State of the economy: May 2022

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Business Activity

The direct impacts of the pandemic on business activity have eased, however significant headwinds persist from ongoing supply challenges and intensifying inflationary pressures.

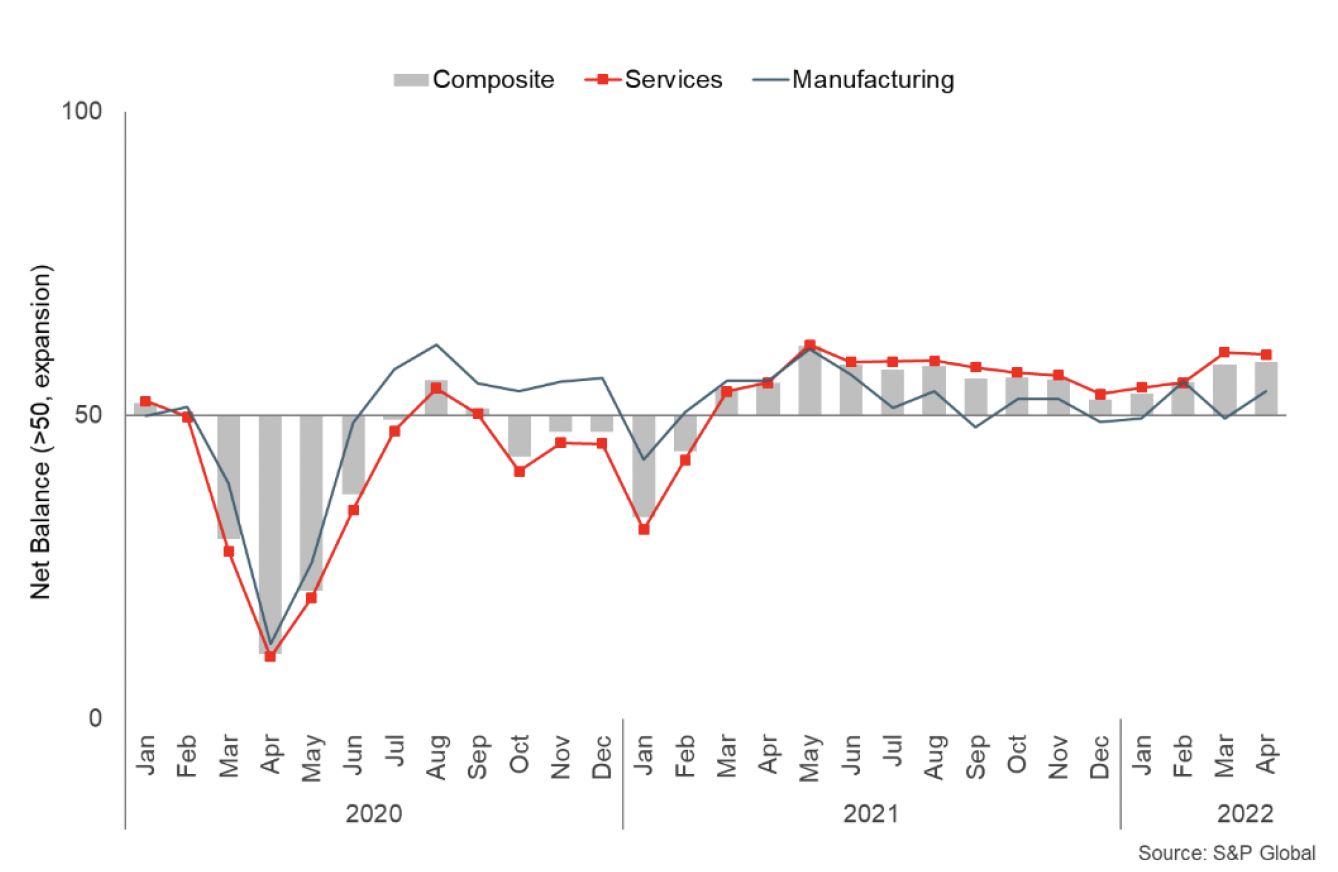

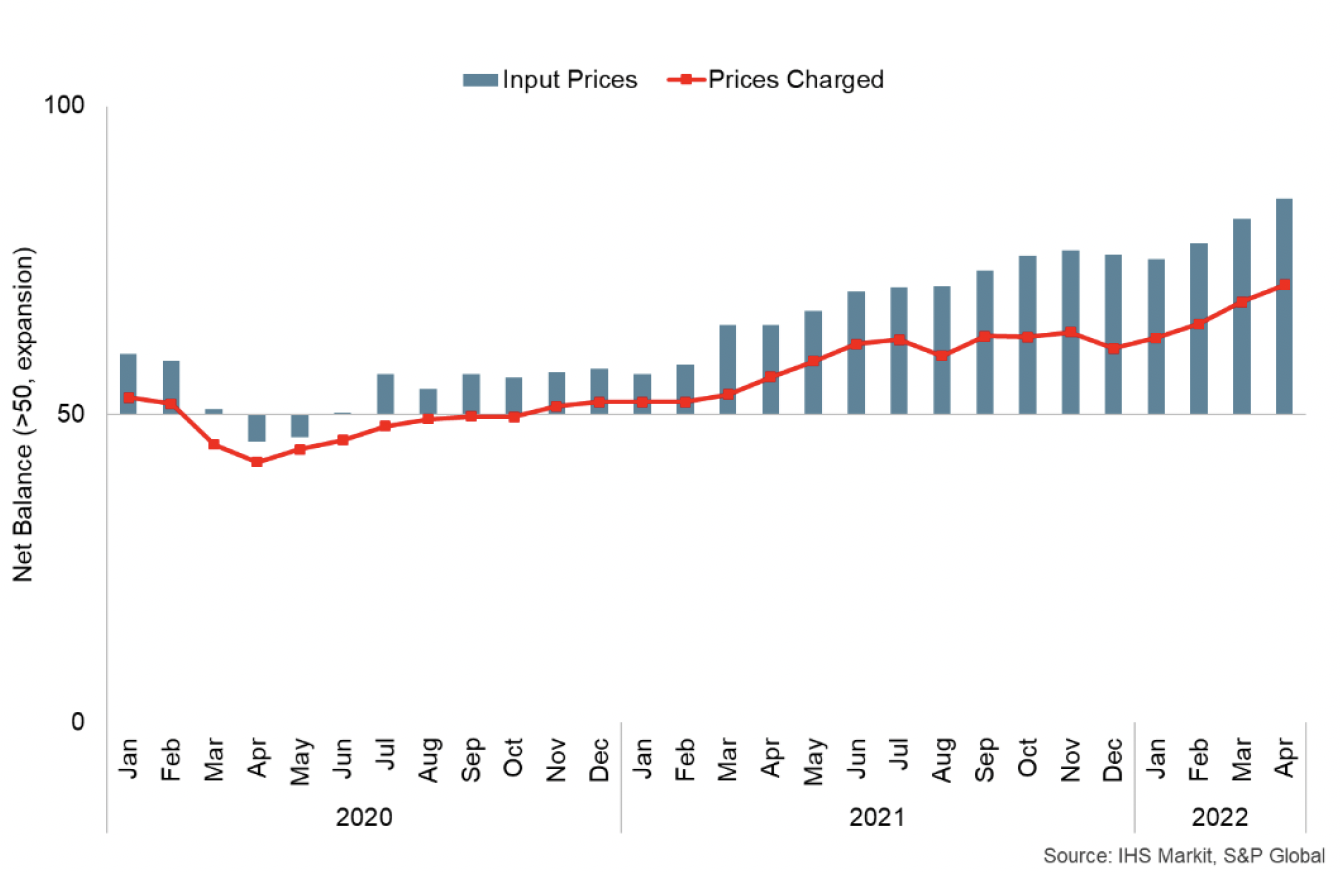

The Purchasing Managers Index (PMI) business survey signalled that Scottish business activity growth accelerated for a fourth consecutive month in April (58.9, its highest rate since May 2021), with the latest momentum supported by a renewed pick-up in manufacturing production, while services output remained strong.[4]

Although the rate of growth slowed marginally in the services sector, panellists cited that reduced pandemic restrictions continued to have a positive impact while producers in the manufacturing sector noted an upturn in orders. However, inflationary pressures and supply chain challenges intensified in April, resulting in prices charged rising to survey records and future activity expectations falling.

