Scottish Government bonds programme: outline business case summary

Summary of the outline business case we developed to assess the case for issuing Scottish Government bonds.

Economic Case

As part of assessing the case for bond issuance, the OBC has considered a range of alternative options, including continued use of the National Loans Fund and other sources of external borrowing.

As well as assessing their ability to deliver the strategic aims above, options were assessed against a standard set of Critical Success Factors (CSFs): potential value for money, supplier capacity and capability, potential affordability and achievability.

Following the initial assessment against strategic fit and critical success factors, policy options involving the issuance of wholesale bonds were taken forward for a more detailed social cost-benefit assessment (CBA), compared against the continued use of the National Loans Fund – the ‘Business as Usual’ option. Across the short-listed options, the detailed assessment assumes that the Scottish Government would borrow £300 million per annum over a 10-year period. The short-listed options taken forward in the OBC are set out below.

Option A: continued use of NLF borrowing, the Business as Usual option.

Option B: a one-off wholesale bond issuance.

Option C: multi-year wholesale issuance assuming the Scottish Government would alternate annually between bonds (5 issuances) and NLF borrowing (5 issuances).

Option D: the Scottish Government issues bonds for five consecutive years, followed by borrowing through the NLF thereafter.

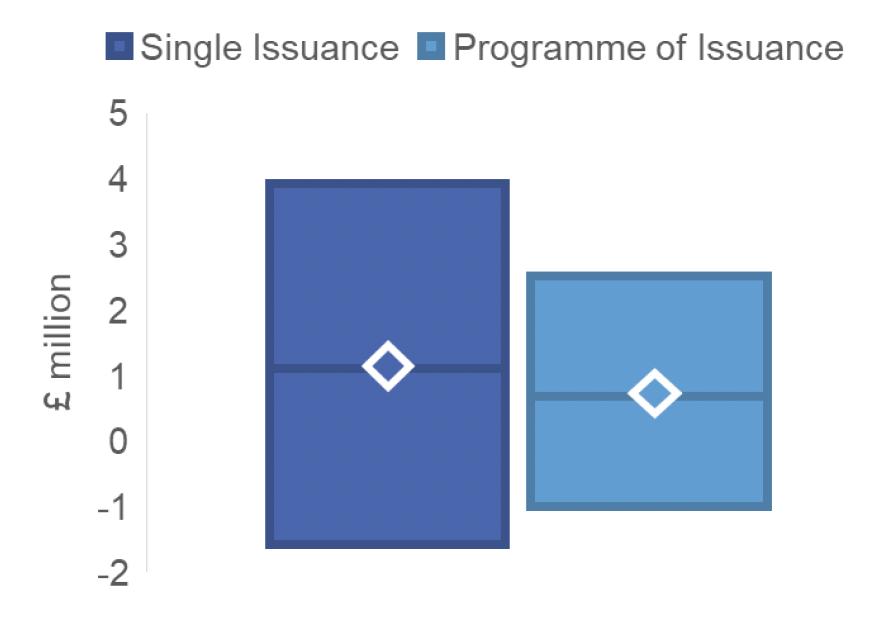

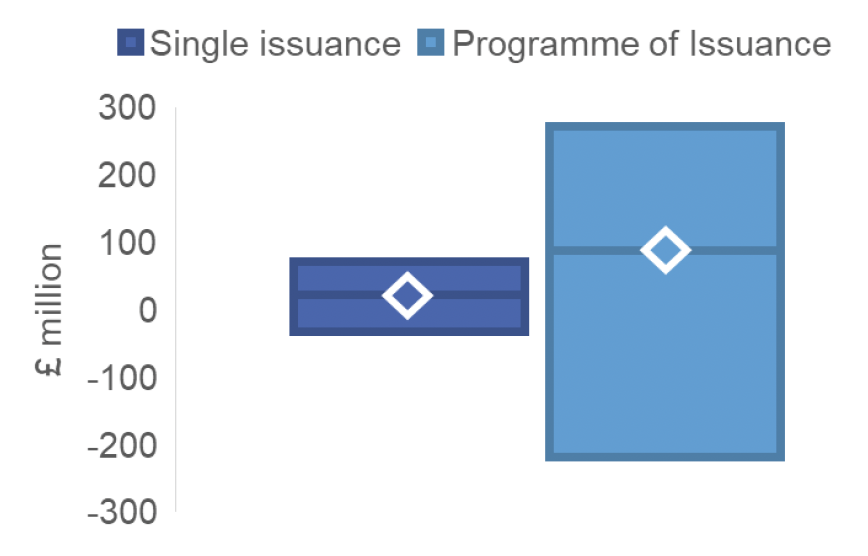

In this summary document, results are presented for a single issuance – corresponding to Option B above – or for a programme of issuance, which reflects Option D. Options D and C are both multi-year programmes but Option D has slightly higher overall present value costs and therefore provides an upper bound estimate. For brevity and clarity, results for the multi-year programme are presented solely for Option D. Other differences between Options C and D are discussed in the financial case.

