Scottish Exchequer: fiscal transparency discovery report

This report seeks to understand the accessibility and connectedness of current fiscal information and data and describes how we could implement improved fiscal transparency services and the benefits that could generate.

2 As-is Summary

This section describes how Scottish fiscal information is currently published and consumed.

2.1 Definitions

Fiscal transparency is about a broad set of linked fiscal information, in a wider sense than just structured data, i.e. including:

- Data in the form of tables in documents, charts, infographics, spreadsheets and machine-readable open data;

- Text that describes the meaning of data, e.g. in documents, spreadsheets and open data portals;

- Any other broader text describing the Scottish fiscal situation;

- Infographics describing a fiscal process or policy.

It is not just about data visualisation, or open data.

Fiscal transparency is about any information relating to the budgeting, revenue and spend of the Scottish public sector, including any economic analysis and forecasting in these areas. It includes procurement data and related information, including on contracts awarded, the subsequent spend, and the organisations benefiting from the spend. Similarly, it incorporates information on grants made by the Scottish public sector, including information on the recipients.

It excludes non-fiscal economic data, e.g. on employment, gross domestic product, business turnover.

The project is focussed on delivering fiscal transparency by online digital means, although this will need to be supported by non-digital means where appropriate, for example face-to-face engagement with stakeholders and the possible physical publication of some outputs for accessibility reasons.

2.2 As-is Service Description

The Scottish Government and associated public sector organisations currently publish a wide range of outputs containing fiscal information - at least 40 separate regular outputs, as well as ad hoc outputs. There are at least ten publishing units, including core government directorates, the Scottish Parliament, and autonomous organisations such as Audit Scotland and the Scottish Fiscal Commission, as shown in the stakeholder diagrams in Section 2.8.

Preparing the outputs

Fiscal data resides in a range of data sources, including many spreadsheets, some dedicated databases (e.g. Revenue Scotland's Scottish Electronic Tax System), and various shared Scottish Government systems such its Enterprise Accounting System and the Hyperion Planning system. Data is sourced from many internal and external organisations, e.g. Her Majesty's Revenue and Customs, Scottish local authorities, other Scottish Government divisions, agencies, and the Office of National Statistics.

Creating the current outputs is often an inefficient and lengthy process, involving the "hand crafting" of documents and spreadsheets.

Output content

Many of the current outputs are very large documents, containing significant amounts of text. For example, the annual budget statement is 170 pages, and the Infrastructure Investment Plan is 163 pages.

Documents are often produced for a particular internal purpose, with large amounts of detail – often for consumption by Parliament or another parts of government. The formats are driven by conventions, internal government processes and organisational structures, accounting standards or parliamentary requirements rather than transparency or a need to communicate with external stakeholders. This naturally makes them less accessible to external users.

Outputs are frequently organised by government portfolios (especially budget related documents), but other ways of organising and categorising outputs are used, for example:

- The 11 National Performance Framework themes, e.g. in the Consolidated Accounts report;

- Sectors of the economy, e.g. in the Climate Change Plan Update;

- Equality themes, risks and protected characteristics, e.g. in the Equality and Fairer Scotland Budget Statement;

- Strategic political budget themes, e.g. a green economic recovery, no-one left behind, etc. (which reflect the political priorities of the current government and hence will change over time).

Often outputs are not categorised in a consistent fashion. Some spreadsheets are difficult for the uninformed user to interpret – e.g. the Level 4 budget spreadsheet, or the monthly over £25,000 spend spreadsheets.