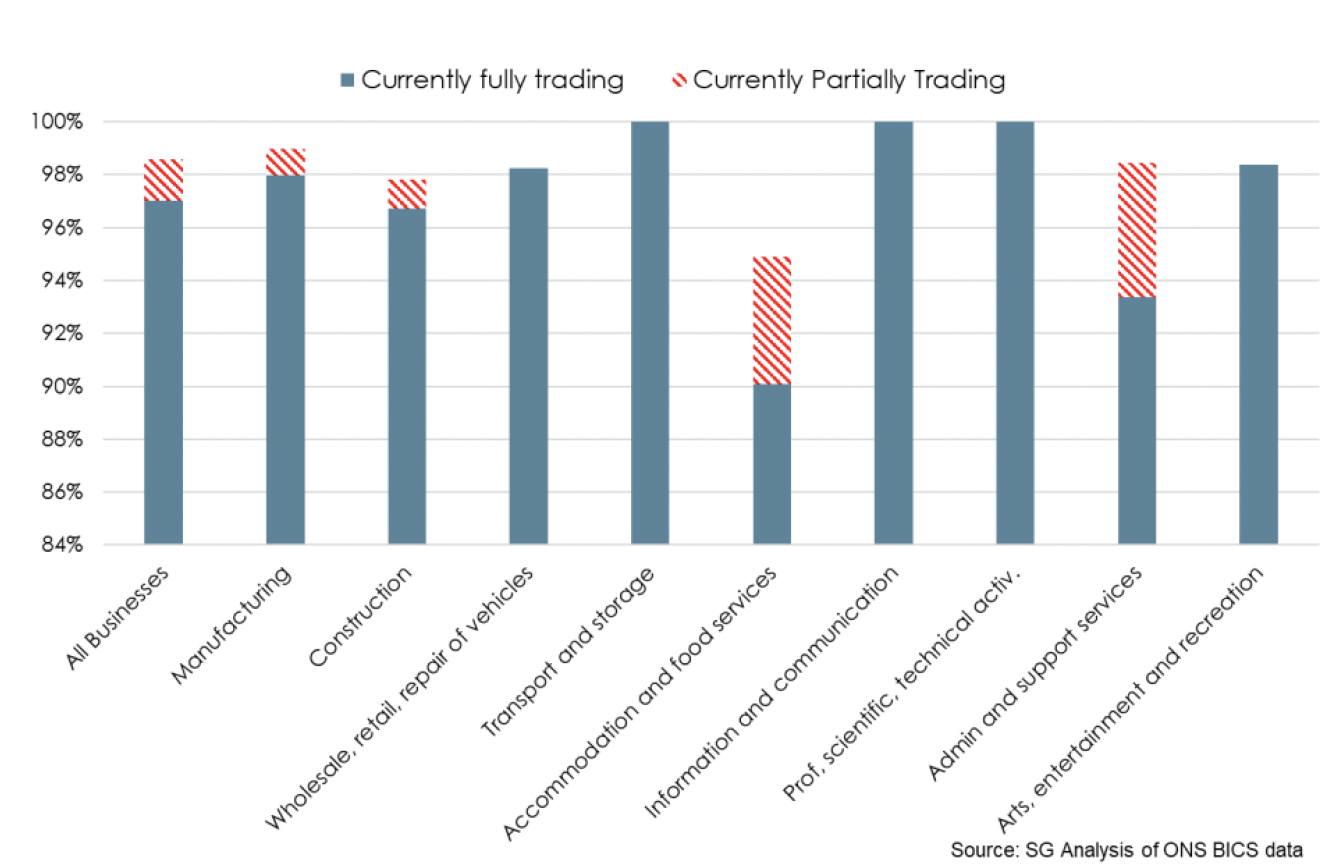

Strengthening business activity has also been reflected in improvements in business trading capacity, though there continues to be variation across sectors. At the beginning of May, business survey evidence signalled that all businesses in the Information and Communication, Transport and Storage and Professional, Scientific and Technical Activities sectors were trading fully.[5] However, lower capacity continued in parts of consumer facing services with 90% reporting as fully trading in the Accommodation and Food Services sector.

