Digital assets in Scots private law: Consultation - Scottish Government analysis

Analysis of the responses to the public consultation on reform of digital assets in Scots private law, which ran from 27 November 2024 and 5 February 2025.

4. Detailed Analysis

Section 4.1 – Primary Legislation

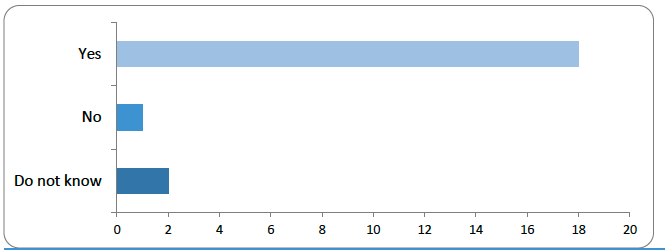

| Option | Total | Percent |

|---|---|---|

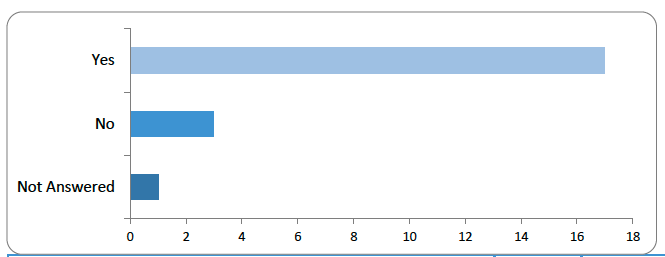

| Yes | 18 | 85.5% |

| No | 1 | 5% |

| Do not know | 2 | 9.5% |

The vast majority (85.5%) of respondents agreed that primary legislation offers the most effective means to resolve current legal uncertainty regarding the status of digital assets in Scots private law. Those in favour emphasised that a definitive legal framework could remove doubt and that to rely solely on the development of case law is likely to be too slow. Legislative intervention would be quicker than waiting for cases seeking judicial authority.

They also highlighted that clear legislation could keep Scotland competitive in digital asset innovation and provide a basis for defining which digital assets are recognised as property. Among the small minority who either disagreed or did not know, no reasons were given to explain their position. One respondent did add that a hybrid approach, combining legislation with regulatory authority, would help to prevent obsolescence as technology evolves.

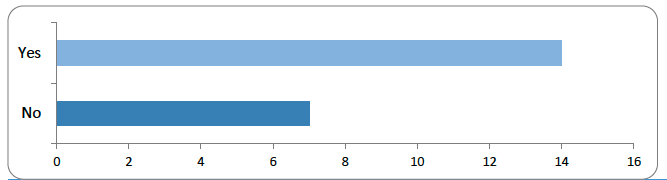

| Option | Total | Percent |

|---|---|---|

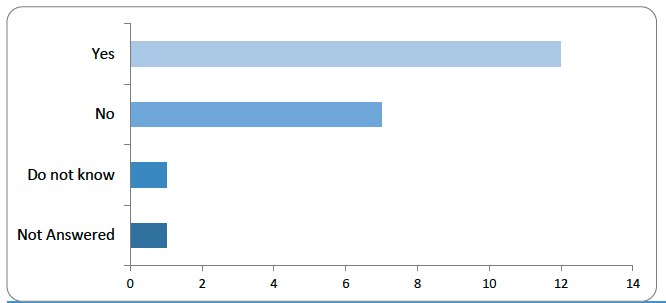

| Yes | 14 | 66.5% |

| No | 7 | 33.5% |

The majority (66.5%) of respondents supported a focused statutory approach to provide clarity, with ‘light-touch’ legislation to mitigate against the risk of stifling innovation. Some respondents cautioned that overly prescriptive legislation could quickly become obsolete, while others raised the importance of including direction on matters like involuntary transfers.