Publishing the Outputs

Fiscal data published by the Scottish public sector is fragmented across a number of online sources, with no single entry point, including:

- The main Scottish Government website normally in the general publications area rather than a dedicated Scottish Exchequer or fiscal area - although dedicated pages hold information on local government finance statistics, economic statistics, taxes and non-domestic rates. Some stakeholders said that it can be time consuming to publish large documents on the website;

- The Scottish Parliament and its Information Centre Research Briefings

- The Revenue Scotland devolved taxes authority webpage;

- Scottish Fiscal Commission publications at the Scottish Fiscal Commission webpage;

- Audit Scotland reports at the Audit Scotland webpage;

- Open data on the Scottish statistics open data portal Public sector contract spend on the Public Contracts Scotland website;[1]

- Data on NHS spend by Public Health Scotland at – the Public Health Scotland Data and intelligence webpage;

- Information on spend and outcomes by Scottish Government agencies and directorates on their own websites (e.g. the Social Security Scotland website, the Transport Scotland website and the Scottish Public Pensions Agency website – and many others) – for example in annual report and account documents;

- Office for Budget Responsibility devolved tax and spending forecasts;

- Her Majesty's Revenue and Customs reporting of the non-devolved taxes, for example Income Tax Outturns.

For example, the main budget report is held on Scottish Government website, the detailed level 4 budget data is published as a spreadsheet on the Scottish Parliament's Information Centre website, while they also publish summary infographics on the budget.

Information on front-line spending and outcomes by government departments, agencies, the NHS and Scottish local authorities is not available to Scottish Government exchequer or finance staff. This information is very fragmented and poorly signposted - the only links found during the study are in the middle of the 146 page Consolidated Accounts annual report (page 16 onwards).

There is often a poor understanding of how the current outputs are used – e.g. generally no data is collected on website usage (with some exceptions, e.g. Revenue Scotland). Neither are there a consistent attempts to obtain direct feedback from users (with some exceptions, e.g. the Scottish Government's Tax team, its Office of the Chief Economic Adviser and Revenue Scotland).

In some cases, social media is used to publicise fiscal outputs, e.g. the Office of the Chief Economic Adviser use Twitter (@scotgoveconomy and @scotgovocea), but this is not widespread.

There is poor accessibility for users with disabilities because of the use of features like embedded images and data tables in PDF documents. Graphics are not presented in a consistent style across all outputs.

There are a few overlaps with information published at the UK level, e.g. details on Income Tax in Scotland published on the UK Government website.

There is very little open data published, with the notable exception of Revenue Scotland and Public Contracts Scotland, who publish data on the Scottish statistics open data portal. Most of the published spreadsheets are not in an open data format, i.e. they are not machine readable without further manual reformatting.

Summary Information Maps

These diagrams summarise the core fiscal outputs published by the Scottish public sector. We have not attempted to catalogue all of the many spending and outcome documents produced by Scottish Government agencies and directorates.

Economic Outputs

- Government Expenditure and Revenue Scotland (GERS)

- Economy Statistics – including monthly GDP

- Various Analytical Reports – Scottish Fiscal Commission

Budget Outputs

- Medium Term Financial Strategy 5 years – Fiscal Principles, Funding outlook, Spending outlook, Text and data

- Capital Spending Review

- Infrastructure investment Plan

- Local Authority Outturn and Budget Estimates

- Scottish Budget – by the Exchequer

- Briefing on the Scottish Budget by the Scottish Parliament Information Centre (SPICe)

- Budget data and infographics (by SPICe)

- Budget Revisions

- Local Government Funding 2020-2021: process overview

- Carbon Assessments – Carbon emissions associated with planned budget expenditure

- Budget impacts by protected characteristics

- Climate Change Plan – estimated costs and benefits associated with the policies set out in the plan (future)

- Local Government Grant-aided expenditure

Actual Spend Outputs

Scottish Assessors Association

Non-Domestic Rate Statistics

- Includes rateable value

SG Non-domestic Rates data

- Inc. appeals, relief statistics, COVID business support grant stats, accounts

Council Tax Data

- Including council tax reduction data

LBTT and LFT Tax Stats

- Annual summary of trends, monthly LBTT stats, quarterly landfill tax, ad hoc stats

Scottish Tax details

- Land and buildings Transaction Tax (LBTT)

- Landfill Tax (LFT)

