Scottish Housing Market Review: Q1 2025

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

7. Mortgage Affordability

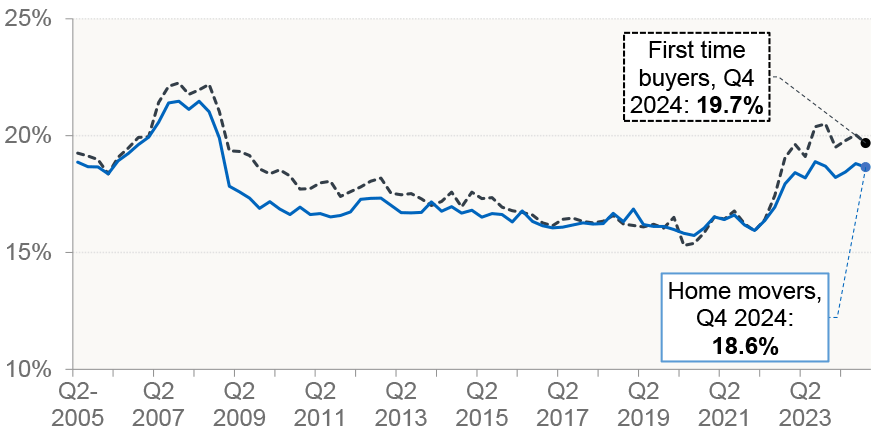

The impact of the increase in interest rates is reflected in measures of mortgage affordability. As illustrated by Chart 7.1, the share of borrower income taken up by capital and interest payments for new mortgages had reached a low in 2020 due to the fall in interest rates in response to the Covid pandemic. Subsequently, the sharp rise in interest rates has translated into a significant increase. For first-time buyers, who tend to borrow a high proportion of the purchase price and are thus relatively more exposed to interest-rate risk, the share increased from a low of 15.3% in Q2 2020 to 20.5% in Q4 2023, although it has then fallen back somewhat to 19.7% in Q4 2024 as mortgage rates have eased. For home movers, the share has increased from a low of 15.7% in Q3 2020 to 18.6% in Q4 2024, which is similar to its post-pandemic high of 18.9% in Q3 2023.

Source: UK Finance

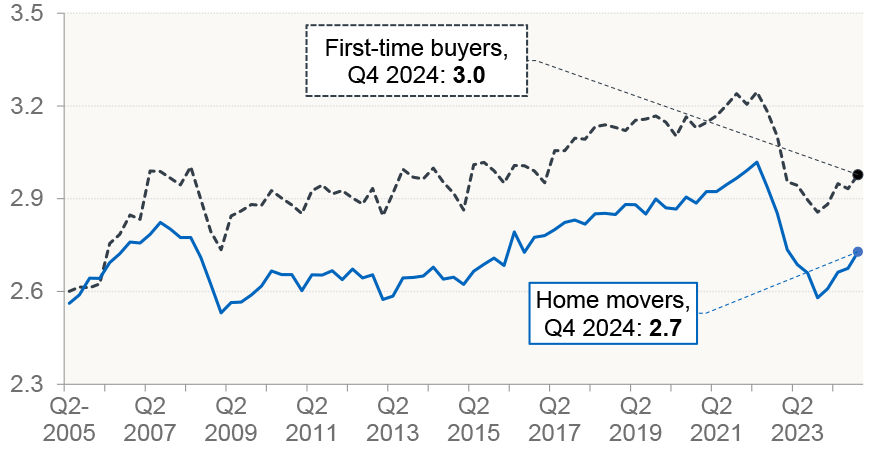

Chart 7.2 shows that the average house-price-to-income ratio for new mortgages in Q4 2024 was 3.0 for first-time buyers and 2.7 for home movers, which for each series is the same as its long-term average since Q2 2005.

Source: UK Finance

Contact

Email: jake.forsyth@gov.scot