State of the economy: November 2021

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Consumption

Consumer sentiment has strengthened significantly over the past year however patterns of household spending and saving continue to adjust to the removal of restrictions.

The pandemic has had a significant impact on consumer sentiment, reflecting amongst many other factors, the scale of the shock to the economy and the uncertainty it has created for household incomes.

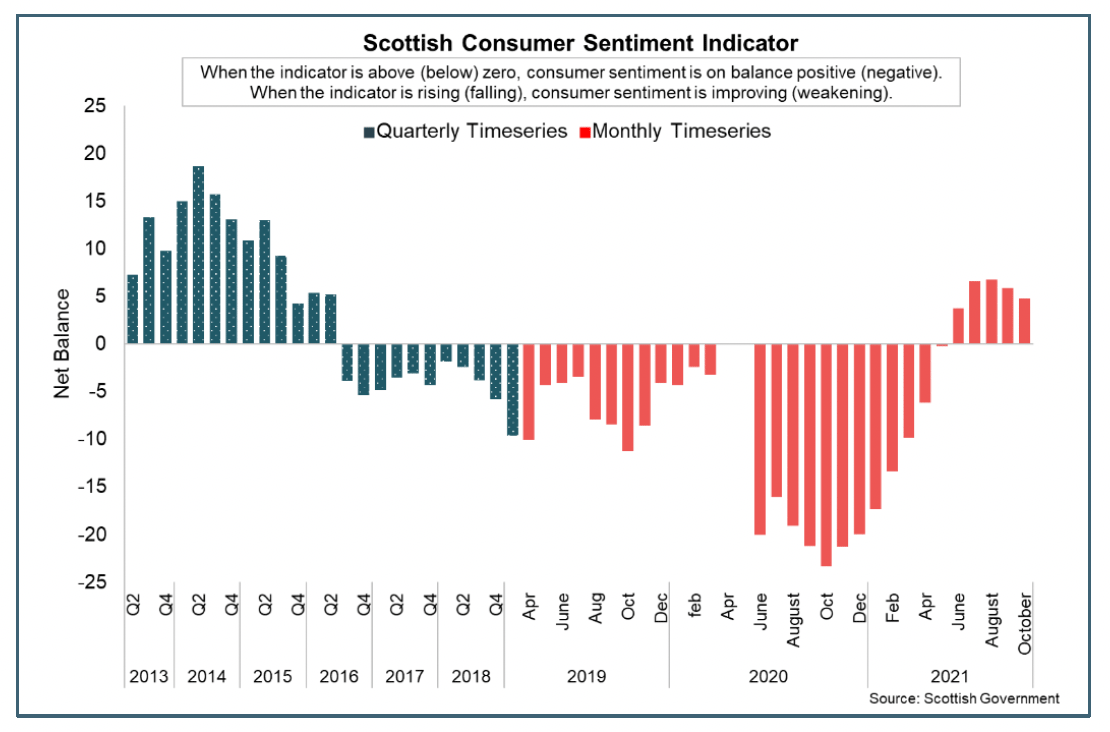

Having fallen sharply during 2020, consumer sentiment has recovered steadily over the past year to back above pre-pandemic levels, likely reflecting improved confidence from the gradual removal of restrictions, delivery of the vaccination programme and the economic recovery that has been underway.

Latest data for October 2021, show the Scottish Consumer Sentiment Indicator stood at 4.8. This was the fifth consecutive month of positive consumer sentiment, however has weakened slightly by 1.1 points from September.[32]

