State of the economy: November 2021

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Global Economic Context

The global economy is recovering however supply chain disruption is impacting global trade and inflation.

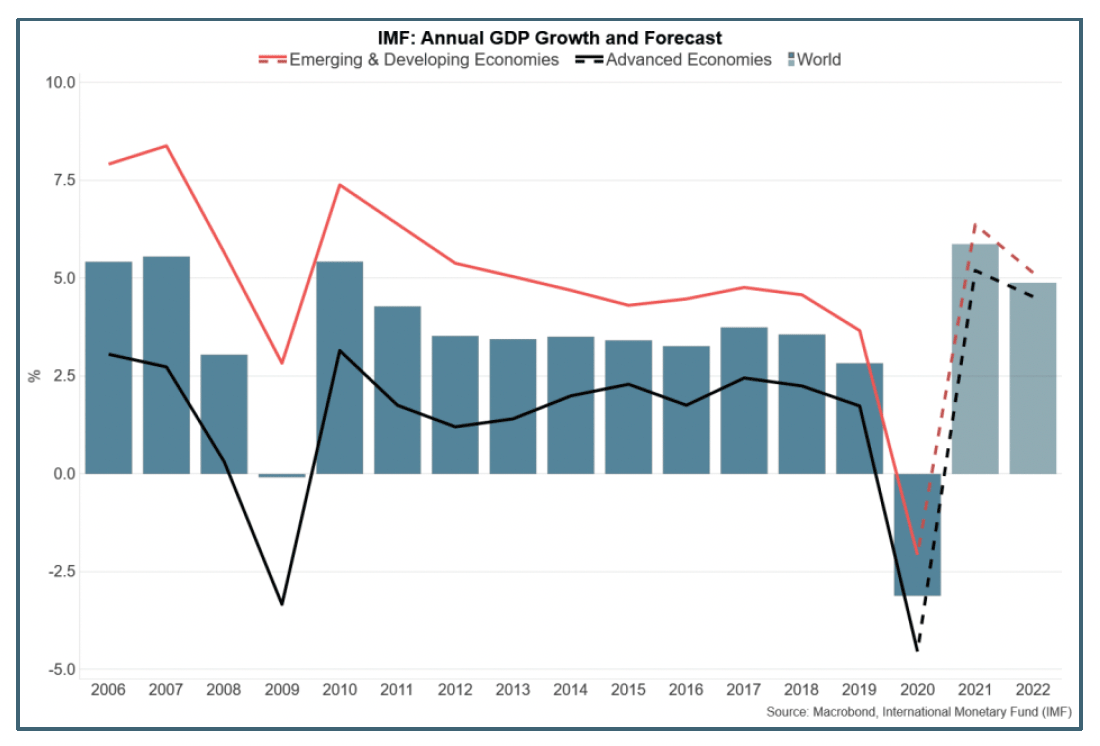

The pandemic has had an unprecedented impact on the global economy. 2020 saw global output fall 3.1%, with a synchronised fall in output across advanced and emerging and developing economies as restrictions were introduced to slow the spread of Covid-19.