There were also indications of improved business turnover at the end of March, with 24% of businesses reporting to be trading with reduced turnover compared with normal expectations, the lowest rate in the time series and down from around 30% at the beginning of 2022. Similarly the proportion of all firms reporting that turnover had improved, increased to 14%, up from around 8%, while over 50% reported that turnover had not been affected.[6]

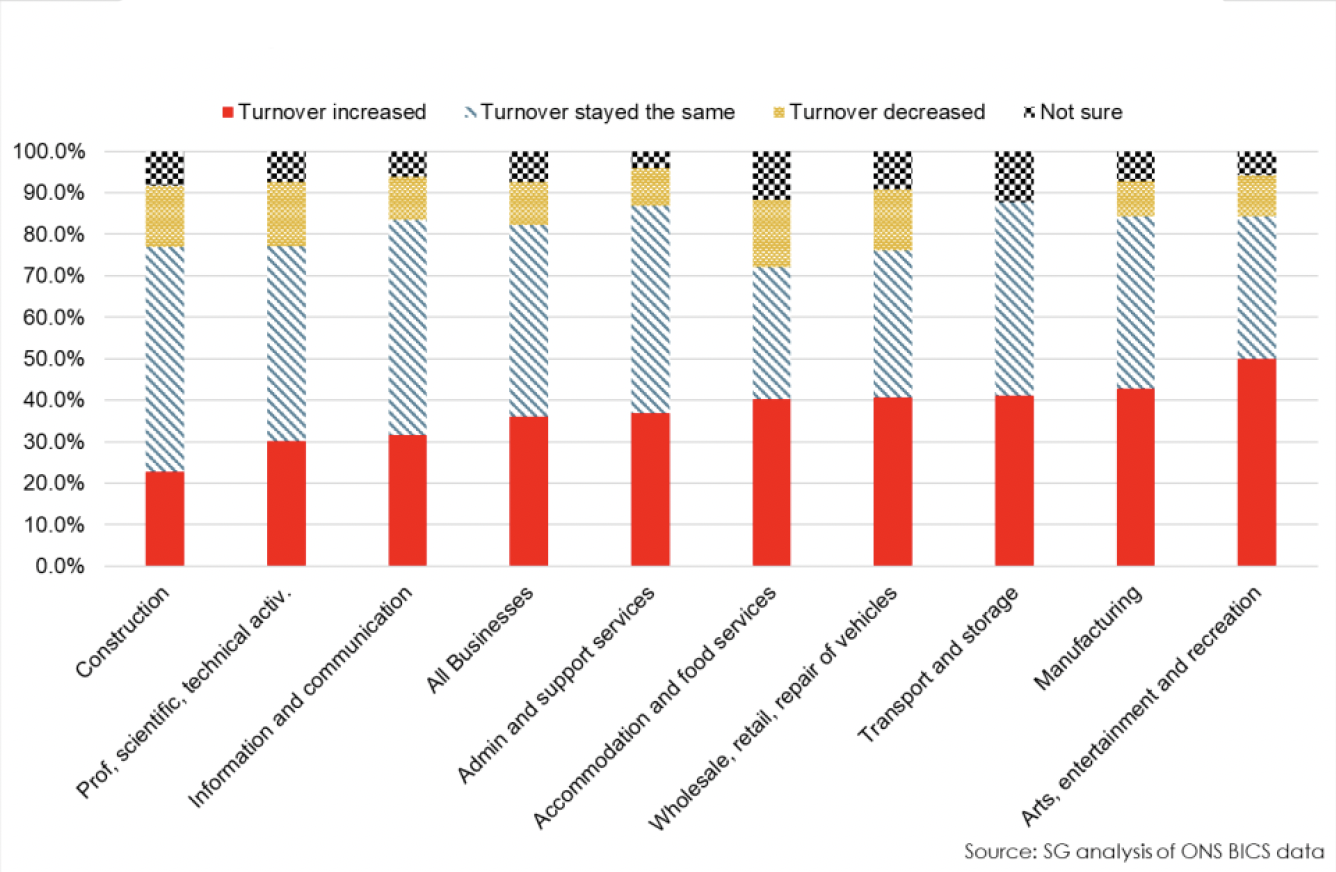

When considering turnover in March 2022, relative to February 2022, 36% of all businesses reported that turnover had increased, compared to 10% reporting turnover had decreased and 46% reporting that turnover had stayed the same. Challenges impacting business turnover at the beginning of May include cost and shortage of labour and cost of materials amongst others.

