Scotland's Migration Service: early insights evaluation

This report presents the findings from an early‑insights evaluation of Scotland’s Migration Service, which will inform future policy development and provide further recommendations.

6. EQ3: To what extent does SMS deliver value for money?

While the service has evolved over time, since the launch of the full service in November 2024, the service supports the economic activity of migrants, employers and investors, specifically:

- Pre-movers considering relocation to Scotland for work or family reasons, seeking guidance on visa options and immigration procedures;

- Post-movers requiring support with visa extensions, renewals and changes to immigration rules;

- Employers addressing skill shortages and seeking advice on hiring or retaining international workers;

- Investors exploring immigration pathways to establish or expand operations in Scotland.

The operating model is described in detail in Chapter 2. For this indicative Value for Money assessment, we draw on survey responses from migrants and employers to quantify the employment supported by SMS. We then apply assumptions about average migrant salaries to calculate an indicative gross value added (GVA) to the economy from employment income based on available evidence. Finally, we compare this estimate of benefit to the service’s costs to date to produce an illustrative benefit-to-cost ratio, where a ratio of 1.0 or above indicates that the service may be delivering value for money.

We do not consider the impact of displacement of domestic workers in this analysis. However, we judge the risk of displacement to be low, as evidence suggests that employers are primarily employing migrant labour to address skill shortages.[43]

We do not quantify economic spillovers or investor impacts due to insufficient data but note this as a significant potential upside factor. We also do not quantify or monetise the social benefits arising from SMS service provision, though future analysis could consider these as part of a more comprehensive evaluation. We explore the data limitations in Chapter 3 of this report.

Migrant, employer and investor use of SMS

As described in this report, the service provides two tiers of support to migrants: a digital platform providing up-to-date and accurate immigration information, and a one-to-one service delivered by Citizens Advice Scotland providing more tailored support. Employers and investors can access three tiers of support: information on a digital platform, one-to-many resources including webinars, and one-to-one appointments delivered by Seraphus.

Users engaged with the service for employment-related support across the digital platform, webinar and one-to-one service offerings.

Digital platform engagement

- Migrants: Between April 2024 and August 2025 there were 208,262 views of the SMS webpages dedicated to visa and immigration, an average of 12,251 views per month.

- Employers and investors: From October 2024 to August 2025, the Skilled Workers Visa section of the employer and investment website received 8,871 views, an average of 887 views per month. The majority of views were from UK IP addresses.

Webinar engagement

- From June 2024 to August 2025, 749 employers and investors attended the webinar service run by Seraphus. There was on average one webinar a month covering topics such as sponsorship, overseas companies expanding to Scotland, and the e-Visa system overview. The most well-attended webinars focused on the Sponsor Management System (61 attendees) and Sponsor license compliance (57 attendees). All webinar attendees were satisfied with the service provided.

One-to-one service engagement

- Migrants: 753 people attended one-to-one service appointments between April 2024 and August 2025. The most common age bracket was 25-34, the majority were female and 79% were post-movers. While migrant use of the service was often multi-faceted, analysis of user data indicates that around half of the 753 people supported had appointments regarding employment-related issues such as worker visa access, switching and renewal.

- Employers and investors: Of 111 service users between April 2024 and August 2025, 82 were employers and 29 were investors. The most common category for employers was the information and communication sector (including individuals working in IT and telecommunications) with professional, scientific and technical sector (including those working in law, accounting, research and development) second. The majority of investors were based in Scotland and the US.

The service impact is explored in more detail in Chapter 5 of this report.

Economic Activity Supported

Migrant employment supported

While direct data on employment outcomes is not available, follow-up survey responses for one-to-one appointments provide partial insight into users’ perceived success. Of the 24 migrant respondents, 18 (75%) reported that their needs were completely met. ‘Needs met’ reflects users’ perceptions of whether the advice helped them and does not directly confirm employment outcomes. Because ‘needs met’ does not distinguish between types of support received, this proxy may both understate some employment outcomes and also capture some outcomes that are unrelated to employment. It is therefore used in this analysis as an indicative proxy in the absence of direct outcome data. Given the low response rate (24 out of 753 migrant service users, around 3%), this proxy does not provide a robust estimate of total employment outcomes and is likely to understate the number of positive employment outcomes. However, because around half of migrant service use related to employment, these responses provide an indicative signal of the potential scale of employment-related support delivered.