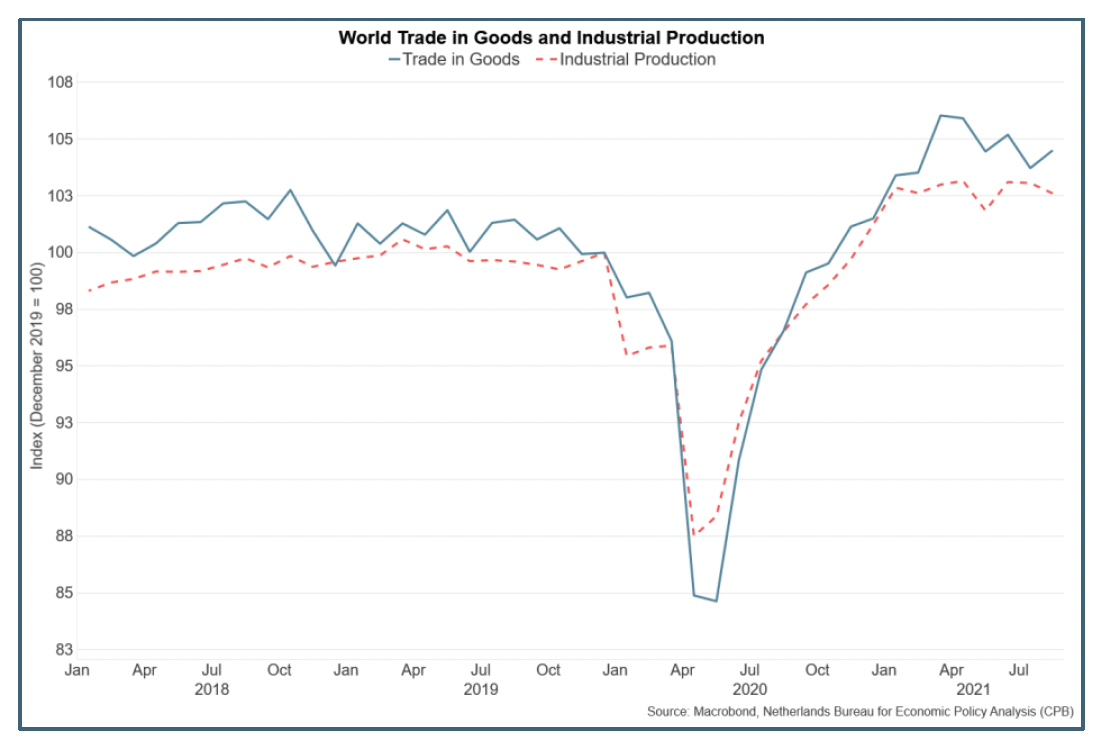

The global economy is recovering from the initial impacts on output in 2020, with latest data indicating that industrial production and world trade in goods is back above pre-pandemic levels. However, the nature of the impact and pace of recovery has varied significantly across countries, partly reflecting differences in the timing and nature of restrictions, the relative success of vaccination programmes, the scale of fiscal support, alongside the ongoing spread of different variants of the coronavirus.

Global demand and output have recovered strongly as restrictions on activity have eased, however the supply side of the economy is re-adjusting more slowly, leading to significant bottlenecks and disruption in global supply chains and a rise in inflationary pressures.