Supporters of a narrow scope did suggest that any future Scottish legislation may need more detail than legislation being progressed for the rest of the UK[2], given a lack of comparable case law in Scotland. Those responding “No” believed any possible future legislation should have a broader scope, including cross-border rules, insolvency and taxation provisions. The scope of the reservations of fiscal, economic and monetary policy and of insolvency under the Scotland Act 1998 are such that the Scottish Government would not seek to make provision concerning either insolvency or taxation in any possible future legislation in relation to digital assets, to avoid encroaching upon either reservation.

There were some concerns around all types of digital assets being within the same category: for example, one respondent raised whether legal recognition should be granted to all types of digital asset, given the potential environmental impact of some blockchain-based assets. Another respondent held the view that recognising assets such as voluntary carbon credits as property could have unintended environmental and regulatory consequences.

Section 4.2 - Classification Of Digital Assets As Property

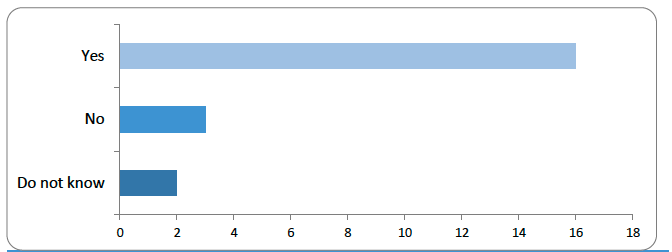

| Option | Total | Percent |

|---|---|---|

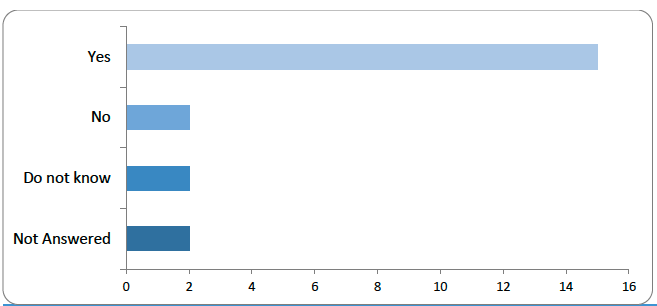

| Yes | 16 | 76% |

| No | 3 | 14.5% |

| Do not know | 2 | 9.5% |

A significant majority (76%) of respondents supported classifying digital assets as incorporeal moveable property, with many persuaded that their intangible nature fits most naturally under this category. Others noted that classifying digital assets as incorporeal moveable property would not fully resolve more practical issues but viewed it as a good first step with respect to their legal status.

By contrast, the Faculty of Advocates held the view that rivalrous, independently existing digital assets could be defined as “digital corporeals” by analogy to physical objects, with their use and treatment being more aligned to traditional corporeal moveable property.

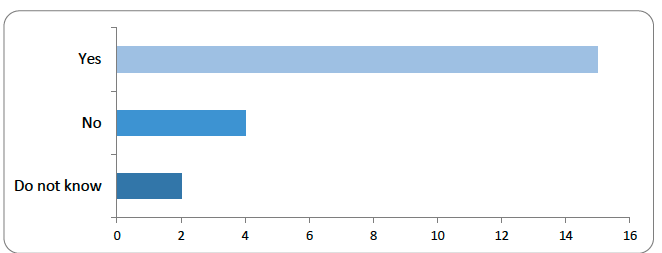

| Option | Total | Percent |

|---|---|---|

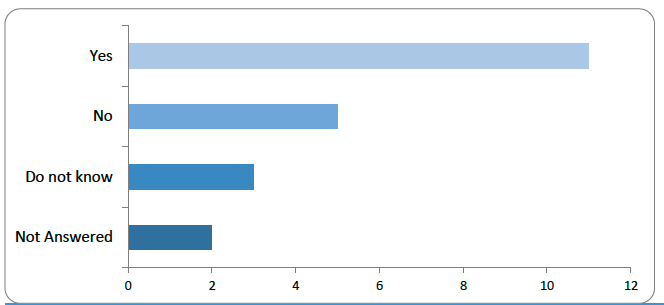

| Yes | 15 | 71.5% |

| No | 4 | 19% |

| Do not know | 2 | 9.5% |

A technology neutral approach was favoured by more than two thirds of respondents, as the preferred approach to help future-proof the law and mitigate against any legislation becoming out-paced by technological advancements.