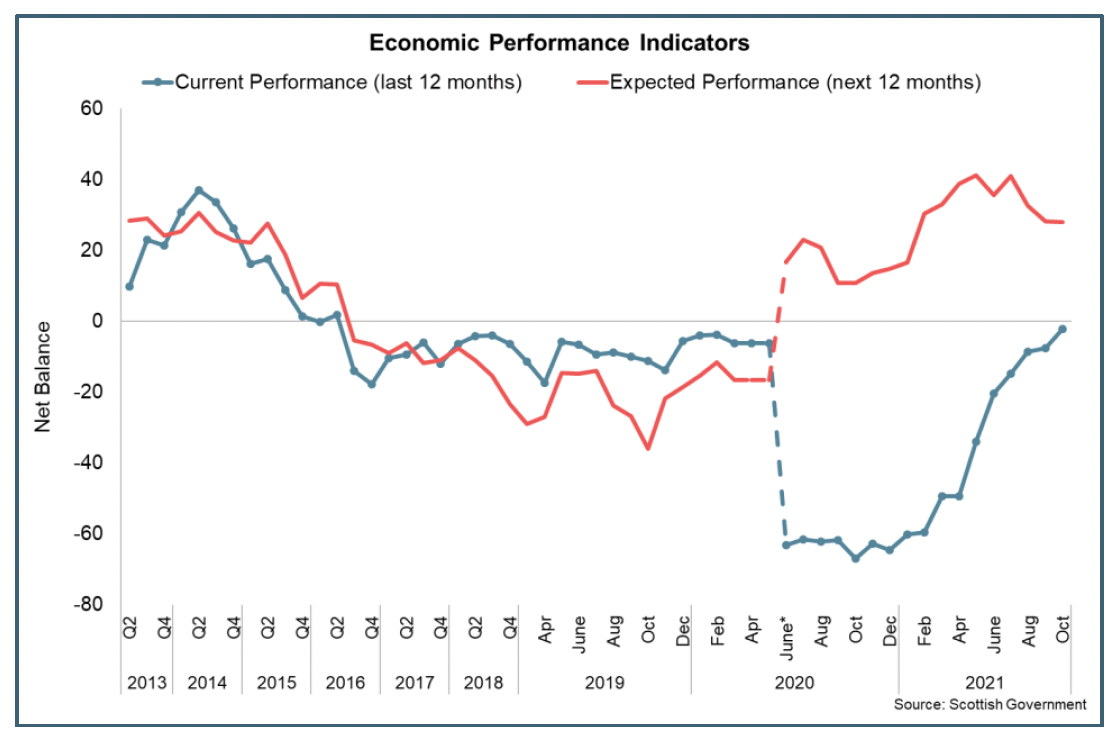

On the economy, respondent's on balance consider current economic circumstances to be slightly worse than last year (-2.2), however sentiment continued to improve. Looking ahead, respondents expect the economy to impove over the coming year relative to the current situation (+28), though the level of optimism has gradually weakened since July.

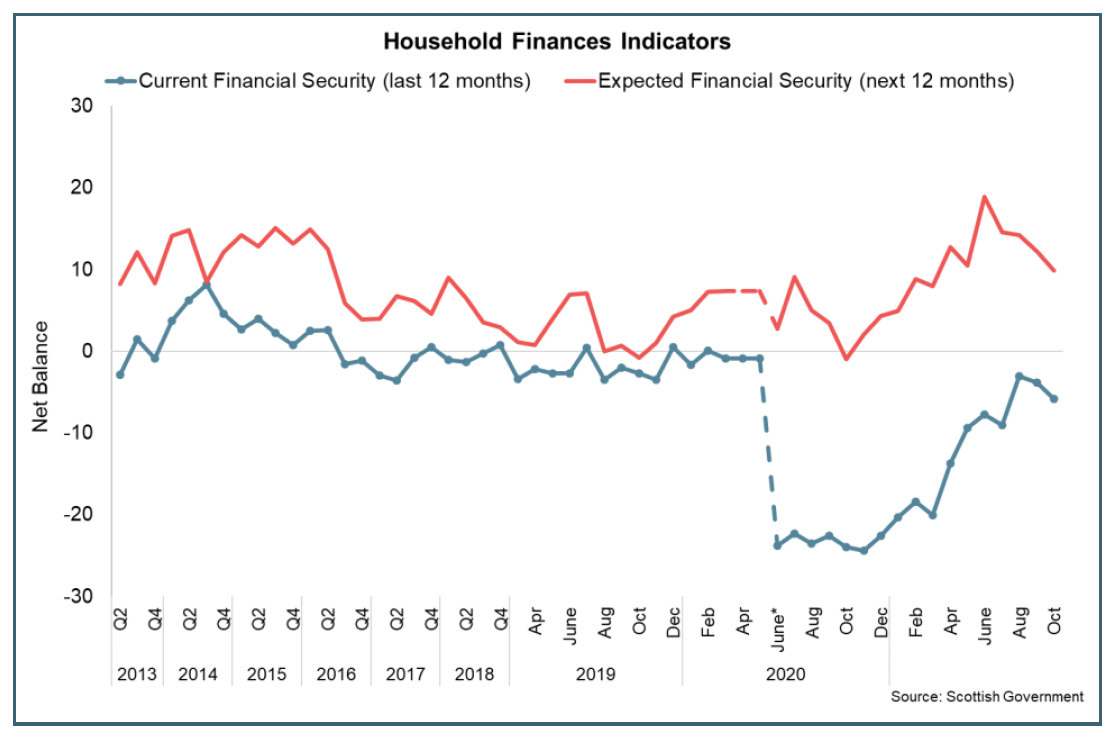

On the issue of sentiment around household finances, households responded that their household finances were less secure than 12 months ago (-5.8), though looking ahead, expect them to strengthen over the coming year (+9.9). However, both indicators have weakened in recent months signalling that uncertainty in this regard remains heightened.

