State of the economy: November 2021

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Business Activity

Businesses activity has strengthened as most restrictions on activity have been removed, however rising input costs raises risks for cashflows.

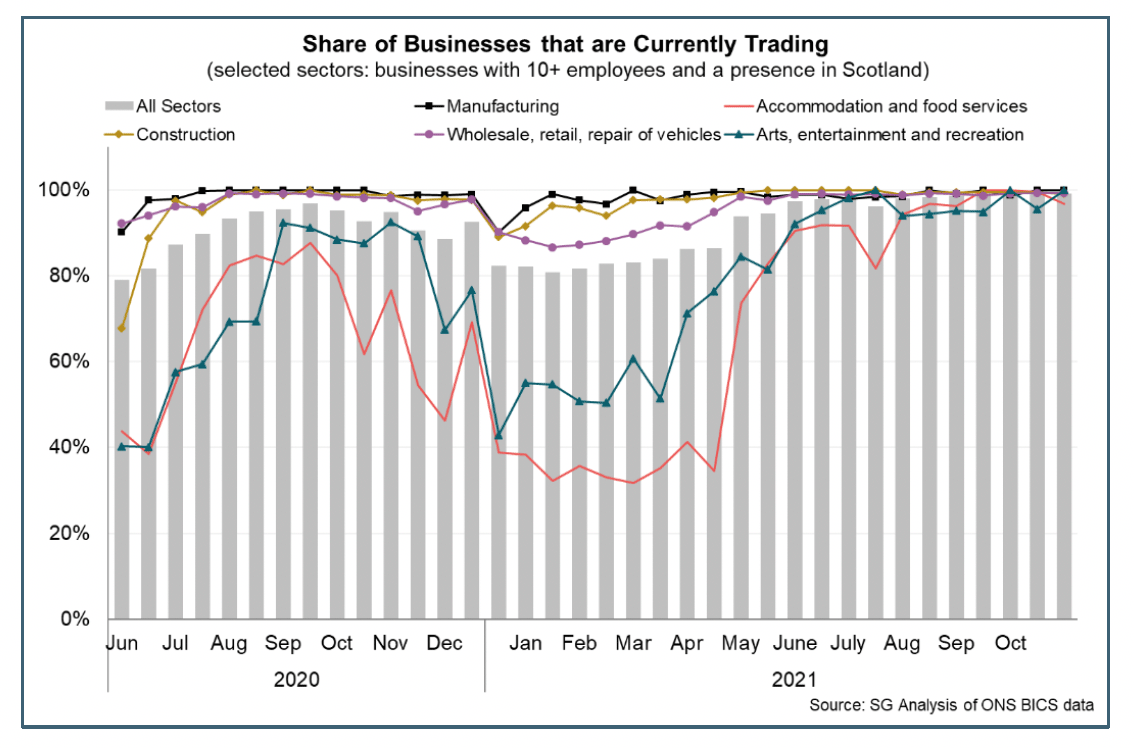

At this stage of the pandemic, businesses in Scotland are back to trading with very limited levels of restrictions on activity. The removal of most remaining restrictions on consumer facing sectors as Scotland moved beyond level 0 restrictions in August (with some protective measures remaining place) has meant that around 99% of business have been trading since August and the gap between sectors that had been most directly impacted by restrictions is effectively closed.