- Scottish Income Tax

The Scottish Fiscal Framework

Revenue Outputs

Forecasts of income tax revenues vs outturn data

- (Scottish Fiscal Commission)

Taxes Infographic

- (By SPICe)

Local Government Benchmarking Framework

- Improvement service

NHS Boards Contract Spend

- Published by individual boards

NHS Cost Books

- Published by Public Health Scotland

Scottish Landfill Communities Fund Projects

Public Contracts Scotland

- Contract award data

Government spend over £25k

- One xls per month – poorly explained and presented

Spend and Revenue Outputs

Forecast Evaluation Report

- Scottish Fiscal Commission

Fiscal Update Report

- Scottish Fiscal Commission

Audit Scotland Local government in Scotland Annual Financial Overview

- Revenue, spend and reserves

Scottish Local Government Financial Statistics

- Income, spending, reserves, debt and pensions

Budget reconciliation (Outturn Report)

- Text and data - technical output mainly for Parliament.

- By risk areas. Lots of text

Audit Scotland audit of the Scottish Government Consolidated Accounts

- Revenue and spend vs budget

Consolidated Accounts

- Text and data - technical output mainly for Parliament

- Actual revenue and spend

2.3 Top-level User Frustrations

Scattered information

Not everything is in one place - data is produced by different bodies, published in different places and people need to patch that story together. Lack of a single source of truth does not foster trust.

Disjointed timeline

Because the documents throughout the budget and planning cycle are snapshots in time, it's hard to track the decision-making that happens between them e.g. how the changes in revenue affect the mid-year revisions.

It is difficult to form a story over time of spending, especially when comparing the current budget to historic ones. Looking at the budget bills themselves allows only for the comparison of intention and the consolidated accounts are in an entirely different format altogether.

Exclusionary conversation

A base understanding of fiscal information/processes is required to understand the documents and foster good conversations. This limits the type and amount of people who are reading these published documents and engaging in the conversation.

Inflexible documents

The documents are published for single administrative purposes of different bodies, but people want to use them in different ways that they are not designed for. They either don't achieve their goals or use up their own time and resources to patch them together to a useful state, which carries the risk of human error.

Inconsistent data

Data is often reported in different ways; there are differing labels, differing depths of data across portfolios, portfolio name changes etc.

All of this makes it harder to analyse how the money is spent and how effective that spending is. Likewise, on the revenue side the need to include the format of Office for Budget Responsibility forecasts and UK tax data in the analysis poses challenges in identifying risks to the budget.

2.4 As-is User Descriptions

Through our research with highly engaged external stakeholders, we have identified three main existing user types: translation user, assurance user and context user. While different people and organisations are often the most comfortable as one type of user, they can still move between each group depending on a specific context of use. It is our assumption that potential future users of the information will fall into the context user type, who are currently the least catered to (e.g. citizens, journalists, business and tech communities). Unfortunately, due to the time constraints of this Discovery, we were unable to speak to them directly so future research with these user groups is recommended.

It is important to realise that those types are not fixed but rather a way of exploring specific motivations and needs which can overlap. This was confirmed by our international research; in particular, international organisations like the International Monetary Fund, Organisation for Economic Co-operation and Development and the World Bank want disaggregated raw data, but need this to be located within the full picture so they have the context or overall system view. Some pointed out that what we call context users may want high-level information but also to be able to drill down to very detailed data about a particular place (their local school or community) or a particular topic.

Translation and Context User Common Needs

- Descriptive summaries

Context and Assurance User Common Needs

- Spending linked to outcomes

Assurance and Translation User Common Needs

- Timeliness

- Quality of data

- Open data

All User Types Common Needs

- The story over time

2.5 Context Users

Context users want to understand what the numbers mean to the cause they care about, specific demographics or their own local area. They are not the most competent in deep financial scrutiny, so they depend on translator users to disseminate and provide the context to the budget document and other financial information relevant to their specific inquiry.