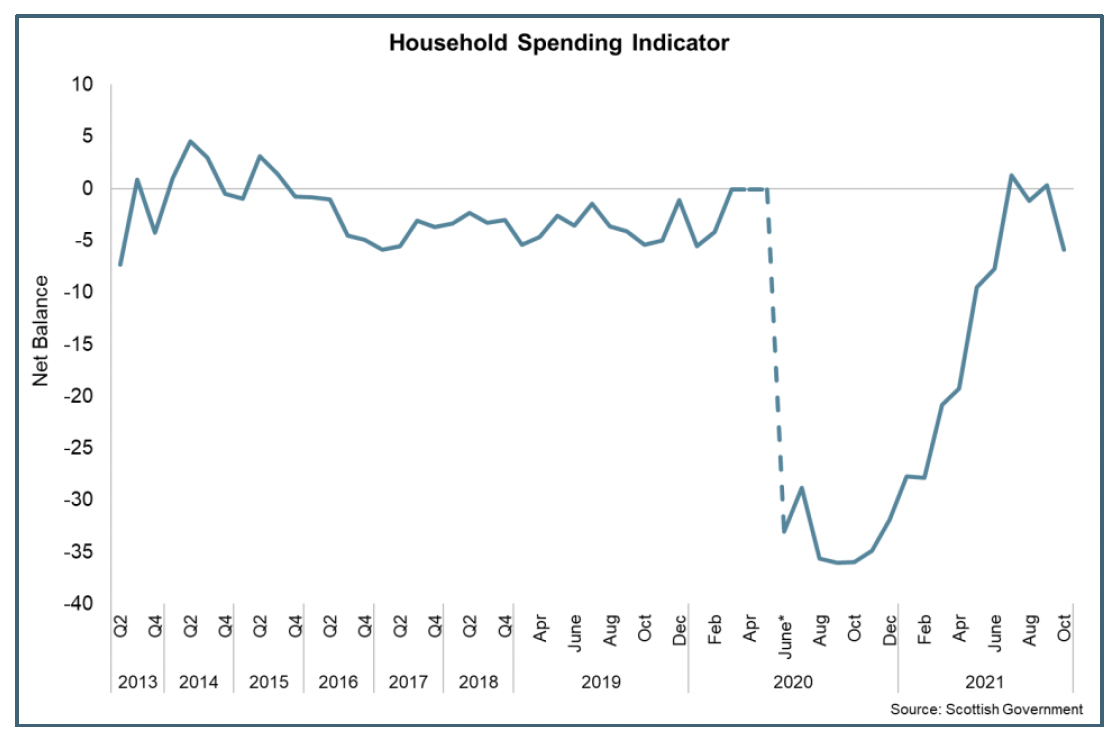

Both the outlook for the economy and household finances influence how relaxed households are about spending money. Households have been increasingly relaxed about spending money over the past year (rising from a low base), however sentiment stabilised over the third quarter before falling in October to a net balance of -5.9. This is in keeping with the recent falls seen in some of the other indicators in October, signalling that respondents confidence about spending money has weakened recently.

Sentiment indicators continue to be highly sensitive to the rapidly moving developments on the pandemic and the unprecedented economic impacts that we have seen. As such, they will continue to be a key indicator in understanding the level to which a recovery in consumer sentiment feeds through to changes in consumption.