The table below summarises the key differences between borrowing through the NLF and borrowing through bonds. These differences will be referred to in the later sections of this summary document. Key distinctions include the borrowing mechanism (direct market issuance for bonds, versus borrowing via the UK Government for NLF), repayment structure (flexible options for bonds versus annuity structure for NLF), interest rates and available tenors.

| Area | Bonds | NLF |

|---|---|---|

| Borrowing mechanism | The Scottish Government borrows directly from international debt markets | The Scottish Government borrows through the UK Government |

| Repayment structure | Bonds can be structured flexibly; however, the Scottish Government is likely to adopt a standard bullet repayment structure. This means that interest payments are made annually until maturity and the principal is repaid in full when the bond matures | The Scottish Government can only access loan structures (such as annuity) in which both interest and principal are repaid regularly |

| Interest rate | Determined by the market | 11 basis points above the interest rate on UK gilts, which are themselves determined by market conditions |

| Tenors (repayment period) | Can vary from less than a year to 40 or 50 years | Can borrow with a tenor ranging from 10 to 25 years |

Benefits

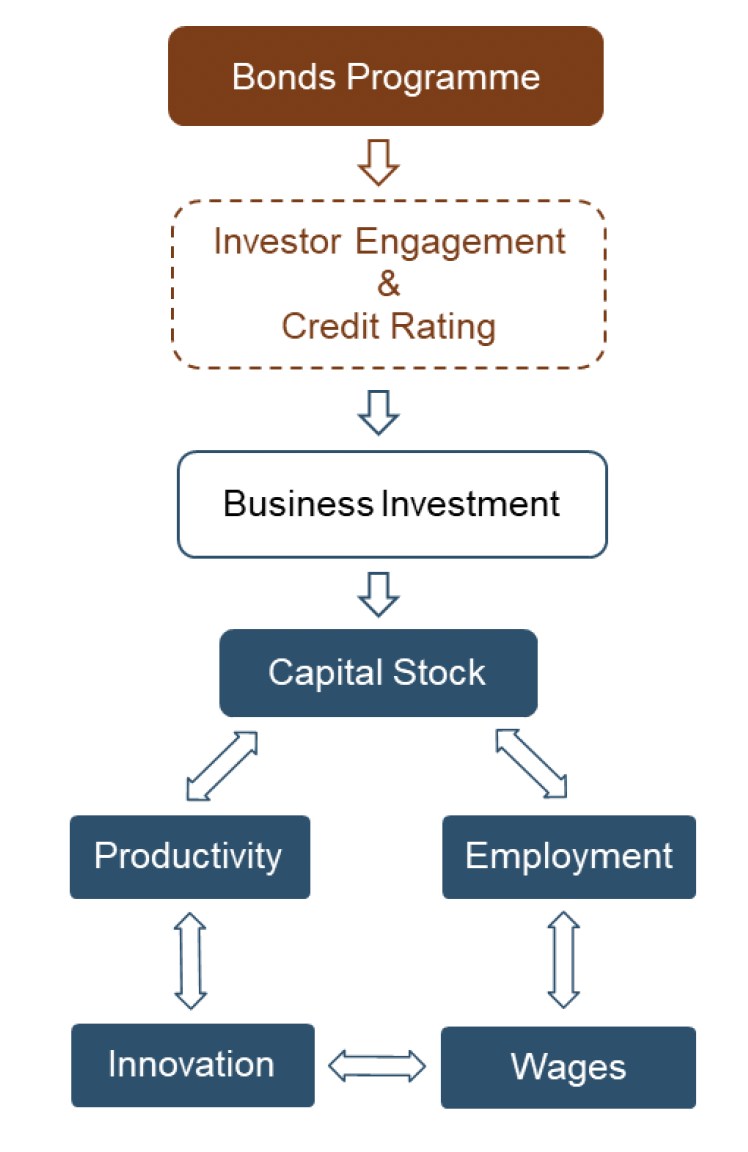

There are a range of quantifiable and non-quantifiable benefits from a potential bond issuance. The Scottish Government currently borrows from the National Loans Fund. From a financial management perspective, accessing alternative sources of borrowing will give access to different repayment structures, which could offer greater flexibility and other benefits, such as increased fiscal discipline. These are discussed in more detail in the section ‘Financial Case’.

