US Export Plan: sector report - renewables

This is one of 8 sector reports that outlines the background research and analysis prepared in support of the US Export Plan and looks to identify the key opportunities in the USA for Scottish companies in this sector.

Exporting to the US

In the short to medium term, US market dynamics will require many exporters to align with technologies prioritised under current federal policy, such as advanced geothermal, CCS, and grid resilience solutions, while navigating tighter compliance rules, compressed timelines and uncertainty for wind and solar projects. As such, given these current trends, Scottish expertise in some areas, such as floating offshore wind, may be more of a potential long-term horizon opportunity. Despite these policy headwinds, demand from US corporations, and particularly from data centres, for clean power remains strong, offering niche opportunities for innovative, cost-competitive solutions that meet domestic sourcing requirements.

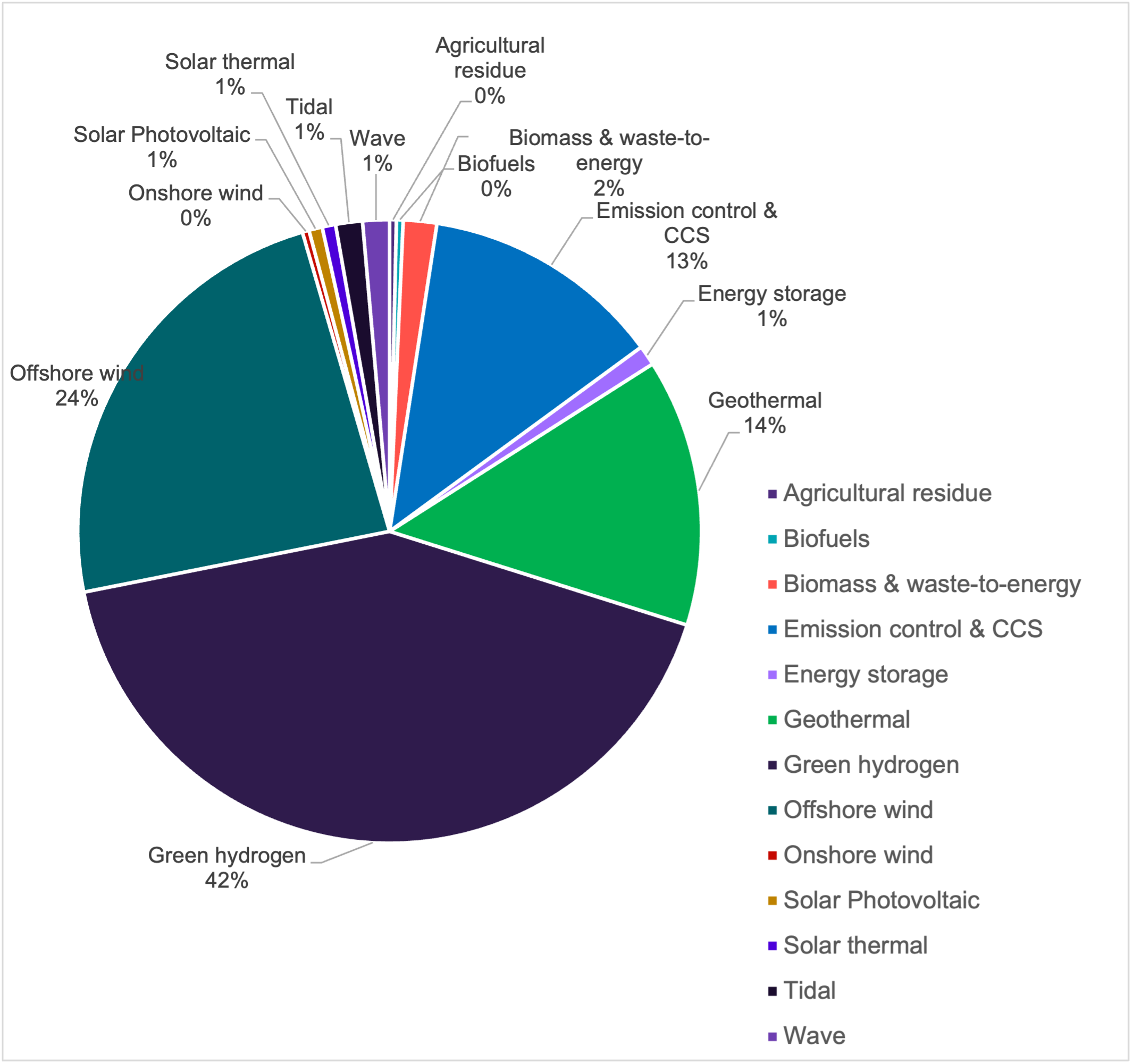

Data from the Clean Energy Pipeline shows there are currently 290 green energy projects in the pipeline across the US (either under construction or pre construction; excluding projects suspended and already in operation) with capacity ranging from under 10 MW to over 4000 MW. Green hydrogen and offshore wind account for the greatest shares of these projects (Figure 2). However, of the 123 green hydrogen projects, only 9 of these are ‘under construction’ leaving some uncertainty over the remaining projects that are yet to start. Geothermal figures appear a bit more hopeful – of the 58 projects, roughly a quarter are under-construction. Nevada and California account for the greatest share of those projects. For offshore wind, while 79 projects are in the pre-construction phase, only 9 are under construction and some of these have faced challenges with stop-work orders and funding being pulled. For example, Revolution Wind (Rhode Island), Sunrise Wind (New York), Vinyard Wind 1 (Massachusetts), Empire Wind 1 (New York) and Coastal Virginia (Virginia) are all under stop-work orders (as of December 2025). This is impacting the major developers including Iberdrola, Orsted, Equinor and Avangrid, prompting some to take legal action against the US Government in Jan 2026.