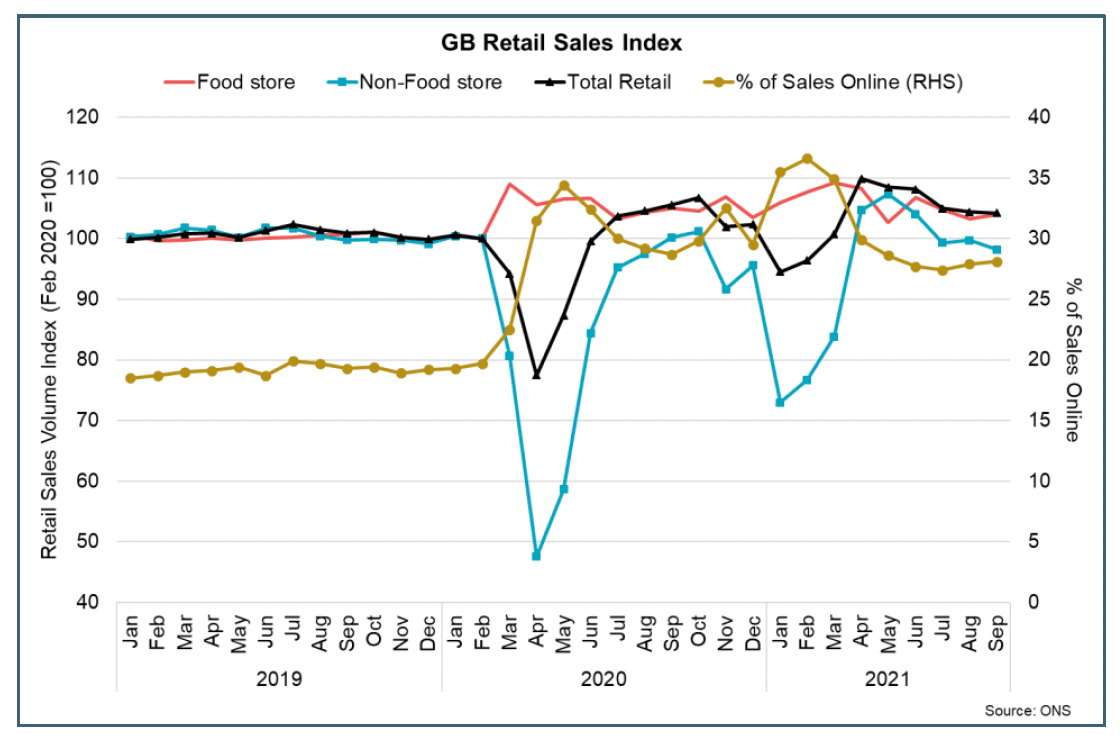

The strengthening in consumer sentiment over the past year has been broadly reflected in strengthening retail sales, which have recovered to 4.2% higher than their pre-pandemic level, having fallen sharply during lockdown restriction periods in 2020 and 2021.[33] However, GB retail sales in September fell 0.2% over the month, following a 0.6% fall in August. Food store sales rose 0.6% and were 3.9% above pre-pandemic levels, while non-food sales fell 1.4%.

The easing back of retail sales in recent months, particularly non-food sales, may reflect a level of displacement in consumer spending as restrictions on consumer facing services further eased enabling increased consumption of consumer services rather than consumer goods.

Furthermore, the split between online retail sales and in-store retail sales has continued to adjust following the removal of restrictions. The proportion of retail sales online increased to 28.1% in September, having been over 35% at the start of the year during lockdown restrictions. While the share of retail sales online has fallen back, it remains substantially higher than in February 2020 prior to the pandemic (19.7%).