Employer and investor economic activity supported

Of 82 employers who used SMS, 29 responded to the follow-up survey (35%). Of those, 28 (97%) reported that their needs were completely met. In the absence of systematic data on hires and retention, we make the conservative assumption that each employer whose needs were completely met may have recruited or retained one migrant worker. If the 97% success rate observed amongst the survey respondents applies to all 82 employers then 79 employers may have been supported to employ at least one migrant.

Of 29 investors who used SMS, eight responded to the immediate follow-up survey, a response rate of 28%. All eight respondents to the survey said that their needs were completely met by the service. Additionally, one investor reported in a feedback form 3 months after their appointment that SMS supported them to register a business in Scotland. If the service can support investment in the Scottish economy this a potential source of high value-added to the economy. To enable inclusion in future evaluations, service providers should aim to gather comprehensive data on investment outcomes, as outlined below.

Total migrant employment supported

Our analysis focuses on users who accessed one-to-one advice, as we lack comparable feedback for website or webinar users. It should be noted that digital platform and webinar use may be delivering value that is currently not being captured.

Data from follow-up surveys of one-to-one appointments suggests that SMS may have supported the employment of at least 18 migrants and that 28 employers may have been supported to employ or retain at least one migrant worker, a combined contribution of 46 migrant employment outcomes. These should be interpreted as indicative rather than confirmed employment results, as this analysis relies on self‑reported ‘needs completely met’ responses as a proxy for successful employment outcome.

The true employment supported figure is likely higher due to very low survey response rates. If we apply the respondent success rates to the total employment-related user base, then 282 migrant employees may have been supported and 79 employers may have been supported to employ at least one migrant, a total of 362 employment outcomes.

However, caution is needed: because of the low number of respondents, the success rates from the sample may not accurately represent the average success rate of all employment-related appointments. It is also possible that some migrants and employers may have had success without the existence of SMS, and a successful outcome cannot be solely contributed to the existence of SMS, though this is not possible to determine from the data. The limitations of the data are discussed in further detail in Chapter 3 of this report.

Value added by supported migrant employment

In the absence of data relating to the salary of service users, we tested some average salary assumptions to estimate the overall GVA contribution of the employment income supported by the service.

To inform the average salary assumption for our value for money evaluation, we considered the minimum salary thresholds for the most popular worker visa types. Migrants can obtain several types of worker visa including the Skilled Worker visa, the Health and Care Worker Visa and others.[1] Home Office Data for the UK shows that in the year to June 2025 there were 287,000 work visas granted, of which 172,000 were core ‘Worker’ visas, including 83,000 Skilled Worker visas and 62,000 Health and Care worker visas.[2]

The minimum salary threshold for the Skilled Worker visa has evolved over time. From April 2024 to June 2025 the minimum salary threshold for the Skilled Worker Visa was £38,700 or the job’s ‘going rate’, whichever was higher. This increased to £41,700 in July 2025.[3]

The Health and Care visa has a minimum salary threshold of £25,000, however some jobs need to be earning at least £31,300.[4]

If the 46 migrant employees we base our analysis on earned the updated minimum salary threshold for the Skilled Worker visa of £41,700, then the estimated GVA contribution is £1.9 million. Meanwhile, if the average migrant was employed on the minimum Health and Care worker visa salary of £25,000, then the GVA contribution is £1.1 million.

In reality, the migrant employees would likely have an average salary above the minimum thresholds for visa eligibility and this analysis is a conservative illustrative estimate of the GVA that could have been added to the economy based on returned surveys asking if needs were met by the service. To make a future evaluation more robust, in addition to data on employment outcomes, service providers should aim to gather data on the visa type and salary of those employed, and the degree to which the service facilitated those outcomes.

