Scottish Housing Market Review Q1 2023

Scottish housing market bulletins collating a range of statistics on house prices, housing market activity, cost and availability of finance and repossessions.

Part of

7. Mortgage Arrears & Possessions

Arrears

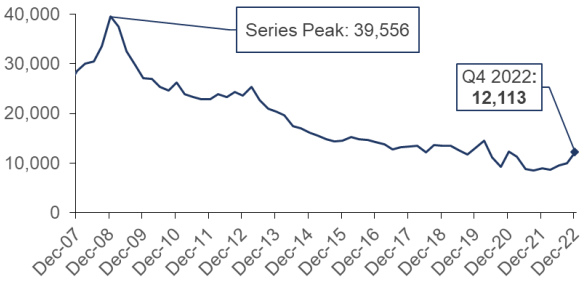

There were 12,113 regulated mortgages that went into arrears across the UK in Q4 2022, an annual increase of 36.0% (3,207), although this is from very low levels in Q4 2021. Comparing to the pre-pandemic period in Q4 2019, the number of regulated mortgages entering arrears has fallen by 7.6% (-997) As shown in Chart 7.1, following a peak of 39,556 in Q4 2008 during the financial crisis, there was a declining trend in the number of regulated mortgages entering arrears, which has started to increase towards pre-pandemic levels. It should be noted that Covid-19 payment holidays were not classified as technical arrears, and thus are not reflected in these figures; however, even when these payment holidays came to an end in April 2021, this did not result in a substantial increase in arrears. (Source: FCA)

Source: FCA

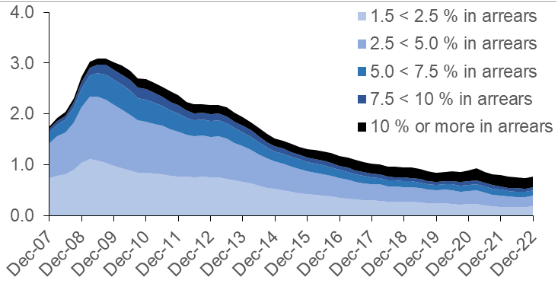

The share of lenders' outstanding regulated mortgage balances that were in arrears stood at 0.77% at the end of Q4 2022. This has remained broadly stable during the pandemic, with arrears at 0.86% at the end of Q1 2020. Chart 7.2 plots the share of lenders' outstanding balances that were in arrears by degree of severity. Arrears reported in the FCA MLAR data relate only to loans where the amount of actual arrears is 1.5% or more of the borrower's current loan balance.

Source: FCA

UK Finance data show that there were 6,060 buy-to-let mortgages in arrears of 2.5% or more of the outstanding balance across the UK in Q4 2022. This is up slightly by an annual 0.8% (50), but remains well below the period of the 2008 financial crisis. The number of buy-to-let mortgages in arrears of 2.5% or more as a percentage of the total number of buy-to-let mortgages was 0.30% as at Q4 2022, very similar to Q4 2021 (0.29%).

Possessions

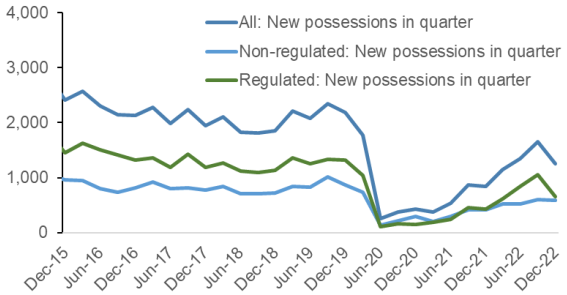

Chart 7.3 shows that despite restrictions on possessions being lifted since 1 April 2021, there were only 661 new regulated mortgage possessions across the UK in Q4 2022. While this was an increase relative to Q4 2021 of 229 (+53.0%), possessions are still substantially lower (down 658, or 49.9%) relative to Q4 2019, prior to the pandemic.

Source: FCA

Contact

Email: William.Ellison@gov.scot