Household Savings and Consumer Credit

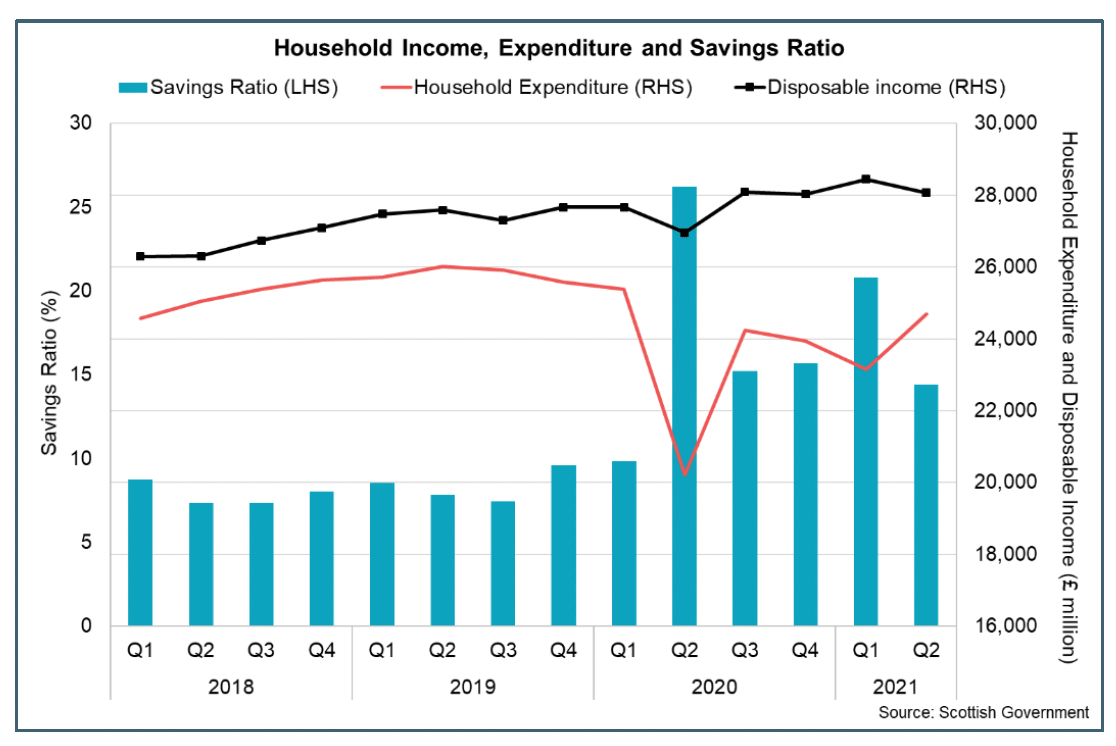

At an aggregate level, households have increased their levels of savings during the pandemic due to a reduction in expenditure coupled with a rise in disposable income through the retention of earnings. This has been particularly evident during periods of lockdown in Q2 2020 and Q1 2021 when consumer facing services were largely closed.

Following these peaks (26% and 21% respectively), the savings ratio fell in Q2 2021 to 14% reflecting that disposable income has remained broadly stable while household expenditure picked up as restrictions eased from the start of the year. This is the lowest rate the savings ratio has been since the start of the pandemic, though remains notably higher than pre-pandemic levels (9.6% in Q4 2019).[34]

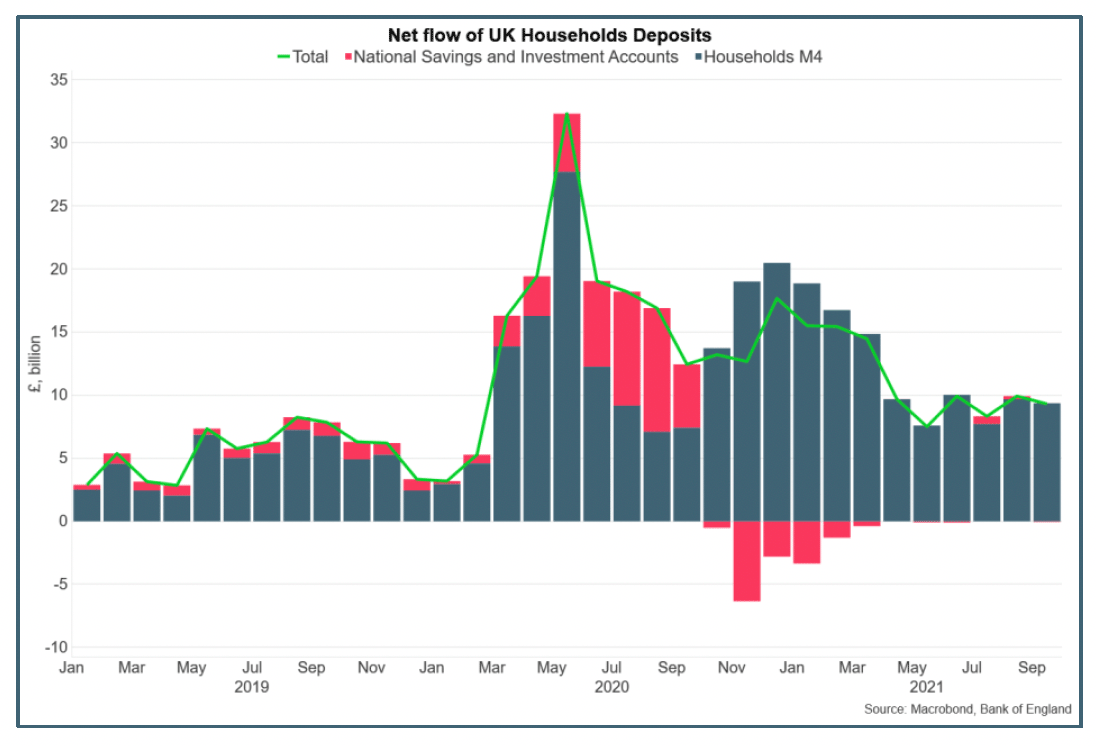

Bank of England data for September provide further insight at a UK level of how household savings have changed over the third quarter of the year.[35] At an aggregate level, net flows from UK households into deposit-like accounts was £9.4 billion in September. Despite monthly variations, net inflows have remained relatively stable over the second and thirds quarters, notably lower than deposits made earlier in the pandemic, however remain around twice as high as pre-pandemic levels when the average net inflow in the year to February 2020 was £4.7 billion.