Costs

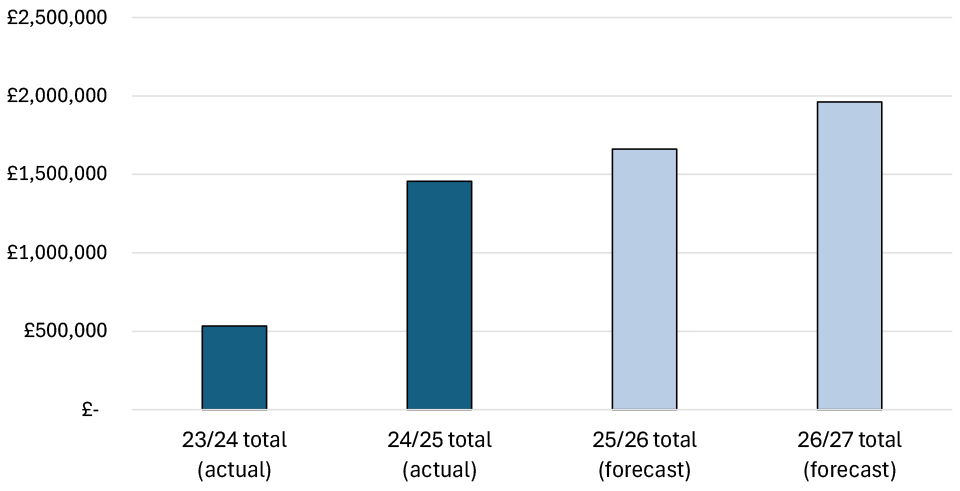

The service is estimated to have cost £2.3 million to set up and run so far. These costs are split into programme costs, which relate mostly to contracts with the operational suppliers and digital supplier, and staff costs for Scottish Government personnel working full-time on Scotland’s Migration Service.

Costs rose in 2024/25, coinciding with the full rollout of the service in November 2024, as delivery scaled up.

Costs are forecast to increase further in 2025/26 and 2026/27, but at a decreasing rate, reflecting the transition from initial setup and expansion toward ongoing delivery and continuous improvement.

| Financial year | Amount (£ thousands) |

|---|---|

| Programme 23/24 (actuals) | 319 |

| Staff 23/24 (actuals) | 214 |

| 23/24 total (actual) | 533 |

| Programme 24/25 (actuals) | 997 |

| Staff 24/25 (actuals) | 459 |

| 24/25 total (actual) | 1,456 |

| 25/26 total (to date) | 267 |

| Total (to date) | 2,256 |

| Programme 25/26 (forecast) | 1,277 |

| Staff 25/26 (forecast) | 383 |

| 25/26 total (forecast) | 1,769 |

| Programme 26/27 (forecast) | 1,463 |

| Staff 26/27 (forecast) | 498 |

| 26/27 total (forecast) | 1,962 |

| Total (actual and forecast)[5] | 5,612 |

Indicative Value for money analysis

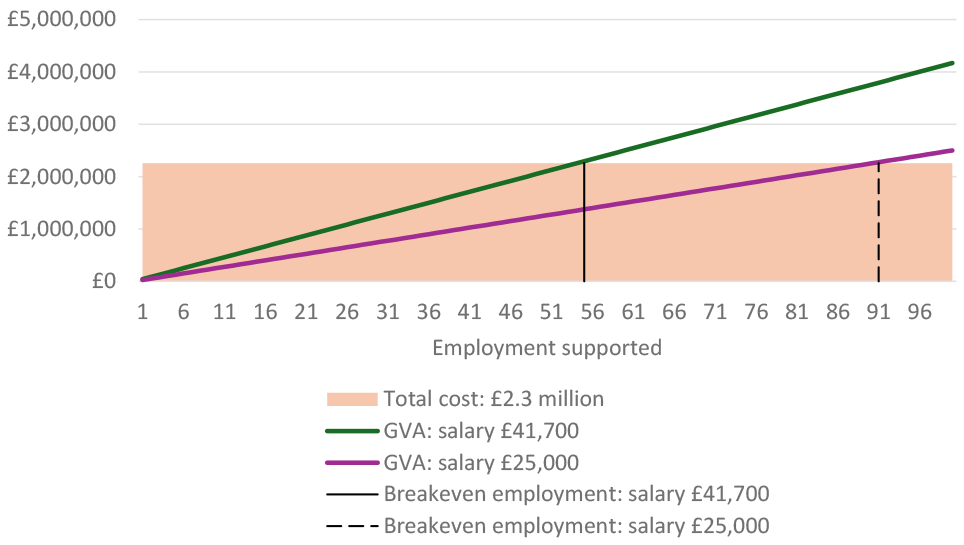

An initial assessment of value for money of the service can be made by comparing the illustrative estimates of the GVA to the economy from employment income, compared to the cost to date of £2.3 million. Assuming an average salary of £41,700 for the 46 individuals that user survey data indicates were supported in employment then the estimated GVA is £1.9 million and the BCR is 0.85, meaning the GVA contributed by the service covers 85% of the cost. If the average salary was the minimum salary threshold for the Health and Social Care Visa of £25,000 then the estimated GVA is £1.1 million and the BCR is 0.51, meaning the GVA contributed by the service covers 51% of the cost.

Our GVA contribution estimates are based only on employment income, lacking the data needed to quantify the contribution from investment, or wider economic spillovers. We also base our estimate only on migrant and employer survey respondents, and the survey response rate was low (3% for migrants, 35% for employers).