Business Activity and Cashflow

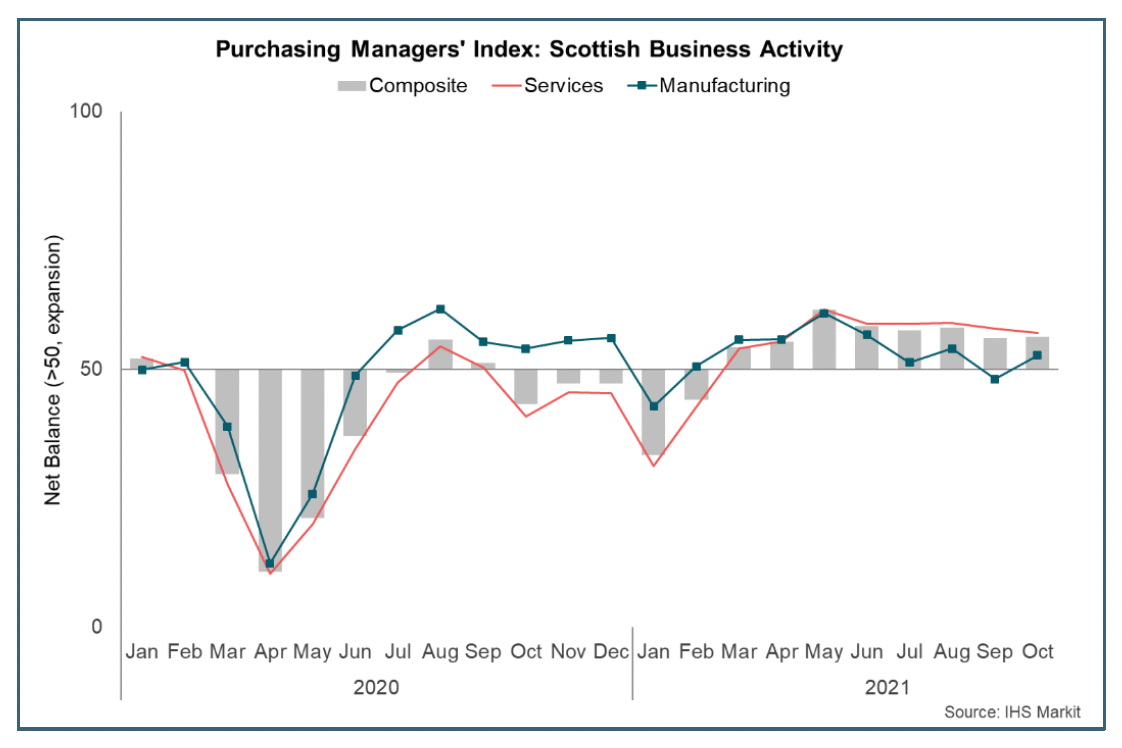

In terms of overall activity, the latest Purchasing Managers Index for October signalled that private sector activity continued to grow robustly over the month with the net balance at 56.3 and up marginally from September.[4] However, the pace of growth has moderated slightly from stronger growth in the second quarter.

The service sector continued to drive growth in October, though at a slightly slower pace than in recent months, and business activity in the sector continued to expand at pace following the easing of restrictions over the second quarter. Manufacturing activity picked up in October, however the pace of activity growth in the sector remained notably slower than earlier in the year.

Sector differences remain a key characteristic of this stage of the recovery. The removal of most of the restrictions on the consumer facing parts of the services sector and subsequent reopening, means that the focus has partly shifted from whether businesses are trading, to the level of capacity they are trading at and the challenges they are facing as they continue to recover.

In October, the consumer facing parts of the service sector continue to report more challenges in their trading and revenue status than other sectors, likely reflecting a combination of legacy effects of having stricter restrictions on activity for the first half of 2021 and some changes in the capacity at which they are trading.

For example, in October 95% of all businesses reported being fully trading (4.3% partially), however this was lowest in accommodation and food services (83% fully trading and 14% partially) and in arts, entertainment and recreation (84% fully trading and 17% partially).[5]