Looking to the month ahead, 18% of all businesses expected turnover to increase in April, while 58% expect it to stay the same, 15% expected turnover to decrease.[7]

However, inflationary pressures have continued to intensify for businesses through higher energy prices, costs of materials and supply chain disruptions. BICS data for March, showed that 53% of businesses reported that input prices increased more than normal, its highest rate in the time series and up from 49% in February. Furthermore 59% of businesses currently trading reported that input prices had increased compared to the previous month. Higher than normal input price increases remained most widespread in manufacturing (69%), construction (67%) and accommodation and food services (56%).[8]

Scottish PMI data also showed the indicator for input cost inflation continued to rise into April, and peaked at a new record high for the third consecutive month (85.0).[9] Respondents noted a range of factors driving this including higher fuel, energy, material, food and labour costs with Brexit, the pandemic and the situation in Ukraine adding further pressures.

This was also the case for SMEs with Scotland's Small Business Index for Q1 2022 reporting that 88.2% of respondents reported increasing overheads, predominantly due to fuel, utilities and inputs, while only 1.6% reported they had fallen.

As a result, firms have continued to pass higher costs through to customers, with the PMI prices charged indicator also increasing to a record high for the fourth consecutive month (71.0). Further business survey data for Q1 2022 indicates that 70% of businesses expected to raise their prices over the next three months as cost pressures hit a five-year high for construction, manufacturing and tourism.[10]

