Publication - Research and analysis

Monthly economic brief: July 2022

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumption

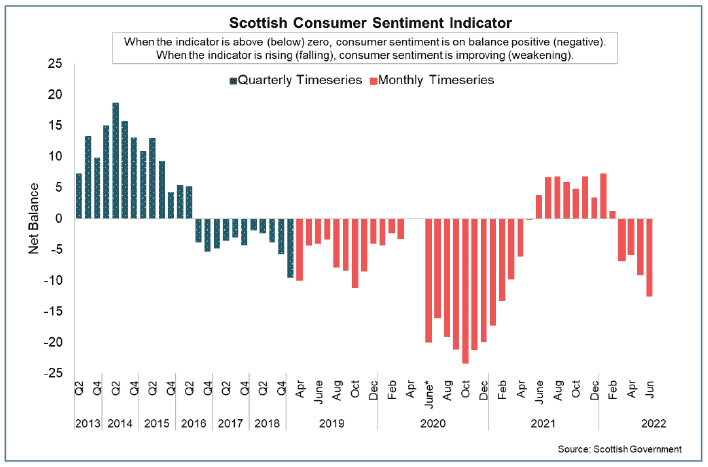

Consumer sentiment continued to weaken in June and is now at its lowest level since February 2021.

Consumer sentiment

- Consumer sentiment indicators continue to be highly sensitive to the rapidly changing economic environment as the economy recovers from the pandemic while at the same time households and consumers are facing significant challenges from the sharp rise in inflation and cost of living.

- These challenges have instensified since the start of the year, which has been reflected in a sharp drop off in the Scottish Consumer Sentiment Indicator.

- Latest data show consumer sentiment declined considerably over the month to June (-12.6 down from -9.1 in May). Overall, consumer sentiment has fallen 19.9 points since the start of the year and is at its lowest level since February 2021.[14],[15]

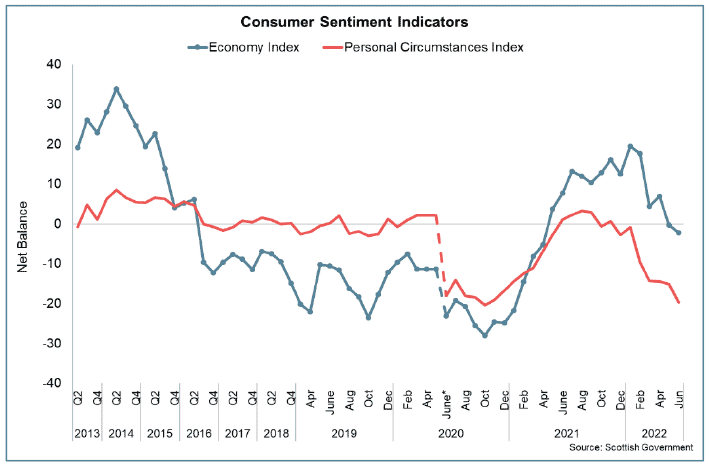

- On the economy, respondents on balance consider current economic circumstances to be worse than last year (-15.5 down from -11.8 in May). Looking ahead, respondents expect the economy to impove over the coming year relative to the current situation (+11.2). Although the level of optimism has been on a downward trend since July 2021, it remained broadly stable over the month.

- In terms of households personal finances, respondents on balance continued to report that their household finances are less secure than 12 months ago (-19.7, down from -16.5 in May). Looking ahead, sentiment towards expected finances fell significantly over the month (-8.7 down from -0.1).

- Both the outlook for the economy and household finances influence the extent to which households are relaxed about spending money. Since the beginning of the year, households have been increasingly uneasy about spending money as inflationary and cost of living pressures have increased, with the indicator falling to -30.4 in June; its lowest level since December 2020.

- Overall, the fall in sentiment since the start of the year has been driven by a combination of falling sentiment regarding the economy as a whole, and falling sentiment regarding personal household financial circumstances and personal relaxedness to spending money.

- This reflects the challenging economic environment households are facing and the risks to consumption growth over the months ahead.