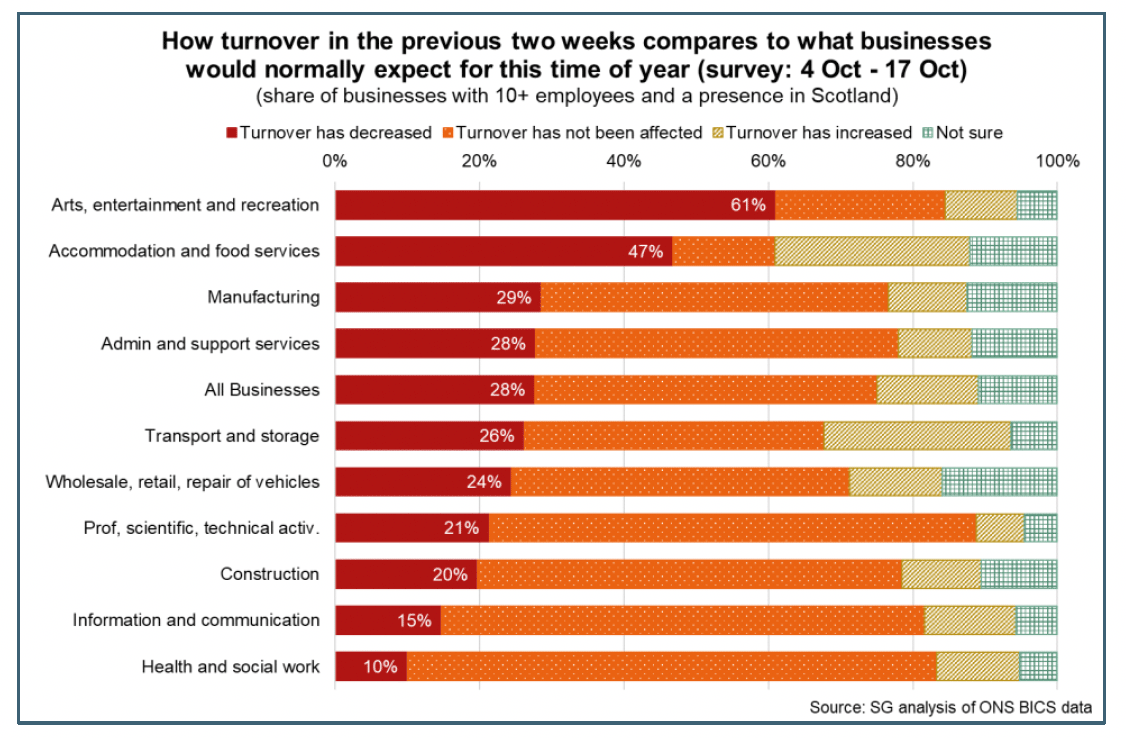

Furthermore the financial performance of businesses continues to vary across sectors. In terms of business turnover in October, 28% of all business reported having lower turnover than normal for the time of year, while 47% reported that turnover was not affected and 14% reported that it had increased. Lower than normal turnover continues to be most widespread in the arts, entertainment and recreation services sector (61%) followed by the accommodation and food services sector (47%). However in the case of the latter, accommodation and food also had the highest share of firms reporting that turnover had increased (27%) alongside the transport and storage sector (26%), emphasising the level of variability within sectors of customer demand.

Overall, turnover performance has improved since March with a rise in the proportion of firms reporting an increase in turnover (from 6% to 14%) and a fall in the share reporting lower turnover (from around 45% to 28%). However, on the cost side, supply chain disruption, rising input costs inflation and employee shortages have emerged as key challenges and risks for many businesses reflecting imbalances following the sharp rebound in demand at this stage of the recovery.

As set out above, this has emerged as both a global and domestic challenge. In Scotland, PMI data for October show the indicator for input cost inflation, particularly for manufacturers, has been on an upward trend since the start of the year and has risen to its highest level on record. Respondents cited that this is due to issues around the pandemic and EU-Exit and greater costs for materials, wages and fuel.[6]