Source: Clean Energy Pipeline (2025)

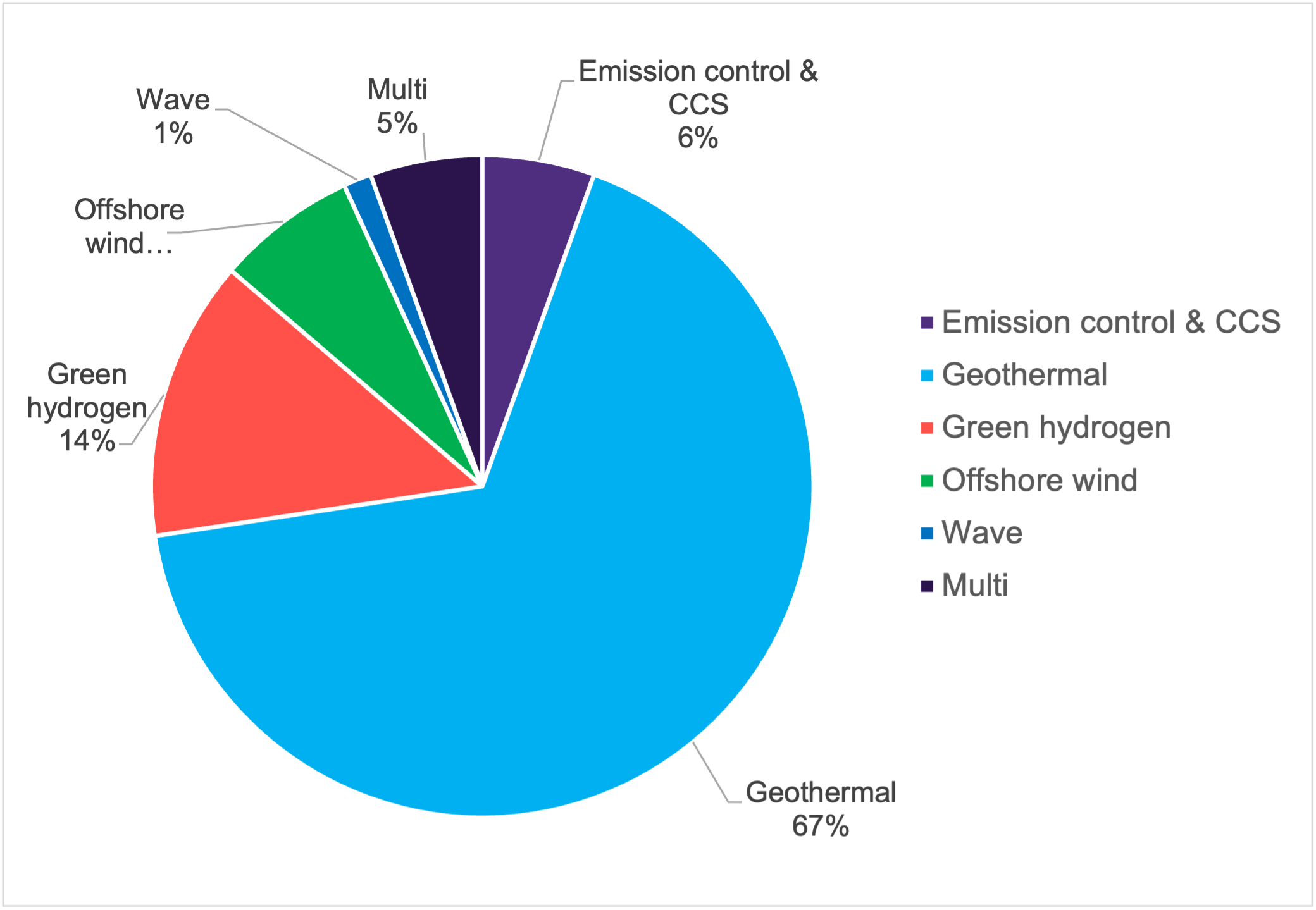

In terms of projects that are in operation (Figure 3), the vast majority of these are geothermal (67%) with a combined capacity of 3029 MW. The majority of these (82%) are located within California and Nevada. Whilst green hydrogen accounts for the second highest share of projects, this only represents 10 projects, with capacity ranging from 1 MW up to 40 MW (for where capacity data is available). The majority of these are located in Texas and California. For offshore wind projects, the pipeline dataset shows just 5 in operation with capacity ranging between 12MW and 200MW. States with offshore wind farms in operation include New York, Rhode Island, Virginia and Maine.

Source: Clean Energy Pipeline (2025)

Although uncertainty persists around individual projects, it is clear that US electricity demand will continue to rise, intensifying the need to scale up generation capacity. This scale of transformation presents an opportunity for Scottish exporters of renewable technologies, grid solutions, and engineering expertise to contribute to the US energy transition. For many Scottish companies, the most effective strategy is not to enter the US market directly but to engage through large global original equipment manufacturers (OEMs) that already have established supply chains, regulatory experience and customer relationships in the US. Partnering with or supplying into these major OEMs allows Scottish firms to scale more quickly, reduce market‑entry risk, and align themselves with projects that already have momentum. This indirect route also helps smaller or scaling exporters manage the complexities of US procurement, compliance, and localisation requirements, while still benefiting from growing demand driven by the US energy transition. Third party engagement is also relevant for some Scottish exporters where partners or competitors in other countries benefit from favourable trade arrangements, such as the exemptions and reduced tariffs for Canada and Mexico. The evolving tariff position for different countries has a critical bearing on competitiveness.

Contact

Email: William.Gray@gov.scot