Publication - Research and analysis

Scottish economic bulletin: June 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation and Cost of Living

Higher global energy prices are yet to fully feed through to consumer prices however some cost of living pressures have risen and consumer sentiment has fallen.

Inflation

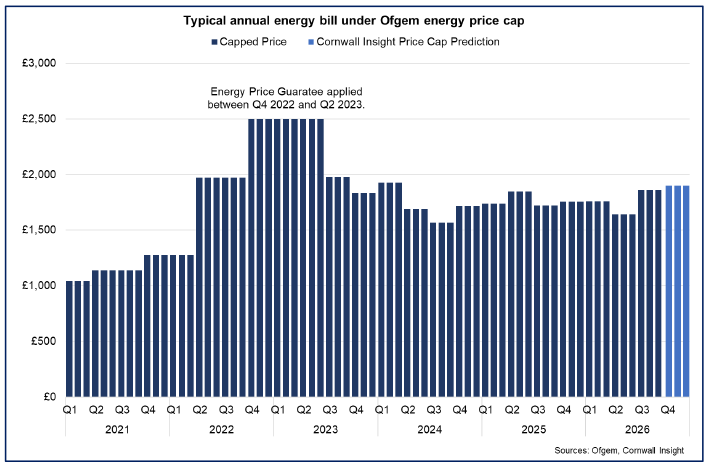

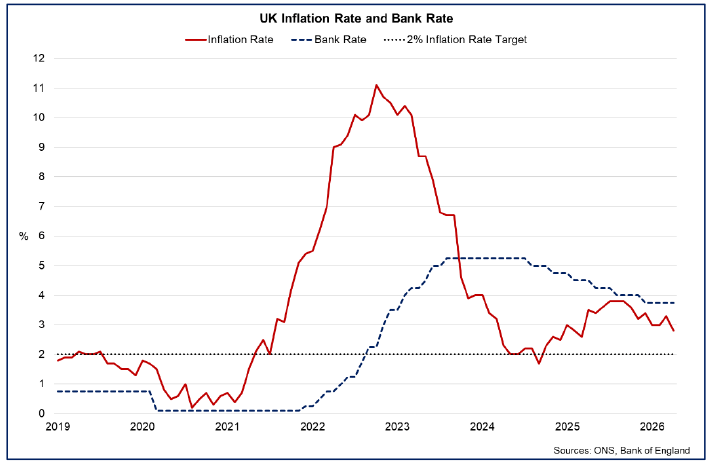

- The UK inflation rate fell from 3.3% in March to 2.8% in April, largely driven by a fall in household energy prices owing to the reduction in the Ofgem Energy Price Cap (EPC) for the period April to June.[3]

- The EPC fell 7% in April, with the announcement made in February prior to the escalation of the conflict in the Middle East, and primarily reflected changes to UK Government policies associated with environmental and social schemes. As such, the sharp increase in wholesale oil and gas prices (c.30% and c.45% respectively compared to before the conflict), are not yet fully reflected in overall consumer price inflation, largely due to the EPC protecting most households’ energy costs and also due to the lagged nature of pass through to wider costs. However, the EPC is set to rise 13% in July, reflecting the increase in wholesale energy prices since March.[4] After July, the EPC will next change in October. Given current energy prices, there is no indication that the cap will change significantly, but the outlook remains very uncertain and dependent on how energy prices evolve.[5]

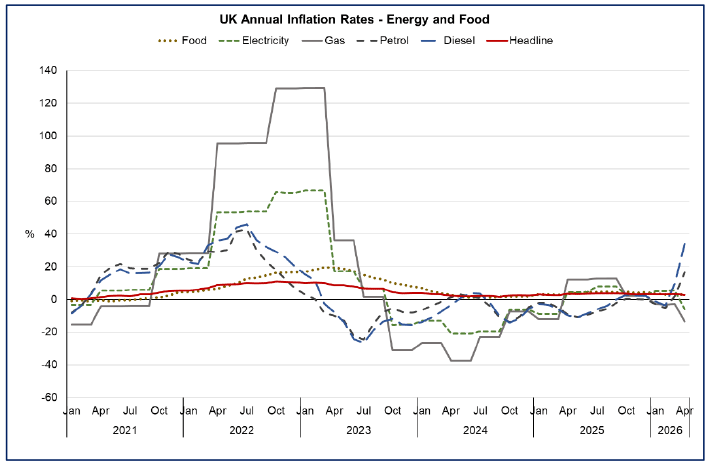

- The impacts are, however, already being reflected in other fuel prices. In April, the CPI rates for petrol and diesel increased for the second consecutive month, with petrol prices rising by 16.6% and diesel prices by 34.1% annually. However, there are indications that prices stabilised during May, and edged down slightly.[6]

- Households using heating oil have also seen an immediate increase in energy costs with April CPI data showing the liquid fuels price index rising 129.6% annually, up from falling by 5.2% in February, prior to the conflict.