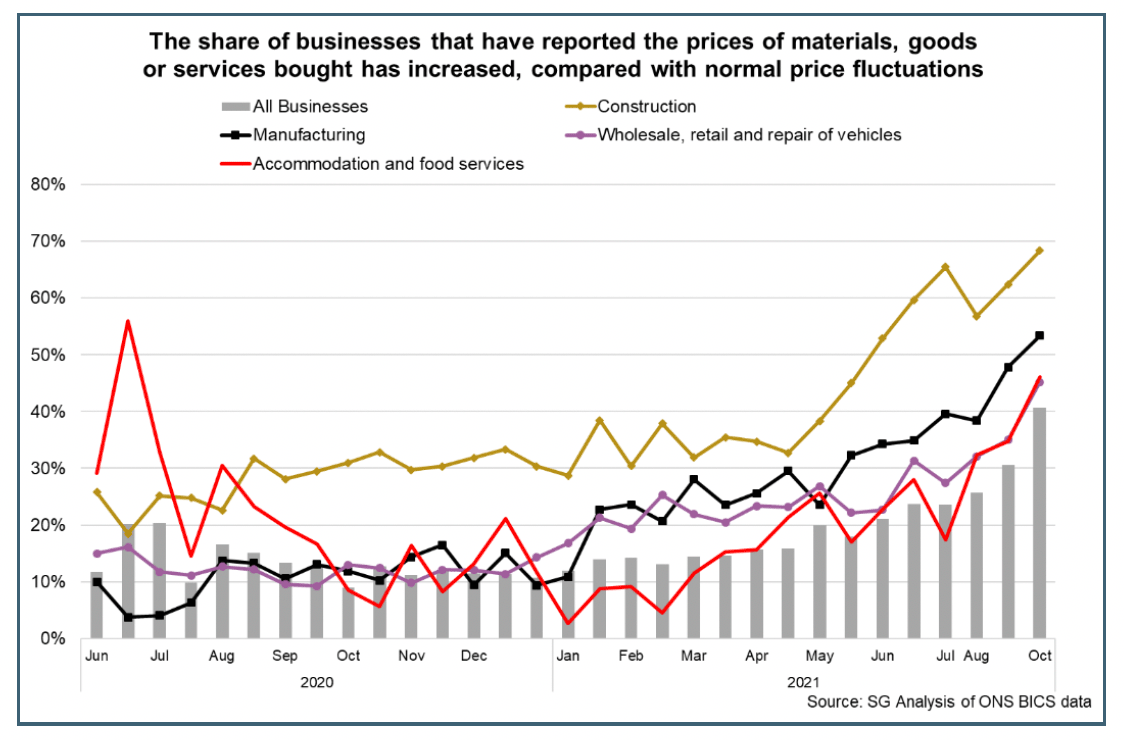

Increased input costs have been evident across sectors. In October, the Business Insights and Conditions Survey (BICS) showed that 41% of businesses had seen prices increase more than normal, however this was most prominent in construction (68%), manufacturing (53%) and wholesale and retail (45%).[7]

Recent business survey data for Q3 2021, showed that firms across sectors were on balance providing positive net-balances for revenue and profit, some for the first time in a number of months.[8] This points to an improvement in demand and business activity, though on the back of an extremely difficult period and as such remains fragile. Alongside this, 86% of respondents in the construction sector and 90% in the manufacturing sector reported concerns around cost pressures for raw materials, with less but similarly elevated levels for overhead costs, indicating that while business conditions have improved, risks to the cashflow of some businesses in the short term remain.

Business Investment and Trade

Cashflow challenges present a key risk to business investment as businesses recover from the recent shocks to economic activity and look to adapt or build capacity.