One respondent did highlight that it could be helpful for any definition of a qualifying digital asset to exclude certain digital things, such as email addresses and social media accounts from being classified as property under Scots private law.

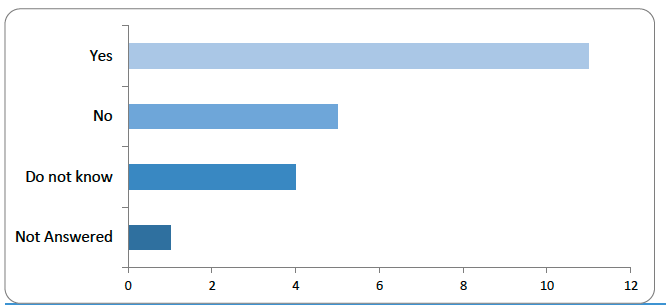

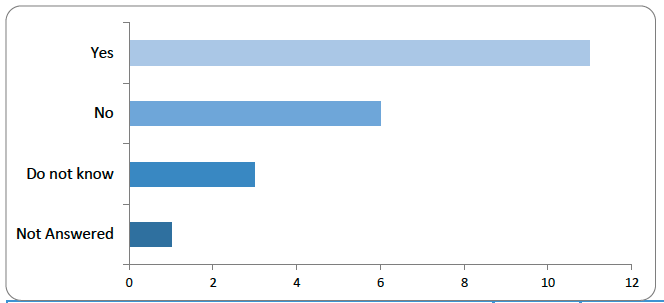

| Option | Total | Percent |

|---|---|---|

| Yes | 11 | 52.5% |

| No | 5 | 24% |

| Do not know | 4 | 19% |

| Not Answered | 1 | 4.5% |

Just over half of respondents endorsed “independent existence” as a criterion to define digital assets for the purposes of any possible future legislation, believing it to offer a clear basis for distinguishing digital assets from purely contractual rights. The technical legal considerations underpinning this question may help to explain why we observed a 19% ‘Do Not Know’ rate from respondents.

Of those who disagreed, respondents flagged potential definitional challenges, especially for assets tied on centralised systems, and questioned whether they remain truly ‘independent.’ A smaller number of respondents stressed that simply existing independently does not automatically make something property, highlighting the need for further clarification.

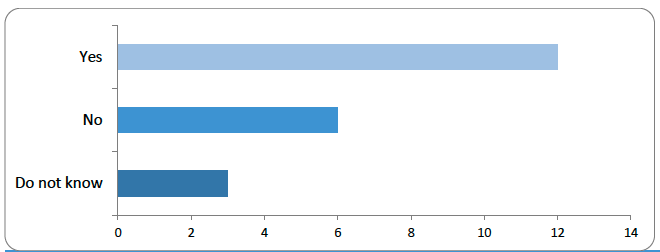

| Option | Total | Percent |

|---|---|---|

| Yes | 12 | 57.% |

| No | 6 | 28.5% |

| Do not know | 3 | 14.5% |

Most respondents agreed that digital assets should be defined with reference to being rivalrous in nature. Some respondents recognised that the emphasis on independent existence and rivalrousness as defining criteria would align with the findings of a report from the Law Commission of England and Wales[3], when considering this issue. Others noted this criterion would help to distinguish digital assets from pure data and other types of digital resources that are non-exclusive as these can be replicated, such as digital files and photographs.

Those with a contrary view questioned the need for rivalrousness to be a prerequisite when non-rivalrous digital assets, such as tokenised streaming rights, also hold value. A dual framework was also proposed by a respondent to classify both rivalrous and non-rivalrous digital assets.