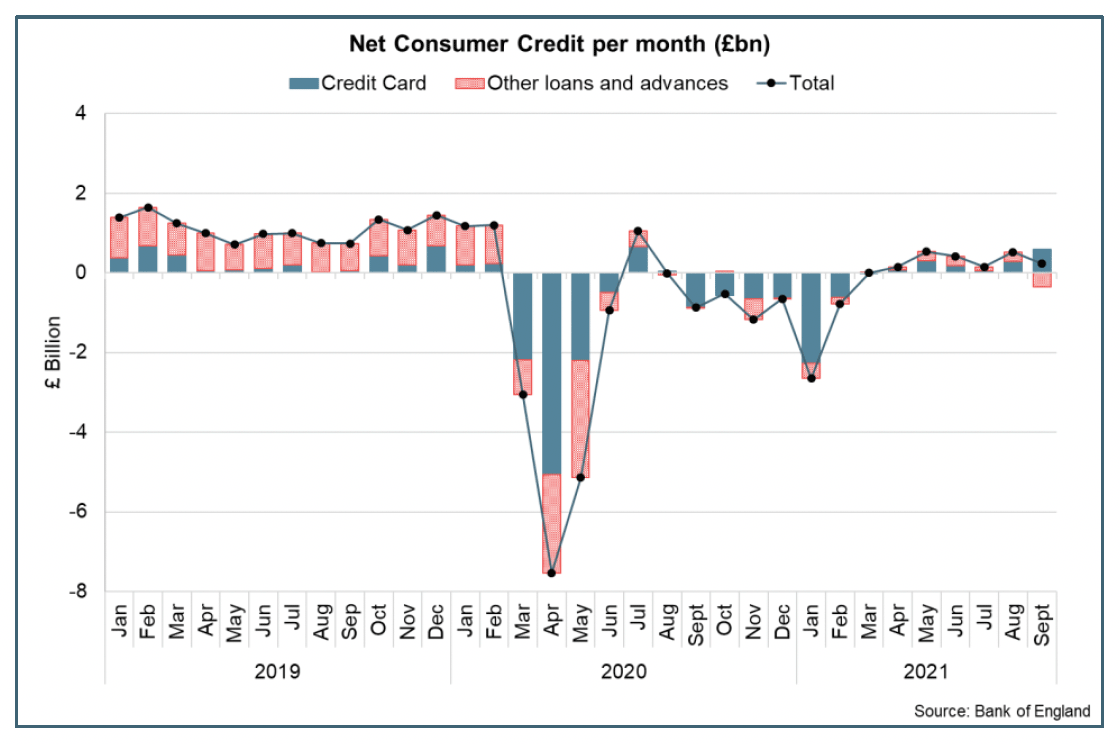

In keeping with higher rates of net deposit flows, net consumer credit has fallen significantly during the pandemic. Consumer credit started to grow again over the second quarter and in September, consumers borrowed £0.2 billion in credit on net. Within this, they borrowed £0.6 billion in credit card debt (the strongest level since July 2020) and repaid £0.4 billion in 'other' forms of consumer credit (such as card dealership finance and personal loans). However, net borrowing remains significantly lower than the pre-pandemic monthly average of £1.1 billion in the year to February 2020.

Looking ahead, the extent and pace at which households retain or spend accumulated savings and further increase borrowing remains uncertain, particularly in the context of the recent rise in consumer prices inflation.

