Scottish Exchequer: fiscal transparency discovery report

This report seeks to understand the accessibility and connectedness of current fiscal information and data and describes how we could implement improved fiscal transparency services and the benefits that could generate.

3 Requirements Definition

This section describes what a future Scottish fiscal transparency solution could look like.

3.1 To-be Stakeholders

The initial set of future fiscal transparency stakeholders is likely to be the same as the stakeholders shown in Section 2.8 above. However, a number of interviewees have stressed that it is difficult to predict who the users of fiscal transparency services will be, and that there will be unexpected users. Others have suggested that ordinary people do not necessarily access government finance data, or become "armchair auditors", even when it is made more easily available.

A number of interviewees recommended that the Scottish Government think about who will be the "intermediaries" – the people who will generate value by placing the data in a useful context and make it understandable/useful for people with particular interests. Although others warned, however, that intermediaries will always have their own agendas so it is important that there is direct provision of data in an understandable form, as well as raw data.

3.2 Benefits and Measures of Success

This assessment of the possible benefits of improved fiscal transparency is based on our user research with external stakeholders, our conversations with internal stakeholders, and our international research into the benefits achieved by improved government fiscal transparency.

We have identified beneficiaries in three main areas, i.e.:

- Benefits to citizens and businesses - such as better targeted resource allocations and improved input to government policies, as well as long term economic benefits to the whole country;

- The government as a whole - e.g. via improved reputation; greater trust in its data; a fuller understanding of how public finances are managed and more productive discussions with citizens and stakeholders - all leading to more effective polices and improved outcomes. There are also benefits for fiscal sustainability;

- Government administrative functions - i.e. by improving the functions of government employees, for example by improving the efficiency with which data is produced and published, or by more effective consultations.

This diagram summarises the key benefits of fiscal transparency, showing how benefits occur at these different levels.

Benefits

Citizens, external stakeholders, business and the economy

Primary Benefit (Fiscally aware culture within Government and across Scotland supporting more effective Government)

- More timely information

- Clearer fiscal understanding (less myths)

- Better resource allocations

- Better policies, decisions and outcomes

- Better consultations and stakeholder conversations

- More transparency

- Meets enhanced public expectations

- More accountability and trust

Wider Benefit

- More Inward Investment

- Improved fiscal analysis

- More small and medium size enterprise (SME) opportunities

- Improved business innovation, creation and efficiency

- Increased financial expertise

Government as a whole

Primary Benefit (Fiscally aware culture within Government and across Scotland supporting more effective Government)

- Better resource allocations

- Better policies, decisions and outcomes

- Better consultations and stakeholder conversations

- More transparency

- Meets enhanced public expectations

- More accountability and trust

- Reduced fraud

- Reduced uncertainty

- Meets Open Government commitments

- Improved credibility and confidence in government

Wider benefits

- More cross-nation comparisons

- Better credit ratings

- Improved tax compliance

Government administration

Wider benefits

- Easier Audits

- Improved information collection and publication

- Improved tax compliance

- Better consultations

- Improved data quality

And in more detail:

| Benefit | Main Beneficiaries | Source |

|---|---|---|

| 1. Investment in improving the underpinning sources of fiscal information within the Scottish Government will make the generation of other fiscal outputs easier, not just in the transparency area. | Admin | International Research |

| 2. Publishing data and information improves data quality, because the act of publishing it forces better internal quality as a result of feedback from external users, e.g. checking of consistency and gaps. | Admin | International Research |

| 3. Better and more accessible fiscal data leads to easier audits. | Admin | International Research |

| 4. Better data to support stakeholder and public consultations. | Gov, Admin | Internal and International Research |

| 5. Good guidance and tax calculators increases tax compliance and hence government revenue (upstream compliance) and reduces administration costs downstream. | Gov, Admin | Revenue Scotland |

| 6. Improved fiscal transparency is in line with the broader commitment by the Scottish Government to open government, including membership of the Open Government Partnership and as described in Scotland's Open Government Action Plan: 2018-2020. | Gov | Internal research |

| 7. Meets public and media expectations for accessible information from governments on matters of public interest. This is likely to have been increased by the recent considerable public and media interest in the presentation of accessible data on the COVID-19 situation with a corresponding increased investment in enhanced data visualisation and open data – for example see the Public Health Scotland COVID-19 Daily Dashboard and the UK Covid data portal. | Gov | Internal Research |

| 8. A more transparent fiscal system could be expected to provide policy makers with incentives to adopt better policies: it reduces the scope for special interest groups and rent-seekers to influence policy and provides public recognition for policies that credibly improve public finances. Better fiscal and economic outcomes, in turn, would reduce the risk of sovereign default reflected in better credit ratings. | Gov | (1), External Research |

| 9. Improved government outcomes through better quality of policy decisions (more evidence-based, more effective citizen input, clearer fiscal and other implications), and increased scrutiny (including at local level) leading to more effective/impactful resource allocations and implementations. | Gov | International Research |

| 10. Supports efforts to minimise fraud and avoid conflicts of interest by providing legislatures, oversight bodies, markets and citizens with the information they need to hold governments accountable. | Gov | IMF |

| 11. Improved accountability, including about the complete fiscal position, long-term costs and benefits of policy changes, and potential fiscal risks. | Gov | IMF External Research |

| 12. Helps achieve financial and economic stability and strengthens the credibility of a country's fiscal plans. | Gov | IMF |

| 13. Reduced uncertainty associated with a given set of fiscal and financial policies, i.e. reducing economic agents' uncertainty around the expected fiscal outcomes, even with unchanged policies. More clarity regarding future fiscal policies and risks would help lower the risk premium set by credit rating agencies, and/or improve access to emergency funding from international organisations (should these be sought in the future). | Gov | (1) |

| 14. Good fiscal data is more likely to lead to inclusion in cross-nation fiscal comparisons, which is valuable for small countries with limited resources to do their own assessments. | Gov | International Research |

| 15. Fiscal transparency encourages more transparency in other parts of government and society - it a by-product and an enabler. | Gov, Citizens | (4) |