When reading the document, they would like to understand in general terms where the numbers came from (the fiscal framework process and numbers), the process behind decision making and what the intended outcome is – as well as what actually happened over time. At the moment, the format does not make this easy as the reader journey is not obvious; with summaries hidden away in appendixes, budget lines not going into much detail and no clear signposting to where they could find more info (i.e. level 4 spending and beyond) or external analyses.

Some financially literate context users can sometimes attempt their own scrutiny (temporarily becoming assurance users) but since there is little support for that, they end up spending a lot of time comparing spreadsheets and taking the numbers to decision makers within government, only to hear that they have misunderstood something or made a mistake.

Example user stories

As a civil society policy officer, I want to be able to easily track the outcome of spending over time and across portfolios so that I can offer the government officials my expertise and help them make more effective spending decisions.

As a sustainability and wellbeing advocate, ideally, I want to be able to access financial data together with other national statistics (like carbon footprint data) so that I can follow the golden thread of systemic interconnections more easily.

As an interested citizen, I want to see how the money was spent in my local area so that I can see the effect of the budget on myself, my family, business and local community.

Key frustrations

- Budget not designed with a clear 'reader journey' in mind;

- It's unclear at the moment how the National Performance Framework feeds into budget process;

- Conversations end up being about understanding the numbers rather than desirable outcomes;

- Feels impossible to follow different budgets' spending over a five year period;

- Hard to know what money is being double counted – referred to multiple times in the budget.

What people said

- 'It's incredibly difficult from the outside to get a grip on how any of this works.'

'My interaction with trying to understand it on government websites is it's hard to figure out. There's no clear reader journey of someone who wants to understand various pieces of the budget and different aspects of junctions of decision making; what feeds into what. Community reports, assessments (…) It's almost like the pages aren't designed for someone coming in who needs help being taken through various pieces.'

'You end up with 20 Excel docs open and it's very difficult to navigate through information on the web. I can't find the golden threads between them. I'm relying a lot on my own focus to do so.

'When trying to speak to someone or find the information, it feels like obfuscation. Even if it's not. (…) For democracy, it's worrying because politicians won't understand it.'

'I wanted to look at the degree to which the Scottish budget was realising the economic and social rights. So, we went in to see if we could track the data on e.g. the right to housing, the right to food, to health, social security.'

'There's a story to tell, but we can't tell it.'

2.6 Assurance Users

Assurance users want to get 'under the bonnet' of the budget narrative and numbers. They see the budget mainly as a policy document – a declaration of intent that will nevertheless change over time. That's why being able to track the budget across its entire life cycle is crucial to them; especially in the context of how complex the Scottish Fiscal Framework has become with the introduction of the most recent devolved powers. While they tend to use raw data, they also benefit from the more contextual analysis of the translation users – as it offers a holistic perspective and another point of view.

The financial data they need for their analysis is often spread across many bodies; there does not seem to be anyone responsible for bringing it all together and translating for the Scottish context. This forces the assurance user to connect all the diverse pieces themselves before analysis, causing strain on their resources and stopping them from performing more complex calculations that could benefit the government on a more ongoing basis.

It also means that many assurance users feel the pressure to become translator users themselves – filling the void that they see as the role of the government itself. A good example of this is Scottish Fiscal Commission publishing regular fiscal updates; showing how the budget funding position is affected throughout the year by various factors related to the Fiscal Framework.

Example user stories

As an auditor I want to be able to access well referenced, up to date, machine readable raw spending data; so that I can trust that my analysis will be truthful and accurate with little risk of human error.

As a parliamentary clerk I want to see how the Scottish tax base is performing based on real time data (including forecasts) and compare it to the UK tax base so that I can monitor the risks to Scottish budget more effectively.

As an economist advising parliamentary committees, I want to be able to easily follow the budget financing from the budget bill, through to revisions, outturns and the final revised position so that I can track the changes in revenue throughout the year and across multiple years; monitoring the state of the Scottish economy.

