Publication - Research and analysis

Monthly economic brief: July 2022

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Labour Market

Scotland’s labour market remains tight with continuing high vacancy rates and declining staff availability.

Official labour market statistics, payrolled employment and claimant count

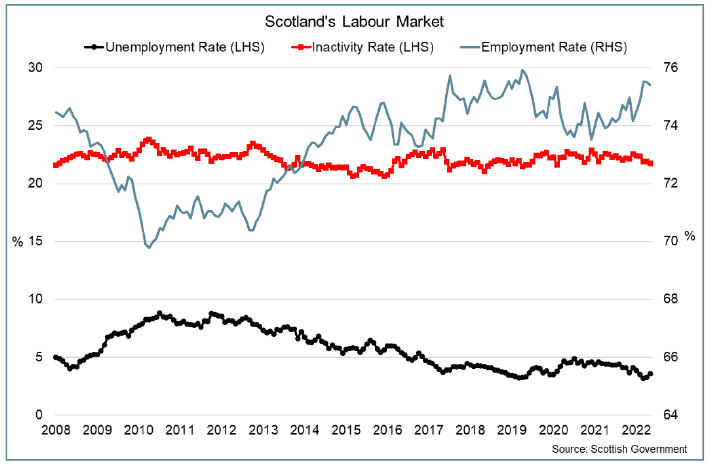

- The latest labour market statistics for March to May 2022 in Scotland show there were 2.7 million people in employment (rate of 75.4%, up 1.4 percentage points over the year), 99,000 people unemployed (rate of 3.5%, down 0.9 percentage points) and 748,000 people economically inactive (rate of 21.8%, down 0.8 percentage points).[6]

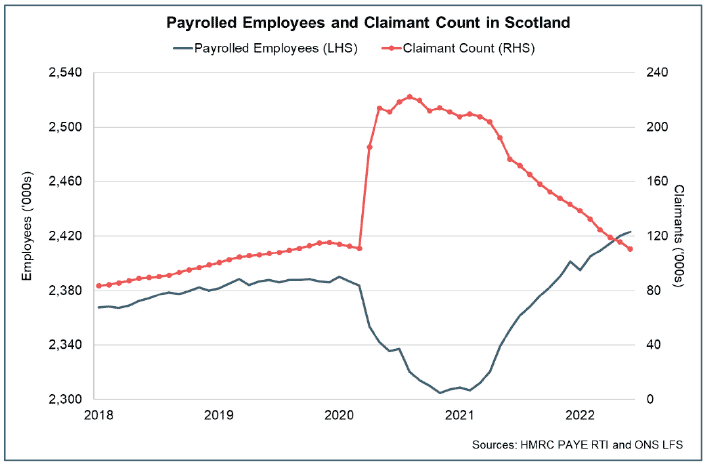

- Pay As You Earn (PAYE) Real Time Information estimates indicate the number of payrolled employees in Scotland continued to increase in June, rising by 3,000 over the month to 2.42 million, 37,000 more than the pre-pandemic level in February 2020. The rate of growth over the month eased to 0.1%, and is slightly below the the average monthly rate of growth over the past year (0.3%).[7]

- Scotland’s Claimant Count (the number of claimants of Job Seekers Allowance and claimants of Universal Credit claiming principally for the reason of being unemployed) also continued its downward trend in May, falling 4.4% over the month to 110,600; a claimant count rate of 3.6%.

- Overall, the claimant count has fallen 50% from its peak in August 2020 and is 1,900 claimants below its pre-pandemic level in February 2020.[8]

Demand and supply of staff

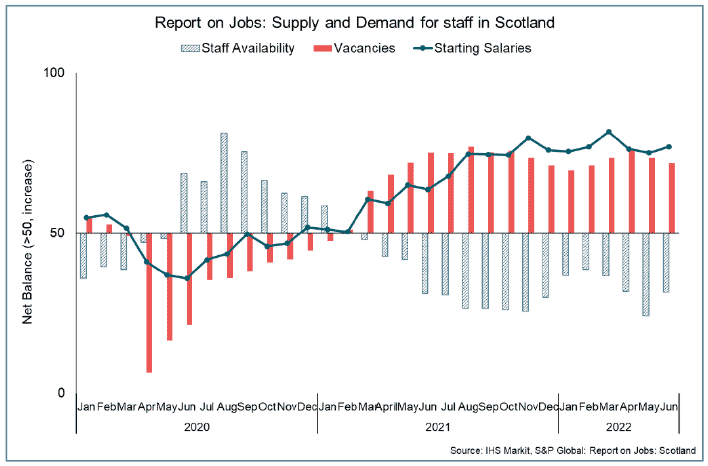

- Business surveys signalled that labour market tightness continued to persist in June with high vacancy rates and falling candidate availability.

- The latest Report on Jobs signalled that overall demand for staff (vacancies) continued to grow in June (71.9) and although the pace of growth slowed over the month, it remained high compared to historical standards.[9]

- Supply side challenges in the labour market have also continued with candidate availability (labour supply) continuing to fall. The rate of contraction in June eased slightly with ongoing skill shortages, the tight labour market and Brexit all linked to the decrease.

- More recent online vacancies data also signal that strong demand for staff continued throughout July, with weekly online job vacancies 33% higher than in February 2020.[10]

- The strength in demand for staff, coupled with low unemployment, falls in candidate availability and challenges in recruiting the necessary staff, meant upward pressure on starting salaries remained elevated in June, with the report on jobs overall pay index rising the month and remaining elevated.

- Labour shortages continue to affect a range of sectors with 38% off all businesses experiencing a shortage of workers in June. The overall share has picked-up since the start of the year and remains most notable in accommodation and food services (44%), construction (43%), and the arts, entertainment and recreation (43%) sectors.[11]

Earnings

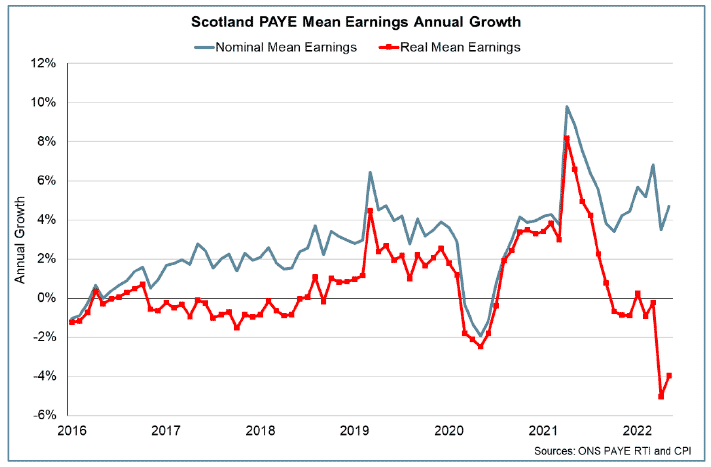

- Nominal mean earnings annual growth has stabalised slightly after a sharp fall during the pandemic and then a strong rebound, in part driven by workers moving into and then out of furlough.[12]

- Latest data show mean monthly nominal pay grew 0.1% over the month in May (UK: -0.9%), and grew 4.7% (UK: 5.3%) annually to £2,601 (UK: £2,842).[13]

- The pace of annual nominal earnings growth in May was similar to annual growth rates in 2019. However, adjusting for inflation, which rose to 9.1% in May, real mean earnings fell 4.0% on an annual basis, the fourth consecutive month of negative annual growth.

Contact

Email: OCEABusiness@gov.scot