| 16. Authoritative and accessible data fosters trust and confidence amongst stakeholders and the public – at national and local levels. | Gov, Citizens | Revenue Scotland, External and International Research |

| 17. Boosts financial market and citizen confidence. | Gov, Economy, Citizens | International Research |

| 18. Reduces the incidence and severity of crises by supporting a timely and smooth fiscal policy response to changing economic conditions. | Gov, Economy, Citizens | International and External Research |

| 19. Better fiscal evidence leads to better resource allocations (which must be measured in a quantitative and qualitative fashion), and more efficient reallocations of spending. | Gov, Economy, Citizens | (4), External Research |

| 20. Consistent, good quality, accessible fiscal data is needed to support informed stakeholder conversations - both internally and externally. It will lead to increased - or more informed - citizen engagement with, and input to, Government decisions. | Gov, Citizens | Revenue Scotland, External Research |

| 21. External agencies will need to spend less time searching for fiscal data, cleaning it up and linking the datasets. This means they can respond quicker and more fully to requests for assistance and / or complete more comprehensive analysis. | Gov, Citizens | External Research |

| 22. Better fiscal transparency will support increased research to inform government decision-making and improve public awareness (by researchers/academics, think tanks, international organisations etc), including policy/service choices and trade-offs (the "difficult decisions"). | Gov, Citizens | International Research |

| 23. Fiscal information will be more accessible and understandable for the wider media, meaning they are more likely to disseminate the information and hence create better civic engagement and understanding. | Gov, Citizens | External Research |

| 24. People and business will be more willing to pay taxes if they know what they are spent on. | Gov, Economy, Citizens | Tax team |

| 25. Better information on Scottish taxes will help to dispel myths about the tax levels in Scotland. | Gov, Economy, Citizens | Tax team |

| 26. Publicising information about tax compliance increases citizens' willingness to pay taxes. | Gov, Economy | (2) |

| 27. International research suggests that improved fiscal transparency creates more opportunities for a more diverse and increased number of small and medium sized companies to bid for and win government contracts. For example South Africa has used publication of contract information to encourage more black- and female-led companies to bid for government contracts. And Ukraine was also cited as a good example of digital access increasing the number of bids for Government contracts. | Gov, Economy | International Research (5) |

| 28. Benefits to businesses in 3 key areas: business innovation, business creation and business efficiency. For example broader and more rapid access to data will make it easier for researchers and businesses to build on Government research. Opportunities may be created for Open Data inspired products or services to add value to the data generated by public bodies. | Economy | International Research |

| 29. Additional inward investment inflows associated with fiscal transparency during the budget execution phase. This effect is additional to those associated with general government transparency, and also additional to those found from related factors such as the quality of institutions, control of corruption and quality of regulation. All else being equal, governments that are more transparent are more likely to receive private investment flows. | Economy, Citizens | (3) International Research |

| 30. With the new powers, there's a big opportunity in Scotland to attract budding economists and finance experts that would in the past move to London. Fiscal transparency will help to make this even more likely. | Citizens | External Research |

| 31. More timely information as a result of better digital outputs – as highlighted by the COVID-19 crisis. | Citizens, Admin | International Research, External Research |

| 32. Improved digital fiscal transparency enables users to search for areas of particular interest which would be impossible or unduly time-consuming or costly to undertake from hard copy or PDF sources. | Citizens | International Research |

Sources

(1) IMF study - Fiscal Transparency, Fiscal Performance and Credit Ratings

(3) Science Direct, Assessing the impact of fiscal transparency on foreign direct investment inflows

(4) Discussions with Mexican government representative

(5) Gov.uk Digital Marketplace

Discussion

Our research suggests that there are many possible benefits from improved fiscal transparency. Some will be achieved relatively automatically, whereas others will require additional/complementary activity with the availability of clear fiscal information a positive starting point for wider engagement or participation.

One international interviewee argued that transparency is a "normative good" – that governments should be transparent, whether or not this provides public goods (including economic benefits) or not.

Measuring the benefits

Many of the benefits of improved fiscal transparency described above are qualitative, and hence hard to measure. And while there will be quantitative benefits, e.g. in areas such as improved inward investment, tax revenues and reduced administration costs – these will be very difficult to separate from other possible causes.

Hence the best way to measure benefits may be by means of ongoing engagement with internal and external stakeholders to gather their opinions on the benefits arising from fiscal transparency. One interviewee suggested that the extent of diversity of end users who are demonstrably using a fiscal transparency portal is a good key performance indicator.

It is also important to avoid treating metrics as measure of success – successful transparency is not just about the number of visits or downloads from a fiscal transparency portal.

3.3 High Level Goals

A Scottish Government fiscal transparency service will have the following high-level goals. The provision of information that is comprehensive, accurate, linked and up-to-date is a prerequisite for all the other objectives.

It should be noted that the desire is to make the existing large amount of fiscal information more accessible and understandable. It is not about publishing more, new or different information, or publishing it at different frequencies to the current approach.

Goals for fiscal transparency services

- To provide, comprehensive, accurate, up to date and linked fiscal information that can be trusted, that enables:

- Open fiscal data that people can easily re-use; and

- The presentation of accessible, usable and understandable fiscal information to a wide range of users, including the general public; that enables:

- The utilisation of other agents of fiscal transparency to achieve shared goals; and

- Improved understanding and engagement on all elements of the Scottish fiscal landscape.

3.4 Scope Definition

Scope of responsibilities

As discussed in Section 2.5 there are many Scottish Government directorates and other organisations (including non-public sector bodies) who currently own and/or publish Scottish fiscal information. In many areas there are overlaps and connections between the type of information held by organisations, as summarised here. The fiscal transparency programme needs to develop a strategy that takes this pattern of information ownership and publication into consideration when deciding on the scope of future fiscal transparency services – both initially and in the longer term.