Retail Sales

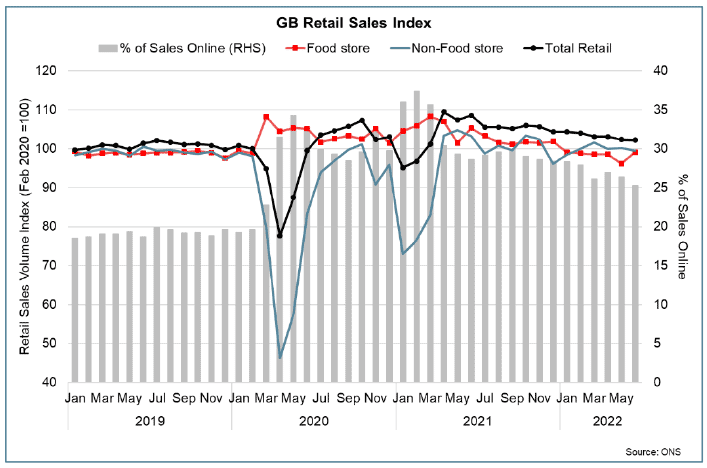

- Retail sales volumes fell by 0.1% in June 2022, following a fall of 0.8% in May and have fallen 5.9% over the year. However, sales volumes remain 2.2% above their pre-pandemic level.[16]

- Non-food stores sales fell 0.7% over the month driven by falls in clothing stores (-4.7%) and household goods stores (-3.7%). Food stores rose by 3.1% over the month with retailers attributing increased sales due to the Queen’s Jubilee celebrations.

- Automotive fuel sales volumes fell by 4.3% in June, down from growth of 0.8% in May, with sales volumes 7.6% below their pre-pandemic February 2020 level. The ONS retail sales publication suggests that record high prices of petrol and diesel was reducing the volume of sales.

- Online retail as a proportion of all retail sales, fell to 25.3% (down from 26.4% in May). This continues the wider downward trend since its peak in February 2021 (37.4%) and is at its lowest proportion since March 2020 (22.8%).

Household Savings and Consumer Credit

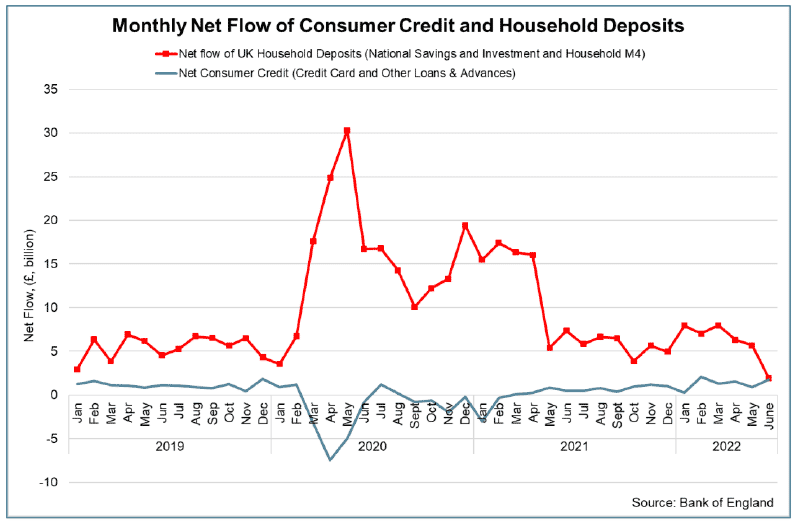

- At an aggregate level, households increased their levels of savings during the pandemic and reduced net credit levels, due to a reduction in expenditure coupled with a rise in disposable income through the retention of earnings.

- Data from the Quarterly National Accounts show that household savings in Scotland in the first three months of 2022 had fallen to 6.4% from their peak of 26.4% in 2020 quarter 2 during the pandemic, meaning they had returned levels similar to before the pandemic levels.[17] Data from the Bank of England data show a similar pattern and provides insights at an aggregate level of how savings and consumer credit flows have evolved in the latest months as economic activity has recovered alongside a rise in inflationary pressures.