- Core inflation, which excludes energy, food, alcohol and tobacco, fell from 3.1% in March to 2.5% in April, and is lower than headline inflation, indicating that the increase in energy prices has not yet fed through to wider consumer prices. However, higher energy costs have the potential to feed through to wider prices in the coming months, both directly and indirectly.

Monetary and Credit Conditions

- The Bank of England forecast inflation to be higher than previously expected, with the latest Monetary Policy Report (MPR) from April using three illustrative scenarios to map out how inflation may materialise, depending on how the Middle East conflict evolves. The scenarios indicate that inflation could rise to between 3.6% and 6% in Q4 2026, which is notably higher than the 2% which was projected in February, prior to the conflict.[7]

- In April, the Bank’s Monetary Policy Committee (MPC) held the Bank Rate at 3.75%, judging that despite the increase in fuel and energy prices, there was no need for a tightening in Monetary Policy at this point due to the current weaknesses in demand and the labour market which currently have the potential to limit the feed through to wider inflation.[8]

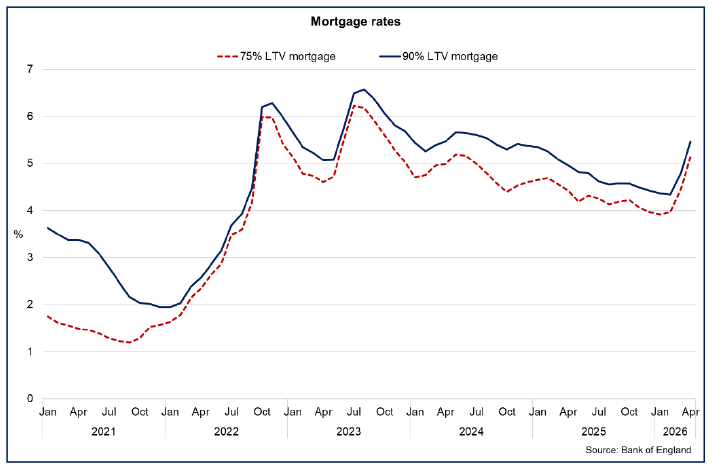

- Increased expectations of higher inflationary pressures and potentially tighter monetary conditions has started to feed through to some borrowing prices faced by households. For example, interest rates on two year 75% and 90% loan to value (LTV) mortgages rose in April to 5.14% (from 3.97% in February) and to 5.46% (from 4.34%).[9]