It is important that organisations that publish fiscal data are responsible for the accuracy of the presentation – even if they were not the original producers of the data. So for example data must be linked and interpreted correctly. Within the wider public sector information needs to be consistent. Wherever possible data should be combined and published in one place to minimise duplication and the resulting increased chance of confusion and inconsistencies.

The Scottish Government areas who own and produce fiscal data are accountable for the accuracy and quality of the data that they produce, and any data that they publish themselves. But they cannot take responsibility for data used and published by third parties.

A core fiscal transparency portal could signpost to other published fiscal information. However it needs to be decided what warnings or endorsements are given with regard to the accuracy of these other outputs.

Scope

Core data

- Core Scottish Fiscal, Financial and Economic (economic analysis, all central government revenue, all budget information, accounts, capital and infrastructure plans, local authority spend summary, climate change and equalities budget assessments)

Other relevant data, owned by:

- Public Contracts Scotland (contract spend)

- Public Health Scotland (NHS Board spend)

- Other Scottish Government Directorates and Agencies

- Scottish Fiscal Commission (budget and revenue analysis; tax forecasts)

- SPICe (mainly budget information)

- Audit Scotland (accounts/audit)

- Revenue Scotland (LBTT and Landfill Tax)

- Local Authorities x 32 (revenue, spend and outcomes)

- Improvement Service (revenue, spend and outcomes)

- UK Government (HMRC, OBR – UK Tax data) (HM Treasury – Block Grant Data)

Scope of types of information

As discussed in Section 2, the target scope of fiscal transparency information for the project includes:

- Any data or text relating to revenue and spend of the Scottish public sector, including economic analysis and forecasting relating to revenue and spend;

- Information on the main Scottish Government budget;

- Procurement and contract spend data and related information;

- Information on grants made by the Scottish public sector, including information on the recipients;

- The details of the budgets, accounts, actual spend, performance and outcomes of the associated delivery directorates, agencies, health boards and local authorities.

For the purposes of the project it excludes non-fiscal economic data, e.g. employment, gross domestic product, business turnover. It also excludes spend by the UK Government in Scotland. These assumptions should be verified in the next phase of the project.

Fiscal transparency is about a broad set of linked fiscal information, in a wider sense than just data – so including unstructured documents and text.

Tax calculators and guidance

Parts of the Scottish and UK governments publish information on how the Scottish tax arrangements impact on Scottish residents and businesses, for example:

- the Non-Domestic Rates Calculator;

- Calculators and guidance for Land and Buildings Transaction Tax

- the Scottish income tax calculator (and non-government calculators, e.g. the WHICH? non-government calculator).

These types of information services are considered to be outwith the scope of improved fiscal transparency services as they do not involve the reporting of fiscal data or information (although tax calculators can be a useful way to increase awareness of income distribution and help explain rationale for tax policy decisions). They should be signposted from a possible central fiscal transparency portal.

General government transparency

The Scottish Government needs to consider if in the long term it wants to expand a fiscal transparency portal to hold a wider set of non-fiscal government information, e.g. on demographics, health, the economy and other government activities, similar to the French Government public data site. The next stage of the project could investigate whether this is something that is being considered elsewhere in government. As previously noted, the Scottish statistics open data portal already gives open access to over 250 datasets from a range of producers, although with a focus on open data.

3.5 User Needs

Based on our conversations with the wide range of internal and external stakeholders we have engaged with during this study, and on our research into international best practice and examples, we believe that the goals and scope defined above can be met by incrementally developing a fiscal transparency service that meets the user needs defined below.

Information sources

Need: Consolidated and linked source data for fiscal transparency reporting

The current data sources are not a suitable source platform for improved fiscal transparency reporting. As far as possible data needs to be consolidated into one place, with proper linkages between data, built-in data quality controls, and efficient population of the data. Data must be consistent. Scottish Government data maturity approaches should be followed.

So that …

- Fiscal transparency outputs can be efficiently generated with minimum manual intervention

- Improved data quality

- Better data integration.

Need: Traceability and integrity

Users need a clear understanding of where the information and data presented has come from.

As shown in Section 2.8 there are several organisations currently publishing Scottish fiscal information, who own the data they publish. This includes data owned, or jointly owned with UK government, e.g. Barnett consequentials, and fiscal reconciliations under the fiscal framework.

So that …

- Users can trust the integrity and accuracy of the fiscal outputs when they come directly from the government.

Need: Up-to-date and complete data

For example on budget revisions, details of delivery spend, the current tax status, borrowing, block grant adjustments and the Scottish reserve position.

For all outputs the date of publication date and the version needs to be clearly stated so that the most recent set of information is clear.

It should be noted that some kinds of data would be hard to show in a timelier way, for example accounts outputs, which are collected after the financial year end after they have been audited.

The completeness of the datasets needs to be explained.

All relevant documents should be included – including guidance notes, other instrumental or key decision-making documents such a framework/strategy documents, governance or review documents. Some of these may be more important to understand allocations and decisions than a row of financial data, or are critical to understand a budget line.

So that …

- Users can have more confidence in the accuracy, coverage and timeliness of the data

- User can properly understand the information.

Content

Need: Better integration of fiscal transparency information

The ability to group and assess fiscal information by key categories and themes e.g. National Performance Framework components,[2] equalities[3] and human rights themes, policies, demographics, portfolios, economic sectors and geographies – at all levels of the budget.

The ability to view fiscal transparency information over time – to show trends.

There needs to be a better way to account for changes in portfolio responsibilities and name changes.

There is also a need to show linkages between taxes, spend and performance, and between portfolios.

The interconnections with the UK tax situation is complex and could be better shown.

So that …

- A better view of the connections across the Scottish and UK fiscal landscape

- Budgets and spend can be assessed against themes, outcomes or geographic areas

- Long term trends can be assessed

- Like-for-like comparisons can be made.

Need: Detailed and integrated data on spending, outcomes and performance by delivery organisations, at a more granular level

For example by NHS Boards, Scottish local authorities and agencies, linked to budget data - showing things that people and businesses care about.

Categorised in a consistent way by the key themes described above.