Key frustrations

- It's hard to make historic comparisons – e.g. in terms of tracking portfolio spending over time (as names keep changing) or how the budget envelope changes with budget cycle;

- Published documents are static snapshots in time that don't show the situation now – making ongoing analysis like tracking risks to the budget finance difficult;

- Information is published in many different places by different bodies, with different financial systems and statutory agendas – i.e. Office for Budget Responsibility forecasts or the non-devolved Scottish tax data reported by the Her Majesty's Revenue and Customs. It makes it hard to keep track of latest updates and link different formats together.

What people said

'If you want to get a sense of how the Scottish government taxes have changed over time – it's really hard because you have the original budget documents but then you don't know what happens after.'

'We pull lots of info from different sources, it's all over the place. You can't get everything from the Scottish Government website. I'd usually go to the Scottish Fiscal Commission to get data before the Scottish Government.'

'The budget has got better, with tables etc. but it's difficult to extract. We want to extract it easier into Excel; we won't be doing anything complicated'.

'The format gets in the way: the data is opaque and dense. The budget document should be split. If the tables were split and published in a different way, e.g. in a machine readable format that would be great.'

'There's no further information from level 4 portfolios. We need to be able to see that breakdown to see how that money is being spent. We've had constant talks with people, but things haven't moved. We got told budget is about ongoing and future spending. We'd like to know this separation. What money has been taken from where to go where.'

'I'm an economist not an accountant – accounts data is a bit alien to me.'

2.7 Translation users

Translation users are often the most comfortable with the current reporting as they have been involved with the Scottish fiscal data in a professional capacity for years. This places them in a unique position of being able to navigate the current complexity and attempt to explain it to others – in the form of expert analysis, blog posts, data visualisations etc. They are the disseminators that emerged to fill the gap caused by the lack of an overarching governmental body tasked with bringing the whole story together, beyond current statutory requirements of official reporting.

Some translation users are comfortable in this role and would like to continue fulfilling it; others would prefer to return to their main duties once the government steps in as they're more comfortable as assurance users.

The existence of translation users also provides an exciting opportunity of creating a collaboration hub – acknowledging their contributions, encouraging further knowledge sharing and allowing new context users to easily access all material in one place. This way, the boundary between internal and external data publishers and users could be blurred, resulting in more effective collaborations and enable participatory governance.

Example user stories

As a disseminator, I want a simple table that explains what money is going up or down in the budget document and the decisions behind the changes so that I can explain the context of spending decisions to people easier and with more confidence.

As an advisor to the Scottish Parliament, I want the financial information to be made more accessible to the laypeople so that the Members of the Scottish Parliament feel empowered to engage more with it directly; allowing them to ask better scrutiny questions that would benefit their constituents and me to focus on complex queries.

Key frustrations

- At the moment, translation users get the data they need beyond official reporting by tapping into their connections within the Scottish Government. While it's a functional arrangement, considerable resources (both externally and internally) would be saved if the same data was timely and easily available;

- It would also mean that they could answer more complex questions than the same ones they sometimes receive – e.g. about underspent that's explained in the provisional outturn statement supplementary document: provided to people in the chamber but not shared publicly;

Regarding the data itself, translation users share many frustrations of the assurance users around how disjointed everything is at the moment and how hard it is to track the story over time and in-depth.

What people said

'Having a one-stop-shop website for everything budgetary and all the information that would allow for people to stitch it together would be useful. One thing that we're always pushing up against in the Parliament is that it's hard to engage members in some of this. You have members of the Finance Committee who are very interested in it, you have a few backbenchers and finance spokespeople (…). But sometimes for the wider MSP group, a lot of them say 'this is too complicated, I don't need to know about this'. The challenge is to show to people that it isn't necessarily complicated. A lot of the time it's just about allowing them to know the minimum amount of info that allows them to ask sensible scrutiny questions.'

'Think about the categorisation of portfolio names – are they intuitive? Is it civil service speak? Do the general public understand?'