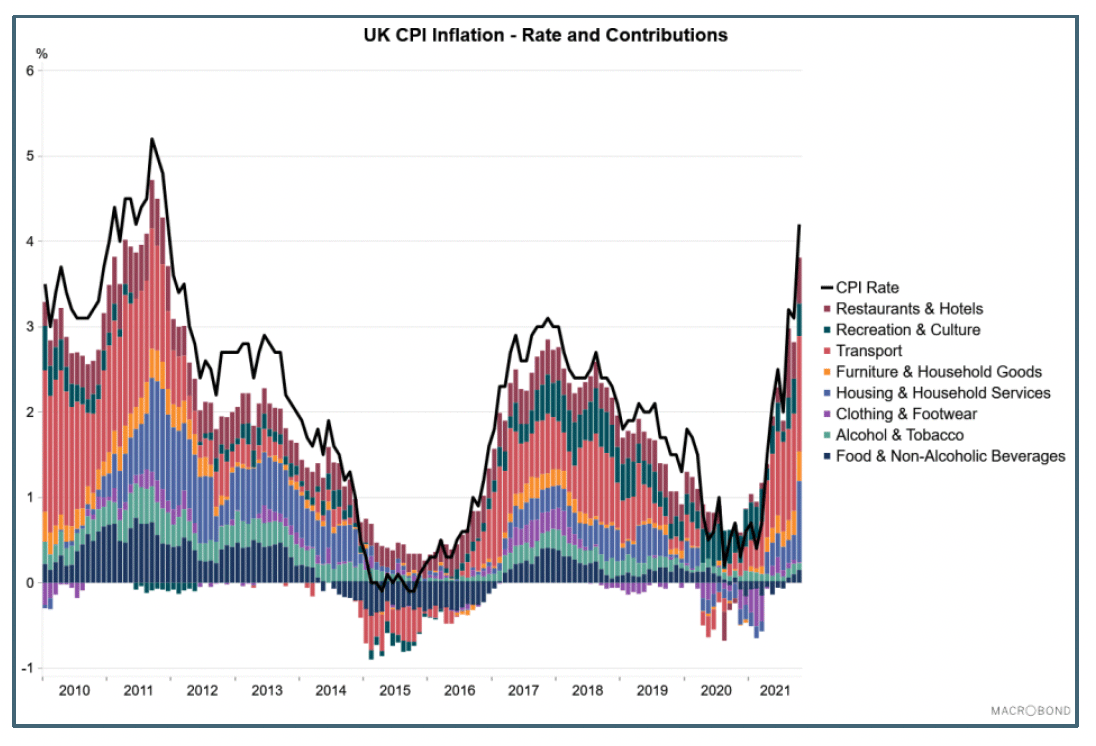

Inflationary pressures have picked up sharply since the start of the year with the CPI inflation rate rising from 0.7% in January to its current rate of 4.2% in September; its highest rate since 2011.[36]

The rate rose from 3.1% in September, with the change driven by broad based positive contributions across all areas and the largest upward contributions from housing and household services, transport and restaurants and hotels.

Box C: Recent Drivers of Inflation

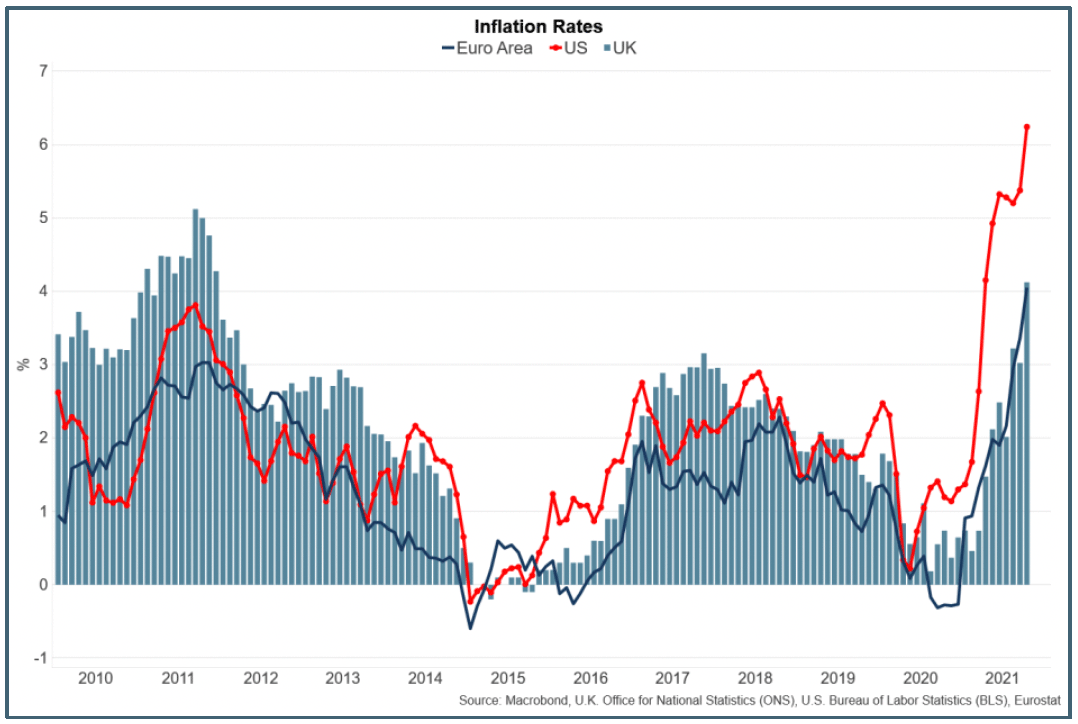

Inflation has risen sharply in the UK and internationally during 2021 to some of its highest levels in a decade as the global economy recovers and rebalances from the shocks to demand and supply during the pandemic to date. UK inflation has risen to 4.2% in October while the rate in the US is 6.2% and is 4.1% in the Eurozone.