Research undertaken for this study suggests that performance data needs to be linked to finance data, and vice versa. On their own they have less meaning, i.e. the inputs need to be known to make a judgement about performance.

Inputs (i.e., finance data) and performance data should be linked to the relevant level of accountability (geographic, organisational unit, institution, level of government), for accountability purposes and, more specifically, to inform citizens in the context of elections.

Greater disaggregation is seen as better than less ("drill down, go deep") although the more detailed a portal becomes, the harder it can be to navigate.

So that …

- Spend can be assessed against outcomes or geographic areas

- Detailed spend can be linked to budget areas

- Outcomes can be mapped to spend and organisations

- A better view on who is benefitting from spend

- Users can "follow the money", i.e. see who is using the money and why

- Government itself can assess efficiency, support improvement and make better informed decisions.

Need: Improved access to current documents and data

For example via a searchable "catalogue" of outputs and advanced search capabilities.

Given the size of many documents just finding the right document would not be enough – users need to be able to find specific content in a document or data source. Documents need to have an accessible summary, an explanation, and must be placed in context.

Additional documents should be published in some areas, e.g. the Provisional Outturn Statement. Outputs produced in response to ad hoc requests for information should also be published wherever possible.

It needs to be decided how the current outputs can be better adapted to public consumption.

So that …

- All users can more easily find the correct content in the right document.

Need: Clear information on the Scottish fiscal arrangements, processes, responsibilities and outputs.

Using effective communications approaches such as infographics, and easily understood language.

For example to explain the budget process, or the way long term capital spend is forecast and allocated, or how the reconciliation process works.

The reserved/devolved split needs to be reflected and explained – where the money comes from and what it is spent on – at both UK Government and Scottish Government and Scottish Government/local government levels.

A glossary of fiscal and relevant government terms would also be useful.

So that …

- Users understand the context and background to the data presented

- Users develop a better understanding of Scottish fiscal processes.

Need: Improved fiscal planning and budget content

Including:

- An intuitive view of the planning and budget processes, and related outputs, for example the financial strategy outputs, Capital Spending Reviews, Infrastructure Investment Plans, draft and final budgets, carbon assessments, Barnet consequentials and budget revisions

- The possible publication of a short accessible people's or citizen's budget in addition to the main budget document. However it should be noted that an Organisation for Economic Cooperation and Development interviewee suggested that some countries are pulling back from citizen's budget documents because they can be seen as patronising, and instead effort should be put into making the main budget documents more accessible.

- A possible pre-budget statement that would disclose the broad parameters of the fiscal policy priorities in advance of the executive budget proposal

- Presentation of outputs based on the planning and budget cycle

So that …

- Users have a better view of the stages in the planning and budget lifecycles

- User can see how budgets evolve and translate into spend

- Users better understand the purpose and context of outputs.

Presentation

Need: A single place to access all Scottish fiscal information

i.e. some form of fiscal transparency portal.

This should include signposting to information owned and published by other bodies, e.g. Scottish Parliament Information Centre, Scottish local authorities, NHS Boards, and potentially non-Government organisations such as Fraser of Allander Institute.

It needs to be decided what warnings or endorsements are given with regard to the accuracy and quality of information published by other bodies. The Scottish Exchequer will not be able to fully verify these outputs, and signposting cannot be taken as a guarantee of quality.

Wherever possible sites with similar information should be combined, in order to minimise and simplify the number of sites publishing fiscal information.

A portal must include a powerful search facility across the whole set of fiscal information, e.g. using natural language questions. There is a need to think through carefully the types of searches that different users will want to do.

Information should be provided on how datasets relate to each other, e.g. the relationship between different levels of Government or with wider arms-length bodies.

It needs to be decided how such a portal would be branded, e.g. as core Scottish Government service, or with a distinct identity.

It needs to be decided if and where fiscal outputs should continue to be published on the Scottish Government website.

Contact details should be provided for requests for clarity and further information.

Search engine maximisation must be undertaken to ensure that users can quickly find a fiscal transparency portal.

So that …

- Users know where to start looking for information on the Scottish fiscal situation.

Need: Data to be presented in a more usable format

Currently large amounts of data is presented as tables in pdf documents or HTML pages. As a minimum data should also be presented in spreadsheet format, and ideally in an open format in line with international open data standards. It needs to be decided if open data is delivered via an open data portal such as the Open access to Scotland's Official Statistics Site, or in the same place as the related data visualisations and tables – or in both places. Data should be split up more, be properly described and of good quality.

There should be a verifiable link for data that is going to be shared onwards.

Some existing spreadsheet outputs could be improved to be more accessible, usable and understandable, e.g. the over £25k spend spreadsheet and the Level 4 budget spreadsheet (although it is recognised that this spreadsheet only represents a point in the development of the annual budget).

So that …

- Users can more easily extract and process data, e.g. intermediaries and researchers will want to be able to take the raw data, scrutinise it, and re-present it in their own desired formats.

Need: Improved data visualisation and explanations

Most current visualisations of fiscal data are embedded in pdf documents and html pages as static images.

Data needs to be presented in a more interactive way, using data visualisation technology and infographics. Visualisations need to be properly explained and set in the correct context. The associated source data needs to be available in the same place.

Geospatial data should be presented via interactive maps.

Data could be explained in an innovative way, for example in comparative terms (e.g. infrastructure spend in comparison to spend on the new Forth Crossing), or by comparison with spending in other countries or other parts of the economy.

The story behind the data needs to be explained – e.g. including a suite of explanatory material that weaves together the information, charts and the explanation. The completeness of the datasets needs to be explained.

It needs to be decided if improved visualisations and outputs should be addition to current documents, or within the documents.

So that …

- Fiscal transparency outputs are more engaging, understandable and accessible to wider range of users.

Need: Accessible and usable outputs

Fiscal transparency outputs must maximise accessibility and usability, including by:

- Ensuring websites, tools, and technologies are designed and developed to maximise ease of use by people with disabilities (see Section 3.7 for further details on accessibility and data visualisation)

- Use clear and consistent layout and design choices to maximise usability

- User clear and simple language avoiding technical terms

- Developing outputs that are designed to function in an adaptive fashion on a wide range of devices and software, including operating systems and browsers

- Minimal navigation to get to an output.