'Each external organisation has a distinct role, but no one has overall responsibility for the whole fiscal transparency framework. A factual summary across all parts of the framework would be really helpful.'

'The information [relating to the Fiscal Framework and the budget envelope] exists but no one has the authority to ask for the information or is tasked to pull it together. The budget document is designed to describe the intent of the government. It misses the summary. There is also a timing issue because the numbers change at different points throughout the year.'

'It took weeks of my life to be able to put together a couple of slides for a presentation because I had to literally go in and try to match funding from 5 different budgets when they were all called slightly different things. Sometimes they would merge and you couldn't tell whether that was the same pot of money or is it now two pots of money put together.

'Governments are elected over time, so it is important to be able to see the continuation over time'.

2.8 As-is Stakeholders

There are significant number of organisational entities with an interest in the production and consumption of Scottish fiscal information – both within and outside the public sector. The diagrams below highlight many of these stakeholders, although it is inevitably an incomplete view at this early stage of the project - our understanding will grow as we progress. We have not attempted to show all the many information flows between the different organisations, although some are described in Section 2.9 below.

In the diagrams (PR) indicates a current producer of fiscal information, i.e. the organisation produces and publishes information they have created. This could include the creation of new data based on data from other sources, e.g. the forecast data produced by the Scottish Fiscal Commission.

(PU) indicates a publisher of information, i.e. the organisation publishes information they have sourced from a producer – which generally involves interpretation in some way, but not the creation of new data.

Core SG Fiscal Stakeholders

There is a core set of Scottish Government stakeholders who have a key role in the production of fiscal information relating to central Scottish Government revenue, budgeting and spend, or information on the Scottish economy. Note this diagram is not intended to be a structure chart, and it only includes fiscal transparency stakeholders, not all teams in the Scottish Exchequer or Financial Management Directorate.

Core Scottish Government Fiscal Stakeholders

Scottish Exchequer and Financial Division

- Performance and Strategic Outcomes (Producer of Information)

- Public Spending (Budget) Team (Producer of Information)

- Infrastructure and Investment (Producer of Information)

- Tax Team (Producer of Information)

- Finance Programme Management (Partners) (Producer of Information)

- Corporate Reporting (including Financial Management) (Producer of Information)

Chief Economist Directorate

- Office of the Chief Economic Adviser (OCEA) (Producer of Information)

Economy Directorate

- Climate Change Division (Producer of Information)

Communities Directorate

- Equality and Social Justice analysis

- Local Government and Analytical Services Division (Producer of Information)

Procurement and Property Division (Corporate Directorate)

- Procurement Development (Producer of Information)

Non-Ministerial Offices

- Revenue Scotland (Producer of Information_

Wider Public Sector Stakeholders

Beyond these core Scottish Government fiscal stakeholders there is a broad set of Scottish and UK public sector stakeholders who contribute or consume Scottish fiscal information, or who audit and advise on fiscal outputs. For example all Scottish Government directorates and agencies produce detailed information on their budgets, spending and outcomes in various formats and locations, including annual reports. However this information is very fragmented, with no central access point or consistent way of presentation. Note this diagram is not intended to be a comprehensive structure chart.

Wider Public Sector

Scottish Parliament and Ministers

- Parliamentary Clerks

- MSPs

- Finance Committee

- Public Audit and Post Legislative Scrutiny Committee

- Subject Committees

- SPICe (Publisher of Information)

- Ministers and Special Advisers

Public Sector Advice and Audit

- Audit Scotland (Publisher of Information)

- Equality Budget Advisory Group

- Scottish Fiscal Commission (Producer of Information)

- Scottish Economic Statistics Consultation Group

Scottish Local Government

- Scottish Local Authorities (Producer of Information)

- COSLA

- Solace Scotland

- Improvement Service (Producer of Information)

- Scottish Assessors Association (Producer of Information)