The rise in inflationary pressures during 2021 reflect a combination of domestic and global factors. At a domestic level, demand for goods and services has strengthened during the year, however base effects in the data have contributed significantly to the pick-up in inflation in recent months as prices this year are compared to lower prices last year which had fallen significantly in the initial stages of the pandemic. Some of the increase will also be driven by policy effects, with temporary cuts to VAT for the hospitality industry now coming to an end.

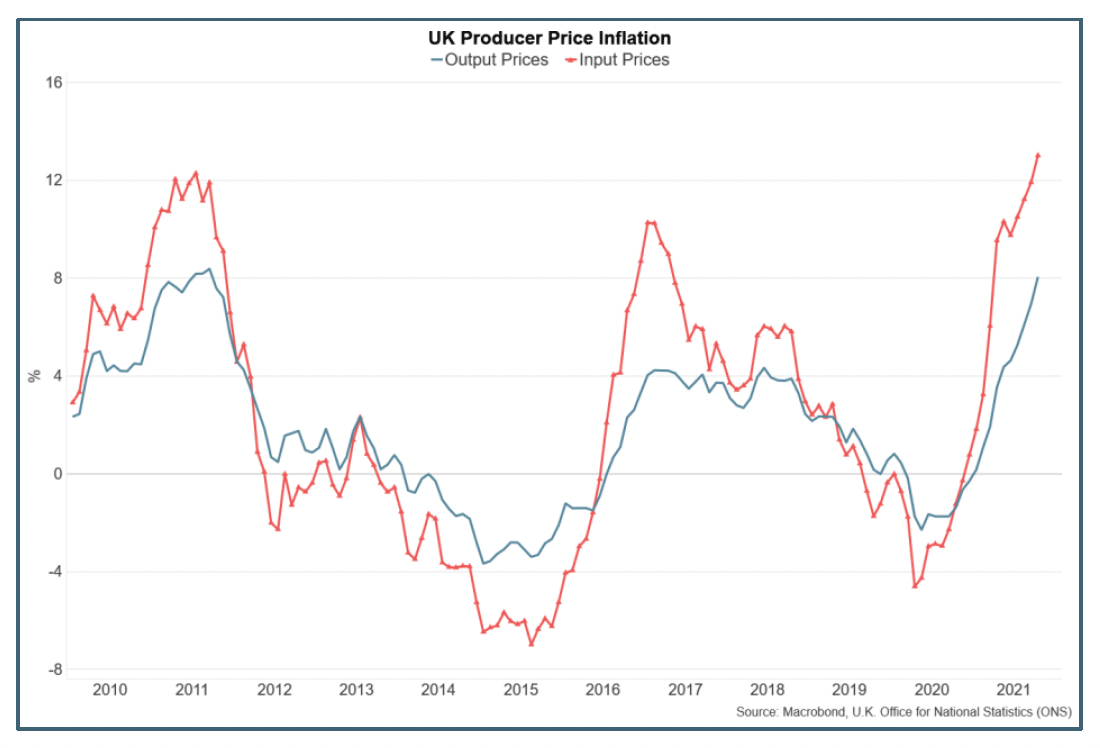

At a global level, the disruption in supply chains and the feed through of rising input costs into consumer prices has been a key driver. UK input price growth rose to 13% in October, while output price growth rose to 8% suggesting that, while businesses are partly absorbing higher costs, higher costs are passing through to consumers.[37]

These drivers of inflation are largely expected to be temporary as base effects in the data moderate and the global economy continues to recover and rebalance enabling current bottlenecks in supply chains to ease. However, most recently the recent sharp rise in energy prices and the feed through to retail gas and electricity prices is expected to generate further upward price pressures in the near term.

The Bank of England forecast inflation to rise above 4% going into 2022 and peak at around 5% in April before gradually easing back toward the Bank's 2% target over 2023. This profile reflects that domestic cost pressures are expected to rise in the near term alongside retail energy prices. However, the level of uncertainty that remains in the economic outlook means there are risks that global supply chain pressures remain persistent while the outlook for domestic price drivers is partly dependent on the pace at which demand in the economy continues to recover.[38]

The rise in inflation has notable implications for household's cost of living and spending power in the short term with real earnings growth expected to remain relatively subdued. Furthermore, current forecasts assume some tightening in monetary policy to ensure inflation is brought back to the 2% target sustainably which would potentially see a rise in interest rates over the coming months which will impact on the costs of certain aspects of debt across households and businesses. At their November meeting, the Monetary Policy Committee (MPC) made no change to monetary policy, maintaining the Bank Rate at 0.1% and the current programme of Quantitative Easing, with their next decision scheduled for mid-December.[39]

Contact

Email: OCEABusiness@gov.scot