So that …

- Users with disabilities are not disadvantaged

- All users can easily navigate and understand outputs on a wide range of devices and software.

Need: Flexibility

A portal must be able to include new information from new or existing sources that become important – for example, in the context of emergencies such as COVID-19.

So that …

- Fiscal transparency services remain current and relevant

Collaboration and communication

Need: Improved two-way communication with users and stakeholders

Including improved communication via social media, online announcements, and online feedback facilities.

Maximum use should be made of high-profile events like the Scottish and UK budgets to publicise outputs.

So that …

- Users are more aware of fiscal transparency outputs

- Users can provide feedback to the Scottish Government in areas like data quality, requests for clarifications and requests for new outputs.

Need: Development of fiscal transparency outputs based on a good understanding of user needs and usage

Potentially including the use of:

- Web analytics to provide data on usage

- Communication with users via mechanisms such as user groups, discussion forms and hackathons

- Ongoing user research.

All feeding into established business processes to act on the information to improve outputs.

So that …

- Fiscal transparency outputs can be iteratively improved based on a real understanding of user needs

- Users know that their ideas and usage is being taken into consideration.

Need: Collaboration and integration with other publishers and consumers of fiscal information

There are a number of Scottish Government directorates, other Scottish public sector bodies and other organisations with an overlapping interest in fiscal transparency, including:

- Core Scottish Government areas, including the Scottish Exchequer and Financial Management Directorate, Chief economist Directorate, Health and Social Care, Economy, Communities and Procurement

- Associated government bodies the Scottish Fiscal Commission, Revenue Scotland and Public Contracts Scotland

- Local Authorities and Scottish public sector organisation who own and publish fiscal data, e.g. NHS Boards, regulatory agencies and delivery bodies.

- The Scottish Parliament, including the Scottish Parliament's Information Centre

- External think tanks like the Fraser of Allander Institute, the Institute for Public Policy Research, the Institute for Fiscal Studies and the Global Initiative for Fiscal Transparency.

All these organisations publish their own fiscal related data and/or consume fiscal data from parts of the Scottish Government, or from external sources. They all have useful skills in data visualisation and a good understanding of the Scottish fiscal landscape, or their delivery areas.

There is a requirement for all areas to collaborate in order to improve Scottish fiscal transparency. A clear understanding of overall objectives, aims, scope, skills, knowledge, priorities, ownership and responsibilities is needed.

So that …

- The Scottish Government can leverage the skills and experience of all organisations interested in improving fiscal transparency in Scotland

- Full use can be made of the available data on public sector revenue, spend and outcomes.

- Duplications, inconsistencies and omissions can be minimised.

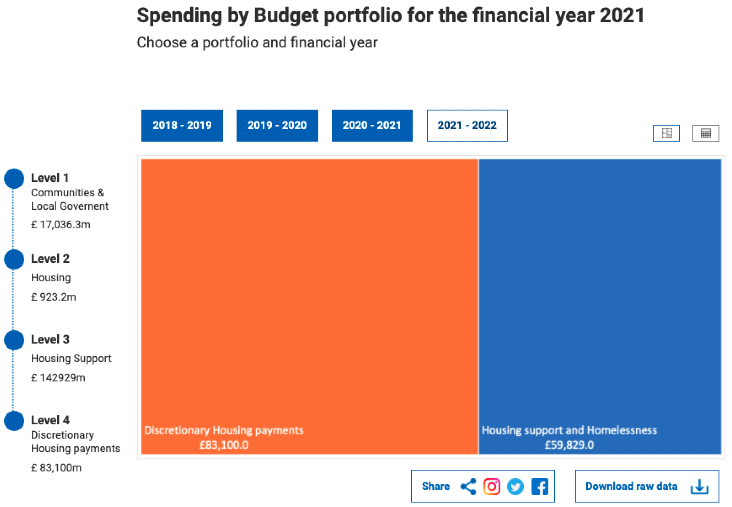

3.6 Speculative Mock-ups

Speculative mock-ups have been designed based on the findings from external user research, internal fact finding, international research and desk research – with inspiration from elements of data visualisation in other international fiscal transparency portals. Example user journeys were created, and from those pain points, opportunities (both short and long term) have been used to speculatively mock-up potential areas for further exploration later in the project. These mock-ups were developed with minimum knowledge of fiscal data and the structures that sit behind the data. In the future it would be beneficial for the designers to collaborate with subject matter experts in these areas.

Mock-up opportunities/screens include:

- Two approaches for a portal home page

- Budgetary spending data-levelled approach

- Geographical and outcome related representation of spending data

- Advanced data search and data visualisation generation.

The mock-ups are intended to show what could be possible in the future. During the Discovery phase we spoke to highly engaged current users, and so did not capture all potential user needs. There is a risk that these mock-ups, as designed at this early stage can introduce bias into the design, and there are a number of decisions that need to be made before designing anything this granular, therefore it is recommended that:

- Further research, design, iteration and testing is undertaken

- Content design is implemented using clear, consistent and accessible language

- An information architecture is defined

- Adhere to current guidance in the Digital Scotland design system and potentially work with them to design data visualisation into their system

- Branding work is carried out once ownership is established.