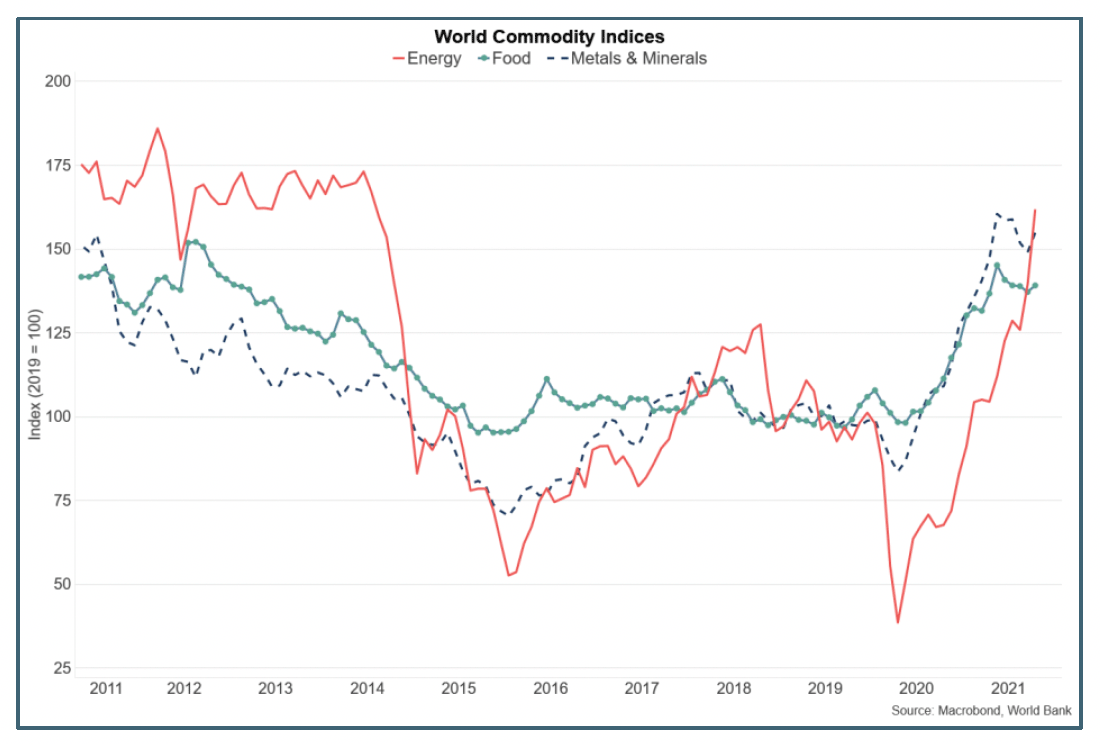

Commodity prices covering energy, food and metals have all risen over the past 12 months and have risen to their highest levels in almost a decade. Compared to pre-pandemic levels at the end of 2019, global food commodities are up 31%, metals 57%, while energy is up 60% having fallen sharply in 2020 at the start of the pandemic.

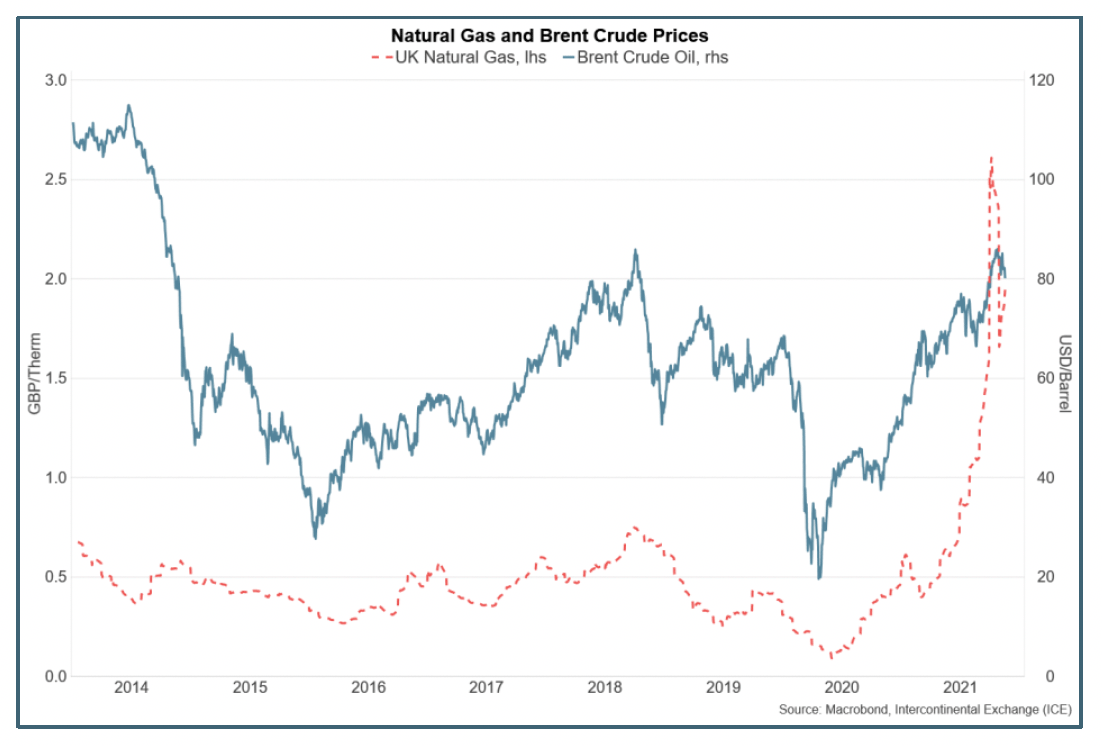

The rise in the energy index has been particularly driven by a rise in natural gas prices which had risen by over 500% on an annual basis, before partly falling back into November, while the Brent Crude oil price has broadly doubled over the past year to over $80 per barrel.

