Publication - Research and analysis

Scottish economic bulletin: November 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumer Activity

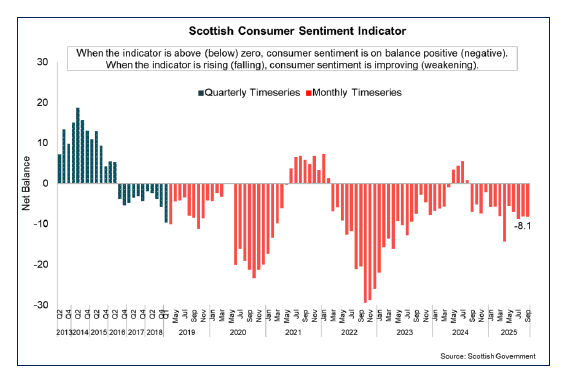

The Scottish Consumer Sentiment Indicator remained unchanged at -8.1 in September.

Consumer Sentiment

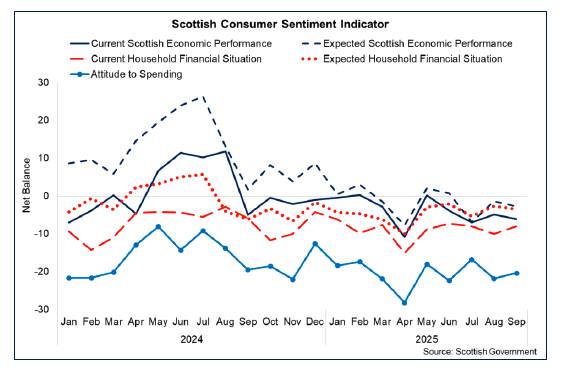

- The Scottish Consumer Sentiment Indicator (SCSI) reflects how people feel the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- In September, the consumer sentiment indicator’s net balance was -8.1, unchanged from August, and remained lower (down 1.2 points) compared to the same point last year.[21]

- The sub-indicators showed that sentiment towards current security of household finances and attitude to spending rose by 2.0 and 1.4 points respectively over the month, while sentiment towards current and expected economic performance declined by 1.2 and 1.4 points, and expected security of household finances fell by 0.9 points.

- Despite the strengthening in the indicators for household finances and spending, their net balances remain the most negative (‑8.0 and -20.3 respectively), reflecting the ongoing challenges facing household budgets.

- More recently at a UK level, the GfK Consumer Confidence Index increased by two points to -17 in October, driven by a strengthening in sentiment on 4 out of the 5 sub measures, albeit that there was a slight weakening in sentiment relating to respondents’ expected personal financial situation over the next 12-months.[22]

Spending and Cost of Living

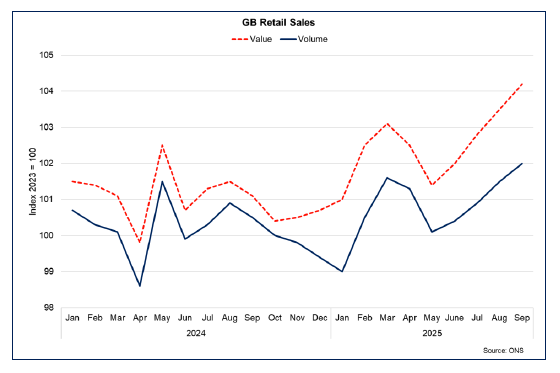

- At a GB level, retail sales growth has strengthened moderately in 2025 following a fall over 2024. Latest data for the three months to September show sales rose by 0.9% in volume terms and by 1.8% in value terms. Over the past year they have risen by 1.0% and 2.2% respectively.[23]

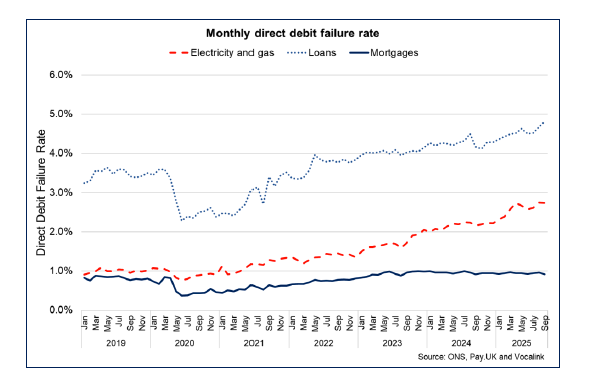

- However direct debit failure rates due to insufficient funds remain elevated, particularly with respect to electricity and gas bills (2.74%) and loans (4.81%), which have continued to rise in 2025. Direct debit failure rates on mortgages, nonetheless, remain comparatively low and have stabilised around 1% since the start of 2024, with the rate currently standing at 0.93%.[24]

- More stable inflation expectations relative to previous years and reductions in the interest rate have supported improved conditions for consumption in recent months. Nonetheless, weakness in consumer sentiment and evidence of an elevated savings ratio reflect that the demand landscape continues to remain challenging.