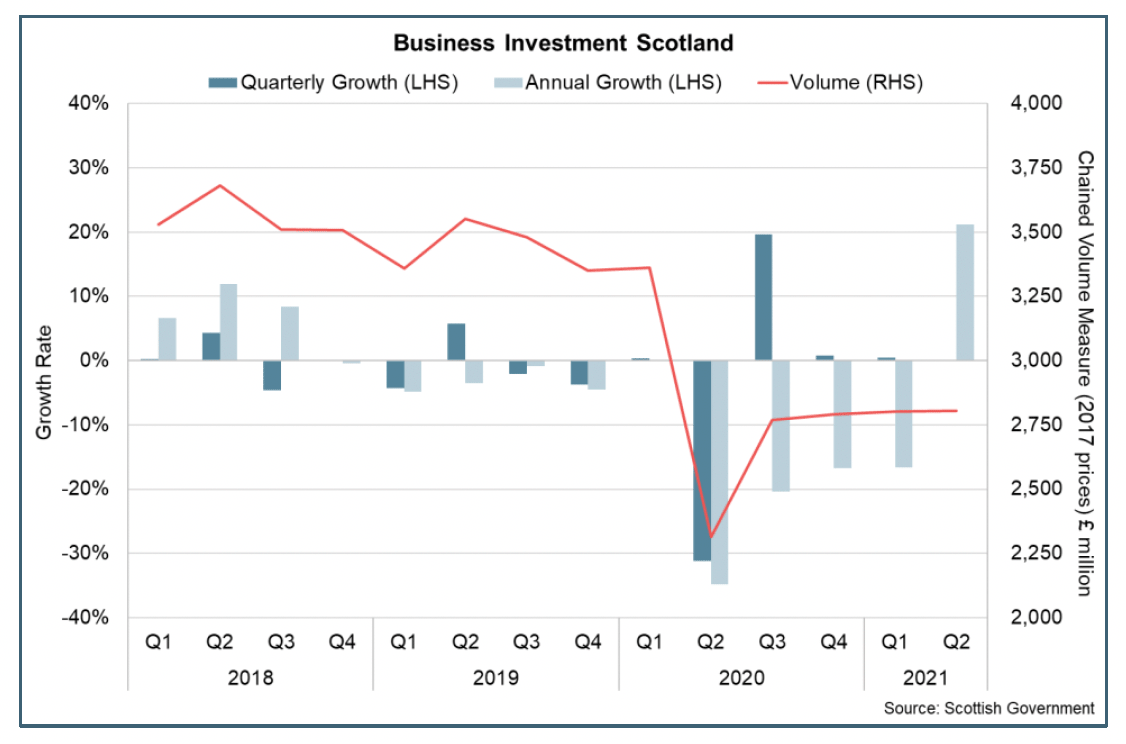

Business investment has fallen sharply during the pandemic and while it has recovered some of the initial fall (up 21% between Q2 2020 and Q2 2021), growth remained relatively flat over the first half of 2021 and remains 16% below its pre-pandemic level in Q4 2019.[9]

Latest business survey data presents a mixed picture for business investment, likely reflecting the ongoing uncertainty in the outlook for businesses and wider cost pressures which have emerged and may present cashflow risks.

In the third quarter of the year, there has been signs of strengthening growth in business investment across construction, manufacturing and financial and business services, while investment in retail and wholesale and tourism fell.[10] Furthermore, in September, BICS data shows that 10.4% of businesses reported that capital expenditure remained lower than normal, however this has improved and fallen from over 19% at the start of the year.[11]