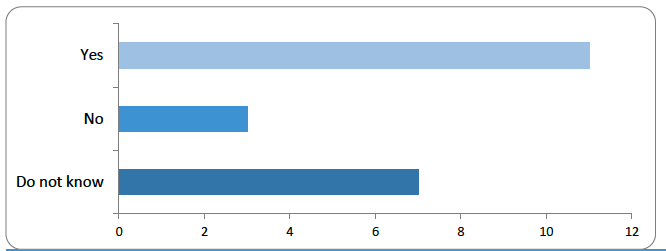

| Option | Total | Percent |

|---|---|---|

| Yes | 11 | 52.5% |

| No | 3 | 14.5% |

| Do not know | 7 | 33.5% |

Just over half of respondents (52.5%) agreed that ‘digital assets’ is the most appropriate term, given its widespread use and recognition, although it is worth noting that one third of respondents answered “Do not know” here. Of those who stated ‘Do Not Know’ one respondent was of the view that the term being used did not matter.

Some respondents highlighted that not everything digital necessarily qualifies as an asset, but no strong opposition emerged to using ‘digital assets’ in possible future legislation. One respondent suggested subclassifications for Non-Fungible Tokens (NFTs) and security tokens to enable the law to better capture the diversity of digital assets, rather than using one legal term as a catch-all.

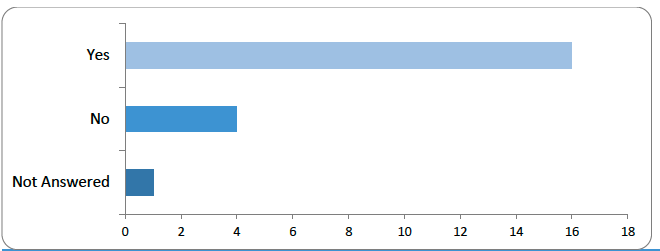

Section 4.3 - Ownership Of Digital Assets

| Option | Total | Percent |

|---|---|---|

| Yes | 16 | 76% |

| No | 4 | 19% |

| Not Answered | 1 | 5% |

A strong majority of respondents (76%) favoured control as the basis for establishing ownership, while acknowledging there may be complexities posed by multi-signature wallets and automated smart contracts. One respondent said that this approach aligns with blockchain and cryptographic security mechanisms. Several respondents highlighted that stolen or hacked digital assets should not grant true ownership rights.

| Option | Total | Percent |

|---|---|---|

| Yes | 17 | 81% |

| No | 3 | 14.5% |

| Not Answered | 1 | 5% |

Most respondents (81%) favoured the dual requirement for the voluntary transfer of ownership, recognising that this would mirror processes for corporeal moveables. Some noted that purely self-executing smart contracts may automatically transfer possession without a distinct instance of delivery each time and so would not create the fresh instance of transfer that Scots law traditionally requires.

The Investment Association commented that regard should be had to market practices, and that possible future legislation should reflect these practices, for example, it should be recognised that transfers of ownership can also happen through contractual terms, such as when an investor fails to pay within a certain period and the fund manager has the contractual right to redeem or transfer the investor’s share.

| Option | Total | Percent |

|---|---|---|

| Yes | 12 | 57% |

| No | 7 | 33.5% |

| Do not know | 1 | 5% |

| Not Answered | 1 | 5% |

A majority of respondents (57%) agreed with this proposal. Those not supportive of this proposal stated that granting ownership in these circumstances would undermine the established nemo plus principle in property law. The Faculty of Advocates expressed caution about deviating from the nemo plus principle, stating: “the nemo plus principle and the vitium reale must be the primary position, consistent with Scots property law generally.” However, the Faculty acknowledged that the question of who should be protected in a transaction - the true owner or the good faith acquirer - is a matter of policy. The policy decision may require a departure from the general legal rule. This principle means that, under Scots property law, a person cannot transfer a greater right to another person than they themselves possess.