- The Bank of England noted in their latest Monetary Policy Report (MPR) that the UK savings rate has not fallen back to historcally more normal levels, suggesting that consumers may be more cautious to spend in light of recent shocks and may be wanting to rebuild precautionary savings and wealth that have eroded in real terms during the period of high inflation.[25]

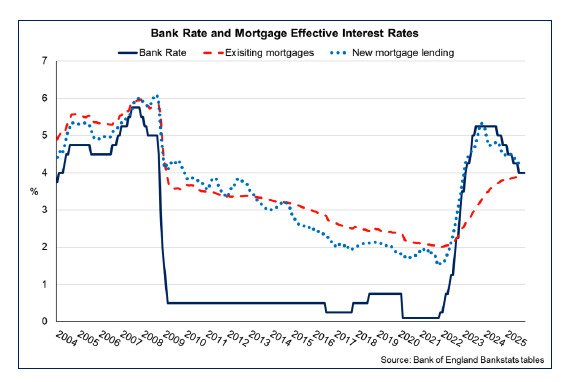

- As the gradual loosening of monetary policy feeds through to economic activity, the effectve interest rate on new mortgages has fallen from 4.26% in August to 4.19 in September, while on the stock of existing mortgages remained stable at 3.89 in September.[26]

Economic Outlook

Latest economic growth forecasts indicate a slight softening in growth next year as inflation starts to gradually fall.

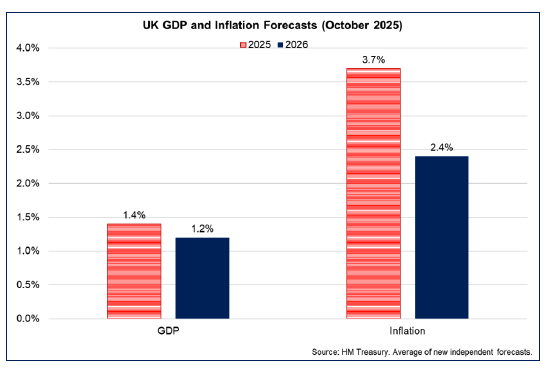

- At a UK level, the latest HMT average of new independent UK forecasts from October, showed that UK GDP growth is projected to strengthen to 1.4% in 2025 before slowing slightly to 1.2% in 2026. More recently in November, the Bank of England projected a similar pattern for UK GDP to grow by 1.5% in 2025 and by 1.2% in 2026, before picking up again to 1.6% in 2027. The OBR is due to publish their next UK forecast alongside the UK Budget on 26 November.[27],[28]

- The global economic outlook remains challenging and presents headwinds to growth. In October, the IMF forecast global growth to slow from 3.3% in 2024 to 3.2% in 2025 and 3.1% in 2026, with the Bank of England projecting the slower global growth in 2026 to weigh on the UK economy.[29]

- For Scotland, the Scottish Fiscal Commission (SFC) forecast in May that Scottish GDP growth is expected to grow 1.1% in 2025, before rising to 1.8% in 2026 and 1.7% in 2027. In the short term, this is broadly in line with the more recent forecast from the Fraser of Allander Institute in October which forecast growth of 1.0% in 2025 before remaining more subdued across 2026 and 2027 (1.0% and 1.1% respectively). The SFC will publish their next forecast alongside the Scottish Budget in January 2026.[30],[31]

- The weakness in GDP growth over the next year will potentially support the weakening in inflationary pressures. The average of independent forecasts from October indicate Q4 on Q4 inflation in Q4 2025 will be 3.7% and fall to 2.4% in Q4 2026. Most recently in November, the Bank of England judge inflation to have potentially peaked at 3.8% in Q3 2025, and expect it to fall to 3.5% in Q4 2025, and continue to gradually fall back to its target rate of 2% in Q2 2027.

- The economic outlook for this year and the next remains subdued, both globally and domestically. Easing inflationary pressures and loosening in monetary policy restrictiveness are expected to be supportive of growth. However this risks being partly offset by increased fiscal uncertainty in the lead up to the forthcoming budgets, which has the potential to weigh on business and consumer confidence and activity.

Contact

Email: economic.statistics@gov.scot