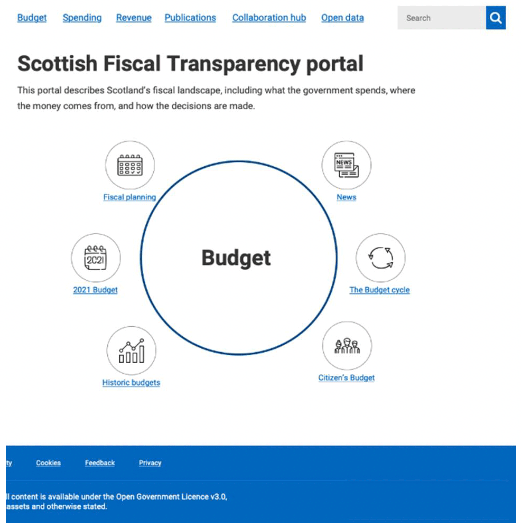

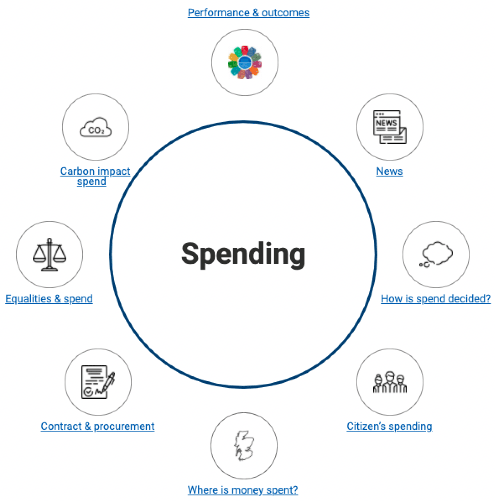

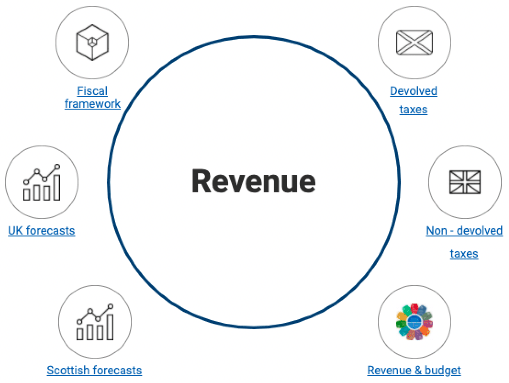

In both fiscal transparency portal approaches, the focus has been to explore the user need for a single place to access all Scottish fiscal information.

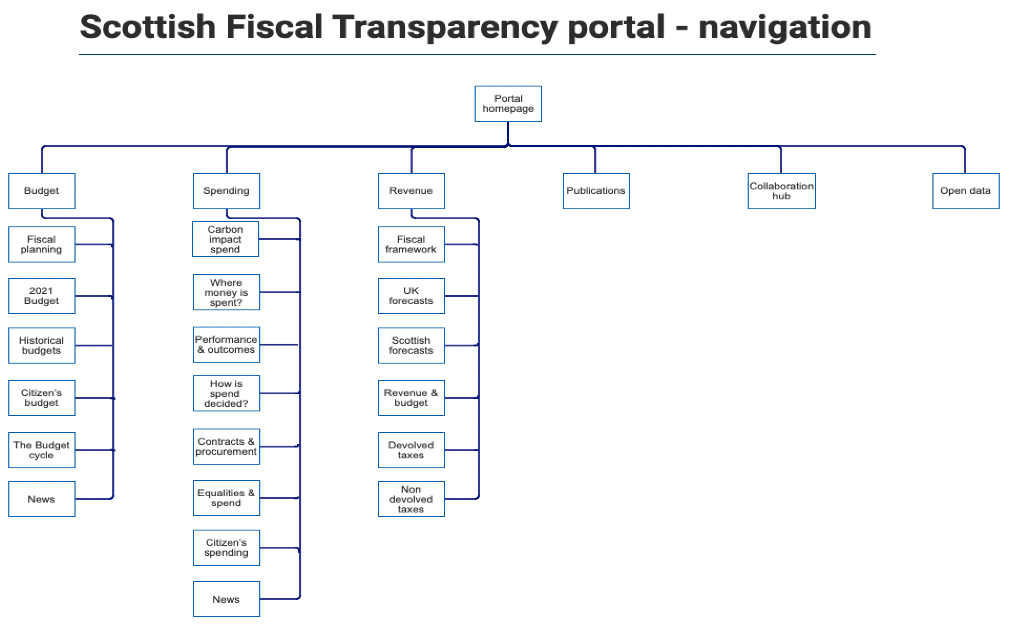

The navigation is structured using information that has been collected from our research. At the moment, we do not have a complete site map. This information architecture has been designed speculatively by grouping areas of a similar theme together to create the structure.

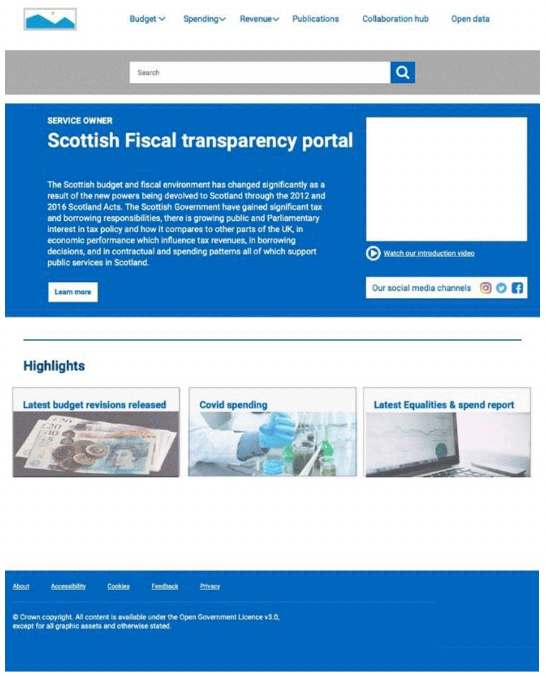

Fiscal transparency portal approach one

Fiscal transparency portal approach one was influenced by the Georgia Fiscal Transparency Portal (see Section 4). In this portal some of the identified opportunities from our user journeys are highlighted. These include:

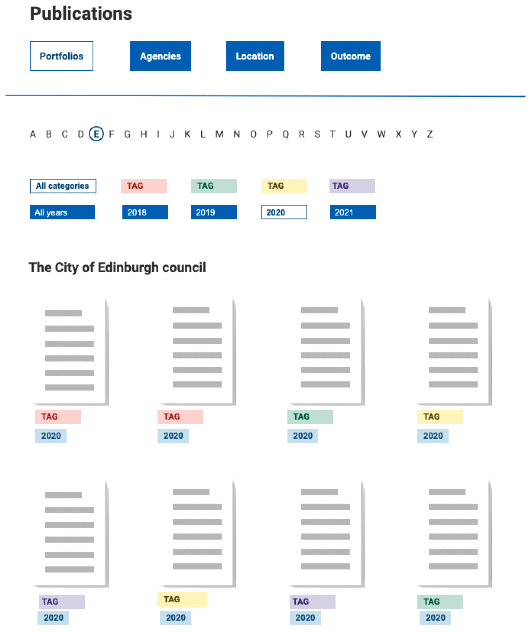

- Publications – to address the user need for improved access to the current documents and data. This could be a filterable, tagged catalogue containing all fiscal documents;

- A collaboration hub – to address the user need for a space for collaboration and integration with other producers, publishers and consumers of fiscal data;

- Searchability – a search bar is prioritised in the interface, because our overseas research showed searchability as being one of the main benefits of digital accessibility;

- Open data - this was identified as a key need from external research and portals that other countries have developed.

The publications screen is based on an example from the Australia Fiscal Transparency Portal. The publications can be filtered by portfolio, agency, location or outcome. Options to filter by tag, year or by first letter of the portfolio, agency etc. are also included. These design decisions were driven by the user need to access existing publications.

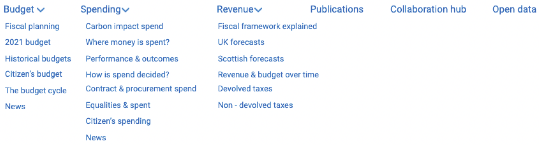

Fiscal transparency portal approach two

Fiscal transparency portal approach two uses styles and components from the Digital Scotland design system. This portal was influenced by the Brazil Fiscal Transparency Portal. Navigational cards have been used to display topical highlights that are relevant to fiscal data. Within the top-level navigation, sub-navigation is included for budget, spend and revenue. The requirements that have been focused on include:

- The use of social media platforms and explanation videos, based on a requirement to have improved two–way communication with users;

- Searchability – based on the overseas research described above.

Examples of data visualisation

Examples of data visualisation were designed based on some of the opportunities identified in our user journeys, and on inspiration from other fiscal transparency portals, with the Scottish context in mind.

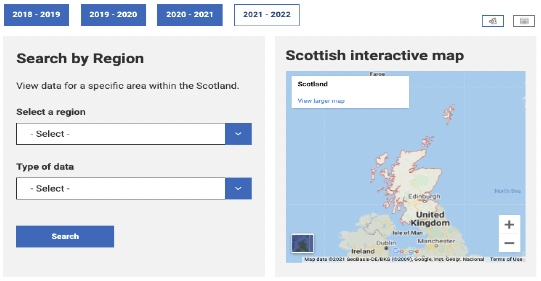

Data by geography:

The visualisation above is based on an example from the Brazil Fiscal Transparency Portal, designed to address the user need of better integration of fiscal transparency information. Focusing on the ability to be able to assess by key themes (geography and by data type). This data can be viewed in two ways, either by map or in a table.

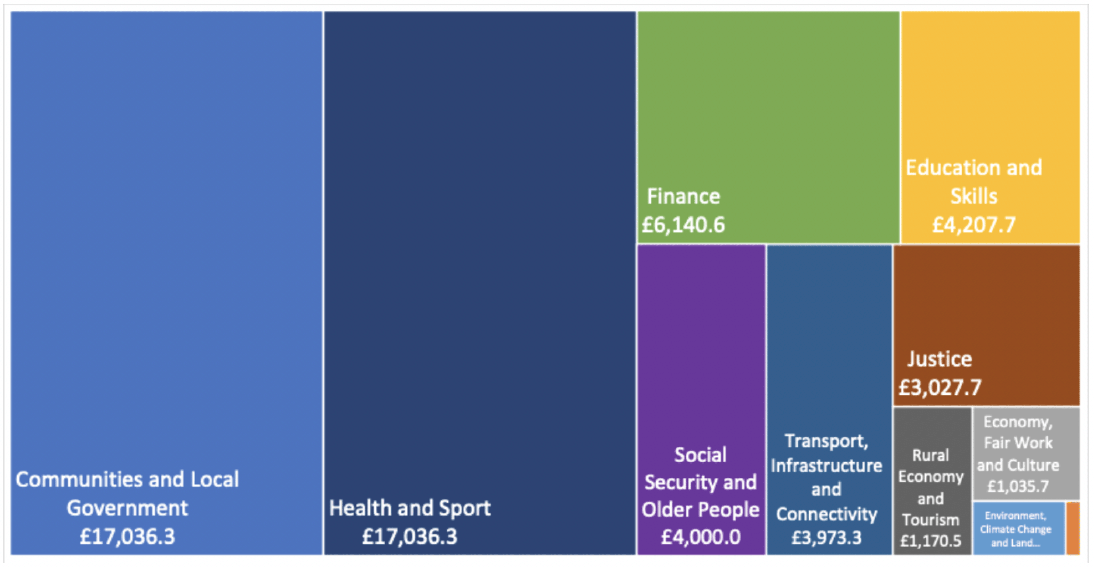

Tree map:

The above tree map chart was designed based on the US Spending Portal and South African Fiscal Transparency Portal. Real Scottish data was used from the Level 4 budget spreadsheet to demonstrate the spending from level 1 through to level 4. This visualisation was based on the following user needs:

- Detailed and integrated data on spending by delivery organisations, at a more granular level;

- Improved data visualisation.

This visualisation also has alternative views (tree map, table and downloaded raw data) to cater for different types of user.