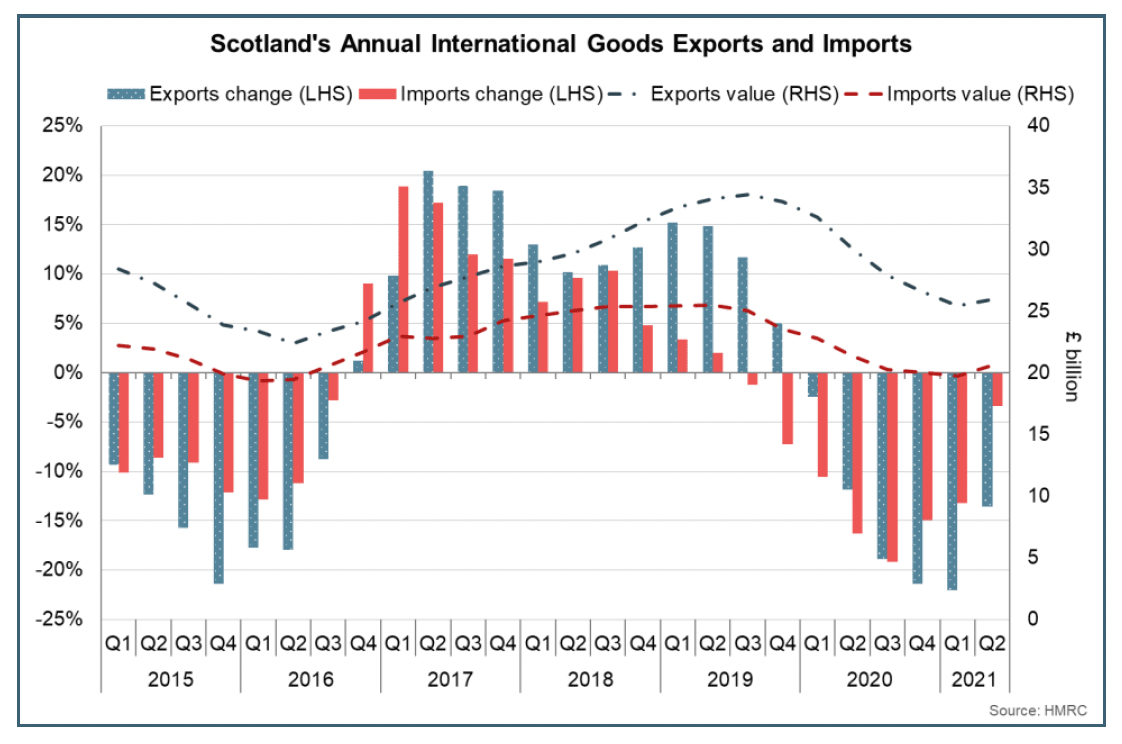

Scotland's international trade in goods has also experienced significant challenges arising from the impacts of the pandemic and the transition to the new trade agreement between the UK and EU.

In June 2021, the value of Scotland's annual goods exports was £26 billion, down 14% compared to annual exports to June 2020.[12] This was driven by a 41% fall in the exports of oil and gas and as such, when excluded, Scotland's goods exports increased by 3%. Similarly, machinery and transport, which is a key exporting commodity for Scotland, also decreased over the year (-6%), however there were increases in exports of chemicals (+19%) and manufactured goods (+16%). In terms of destination, Scotland's annual goods exports to the EU fell 14% to £13.2 billion while exports to non-EU countries fell by 13% to £12.8 billion. Over the same period, goods imports decreased by 4% to £20.6 billion.

The latest quarterly data indicates that the value of trade (exports and imports) has strengthened from the sharp fall in the second quarter of 2020, however has eased slightly in the first half of 2021.