On the basis of outcomes indicated by a proxy measure for successful employment from follow-up surveys only, the estimated benefit-cost ratio (BCR) is below 1.0 (0.51–0.85), implying that the monetised employment benefits captured in the available survey data do not fully offset costs to date. However, our estimate of migrant employment income is highly conservative for two reasons: (i) it applies minimum visa salary thresholds in the absence of salary data; and (ii) it assumes that users who did not respond to follow-up surveys generated no employment outcomes at all. Given the very low migrant response rate in particular, it is plausible that additional employment outcomes occurred but were not captured in the survey data, which would increase the BCR. Due to lack of data, we also omit potentially high-value investment and there are also a number of potential non-monetised benefits; these are highlighted in more detail below.

Sensitivity analysis shows that under this modelling framework, to break even at a salary of £41,700 the service would need to have supported the employment of 55 individuals, while at a salary of £25,000 the service would need to have supported the employment of 91 individuals. Meanwhile, assuming that the employment of 46 migrants employees was supported, for the service to be associated with a benefit-cost ratio of at least 1.0 then the average salary would need to be at least £49,050.

Assuming an average salary of £41,700 then an additional 9 people would need to have been employed because of the service but the migrant or employer did not respond to the follow up survey; this equates to a success rate for employment-related non-respondents of just over 2%. Meanwhile, assuming a lower average salary of £25,000, for the service to break even then an additional 45 people would need to have been employed because of the service but the migrant or employer did not respond to the follow up survey; this equates to a success rate for employment-related non-respondents of just over 11%.

As above, if we apply the service success rates of migrants and employers who responded to the survey to the total employment-related user base then up to 362 employment outcomes may have been supported, resulting in much higher monetised benefits and a larger BCR. We have also assumed only one migrant was supported in employment per employer, while some large employers may have employed multiple migrants. However, caution is needed: because of the low number of respondents, the success rates from the sample may not accurately represent the average success rate of all employment-related appointments. We also do not have the data to assess the additionality of employment supported by the service.

It is also possible that the 46 migrant employees we have based our analysis on could have had the average salary of at least £49,050 needed for the employment income supported by the service to cover its cost.

Furthermore, investment impacts could represent a high-value additional source of economic benefit, but they cannot be quantified with the current data. All eight investor respondents reported that their needs were completely met, and one investor reported registering a business in Scotland following an SMS appointment:

“The consultation brought clarity to my plans and I registered a business in Scotland less than a month after the consultation, and the business is very promising.”

This anecdotal example of potential investment activity provides early indicative evidence of potential investment-related outcomes, but the scale and associated economic impact are unknown and are not included in the monetised VfM estimates presented here.

There are also multiple sources of potential non-monetised social benefits such as improved wellbeing and social inclusion that fall out with the scope of this analysis. In addition to economic outcomes, qualitative evidence suggests SMS may deliver social value. Users reported reduced stress, increased confidence, and improved understanding of immigration processes. These outcomes contribute to wellbeing and social inclusion, which are important components of public value and align with the service’s Theory of Change (see Figure 1). Further detail on social impacts is provided in the Impact Evaluation. Any investment associated with business activity supported by SMS could, on its own, offset the service costs through additional jobs and investment. However, due to limited data, the scale of the investment cannot be quantified, and investment impacts have not been included in this analysis.

Overall, while the available monetised evidence does not demonstrate that monetised benefits of SMS outweigh costs to date, sensitivity analysis indicates that under our modelling framework, only a small number of additional unobserved employment outcomes would be required for break‑even under conservative assumptions. On this basis, and noting that break‑even would require only a 2–11% employment success rate among non‑respondents under conservative assumptions, the analysis suggests that the service may be delivering value for money, subject to the significant data limitations noted. Economic benefits may increase in future years if awareness and uptake grow, although this will depend on user behaviour, external constraints, and the service’s ability to support successful outcomes. To enable a fuller analysis of the value for money of the service, we recommend more comprehensive data collection on employment and investment outcomes from service use, and the degree to which the service facilitated those outcomes.

Limitations and recommendations

The assessment this evaluation is able to make on the service’s indicative value for money is limited by the data available. The analysis is therefore subject to several caveats including:

- Low survey response: Employment impact estimates are based on 61 follow-up survey responses (24 migrants, 29 employers, 8 investors) out of 753 migrants, 82 employers and 29 investors.