Monitoring the economic impact of COVID-19 in real time

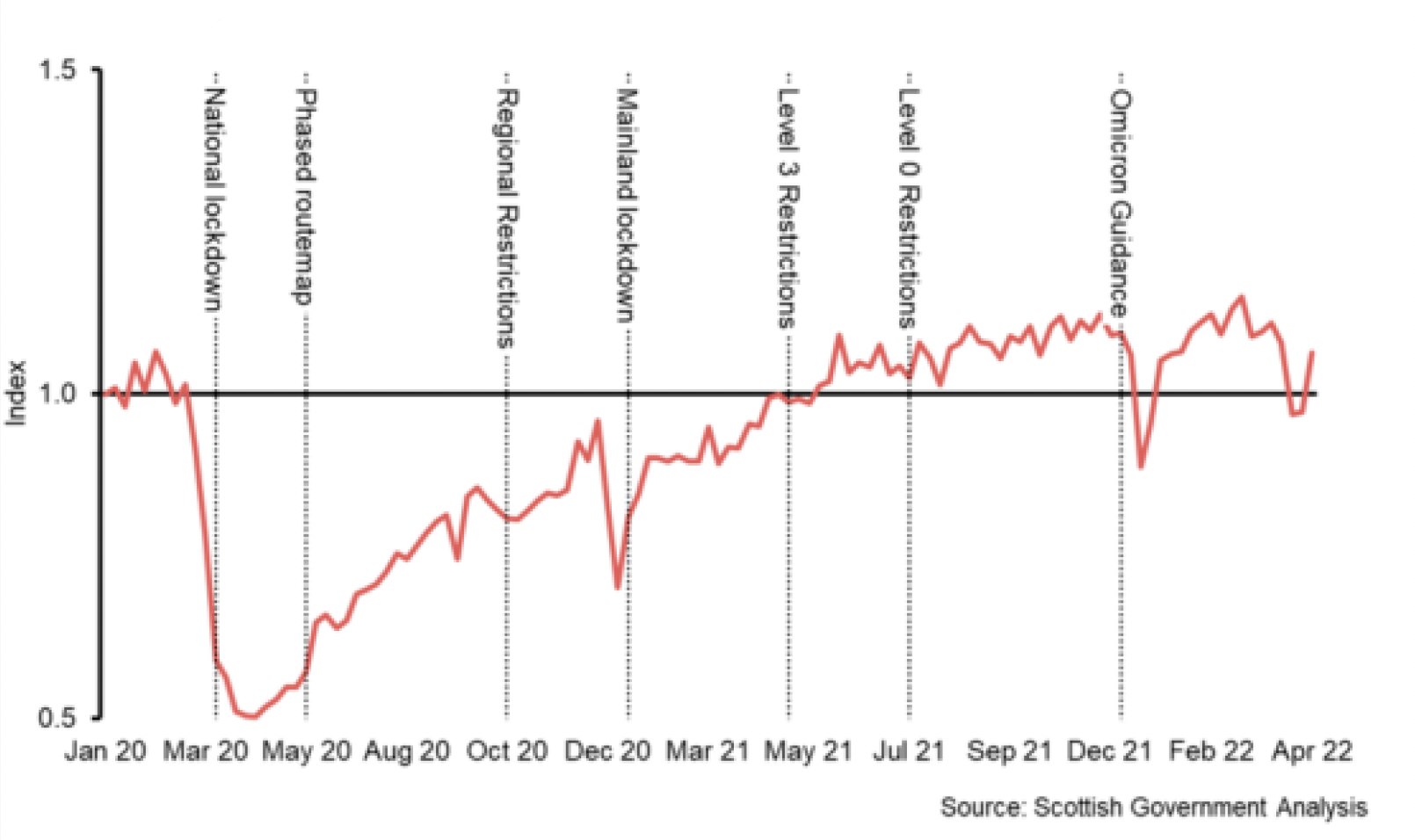

In the July 2020 Monthly Economic Brief we set out our Real Time Economic Impact Index, which we used to monitor the economic impact COVID-19 was having on the economy on a weekly basis. The quickly changing nature of the pandemic and the government response meant that traditional measures of the economy, which do not provide a real time assessment but instead look over longer periods such as a month or a quarter, were less timely.