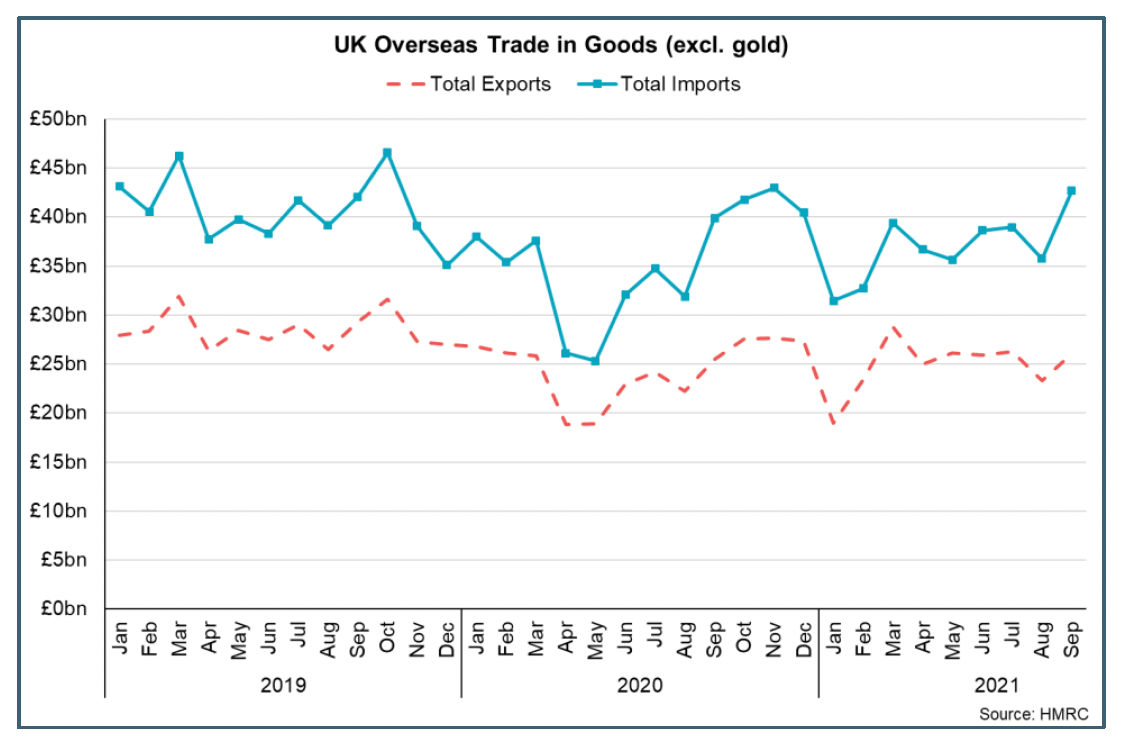

The most recent monthly UK trade data for September[13] signals that trade has strengthened from the falls at the start of the year and goods exports were 2% higher than in September 2020. However, for the period January to September in 2021, goods exports remain 11% below the equivalent period in 2018 prior to the pandemic and trade volatility in 2019 surrounding EU Exit. In terms of key exporting sectors for Scotland, in September, total exports of Scotch whisky remained unchanged over the month however in the first nine months of 2021 were down 1% compared to the same period in 2018. Exports of fish fell 9% in September and in the first nine months of 2021 were 12% down on same period in 2018.

