Scottish economic bulletin: November 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation

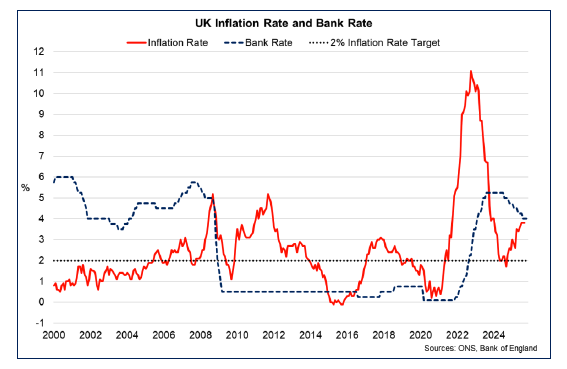

The inflation rate was unchanged at 3.8% in September, slightly below expectations.

- Inflation remained stable in September at 3.8%, for the third month in a row.[3] There was a notable increase in the inflation rate of transport (3.8%, up from 2.4%), mainly driven by motor fuels and air fares, which were offset by a fall in the inflation rates of recreation and culture (2.7%, down from 3.2%), and food and non-alcoholic beverages (4.5%, down from 5.1%).

- More broadly, services price inflation remains elevated relative to goods price inflation, though was unchanged from August at 4.7%. Goods price inflation continued on an upward trend, rising from 2.8% in August to 2.9% in September, its highest rate since October 2023.

- Core inflation (excluding energy, food, alcohol and tobacco) rose by 3.5% over the year to September, down from 3.6% in August.

- Inflation remains above the Bank of England’s 2% target rate, although the Bank expect UK inflation to have now potentially peaked at 3.8%. The September inflation rate was lower than previously forecast by the bank in August, when they expected inflation to rise to 4% in September. Their November forecast expects inflation to now fall gradually to 3.5% in Q4 2025 and back to target in Q2 2027.[4]

- The Bank’s Monetary Policy Committee (MPC) judge that risks to the inflation outlook have become more balanced in recent months. Strong wage growth and higher household inflation expectations risk putting upward pressure on the inflation outlook. However continued subdued household consumption and an elevated savings ratio could weigh on the inflation outlook.

- The MPC voted 5-4 in November to maintain the Bank Rate at 4%, with four members voting for a 25 basis point cut to 3.75%. On balance, the MPC set out that they require further data points to confirm that inflationary pressures are continuing to fall before making their next cut.[5]

Box 1: Assessing the case for Scottish Government Bond Issuance

Since 2023, the Scottish Government has been considering whether it should issue bonds, which was one of the recommendations of its Investor Panel Report.[6] The Scottish Government now announced it had received a high investment grade rating and parity with the UK government from two rating agencies, Moody’s and S&P, and confirmed intentions to initiate a programme of bond issuances over the next parliamentary term to fund capital investment.

The Scottish Government currently borrows through the National Loans Fund (NLF) to support capital investment. Issuing bonds involves borrowing directly from international debt markets, rather than through the UK Government, giving more flexibility over the repayment structure, loan durations and interest rates.

A summary Outline Business Case (OBC)[7] assesses bond issuance against other borrowing options, including the NLF, by considering strategic fit, value for money, supplier capacity and capability, affordability and achievability. It finds that a multi-year bond programme could best meet strategic objectives, maximise fiscal and economic benefits, and offer value for money.

Source: Scottish Government Bonds Programme: Summary Outline Business Case

The business case concludes that, on a discounted basis, bonds could either generate small savings or, more likely, result in additional annual costs of less than £2 million per bond issued. While bond issuance is likely to involve additional long-term costs under current market conditions, it could release resources in the short term for investment in public services due to differences in repayment profiles, with bonds only repaying the principal at maturity. In favourable market conditions, the short-term savings from bonds could outweigh the higher lifetime costs.

This aligns with the Investor Panel’s recommendation that the Scottish Government should consider issuing debt in international markets to raise Scotland’s profile, engage with investors and promote Scotland’s investment story.[8] A strong credit rating, a track record in capital markets and active investor engagement aim to benchmark Scotland’s economy internationally and help attract investment, supporting jobs and productivity. This could broaden Scotland’s investor base by reaching less-informed investors.

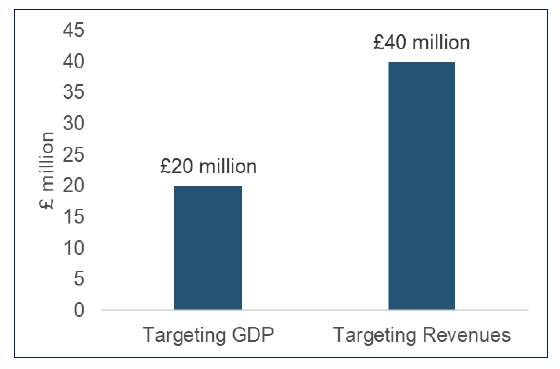

Were there to be additional costs from bond issuance, the business case considers the level of investment required to offset these or achieve a Benefit Cost Ratio of 1. This would require only a modest permanent increase in business investment of 0.1% to 0.2% (equivalent to £20-40 million). A bond programme and credit rating could therefore act as a signal of economic confidence and support broader investment goals in Scotland.

Source: Scottish Government Bonds Programme: Summary Outline Business Case

Bonds will not increase the amount that the Scottish Government intends to borrow but rather help the Scottish Government diversify its funding sources, support overall fiscal discipline and develop Scottish institutions. From a public finance perspective, under favourable market conditions these advantages alone could deliver value for money. They represent a significant development in the maturity of Scotland’s public finances after more than 25 years of devolution.

Contact

Email: economic.statistics@gov.scot