UK Government

- UK Statistics Authority

- UK Treasury (Producer of Information)

- Office for Budget Responsibility (Producer of Information)

Health Sector

- Health and Social Care Directorate (Health Finance)

- Public Health Scotland (Producer of Information)

- NHS Boards

Other Scottish Government Directorates and Agencies – for example

- Transport Scotland (Producer of Information)

- Scottish Public Pensions Agency (Producer of Information)

- Social Security (Producer of Information)

- Historic Environment Scotland (Producer of Information)

- Registers of Scotland (Producer of Information)

- And many others (Producer of Information)

Non-Public Sector Stakeholders

Outwith the public sector there are many organisations with an interest in Scottish fiscal information, some of whom who re-interpret and re-publish fiscal information. This includes think tanks like the Fraser of Allander Institute, Institute for Public Policy Research, Institute for Fiscal Studies and the Global Initiative for Fiscal Transparency. Think tanks may be users of Scottish Government fiscal information, and/or influence and offer advice on fiscal transparency. Note this diagram is not intended to be a comprehensive structure chart.

Non-Public Sector

Non-Public Sector Users of Fiscal Information

- Technology and Digital Companies

- Academia (Publisher of Information)

- Consultative Companies

- The Media (national and local) (Publisher of Information)

- Third Sector

- Citizens

- Think Tanks (Publisher of Information)

- Professional Bodies *

- Businesses and Investors

- Data Aggregators

- Other international governments

- Credit Agencies

- Civil Society organisations

- International organisations, for example IMF, OECD, NGOs, Open Government Partnership

- Lobby Groups

Non-Public Sector Recipients of Public Funds

- Third Sector

- Businesses

* e.g. the Royal Institute of Chartered Surveyors.

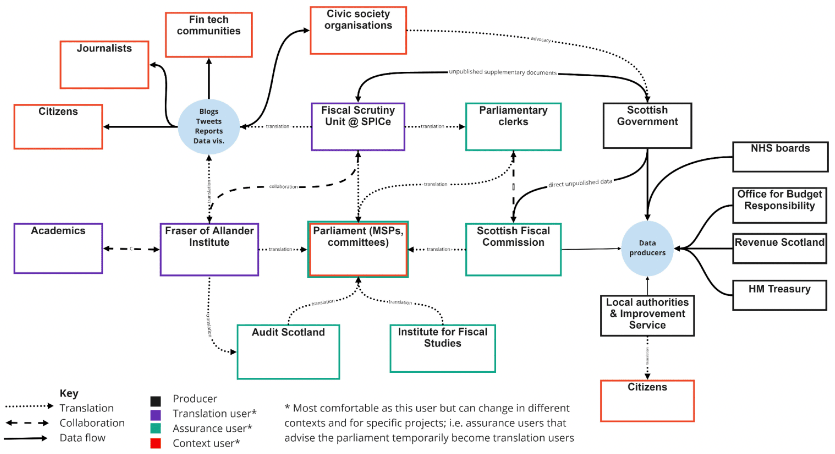

2.9 Stakeholders Information Exchanges

The diagram below is the project team's interpretation of the as-is stakeholders outwith the core Scottish Government directorates and Revenue Scotland, and how they exchange information with each other. It is intended to be illustrative of the broad flows around the ecosystem that exists around financial data in Scotland and is not comprehensive. One of the key discoveries of the external research was how interconnected the bodies we spoke to are – in terms of helping each other source specific missing or unclear data, collaborations and dissemination of findings in an accessible format.

What has become clear is that there is no simple distinction between a single data producer (e.g. the Scottish Exchequer) and data users (external organisations); instead, there is a rich ecosystem built around positive scrutiny and risk assessment, intended as a way to make sure the money in Scotland is spent effectively and with the greatest possible benefit to people living in it. This creates an opportunity for the Scottish Government to facilitate those existing networks of relations, becoming an encouraging and enabling partner.

Contact

Email: niall.davidson@gov.scot