Strong global demand and supply chain disruption has also been reflected in a sharp rise in global freight costs as capacity across supply chains has continued to re-adjust to the strong rebound in demand (see Box B) while temporary restrictions and closures across countries continue to further impact the recovery.

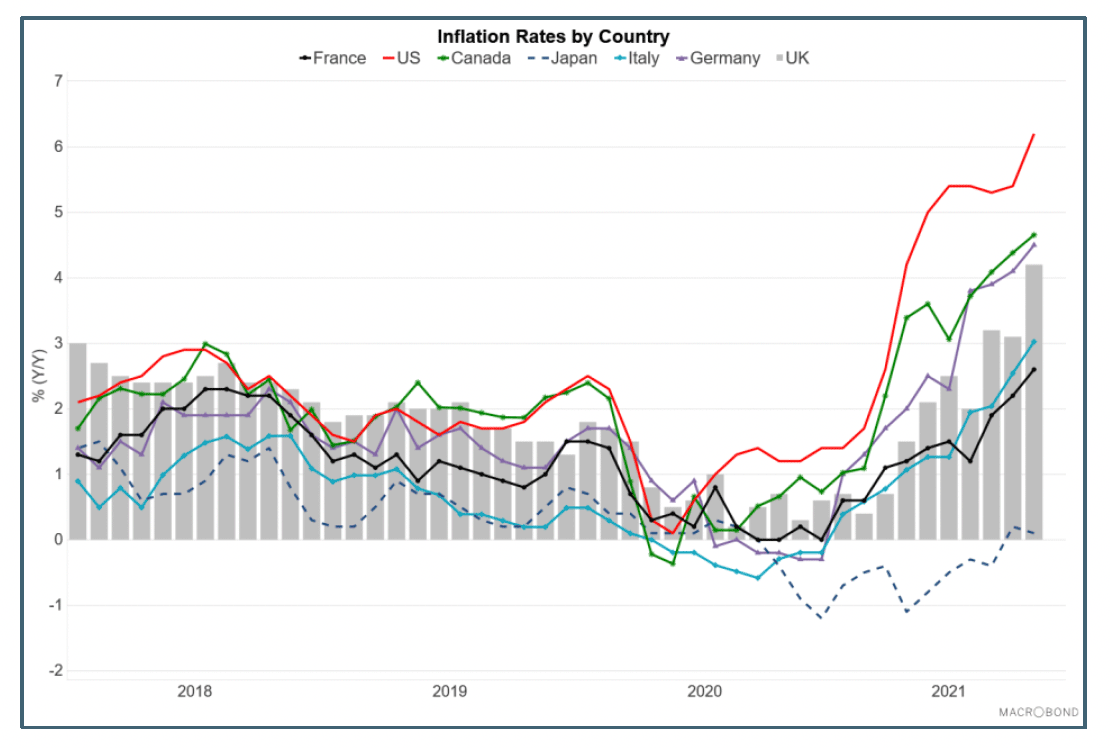

Imbalances in global supply chains and the associated increase in costs, alongside domestic recovery in demand has fed into a rise in inflationary pressures across countries in 2021 with inflation in many countries rising to their highest rates since the financial crisis.

Much of the global supply chain and inflationary challenges are expected to be temporary as the economy rebalances from the sharp impacts on economic activity during the pandemic to date, however, central banks have revised up their medium-term outlook for inflation, and price pressures are expected to persist for most of 2022.

Although global output is back above pre-pandemic levels,[1] the pace of global recovery slowed over the third quarter, reflecting the impacts on activity of supply chain challenges and further indicating that the short run outlook for 2022 remains challenging. The IMF forecast global GDP to grow 5.9% in 2021, slowing to 4.9% in 2022.[2]

Contact

Email: OCEABusiness@gov.scot