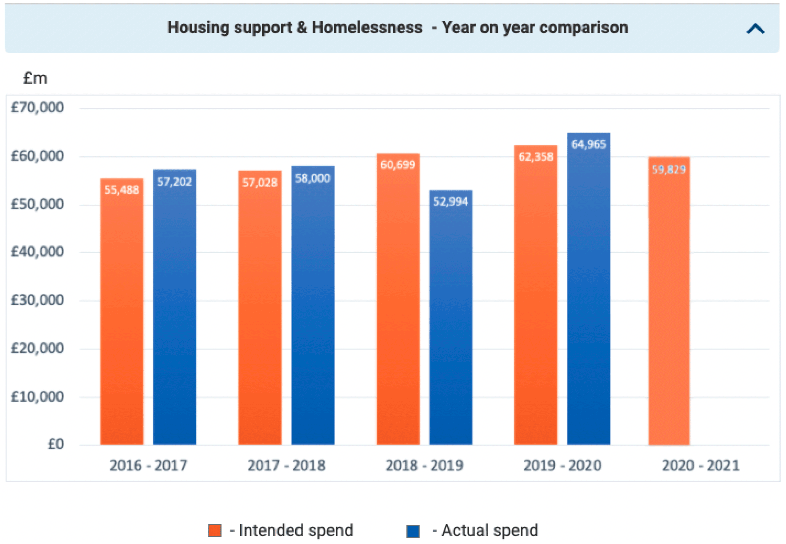

Intended vs actual spend:

The above visualisation shows the difference between intended spend and actual spend. This visualisation is based on an example from the Germany Fiscal Transparency Portal. This approach would allow for an improved ability to scrutinise the Scottish fiscal situation and comparisons over time.

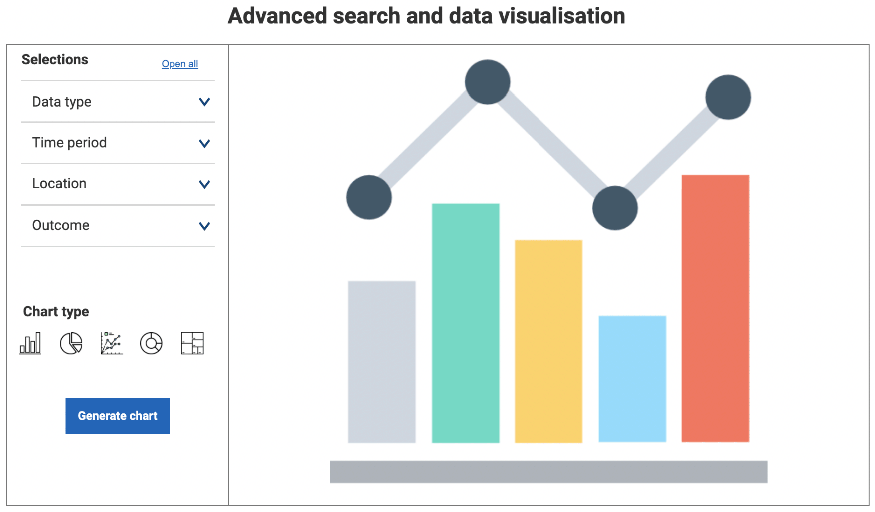

Advanced data visualisation

The above visualisation has been designed based on an example from the Brazil Fiscal Transparency Portal. This could enable users to choose their selection criteria and create their own graphical or non-graphical downloadable data file/display as required. This visualisation is designed to explore the need for more useable data and improved data visualisation.

3.7 Accessibility Approaches

All digital solutions must be designed so that they are usable independently and without barriers by people with long-term limiting health problems or disabilities. The Scottish Government is committed to providing accessible digital services as a vital part of their commitment to equal opportunities. Due to the scope of this Discovery, we did not get the opportunity to speak to people with disabilities directly. As such, it is crucial to focus on their experience in the next stages of the design process in order to make sure that the future service takes into account their specific needs. While the guidelines below can provide a good starting point, they should not be seen as a replacement of targeted accessibility testing.

Digital Scotland have published accessibility guidance as part of the design system they have created. They have outlined some best practice guidelines for designing digital services including:

- Enabling keyboard interaction – all content should be accessible without use of a mouse;

- High colour contrast to ensure good levels of readability - this applies to text, images, gradients, buttons and other elements;

- Use of Alternative Text for all images describing the function of the image;

- Heading structure.

The W3C Web Accessibility Initiative (WAI) standards are considered to be the international standards for web accessibility. The standards provide a comprehensive set of technical specifications, guidelines, techniques, and supporting resources that should be used to develop accessible digital fiscal transparency services. However, the standards do not explicitly address data visualization, and there are particular approaches to be considered when maximising the accessibility of data visualisations and infographics, for example:

- Keep visuals clear and contrasted and data tables simple;

- Carefully consider colour usage to make sure outputs are clearly visible to people with the various forms of colour blindness;

- Colour should not be the only visual cue, for example consider the use of text labels or patterns;

- Consider incorporating easy access auditory cues that explain data metrics for those visually impaired;

- Label data directly instead of relying exclusively on legends (which requires colour interpretation);

- If possible, design data tables and visualisations that have alternative text options in order to be translated by screen reading tools for visually impaired users;

- Users should be able to do anything with a keyboard that they can do with a mouse;

- Ideally, provide the data in a downloadable open format so that visually impaired users can reorganise it using their chosen methods and tools.

The nature of data visualisations may mean that they are harder to make accessible compared to text information. The project should review approaches taken to accessibility in other public sector data visualisation sites, e.g. the Public Health Scotland Covid-19 dashboard. It will be important to allocate resources to accessibility, especially the accessibility of visual outputs.

For more details see

- Accessibility Considerations in Data Visualization Design (keen.io);

- Data Visualization and Accessibility: Three Recommended Reads and Top Tips | by Susan Currie Sivek, Ph.D. | Towards Data Science;

- Data Visualization Accessibility: Where Are We Now, and What's Next? | by Melanie Mazanec | Nightingale | Medium;

- Dos and don'ts on designing for accessibility - Accessibility in government (blog.gov.uk).

Contact

Email: niall.davidson@gov.scot