Publication - Research and analysis

Monthly economic brief: July 2022

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Output

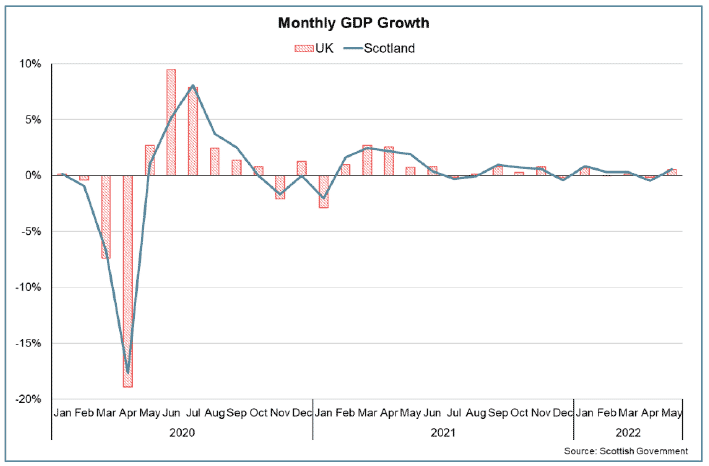

Scottish GDP growth picked up in May, however has generally slowed from the first quarter with growth of just 0.1% over April and May.

- In May, Scottish output grew by 0.6% (UK: 0.5%), and GDP is now 1.1% above its pre-pandemic level in February 2020 (UK: 1.7%).[1]

- Although the economy returned to growth in May after the fall in April, over the two months there has been cumulative growth of just 0.1%.

- In the three months to May, GDP is estimated to have grown by 0.7% compared to the previous three month period, with the pace of growth slowing compared to the first quarter of the year. This slowing of growth is consistent with the results for the UK as a whole.

- At a sectoral level, GDP growth was broad based in May. Services output grew by 0.4%, while construction grew by 1.7% and production grew by 1.1%.

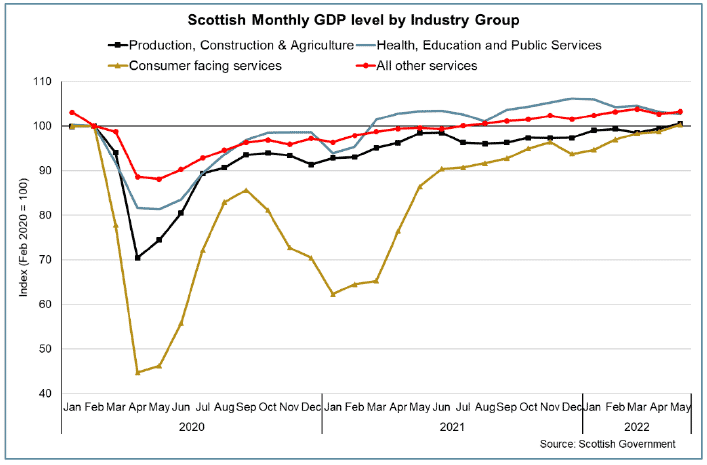

- Within the services sector, output in consumer facing services grew by 1.6% and has surpassed the pre-pandemic level of February 2020 for the first time. Growth in sectors such as professional, scientific and technical services (+4.2%) outweighed the slowing in retail (+0.2%) and hospitality growth (0.5%) observed over recent months. Health, education and public services output fell by 0.4%, and output in all other services grew by 0.5%.

- Within the production sector, growth over the month was largely driven by growth of 8.9% in the electricity and gas supply industry due to record levels of wind power generation during May, while manufacturing output fell by 0.3%, its fourth consecutive monthly decline in output. Overall output in production, construction and agriculture grew by 1.1% compared to the previous month.

- Recovery in output back to pre-pandemic levels continues to vary by sector. Output in the production, construction and agriculture group is 0.6% above its pre-pandemic level, however this is driven by the construction sector (4.7 above) while production output remains 1.2% below. In the services sector, despite contracting in the most recent months (mostly due to the reductions in NHS test and trace activities throughout April), health, education and public services remains 2.7% above while consumer facing services is 0.3% above and output in all other services was 3.2% above its pre-pandemic level.

Contact

Email: OCEABusiness@gov.scot