Legal academics from the University of Aberdeen stated although the proposition set out in question 10 is a departure from the standard position in Scots property law, given the pseudonymous nature of digital assets, the methods and potential ease of transferring digital assets, as well as pragmatic considerations around making the relevant systems work effectively, they support this proposed departure from the nemo plus principle.

Some respondents suggested a limited exception for good faith acquirers for value, such as applying it to cryptocurrencies but not to all digital assets.

Respondents including the University of Aberdeen legal academics drew an explicit analogy between digital assets and cash (and certain negotiable instruments), where the traditional nemo plus rule does not apply and a good-faith purchaser can obtain ownership from a non-owner, as noted in their response.

Responses were narrowly in favour of recognising good-faith acquisition for value, with those in favour emphasising the importance of treating digital assets like cash to protect bona fide purchasers.

Section 4.4 - Preservation Of General Principles

| Option | Total | Percent |

|---|---|---|

| Yes | 15 | 71.5% |

| No | 2 | 9.5% |

| Do not know | 2 | 9.5% |

| Not Answered | 2 | 9.5% |

Many respondents (71.5%) agreed that possible future legislation should state that the general principles of Scots private law (such as contract law) continue to apply to digital assets and noted that if digital assets are legally recognised as property, then these principles would naturally extend to them; however, including express provision to this effect in legislation could help eliminate uncertainty in practice. Some respondents viewed this as potentially useful for market confidence but as arguably unnecessary as, if appropriately categorised in legislation, digital assets should automatically be governed by Scots private law principles.

| Option | Total | Percent |

|---|---|---|

| Yes | 11 | 52.5% |

| No | 5 | 24% |

| Do not know | 3 | 14.5% |

| Not Answered | 2 | 9.5% |

Most respondents (52.5%) agreed that digital assets qualifying as property should naturally be eligible to be held on trust. Whilst some suggested that a clarificatory provision could provide reassurance to market participants but is not legally essential.

There were comments raised that including specific statutory provisions for trusts in this area might prompt questions about why similar provisions do not exist in other areas of Scots private law. However, there were comments agreeing with the ERG’s rationale - that clarifying whether digital assets can be held on trust is beneficial to avoid uncertainty that could otherwise hinder custodial and financial arrangements, and that these assets should not be excluded from trust arrangements simply because they are new.

| Option | Total | Percent |

|---|---|---|

| Yes | 11 | 52.5% |

| No | 6 | 28.5% |

| Do not know | 3 | 14.5% |

| Not Answered | 1 | 5% |

Responses marginally favoured including additional provisions (52.5%), with key considerations around ancillary changes for insolvency law and diligence. Some respondents thought that clarity on enforcing court orders or securing digital assets would assist, noting that existing mechanisms (e.g. arrestment) may not be well-suited. One respondent proposed legislative changes to allow digital assets to fall under statutory pledge or another recognised security mechanism. The scope of the insolvency reservation under the Scotland Act 1998 is such that the Scottish Government would not seek to make provision concerning insolvency in any possible future legislation in relation to digital assets, to avoid encroaching upon this reservation.

Several respondents highlighted international and cross-border issues, particularly in relation to taxation and the relevant jurisdiction in which where digital assets are located to help simplify inheritance tax and capital gains tax liabilities, as well as broader corporate and personal taxation. Others identified cross-border enforcement and conflict of law rules as areas worth further consideration. The scope of the reservation of fiscal, economic and monetary policy under the Scotland Act 1998 is such that the Scottish Government would not seek to make provision concerning taxation in any possible future legislation in relation to digital assets, to avoid encroaching upon this reservation.