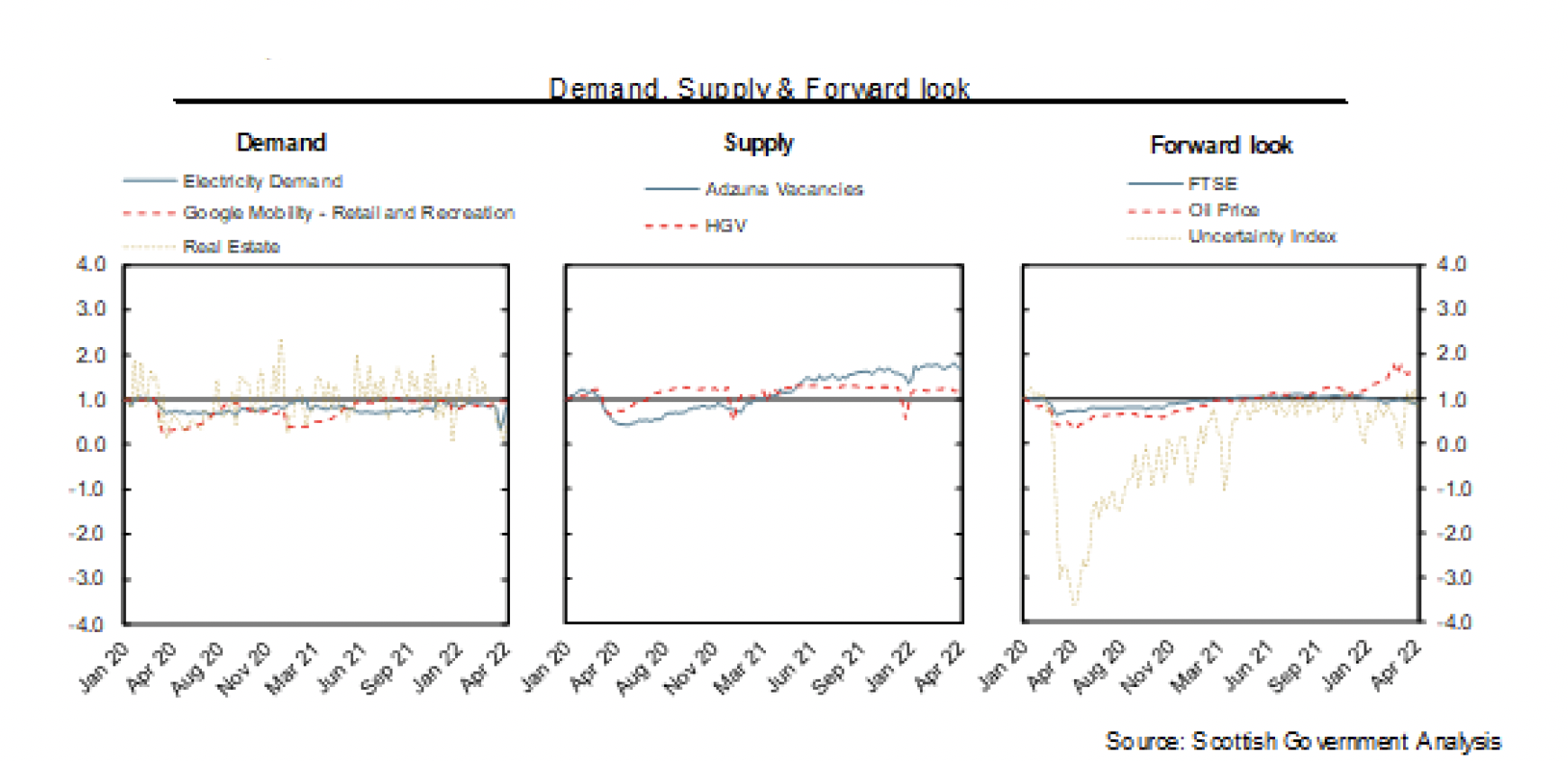

The Real Time Economic Impact Index used a set of high-frequency indicators to report on economic impacts on a weekly basis, looking across three areas: demand, supply, and future expectations.

As can be seen in the chart, the Real Time Economic Impact Index performed well in tracking the impacts of the pandemic

It deteriorated before lockdown was introduced, highlighting the importance of changing behaviour and expectations, falling heavily (significantly below 1) as the lockdown was then in place. The Index then recovers but deteriorates each time there are new stages of restrictions, although to a lesser extent each time. The index recovered to pre-covid levels during 2021, and then dipped again following the tightening of restrictions in response to the Omicron variant.

Looking across the different indicators it can be seen that many of the individual indicators have returned to pre-pandemic levels, whilst supply indicators have stabilised above these levels. Greater HGV traffic likely reflects the increased use of online retail, whilst the elevated vacancy data likely reflects labour market shortages discussed in more detail in the Labour Market section.

Whilst indices like this have been useful in monitoring the real time impacts of COVID-19, as time passes there is considerable uncertainty around both the best choice of variables and the strength of the link between the performance of the index and that of the economy. As we move into a new phase of the pandemic, it becomes difficult to disentangle possible structural changes from ongoing economic harm being caused by COVID-19.

With the reduced need for real time monitoring of the economy, the focus is shifting back to measuring economic impacts by traditional measures.

Business Investment

The uncertainty during the pandemic, supply chain disruption and inflationary pressures have resulted in challenging conditions for business investment.