- Illustrative assumptions: GVA and BCR calculations assume minimum visa salary thresholds and one migrant per employer. Actual salaries and employment numbers may differ.

- Exclusions: Analysis does not account for social benefits, wider economic spillovers, or displacement effects (judged low risk).

- Additionality: In the absence of data on employment outcomes and the degree to which the service facilitated those outcomes, it is not possible to quantify the additional impact of the service.

- Forecast uncertainty: Cost forecasts for 2025/26 and beyond are indicative and subject to change.

To strengthen future service value-for-money evaluations, it would be valuable for service providers to systematically collect follow-up data from migrants and employers on employment outcomes, earnings, investment and crucially, the role of SMS in facilitating these outcomes.

Specifically, for migrants and employers it would be beneficial to systematically gather data on:

- Employment outcome

- Visa type

- Salary

- Number of migrants employed

- The role of SMS in delivering this outcome

And for investors:

- Investment outcome

- Magnitude of investment

- Number of jobs created

- The role of SMS in delivering this outcome

For KPI 1, in addition to the degree to which user needs were met, it would be beneficial to categorise this by what the need was, so that the success of service provision related to employment and investment can be assessed.

While this evaluation focuses on one-to-one service appointments due to the availability of follow-up data, it is possible that the digital platform and webinar services have also contributed to employment and investment outcomes. These channels reached a large number of users, over 1.4 million migrant website views and 308 webinar attendees, with high engagement and satisfaction rates. Given the relevance of the content (e.g. visa guidance, sponsorship, investment pathways), it is possible that some users acted on this information to make employment or investment decisions.

To better understand and quantify the impact of these service offerings, service providers should issue follow-up surveys for digital and webinar users to determine whether the information provided would support employment or investment decisions and ideally, the nature and number of those outcomes (e.g. jobs secured, businesses registered). Capturing this data would ensure that the contribution of all service components is recognised.

Summary

Throughout its development and delivery, SMS has incurred costs across more than three years. The interim evaluation covers the time period of March 2024-August 2025. However, within that period the full expanded service has only been in place since November 2024. Therefore total SMS costs map disproportionately against the delivery period. While establishing the interim and expanded versions of SMS, upfront costs occurred in line with profiling. Those costs have not been repeated, will not require to be repeated during the remainder of current contracts, and would not require to be repeated if the service was to be re-procured for the period beyond March 2027. Therefore, the overall impact of those areas of expenditure on service cost effectiveness would reduce over time. Thus, building on the positive initial outcomes from the interim and expanded service, in future we would expect to see an increasing net contribution to the Scottish economy.

There are two main channels of potential economic benefits from the scheme. Firstly there is the contribution made by additional employment related outcomes for those supported by the service. Secondly there is the potential impact of additional investment should investors look to locate in Scotland or increase existing investment in Scotland following engaging with the service. Such investments, if leading to the creation of additional employment and/or new capital investment in Scotland have the potential to make a significant contribution in terms of economic benefits.

Indicative value for money modelling was carried out using data from user feedback surveys, to generate illustrative estimates of employment-related economic activity supported by the service. In the absence of data on employment outcomes, this analysis was based upon the proportion of service users who attended advice appointments and indicated in feedback surveys that the service had “completely met” their needs. Using the limited evidence available, this illustrative analysis indicated that between April 2024 and August 2025, the estimated benefit-cost ratio of the service was below break even. However, relatively small numbers of additional unobserved employment outcomes would have been sufficient for SMS to break even under the conservative modelling framework employed.

This finding should be treated as a conservative estimate for a number of reasons. Firstly, analysis was based upon data from a small number of user surveys, and did not consider the outcomes of users who did not return a user feedback survey. As such, the potential employment supported as a result of the service may have been understated. Secondly, while SMS provides services to individuals, employers and investors, the timing of the evaluation means that analysis focused on the employment outcomes of individuals completing user feedback surveys. As such, economic benefits specific to employers and investors were not considered as part of this economic analysis. Lastly, this analysis did not account for the wider social benefits of the service (e.g. improved wellbeing of migrants and increased confidence in navigating the immigration system), which also contribute to benefits.

Taken together, these findings suggest the service may be delivering value for money, though this conclusion remains highly uncertain. Looking ahead, the value of SMS may be expected to grow as awareness and uptake increase. Strengthened and more systematic outcome tracking, particularly on employment, earnings, investment outcomes and the role of SMS in facilitating these outcomes, would enable a more robust and conclusive assessment of value for money in future evaluations.

Contact

Email: migrationservice@gov.scot