- At an aggregate level, net flows from UK households into deposit-like accounts fell significantly in June. Net inflows eased to £1.9 billion, down from £5.6 billion in May and below the average monthly net flow of £4.7 billion during the 12-month pre-pandemic period up to February 2020.[18]

- Alongside this, net consumer credit fell significantly during the pandemic, however started to grow over the course of 2021. In June, consumers’ borrowed an additional £1.8 billion, following £0.8 billion of borrowing in May. This is above the pre-pandemic average up to February 2020 of £1.0 billion. The annual growth rate for all consumer credit increased to 6.5% in June; the highest rate since May 2019.

Inflation

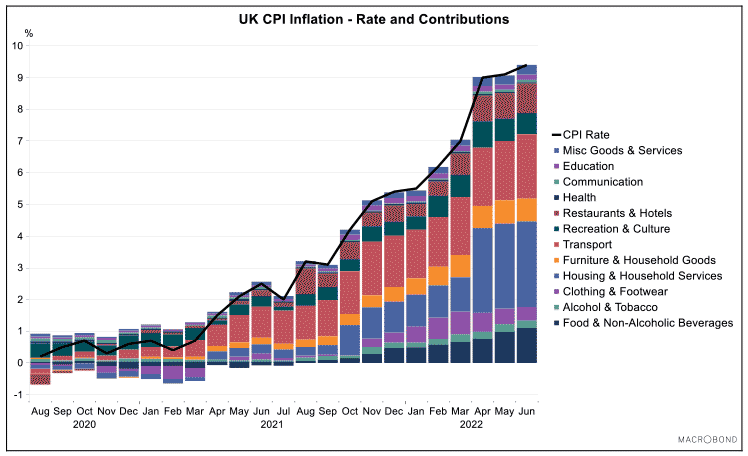

- UK CPI inflation rose to 9.4% in June 2022, up from 9.1% in May and has risen to its highest rate since 1982.[19] Inflation rates have also continued to rise in the US (8.6%) and in the Eurozone (8.6%), in part reflecting rising energy prices over the past year.

- In June, UK consumer prices rose over the year across almost all goods and services monitored. Most notably there was large increases in electricity, gas and fuel prices (+70.2%), transport (+14.9%), furniture (+14.9) and in food and non-alcoholic beverages (+9.8%).

- Looking ahead, the Bank of England forecast inflation to rise to over 11% in October 2022, reflecting higher food, core goods and services price inflation and a prospective large increase in the Ofgem price cap, which are expected to intensify cost of living challenges.

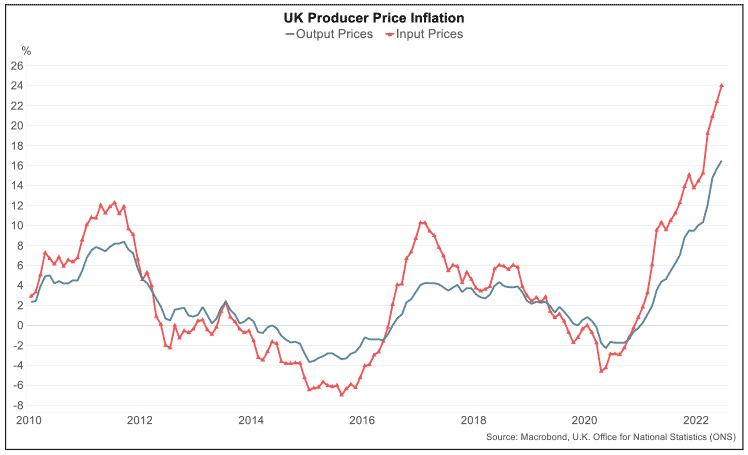

- The pass through of higher energy and material prices from producers to consumers is an important aspect of this. Producer price inflation (changes in the prices of goods bought and sold by UK manufacturers, including price indices of materials and fuels purchased and factory gate prices) has risen over the past year and has remained elevated. In June input price inflation rose to 24.0% (up from 22.4% in May) and is at its highest rate since records began in January 1985, while output price inflation was 16.4% (up from 15.8% in April) its highest rate since September 1977.[20]

- In response to the further rise in underlying inflationary pressures for the year ahead, the Bank of England’s Monetary Policy Committee (MPC) increased the Bank Rate by 0.25 percentage points to 1.25% in June; its fifth consecutive rate rise since December and up from 0.1% over this period.[21]

Contact

Email: OCEABusiness@gov.scot