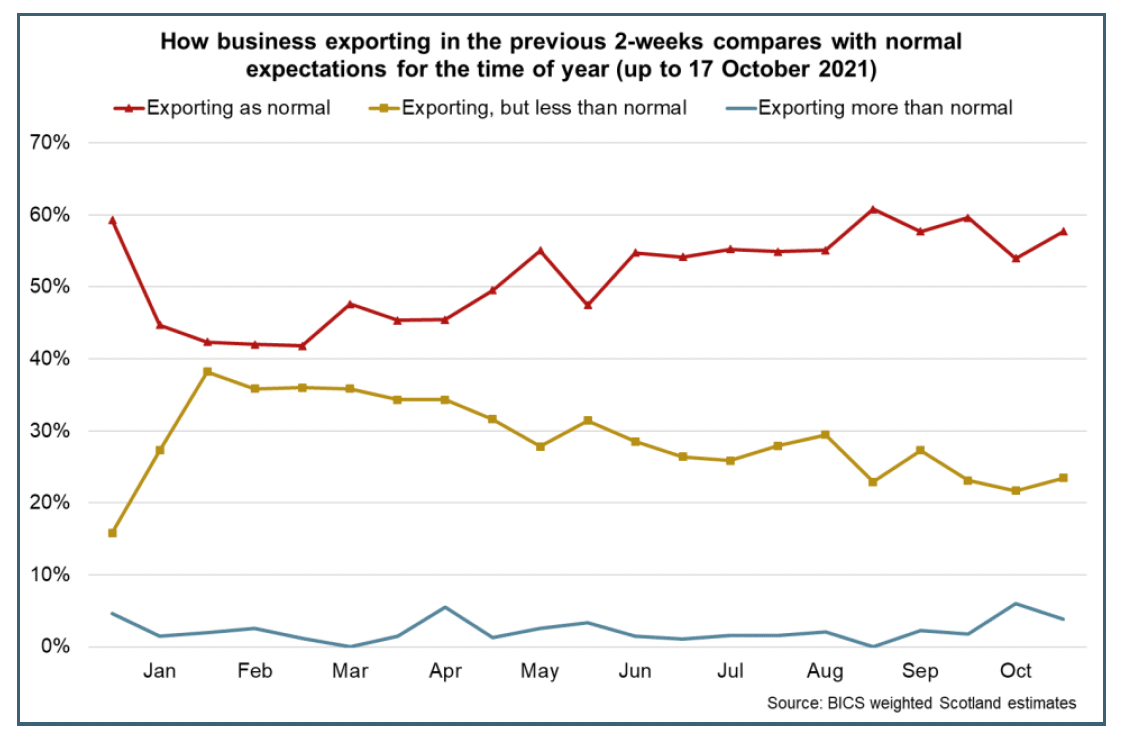

More recent business survey data for October indicates further improvement in trade activity from the start of the year with 58% of Scottish businesses reporting to be exporting as normal for the time of year (up from 42% at the start of February) while 24% were exporting less than normal (down from 38% at the start of February).

However, supply chain bottlenecks have emerged as the global economy adjusts and rebalances from the impacts of restrictions during the pandemic, while for some sectors, the new trading relationship with the EU provide further challenges. In October, 37% of exporters and 43% of importers reported facing changes in transportation costs while 15% of exporters and 23% of importers reported a lack of hauliers to transport goods or lack of logistics equipment.[14]

Box A: Estimates of economic scarring from the pandemic.

The economic policy response to the pandemic sought to protect the productive capacity in the economy through measures such as the furlough scheme and business support. The aim was to minimise the extent of economic scarring and so it is useful to consider the extent to which this has taken place.

Output in the Scottish and UK economy is forecast to return to pre-pandemic levels over the coming months, however the impacts of the pandemic on labour supply, investment and productivity are expected to have some longer term/permanent impacts (scarring) on the potential output from the economy.

Due to the longer term nature of scarring on potential output, estimates of the scale of scarring are uncertain and subject to revision as new data on the pace of recovery as well as on the extent of economic challenges associated with the reopening of the global economy become available.

In October, the Office for Budget Responsibility, revised down their estimates of medium term scarring on potential output in the UK economy to 2% (down from 3% in March), reflecting that the pace of the recovery back to pre-pandemic levels of output, the labour market, capital investment and total factor productivity have performed more strongly than previously forecast.[15]

Similarly in November, the Bank of England estimated the level of potential supply in the UK economy in 2024 will be around 2% lower than would have been implied by the MPC's pre-pandemic projections.[16]

In terms of the Scottish economy, the latest forecast from the Scottish Fiscal Commission in August revised up the rate at which GDP is expected to return to pre-pandemic levels of output, reflecting the stronger than expected period of growth since their previous forecast in January. As a result of the subsequent upward revision to trend productivity, trend GDP in 2025 is forecast to be 2% lower than pre-pandemic forecasts (down from 3% lower forecast in January 2021).[17]

Overall, stronger than expected economic activity in 2021 and the upward revisions to forecasts compared to the start of the year has meant that some estimates of scarring impacts on the economy from the pandemic have slightly fallen and are currently converging around 2%.

There remains significant uncertainty in the medium to long term outlook for the labour market, skills and capital investment and the extent to which falls in these areas will recover, however latest data continues to signal that the aggregate impacts on the labour market have been less than expected following the end of the furlough scheme.

Furthermore, impacts of the pandemic on the economy continue to be complicated by the effects of EU Exit and the move to the new economic relationship which is expected to weigh on potential supply. The OBR estimate that the reduction in trade post EU Exit will result in a 4% reduction in long-run potential productivity, which is bigger than the expected long run effect of the pandemic.

Overall, the degree of economic scarring appears to be low, particularly when compared to what had initially been feared and this, to a large extent, reflects the policy response, which the OBR has described as "remarkably successful".

Contact

Email: OCEABusiness@gov.scot