Consumer Sentiment

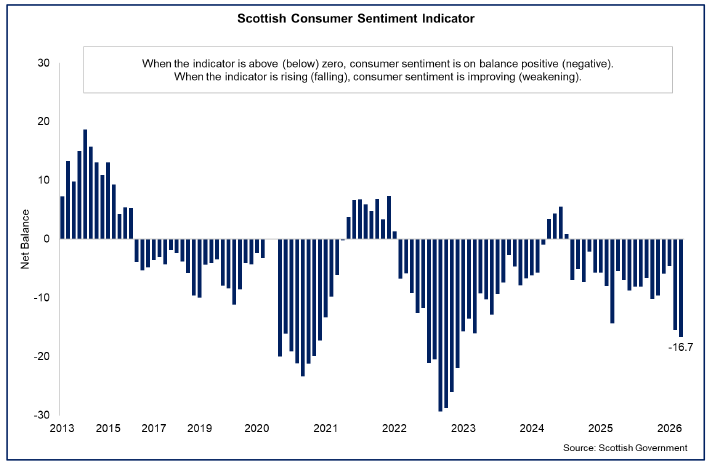

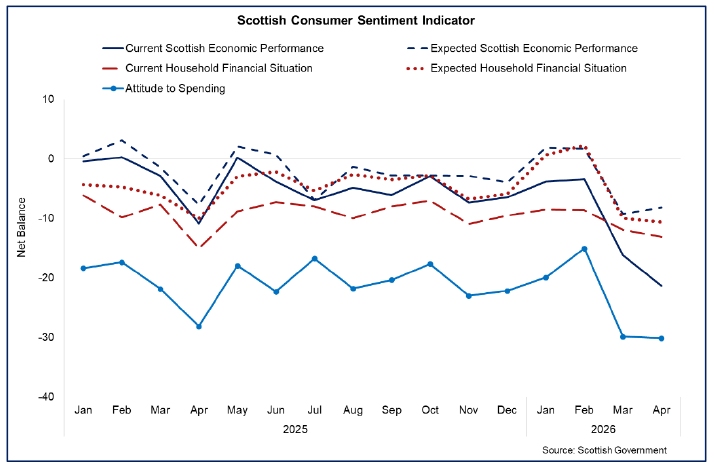

- The Scottish Consumer Sentiment Indicator reflects how people feel the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- Consumer sentiment has fallen sharply over March and April, likely reflecting the potential impacts that higher global energy prices could have on the economy and cost of living. Following a 10.8 point fall in March, the consumer sentiment net balance fell by a further 1.2 points in April to -16.7; its lowest level since January 2023.[10]

- All five sentiment sub-indicators fell in March and latest data for April show they all remain in negative territory, with sentiment weakening further across four of the five sub-indicators covering current economic performance, current and expected household finances, and spending attitudes.

- The largest decline in April was in the current economic performance sub-indicator (-5.1 points), while expectations of future economic performance strengthened modestly by 1.1 points, following a sharp 11-point fall in March. The further moderate falls across the household finances and spending indicators reflects the increased concerns that respondents have for cost of living.

Business Conditions

The sharp rise in fuel prices is impacting on business costs and business optimism in the face of ongoing subdued demand conditions.

Business Activity

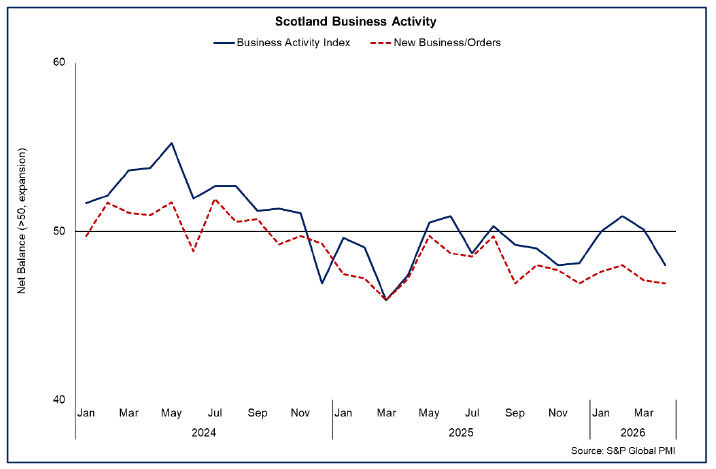

- Business surveys continued to indicate that business activity growth remained subdued through the first quarter of 2026, albeit marginally stronger than in the final quarter of 2025, however latest data for April suggests that activity may have softened slightly since the escalation in fuel prices from the conflict in the Middle East.

- The RBS Growth Tracker business survey indicated that business activity fell in April with a reading of 48 (a reading below 50 indicates contracting business activity) following marginal growth through the first quarter. Weak underlying demand remains a key driver of this with an increasing balance of businesses reporting facing a fall in new orders amid the rise in energy prices and increased uncertainty over March and April.[11]

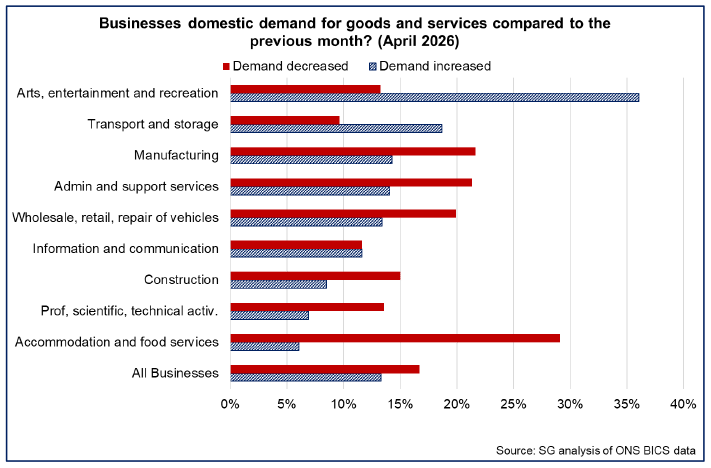

- The Business Insights and Conditions Survey (BICS) for April also indicates that a higher share of businesses reported a decrease in demand than an increase. At a sector level, the survey indicates that the accommodation and food services sector (29.1%) and manufacturing sector (21.7%) had the highest shares of businesses reporting a fall in domestic demand in April. In contrast, higher shares of businesses in arts, entertainment and recreation (36.1%) and in the transport and storage sector (18.7%) reported an increase in demand over the month.[12]

Contact

Email: economic.statistics@gov.scot