One respondent proposed establishing an expert group to advise on both legal and technological developments, ensuring that the legislation remains future-proofed and technology-neutral, stating that while a technology-neutral approach offers significant benefits, it may also impact judicial resources. The Law Commission of England and Wales initially envisioned such a group to provide advisory opinions and develop technical standards; however, the UK Government’s Property (Digital Assets etc.) Bill currently does not make explicit provision for such a body, although the UK Jurisdiction Taskforce has partly assumed that role. It was recommended that Scotland create its own expert group, leveraging local legal and computer science expertise from institutions such as DeCaDe and the Input Output Research Hub. It was suggested that such a group could play a crucial role in keeping the legislative framework current by advising on evolving technical standards and by guiding the courts in determining whether a digital asset meets the statutory criteria.

Another respondent advocated for a ban or severe restrictions on crypto-related businesses in Scotland, arguing they have no practical use case. The scope of the reservation in respect of business associations under the Scotland Act 1998 is such that the Scottish Government would not seek to make provision concerning the creation, operation, regulation or dissolution of businesses in any possible future legislation in relation to digital assets, to avoid encroaching upon this reservation.

Some of the consultation responses to question 13 made suggestions which would be outwith devolved competence. The Scottish Government does not intend to make any provision outwith devolved competence in any potential future legislation.

There were also concerns about the environmental impact of digital assets and the need for public registries or standards to identify and manage flagged or stolen assets to combat fraud. While the regulation of financial services and financial markets remains reserved to the UK Government, the Scottish Government continues to monitor regulatory developments to safeguard and promote Scotland's interests. Given that the possible future legislation consulted on is intended primarily to confirm the status of digital assets in Scots private law, it neither encourages nor discourages the use of such assets by businesses or individuals.

Section 4.5 – Roundtable Discussions

To support the online consultation, a series of roundtable discussions took place in Aberdeen, Edinburgh, and London. The purpose of these sessions was to have targeted discussions with a diverse range of stakeholders, including legal professionals, academics, fintech representatives, and government officials and to explore the recommendations in the consultation . The legal roundtable generated an overall positive dialogue, with widespread support for the development of possible new legislation and acknowledged that a lack of case law in this area leaves Scotland at a disadvantage in terms of judicial guidance. Additionally, there was concern that, particularly for tokenised securities, many commercial transactions involving digital assets are occurring offshore or through business arrangements in markets outside of the UK.

From the commercial perspective, there was clear support that for the UK in general and Scotland in particular, to be recognised as a technology hub, it must offer greater legal certainty, with tailored legislation playing a key role in achieving this in Scotland.

In discussions with fintech stakeholders, the group emphasised the importance of formally recognising digital assets as a distinct asset class to build confidence and stimulate greater investment and growth in the sector. They highlighted the significance of tokenisation and the potential for fractional ownership, viewing these developments as having substantial practical and commercial benefits that should be accurately reflected in the law.

The group considered that current UK legal frameworks lag developments in other jurisdictions where there are more rapid legal and regulatory developments to keep pace with technological and commercial progress. Singapore and Dubai were specifically mentioned as examples of forward-looking jurisdictions, while Californian law was expected to increasingly influence arrangements involving blockchain-based digital assets. Developments in Liechtenstein were also raised, given the recent enactment of blockchain-specific legislation addressing challenges like anti-money laundering. The scope of the reservation of money laundering under the Scotland Act 1998 is such that the Scottish Government would not seek to make provision concerning money laundering in any possible future legislation in relation to digital assets, to avoid encroaching upon this reservation.

Questions were raised about the applicable laws for individuals domiciled in Scotland who hold digital assets subject to foreign jurisdictions, and what opportunities exist for Scotland to take a leadership role in this field. The group stressed that, beyond achieving legal clarity, Scotland should also provide other business incentives - such as a favourable tax environment and enhanced consumer protection (however, these are mostly reserved matters and therefore the Scottish Government would not seek to make provision concerning taxation or consumer protection in any possible future legislation in relation to digital assets, to avoid encroaching upon these reservations) - and considered how Scotland could expand its market presence in this area.

Contact

Email: digitalassets@gov.scot