAs according to factors other than revenue growth in rUK would violate each of the Smith Commission's principles.

In addition, it is also worth remember that while introducing an element of insurance against divergence in revenues trends could, in certain circumstances, improve consistency with the 'no detriment' principle, it would be very challenging to make this consistent with 'economic responsibility'.

Finding compromise… can the principles be prioritised?

If no method is fully consistent with the Smith Commission Agreement's principles, and different methods better satisfy the different principles to varying extents, the Scottish and UK governments have two ways forward when determining which BGA indexation method to use.

One option is to agree how much weight to put on different principles. For example, the higher the weight one applies to the 'no detriment principle', the more attractive methods that adjust for factors such as initial revenues per capita, tax base structures, and population and demographic change, are likely to be. Such methods are also likely to be more attractive the more weight one places on the idea that the UK government should continue to bear the risk associated with UK-wide shocks, given such factors are likely to affect how UK-wide shocks impact on Scotland specifically.

In contrast, the more weight one applies to the 'taxpayer fairness' principle, the more attractive the Levels Deduction and to a lesser extent the CM method would be. These methods would also be more consistent with the 'economic responsibility' principles.

In its response to our consultation, the Scottish Government said that it felt the 'no detriment' principle should be prioritised. The UK government did not respond to the consultation, but in 2016 interpreted the 'no detriment' principle as applying in the first year of devolution only, with the 'taxpayer fairness' principle applying in subsequent years.[11] Agreement would therefore require compromise.

The Scottish Parliament Finance and Public Accounts Committee asked that this independent report make a recommendation on which principles to prioritise. This would be beyond the terms of reference agreed for this report, which explicitly requested that this we do not make recommendations. It is also our view that this fundamentally political decision needs to be made by elected politicians. However, we can make some suggestions on the issues only should consider when prioritising the principles.

Two seem most relevant.

The first is the priority placed on redistribution and sharing within the UK's fiscal union. The more priority placed on this, the greater the priority one would want to assign to the 'no detriment' principle (including in years following devolution) and the principle that the UK government should bear the risk of UK-wide economic shocks.

If one puts significant emphasis on redistribution and sharing as key tenets of the fiscal union, one would presumably accord lower priority to the taxpayer fairness principle. In particular, one would presumably be relatively unconcerned about revenues being redistributed from rUK to Scotland to compensate for its lower tax capacity – indeed, this could be seen as a positively good thing if one prioritises redistribution and sharing within the Union. In addition, a concern for redistribution and risk sharing would also suggest an openness to considering a role for fiscal insurance and updates to the BGAs for large and/or long-term divergences in revenue and spending trends. This could redistribute funding from rUK to Scotland or vice versa, depending on relative tax base growth.

The second is the importance placed on increasing the responsibility of the Scottish Government for improving the economic performance of Scotland. The greater the emphasis placed on this, the greater the emphasis one would wish to place on the 'economic responsibility' and 'taxpayer fairness' principles. For example, if one feels that the Scottish Government should be responsible for addressing its low revenues per capita for income tax post-devolution, one may be willing to see the unwinding of existing redistributive flows, as implied by the Levels Deduction approach.

In other words, the question here is fundamentally about what type of fiscal union that exists between Scotland and rUK in respect of taxes and social security benefits that are devolved. Does devolution mean a fundamental shift towards greater local responsibility for relative economic performance, and an unwinding of previous risk-sharing and redistributive arrangements? Or does devolution take place in the context of a fiscal union which still emphasises a high degree of risk-sharing and solidarity, even for taxes and spending which is devolved?

The extent to which this question can be answered by drawing on wider precedence in the operation of fiscal arrangement across the UK is ambiguous. On the one hand, for taxes that have been devolved prior to 2016, such as Non-Domestic Rates and Council Tax, there is no explicit revenue sharing between Scotland and rUK. Effectively, something akin to Levels Deduction operates for Non-Domestic Rates, with changes in revenues for this tax in rUK translating into a population-based adjustment to the Scottish Government's block grant funding. Similarly, there is no explicit needs assessment on the spending side, which allocates the Scottish budget population-based shares of changes in rUK spending.

On the other hand, arrangements in Wales now incorporate a 'funding floor' to prevent funding for the Welsh Government falling below a particular per capita level relative to equivalent spending in England, and do take account of the differential tax base structure in Wales. More generally, the benefits of fiscal pooling and sharing are frequently stressed by the UK government as major principles of UK's fiscal union.

Finding compromise…the division of responsibility for different types of fiscal risk

An alternative approach to agreeing the BGA mechanisms would be to focus on the types of risks and incentives one thinks the Scottish Government should face in relation to devolved taxes and social security benefits. One of the respondents to our consultation suggests that the Smith Commission was a "rushed fix" and argues that it should not be "decisive for the decisions to be taken in the Fiscal Framework Review".

For example, one may decide that the Scottish Government cannot now influence its initial levels of revenues per capita and tax base structure. On the other hand, one may decide that while relative population and demographic trends are largely explained by factors outside of the Scottish Governments control, it does have sufficient influence – through policies that make Scotland a more attractive place to live and raise a family – for it to face the financial effects of such policies.

Such reasoning would point towards the use of the CM method, with an appropriate tax base structure adjustment (such as separate BGAs for each tax band). This could be complemented by a degree of fiscal insurance to prevent large divergences in population and demographic trends having substantial detriment to the Scottish budget, given that a significant part of such divergences are likely to be outside the Scottish Government's control.

If instead, one felt that the Scottish Government should be insulated from risks associated with differential population growth, but that it should bear the consequences of having fewer high earners than rUK, one could favour the standard (i.e. currently used) IPC method.

The need for transparency

Both during and following the re-negotiation of the Scottish Fiscal Framework and BGA calculation methods, the Scottish and UK governments should also bear in mind the transparency and public understanding of the operation of the BGAs. These issues of transparency and understanding were raised by a number of respondents to our consultation. There may be a trade-off between more complex mechanisms which better meet certain Smith Commission or other principles, and the ability of key stakeholders in the Scottish and UK parliaments and civil society to understand the rationale for and implications of the arrangements.

The governments should set out not only the calculations that will be used but explain clearly why these arrangements have been chosen, and what their implications are for the types of risks and incentives the Scottish Government will face. They should highlight which Smith Commission principles have been prioritised, and if alternative principles have guided decisions, what those principles are.

The governments should continue to publish – and if possible improve – analysis of the outcomes of the operation of the Fiscal Framework. This should include figures for the BGAs and devolved revenues and spending. Additionally, where adjustments have been made to account for differential population and demographic change and/or differences in tax base structures, or insurance mechanisms been implemented, the impacts of these on the BGAs (and the net tax/spending positions) should be shown so that the transfers to/from the Scottish Government that these entail can be monitored, informing any further future reviews of the Fiscal Framework.

In summary, the BGAs are a critical component of tax and social security devolution. No single method perfectly meets all the principles of the Smith Commission Agreement simultaneously. In agreeing a mechanism to use in future, compromise will be required. Both governments should aim to set out transparently the rationale for whatever compromise solution is ultimately agreed, and the implications of that for the way in which various fiscal costs and risks are shared.

Contact

Email: matthew.elsby@gov.scot