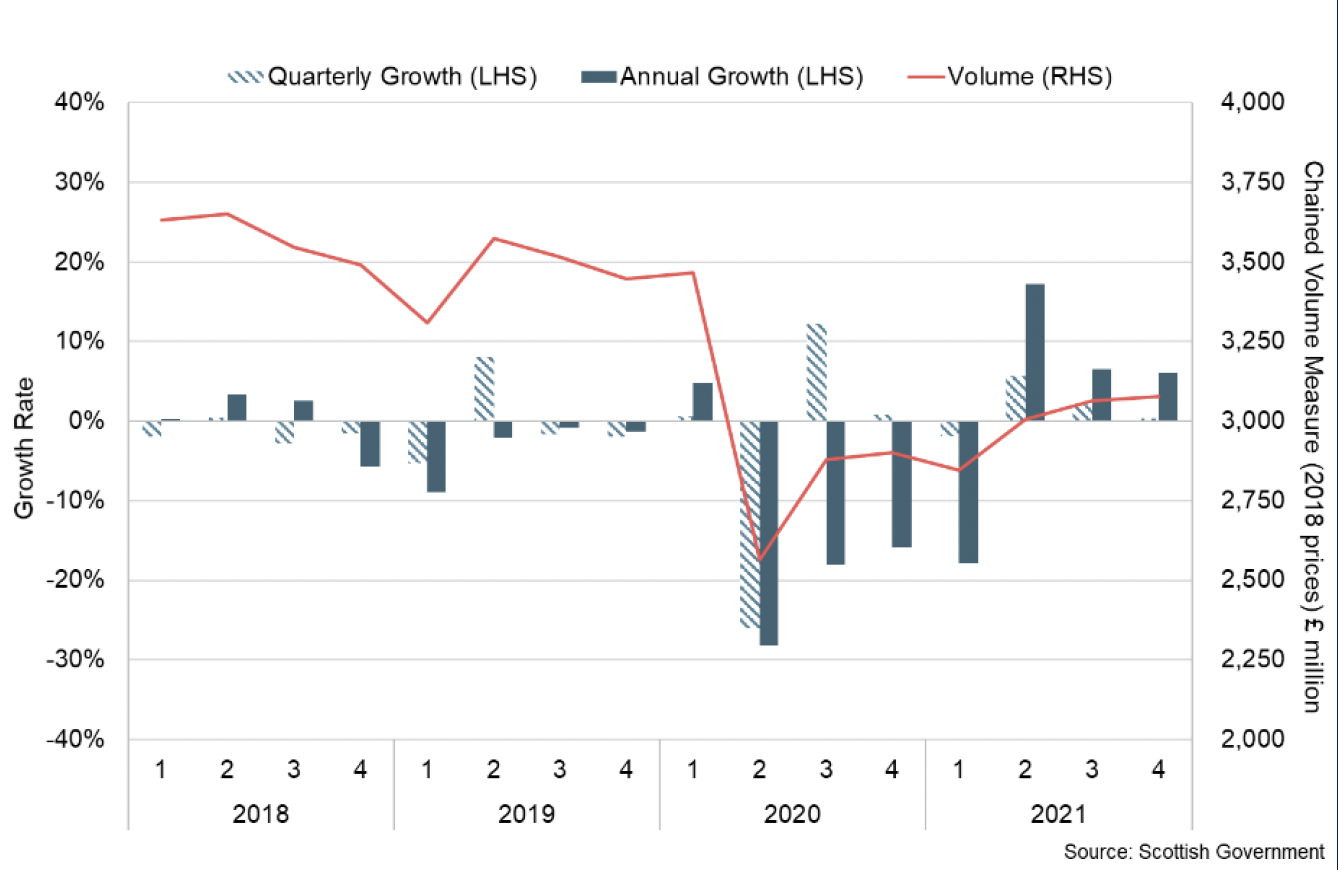

Although business investment continued to strengthen over 2021 it remains subdued. Latest data for Q4 2021 showing growth of 0.4% over the quarter and 6.1% over the year. In comparison to the pre-pandemic level in the fourth quarter of 2021, the volume of business investment remains £369 million, or 10.7% below and has been slower than other indicators in recovery to pre-pandemic levels.[11]

Latest business survey data continues to present a mixed picture for business investment, likely reflecting the ongoing uncertainty in the outlook for businesses and wider cost pressures which have emerged and the different challenges which sectors are facing.

In the first quarter of 2022, there have been signs of strengthening growth in business investment across construction, manufacturing, and financial and business services, while investment in retail and wholesale remained negative and tourism firms expect to cut back on investment.[12] In March, BICS data shows that over half of businesses (51%) report that capital expenditure has not been affected compared to normal expectations for the time of year. However, 9% of businesses reported that capital expenditure was lower than normal and 10% reported capital expenditure is higher than normal (both at their strongest points in the time series).[13]

At the beginning of May, 16% of all businesses expect capital expenditure will increase in the next three months while 43% expect it to remain the same, 9% forecast a decrease and an additional 20% are not sure. When asked what would limit business capital expenditure in April 2022, 51% of all businesses were not expecting any limits to capital expenditure while 16% responded that uncertainty about demand or business prospects would be a limiting factor.[14]

Contact

Email: OCEABusiness@gov.scot