In addition, there are a range of potential wider economic benefits, which flow through two main channels:

- Improving information about Scotland’s economy - credit ratings provide essential information to investors, helping them benchmark risks. The credit ratings from Moody’s and S&P Global are a public endorsement of Scotland as a high investment grade country.

- Improving networks and intermediation in the economy - providing more opportunities for investors to learn about investment opportunities in the Scottish economy.

These reflect the Investor Panel recommendation that the Scottish Government should consider issuing debt in international capital markets to raise Scotland’s profile and promote its investment story. This aligns with existing economic policy priorities, which aim to improve investor engagement and market visibility. There is strong evidence that increasing private capital investment supports business growth, productivity, and innovation. Addressing Scotland’s historic under-investment – particularly in business and infrastructure – could help close the productivity gap with international peers.[5]

Inward investment, including FDI, plays a critical role in Scotland’s economy.[6] Although foreign-owned businesses make up just over 3% of all businesses, they account for a disproportionate share of employment, exports, and R&D. Foreign-owned firms tend to be more productive and pay higher wages, with positive spillovers to domestic firms. Research shows that once a foreign investor enters a market, the likelihood of further investment increases – highlighting the importance of attracting a broad base of first-time investors.[7]

A bond programme could enhance Scotland’s visibility and credibility with investors. Sovereign and sub-sovereign credit ratings serve as trusted indicators of financial stability and risk, acting as an economic barometer and a source of information for investors. Participation in international capital markets and a credit rating could play an important role in reaching relatively uninformed investors, potentially expanding the investor base in Scotland.

Whilst the channels through which increased investment can benefit the economy are well established, it is not possible to directly quantify how much investment would arise directly from the programme. Overall, however, a bond programme and credit rating have the potential to act as a signal of economic confidence and support broader investment goals in Scotland.

Costs

The costs of a bond issuance cover Scottish Government expenses associated with supporting the issuance and ongoing reporting procedures, procuring expert advice, and the differential interest costs associated with a bond issuance compared to NLF borrowing.

In line with HM Treasury Green Book principles, costs have been analysed in real terms, removing the effect of inflation. The standard Green Book social time preference rate has been used to discount future costs. Applying this approach to costs provides a set of consistent costs for comparing between options, referred to as present value costs.

In practice, forecasting market conditions several years ahead is challenging. Although current interest rates across different maturities can be used to infer expectations of future rates, in practice future interest rates are uncertain and may differ – especially beyond the short-term horizon. The wider business case also considers potential future Scottish Government credit spreads as part of the scenario analysis. These assumptions are not being published at this time due to commercial sensitivity.[8]

All scenarios in the business case assume that the Scottish Government will borrow £300 million per annum over a 10-year period.

The figures above show the range of total present value of additional costs in 2024-25 prices across different issuance options compared to borrowing via the NLF. This range is influenced by the tenor of the issue, market interest rates and the assumed credit spread. The range covers all potential tenors and also includes more extreme market scenarios, such as a substantial increase or decrease in wider interest rates. The equivalent annual cost per bond, relative to the cost of equivalent borrowing from the NLF, is also presented. It is calculated using the total present value of costs, the number of bonds issued over the period and the years during which additional costs will be incurred over NLF borrowing. Annual costs per bond for a programme of issuance are lower than annual costs for a single issuance as fixed costs, such as staffing and reporting costs, are spread over multiple issuances.

The actual borrowing policy can be refined to consider different combinations of tenors, amounts, market conditions and timing of issuance, whereas options and costs presented in the business case are kept high level to provide an illustration of potential costs and benefits.

Comparison of costs and benefits

As with all appraisals, the comparison of costs and benefits involves a mixture of quantified and unquantified elements. For benefits, whilst some of the fiscal benefits of bond issuance will be captured in the present value of costs other benefits are harder to quantify. This includes increased flexibility from diverse sources of borrowing and potential for improved fiscal discipline. The repayment profile of bonds also differs from NLF borrowing in that the principal is repaid in full at maturity, rather than through equal instalments over the life of the issuance. This structure would release funding in the earlier years, but necessitate a larger allocation for principal repayment at maturity. This is set out in further detail in the charts in the annex and in the next section.

As noted above, whilst it is possible to quantify the economic benefits associated with greater investment, there is significant uncertainty as to how much investment will be attracted. Similarly, on the cost side, whilst most costs are captured through the present value of borrowing costs – which will be driven by market conditions several years down the line and are subject to uncertainty – there may be other risks and costs excluded from this analysis that are harder to quantify.

A decision to issue a green bond – a debt instrument used to finance projects with clear environmental benefits – may also have an impact on cost and benefits. Final decisions on formal Use of Proceeds structures (such as Green or Sustainability Bonds) will be made closer to issuance – at this stage the Scottish Government is confident in the strategic alignment and is likely to be able to fulfil the associated standards for Green Bonds. However, it is considered prudent at this stage to retain flexibility and keep all options open.

As a consequence, the current cost-benefit assessment does not account for any additional impacts from issuing a labelled (or green) bond. These impacts will be discussed in future versions of the Business Case.

Analysis suggests that Bonds, in a multi-year programme of some form, and subject to market conditions could (on a discounted basis) either generate small savings or (more likely) additional annual costs of less than £2 million per bond issued, based on a prudent assumption about the potential spread between any future Scottish Government bond and UK gilts. The Scottish Government achieving a high investment grade rating and parity with the UK Government – as confirmed by Moody’s and S&P Global - provides strong evidence that the actual spread is likely to be narrower than the prudent assumption underpinning the business case.

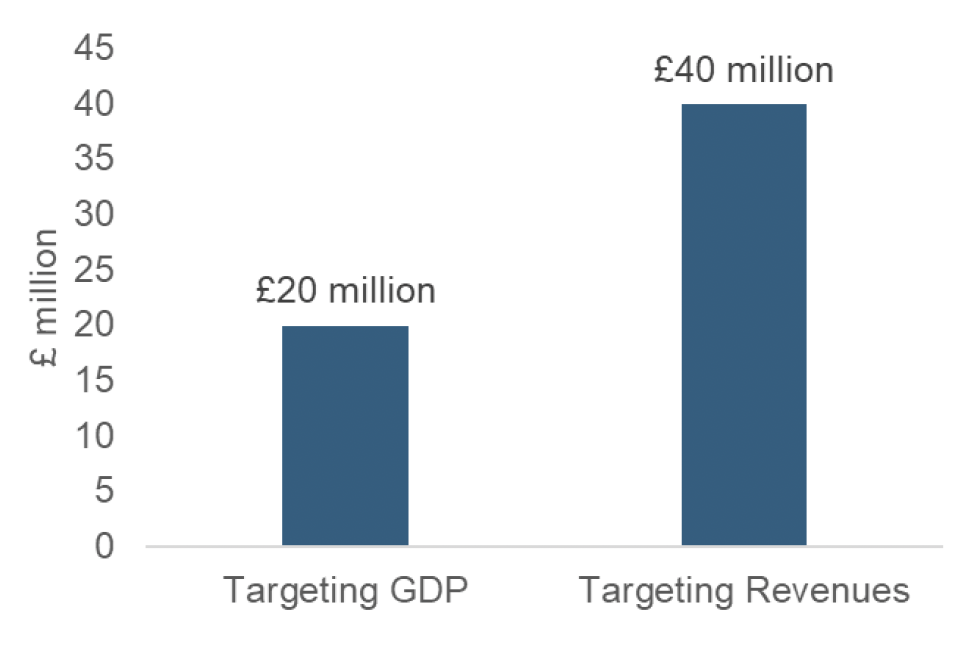

The bonds programme and a credit rating could enhance Scotland’s investment profile and attract additional investment. Rather than quantify the benefits associated with this directly, the analysis below considers the increase in investment that would be required for the economic benefits to at least offset any costs, that is, for the programme to have a Benefit Cost Ratio (BCR) of 1. [9]

A macroeconomic model of Scotland is used to estimate the increase in business investment required to offset the additional lifetime costs associated with a bond programme either through an increase in GDP or public revenues. Taking one of the possible options for a multi-year programme from the range presented earlier in this section, the modelling results suggest that a permanent annual increase in investment of 0.1% to 0.2% would be needed to achieve a Benefit Cost Ratio of 1. In this example, an increase in investment is equivalent to £20 to £40 million, based on the current level of annual business investment in Scotland. The modelled increases required to achieve a BCR of 1 are relatively small compared to annual changes in business investment in Scotland, suggesting that only a modest amount of additional investment is needed to reach this threshold.

As such, there is high confidence that bond issuance would deliver value for money, if it attracts additional investment into Scotland. Compared to a single issuance (Option B), a multi-year programme (Options C and D) is more likely to maximise economic benefits through continuous engagement with investors, regular financial reporting and a sustained presence in international debt markets.

Contact

Email: OCEABusiness@gov.scot